Quick Answer

Choose a plan based on control and activation terms, not price alone. The best medical evacuation insurance setup for remote travelers is the one whose wording matches your real scenario: some products move you to local adequate care, while some membership programs focus on return to a chosen home hospital after stated triggers. Confirm who authorizes transport, what event activates benefits, and whether self-arranged transport is unpaid.

The Medevac Decision Matrix: Prioritizing Control Over Cost#

When you choose a medevac plan, decide control first and price second. The key questions are who approves transport, where you can be sent, and how the handoff is managed. In a real emergency, that operating model can matter more than small premium differences.

For long stays, this is not just a rescue decision. It is also a continuity decision. Some insurance-style benefits focus on transport to the nearest appropriate facility. Some membership-style programs focus on returning you to a hospital of choice once their trigger is met.

| Decision point | Medical evacuation insurance | Transport membership |

|---|---|---|

| Destination control | Often to the nearest appropriate facility | May prioritize your hospital of choice at home, based on membership terms |

| Medical necessity standard | Often requires transport to be medically necessary | Varies by product; do not assume necessity is waived |

| Activation trigger | Emergency event plus assistance-team coordination/authorization may be required | Can require hospitalization plus distance (for example, 150 miles or more from home or 100+ miles from home in some products) |

| Exclusions | May exclude preexisting conditions or adventure activities | Rules still apply; eligibility and covered scenarios are product-specific |

| Bedside-to-bedside logistics | Often coordinated through insurer assistance channels, sometimes with advance contact requirements | Some offerings describe point-of-illness rescue to nearest facility, with possible later repatriation |

| Family/support-network coordination | Some plans include bedside-relative transport (example trigger: hospitalization more than 48 hours) | May help family coordination if transport returns you closer to your support network; verify explicit family benefits |

What this means in practice#

If your priority is rapid transport to competent care, insurance-style evacuation can fit that job. If your priority is getting back into your own provider network after stabilization, a membership-style transport program can be a better fit.

The cost risk is material either way. Published figures range from $20,000 to $200,000, with other sources citing higher ceilings, and remote-area evacuation can exceed $100,000. Treat those as broad ranges, not guaranteed numbers.

Also keep the contract type straight. At least one major provider states its program is a membership, not insurance, and does not reimburse member-incurred expenses.

The two checks that prevent most failures#

- Verify the exact policy or membership wording before purchase: who authorizes transport, where you can be sent, and what event activates benefits. If anything is unclear, mark the transport trigger as "Current transport trigger pending official verification" or the eligibility wording as "Current eligibility wording pending official verification."

- Confirm the activation workflow. Some benefits require advance coordination through the assistance team, and self-arranged transport may not be paid or reimbursed.

Quick decision matrix#

| Your profile | Likely fit | Why |

|---|---|---|

| Short trips, strong local care | Insurance may be sufficient | You are optimizing for emergency transfer to adequate care |

| Long stays, uneven regional care quality | Membership may be stronger | Destination control and continuity can matter more |

| Low risk tolerance + high work dependency | Sometimes both | One layer handles emergency evacuation logistics; one layer can support return to known care |

| Adventure activities or preexisting-condition concerns | Verify before buying either | Exclusions and activity tiers can determine whether coverage works at all |

Practical rule: if you only need emergency movement to appropriate care, insurance may be enough. If you need destination control and a return to your own clinical network, membership deserves a serious look. Related: A Deep Dive into FinCEN's Beneficial Ownership Information (BOI) Reporting.

Architecting Your Resilience: The 3-Layer Safety Net#

Once you know what kind of transport control you want, build the rest of the plan around it. For a long stay, it is safer to treat treatment access, transport logistics, and wider disruption support as separate decisions unless one contract clearly states it covers all three.

