Quick Answer

Small businesses should choose HRIS, payroll, EOR, and MoR tools by risk, not by feature count. Use a payroll provider when paying people correctly is the main compliance job, add an HRIS when you have employees and need centralized records, consider an EOR for cross-border hiring arrangements, and use an MoR only for documented billing needs after you verify contract responsibilities in writing.

Pillar 1: How Do You Build a Bulletproof Revenue System?#

Protecting revenue comes down to sequence. First, decide who carries payment and compliance liability. Next, make your invoices hard to reject. Then separate your money rails and lock terms before any work starts. Get that order right and many avoidable cash-flow problems show up earlier, when they are still easier to fix.

| Element | Before kickoff | Risk named in article |

|---|---|---|

| Signed scope | Part of the minimum sequence | Work starts after a verbal yes |

| Billing trigger | Part of the minimum sequence | Argument over milestone approval |

| Invoice schedule | Part of the minimum sequence | Argument over invoice timing |

| Late-payment terms | Part of the minimum sequence | If it is fuzzy, you are relying on memory and goodwill |

| Escalation path | Part of the minimum sequence | Unclear who inside the client can release payment |

-

Choose the right commercial model. An Employer of Record (EOR) legally employs talent on behalf of a company. That matters if a client wants to hire you as an employee in their market. A Merchant of Record (MoR) does a different job. It takes legal and financial liability for payment processing. If you are a solo operator selling services across borders, an MoR can help when a client is uneasy about paying a foreign contractor and you want the platform, not the client, to carry more of the payment-compliance burden. It lowers friction, but it is not the same as guaranteed payment.

-

Make invoices difficult to bounce. A rejected invoice is an immediate threat to cash flow, so build a pre-send check rather than fixing errors after accounts payable pushes back. Use a checklist to confirm the legal and tax details required for that specific deal are complete before sending.

In the EU B2B reverse-charge example, the invoice must state "reverse charge" and include both VAT numbers. Before you send it, confirm the tax treatment for the client's jurisdiction, then run an EU VIES check when a VAT ID is involved. That step can prevent an ordinary payment delay.

| Payment route | Fee transparency check | FX handling check | Payout timing check | Reconciliation check |

|---|---|---|---|---|

| Local business bank transfer | Confirm all transfer and receiving fees upfront | Confirm how non-local currency is handled | Confirm expected settlement window with your bank | Confirm invoice references map cleanly to statement lines |

| Payment wallet or processor balance | Confirm fee breakdown and net payout logic | Confirm where conversion happens and what rate source is used | Confirm provider processing windows | Confirm payout reports include fee and net details |

| Multi-currency business account | Confirm account-level and transfer fees by currency | Confirm hold/convert options and quote expiry rules | Confirm timing by currency corridor | Confirm ledger/export views by currency |

| MoR payout | Confirm client-facing charges and payout-side deductions | Confirm who controls conversion and rate visibility | Confirm payout schedule and delay conditions | Confirm export detail level for payout reconciliation |

-

Separate business and personal money early. Do this before volume increases, not after. Use a dedicated business account and keep client receipts, tax reserves, and personal spending apart. Once you start billing internationally, mixed accounts make tax tracking and reconciliation much harder later. A practical default is to route all income into business-only accounts, then automatically move 25-30% into a tax reserve if that fits your situation.

-

Go contract-first, not invoice-first. Your minimum sequence is simple: signed scope, billing trigger, invoice schedule, late-payment terms, and an escalation path before kickoff. If any part is fuzzy, you are relying on memory and goodwill. A common failure mode is familiar: work starts after a verbal yes, then the real argument begins over milestone approval, invoice timing, or who inside the client can release payment.

Revenue system baseline you can implement this week:

- Pick one default path for new clients: direct invoice, multi-currency account, or MoR for higher-friction cross-border work.

- Build one invoice template with legal fields and a tax-treatment check.

- Add one pre-send verification step: client legal name and VAT validation in VIES where relevant.

- Keep operating cash and tax reserves in business-only accounts.

- Put the contract and invoice schedule in the same intake step so work never starts unsigned.

Once that baseline is in place, the next job is compliance: making sure your entity, tax position, and worker classification actually match how money is moving.

You might also find this useful: A Guide to Understanding Your Employee Benefits Package.

Pillar 2: What Does Ironclad Compliance Actually Look Like for a Solo Professional?#

Compliance is easiest to manage when you treat it as a monthly control routine instead of a year-end scramble. Keep a compact evidence pack, review the same triggers each month, and flag any legal rule that still needs jurisdiction-specific confirmation before you rely on it.

- Use a documented payroll-to-distribution workflow for S-Corp operations.

If you run a U.S. S-Corp, keep payroll and owner distributions as separate entries, with separate support. A practical sequence is: run payroll, confirm wage payment, then book the distribution. Keep a standing note for any current legal requirements around compensation, officer treatment, and state registration that still need advisor confirmation.

Your monthly check is straightforward: match payroll records to bank movement, then confirm distributions were not recorded as wage substitutes. Keep records in distinct buckets so wages, draws, and reimbursements do not blur together.

- Set benefits and retirement workflows only after funding mechanics are clear.

Pick the plan only after you decide how contributions will actually move: through payroll, owner transfer, or both. Then confirm your tooling can produce a clean contribution trail you can reconcile later.

Keep a minimal audit trail each month: the plan setup record, provider confirmations, and a dated contribution log tied to the funding event. For plan limits, deadlines, or eligibility, do not guess; keep those items flagged for provider or advisor confirmation.

- Track residency and sourcing with a repeatable log.

Do a light update monthly and a deeper review quarterly. At minimum, log where you stayed, where you worked, and your workdays by jurisdiction.

For California, if you lived inside or outside the state during the year, you may be a part-year resident. Nonresidents are taxed on California-source taxable income, and the FTB example uses CA Workdays / Total Workdays = % Ratio for allocation. Escalate to a specialist if your work pattern changes materially or you may be nearing a residency or sourcing threshold that needs current confirmation.

- Build FBAR controls around maximum values, not year-end balances.

The FBAR trigger is $10,000 at any time during the calendar year (single-account maximum or aggregate maximum). Track each account's yearly high-water value, not just the closing balance.

Record values in U.S. dollars and round up to the next whole dollar (for example, $15,265.25 -> $15,266). Use the Treasury rate for the last day of the calendar year when available; if unavailable, use another verifiable rate and keep the source. If eligible and aggregate maximums cannot be determined, use Item 15a for filers with fewer than 25 accounts. For spouse joint e-filing with one digital signature, complete and retain Form 114a (do not send it to FinCEN).

| Control area | Required trigger | Tracking input | Filing owner | Failure risk |

|---|---|---|---|---|

| S-Corp payroll workflow | Needs current payroll and state-law confirmation | Payroll records, bank wage proof, distribution log | You + payroll/tax advisor | Wage and distribution records become indistinct |

| Benefits/retirement funding | Needs current plan limit, deadline, and eligibility confirmation | Plan setup record, contribution log, provider