Plan in three separate layers: who pays for care where you are, who moves you if care must change, and who manages non-medical disruption. Use a simple rule: each layer has one job. If a benefit sounds broad, treat it as unconfirmed until the contract language proves otherwise.

| Layer | Primary function | Typical trigger | Owner or contact path | Common exclusions or limits to verify | Failure risk if missing |

|---|---|---|---|---|---|

| Base health cover | Supports payment/authorization for treatment where you are | Illness or injury needing care | Plan support line, administrator, or provider support desk | Coverage scope and authorization/documentation requirements vary by plan | Care can be delayed or become costly even when services exist |

| Transport cover | Coordinates approved medical movement when transfer is authorized | Medical need plus plan/program authorization | Assistance or transport coordination line | Authorization, timing, destination, and reimbursement terms are plan-specific | Transfer can be delayed or unavailable when needed |

| Crisis or security support | Handles non-medical disruptions that affect care continuity | Disaster, infrastructure/communications failure, or security disruption | Crisis hotline, security desk, employer assistance contact, or local emergency channels | Response scope and operating limits vary; confirm escalation path and service hours | A manageable medical issue can escalate into a logistics failure |

Layer 1#

Role: pay for treatment where the event happens. Includes: covered medical care as defined by your plan. Does not include: guaranteed relocation or broader disruption response unless explicitly included.

This layer comes first because care continuity depends on more than the clinic. Power, water, IT, communications, supply chains, and workforce availability can all affect service delivery. Before departure, confirm your authorization route and claim-document checklist.

Layer 2#

Role: manage transfer logistics when care needs to change. Includes: coordination workflow and covered transport arrangements under your plan terms when authorized. Does not include: benefits that are not explicitly written in the contract.

Keep a process-first mindset. Confirm who authorizes transfer, how requests are made, and what happens when advance notice is not possible. Public transportation-access policy shows why process matters operationally: guidance discusses long-distance trips and extended waits, conditional obligations with prior authorization, and urgent transport exceptions to advance notice. Those public-program rules are not the same as private international medevac products.

Layer 3#

Role: manage disruptions a medical policy alone cannot solve. Includes: support when travel, communications, or infrastructure conditions break continuity. Does not include: routine medical-claims payment unless expressly bundled.

Keep this layer separate because infrastructure shocks can break care continuity even when the underlying medical issue is treatable. Resilience planning is a cross-sector responsibility, so this layer should connect medical planning with practical continuity support.

A practical build order#

For long-stay planning, one practical sequence is to start with treatment access, then confirm transport workflow, then add disruption support.

- Choose base health cover first. If local treatment cannot be authorized or paid smoothly, everything downstream slows.

- Choose transport cover second. Verify request methods, authorization steps, and timing expectations in writing before you rely on it.

- Add crisis support third when your destination or work profile warrants it. This layer helps protect continuity when non-medical disruption causes the failure.

Across all three layers, apply the same test. If you cannot name the activation trigger, the contact path, and the required documentation, the safety net is not ready yet. You might also find this useful: The Best Email Encryption Tools for Freelancers.

The Business Imperative: Why Standard 'Travel Insurance' Fails#

Standard travel coverage can help with trip disruption, but it often leaves the transport piece weak or undefined. For a remote professional, this is a continuity decision: who pays, who coordinates, and where you are taken when you cannot manage logistics yourself.

CDC guidance treats travel disruption, travel health, and medical evacuation as separate coverages, not interchangeable ones. When you compare options, prioritize operating terms over marketing language: payment flow, coordination authority, destination rules, and activation requirements.

For budgeting, avoid stale price charts. CDC notes evacuation from a remote area can cost more than $100,000. Costs can vary by route and clinical context, so verify current ranges before relying on any estimate.

| Product type | What it usually pays for | Who coordinates transport | Destination control | Claim friction | What falls on you |

|---|---|---|---|---|---|

| Trip-cancellation focused policy | Prepaid trip losses when plans change | Usually no medical transport coordination | Not applicable | Policy claim terms vary; medical transport is typically outside scope | You still need separate medical and transport cover |

| Travel policy with an evacuation benefit | Emergency transport under policy terms | Insurer or assistance team after authorization | Often nearest adequate facility first, then home if warranted | Medical-necessity review and approval rules under policy terms | You must call the assistance line quickly and follow process |

| Credit-card travel assistance or evacuation benefit | Sometimes referral-only services; some cards include capped evacuation benefits | Benefit administrator | Commonly nearest hospital or medical facility, not hospital-of-choice | May require enrollment, advance approval, card-use conditions, and formal claims with no reimbursement guarantee | You must know eligibility rules before departure and prove them during the event |

| Hospital-of-choice transport membership model | Transport service itself, subject to membership terms | Membership or transport team | In marketed examples, transport to a chosen home-country hospital; product-specific, not universal | Trigger rules still apply; example language includes hospitalization 150 miles or more from home | You must verify destination rights, exclusions, and activation details in writing |

False sense of coverage#

Many coverage gaps start with a category mismatch. The U.S. State Department says trip-cancellation insurance usually does not pay overseas medical costs. CDC says credit-card benefits are not a substitute for travel disruption, travel health, or medical evacuation insurance.

| Checkpoint | What to confirm |

|---|---|

| Direct payment | Direct payment to hospitals versus reimbursement |

| 24-hour support | Availability of a 24-hour physician support center |

| Destination rule | Nearest adequate facility versus home-country hospital |

| Enrollment | Enrollment and advance-approval requirements |

Card benefits are especially easy to overread. Visa Signature emergency services language describes assistance and referral support and says you are responsible for actual service costs. Chase Sapphire Reserve advertises emergency evacuation and transportation up to $100,000. But transport must be arranged and approved in advance by the benefit administrator, and it is generally to the nearest hospital or medical facility.

Before departure, confirm these points in your actual policy or benefit guide:

- Direct payment to hospitals versus reimbursement.

- Availability of a 24-hour physician support center.

- Destination rule: nearest adequate facility versus home-country hospital.

- Enrollment and advance-approval requirements.

Decision checkpoint#

Use this rule of thumb when you decide:

- Standard travel coverage may be enough if your trip is short, you already have reliable overseas medical coverage, and you accept transfer to the nearest adequate facility.

- Dedicated medevac cover is often worth adding if you are on a long stay, working from a remote or limited-care location, or you need a realistic path back to your home medical network.

- Keep activation documents accessible: policy certificate or benefits guide, proof of enrollment if required, emergency assistance numbers, and your policy, member, or card details.

If you want a deeper dive, read The Crypto Cautionary Tale: Why Freelancers Should Be Wary of Crypto Payments.

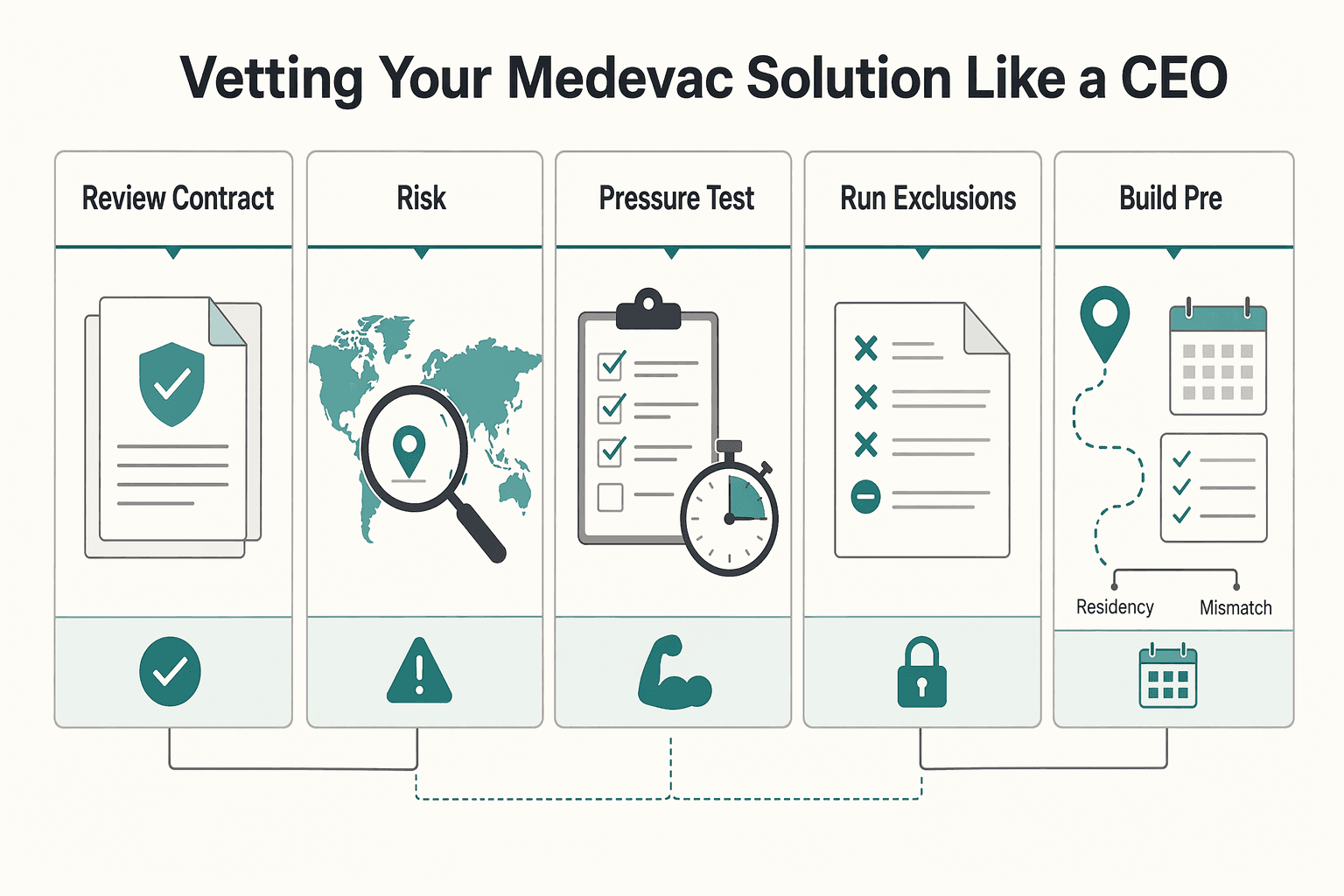

Due Diligence: Vetting Your Medevac Solution Like a CEO#

The purchase decision is only half the work. Pressure-test the contract and activation path before you rely on the plan. Use a two-pass checklist: verify contract terms before you buy, then re-verify activation details before departure.

| Step | What to review | Key details |

|---|---|---|

| Review the contract first | Description of coverage | Confirm medical necessity, nearest adequate facility, pre-existing-condition language, excluded activities, distance-from-home minimums, and trip-length limits |

| Match coverage structure to your real risk | Risk method | Use destination profile, transport complexity, and possible out-of-pocket exposure; recheck trip-length caps in the certificate |

| Pressure-test pre-existing-condition wording in writing | Provider answers | Ask what pre-existing-condition expenses are excluded, whether any limited carve-out is available, and where the terms are defined |

| Run an exclusions fit test against your actual routine abroad | Actual routine abroad | Check prohibited activities, distance-from-home minimums, and whether non-medical evacuation is included or requires an added security upgrade |

| Build a pre-departure readiness file for your family or backup contact | Shared file | Include policy certificate or membership confirmation, assistance numbers, passport copy, itinerary or local address, and written authorization or contact instructions |

-

Review the contract first. Start with the description of coverage, not the sales page, because definitions, limitations, and exclusions are what matter at claim time. In the policy wording, confirm these exact terms: medical necessity, nearest adequate facility, pre-existing-condition language, excluded activities, distance-from-home minimums, and trip-length limits.

-

Match coverage structure to your real risk, not a headline limit. A higher limit is not enough if destination rules or approval triggers do not fit how you travel. Use a risk method: destination profile, transport complexity, and possible out-of-pocket exposure if part of transport falls outside terms. Keep the coverage benchmark marked "Current coverage benchmark pending official verification" until official policy wording supports it. If you are on long stays, recheck trip-length caps in the certificate.

-

Pressure-test pre-existing-condition wording in writing. Treat this as a denial-risk checkpoint. Some wording excludes expenses related to pre-existing conditions, while one cited example includes an Acute Onset of a Pre-existing Condition carve-out for travelers under age 80. Ask the provider to answer, in writing:

- What pre-existing-condition expenses are excluded under this plan? - Is any limited carve-out available (such as Acute Onset), and what conditions apply? - Where in the description of coverage are these terms defined?

-

Run an exclusions fit test against your actual routine abroad. Check whether your real behavior is covered, especially prohibited activities and any distance-from-home minimums. One provider comparison says some companies refuse service for injuries tied to prohibited activities. Also separate medical evacuation from non-medical crisis evacuation, since non-medical support may require an added security upgrade. For conflict or unrest scenarios, verify whether non-medical evacuation is included or requires that upgrade.

-

Build a pre-departure readiness file for your family or backup contact. This is about reducing burden and making activation easier. Share one file with the person who would act for you, including: policy certificate or membership confirmation, assistance numbers, passport copy, itinerary or local address, and written authorization or contact instructions for who can speak with the assistance team. Recheck distance-from-home triggers before each major leg, since eligibility can depend on where you are when the event happens.

For a step-by-step walkthrough, see The Best Travel Insurance with Electronics Coverage for Remote Workers.

After you shortlist providers, use this relocation reference to cross-check destination admin requirements before you lock your emergency plan. See Visa Cheatsheet for Digital Nomads.

Conclusion: Your Pre-Deployment Medevac Checklist#

The goal is straightforward: establish a documented pre-departure plan with clear roles and decision points. Use this as a pre-departure operations check, not a last-minute scramble. Before you leave, complete readiness documentation, assign responsibilities, and confirm the plan can adapt if conditions change. Do not depart until every item is confirmed, documented, and shared with your designated emergency contact.

| Checklist area | Question | What to keep documented |

|---|---|---|

| Risk context | Have you documented destination hazards, local care constraints, and transport gaps before finalizing your plan? | A usable risk baseline |

| Control preference | Have you confirmed in your plan documents who is authorized to make transport decisions? | The certificate PDF and written confirmation |

| Coverage verification | Have you kept coverage details marked "Current coverage details pending official verification" until they can be tied to your route, remoteness, and transport complexity? | The verified details, issue date, and exact document name in one file |

| Exclusions and eligibility | Have you checked full wording for exclusions, eligibility limits, waiting periods, and trip-status rules for your actual scenario? | The relevant sections you validated; if terms are unclear, mark them as unknown |

| Provider confirmation workflow | Have you confirmed who calls first, what event triggers transport coordination, and what documents you and your emergency contact must have ready? | Those documents organized in a shared location and available offline |

| Layer 1 and Layer 2 handoff | Have you documented which arrangement pays for treatment (Layer 1) and which arranges transport (Layer 2), including any authorization or record-sharing handoff? | The handoff steps in plain language and any unresolved ownership |

- Risk context: Have you documented destination hazards, local care constraints, and transport gaps before finalizing your plan? If not, you are choosing without a usable risk baseline.

- Control preference: Have you confirmed in your plan documents who is authorized to make transport decisions? Save the certificate PDF and written confirmation so your emergency contact can act on clear terms.

- Coverage verification: Have you kept coverage details marked "Current coverage details pending official verification" until they can be tied to your route, remoteness, and transport complexity? Record the verified details, issue date, and exact document name in one file; if anything is unclear, mark it as unknown until verified.

- Exclusions and eligibility: Have you checked full wording for exclusions, eligibility limits, waiting periods, and trip-status rules for your actual scenario? Review the full certificate text and note the relevant sections you validated; if terms are unclear, mark them as unknown.

- Provider confirmation workflow: Have you confirmed who calls first, what event triggers transport coordination, and what documents you and your emergency contact must have ready? Keep those documents organized in a shared location and available offline.

- Layer 1 and Layer 2 handoff: Have you documented which arrangement pays for treatment (Layer 1) and which arranges transport (Layer 2), including any authorization or record-sharing handoff? Write the handoff steps in plain language so there is no delay during escalation, and flag unresolved ownership before departure.

We covered this in detail in The Best Business Travel Insurance for Digital Nomads and Executives. Before departure, centralize your planning workflow so documentation, payment operations, and tax/admin prep stay in one place: Explore Gruv Tools.

Frequently Asked Questions

Is medevac coverage worth it for a long stay or remote assignment?

Yes, if an air-ambulance bill would be financially disruptive for you. U.S. guidance says evacuation back to the United States can run $20,000 to $200,000, and you should not assume U.S. government payment abroad or Medicare coverage outside the U.S. Action: compare your health plan, employer plan, and card benefits for evacuation exclusions, then keep your certificate and emergency assistance number in your readiness file.

How much evacuation coverage is enough?

There is no single number that works for everyone, because wording controls outcomes as much as limits. You need to confirm transport triggers, destination rules, and whether the assistance company must coordinate transport in advance, because some plans require advance coordination for evacuation transport benefits. Action: leave the coverage range marked "Current coverage range pending official verification" until the certificate confirms it, then verify "medical necessity," "nearest appropriate facility," and coordination requirements.

Can you buy coverage after you have already left home?

Sometimes, but treat it as provider-specific rather than guaranteed. Some products allow post-departure purchase, and at least one example applies a 72-hour waiting period before full coverage starts when bought during travel. Action: confirm eligibility for your residence and destination pair, keep the provider waiting-period rule marked "Current provider waiting-period rule pending official verification" until the official certificate or purchase terms verify it, and save your purchase timestamp and certificate PDF.

Does it cover COVID-19 or other epidemic-related illness?

Only if your plan wording includes epidemic-related covered reasons or does not exclude them. At least one current plan explicitly lists epidemic-related reasons tied to emergency medical care and emergency transportation, but that does not automatically carry to other plans. Action: search your policy for “epidemic,” “pandemic,” “emergency transportation,” and exclusions, then get written confirmation from support.

What is the difference between medical evacuation and repatriation of remains?

They are separate benefits with different triggers and documentation. Medical evacuation applies when you need transport for treatment, while repatriation of remains applies after death and may have its own benefit line and limit. Action: verify both benefit sections separately, confirm whether coordination rules differ, and keep passport and emergency-contact documents accessible for your backup contact.

Should you buy insurance or a transport membership if you want more control over where you go?

If destination control is your priority, compare the wording closely. Many insurance plans describe transport to the nearest appropriate facility, while some memberships market transport to your hospital of choice after trigger conditions are met. Those conditions can include inpatient status and minimum distance from home, for example 150 miles in one case and 100+ miles in another, so control depends on whether your scenario fits the terms. Action: run a side-by-side check of trigger condition, distance rule, inpatient requirement, and destination language before you choose.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- aspr.hhs.gov/HealthCareReadiness/guidance/Documents/Healt...trusted

- cdc.gov/yellow-book/hcp/health-care-abroad/travel-in...trusted

- cdc.gov/niosh/docs/2025-107/pdfs/2025-107.pdftrusted

- cms.gov/regulations-and-guidance/guidance/manuals/do...trusted

- fema.gov/sites/default/files/documents/fema_npd_devel...trusted

- fema.gov/sites/default/files/documents/fema_national-...trusted

- medicaid.gov/federal-policy-guidance/downloads/smd23006.pdftrusted

- medicaid.ncdhhs.gov/nc-medicaid-managed-care-non-emergency-medic...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Freelance Crypto Payments That Protect Cashflow and Reduce Disputes

Crypto payments make sense only when they improve how reliably you get paid after you plan conversion, compliance, and recordkeeping up front. They can reduce friction in some international setups where traditional platforms add fees, restrictions, or extra steps. They also move risk onto conversion timing, exchange-fee exposure, and documentation quality, so use a simple acceptance test before you agree:

Beneficial Ownership Reporting in 2026 for FinCEN BOI Decisions

Use this as an execution guide, not a legal memo. Your job is to make a current BOI decision, document why you made it, and avoid cleanup later. The outcome is straightforward: confirm whether your entity is in scope, prepare what you need if it is, and keep dated proof of the basis you used.

The Best Email Encryption Tools for Freelancers

You can choose an email encryption route, test it in a real exchange, and keep contract and invoice threads moving.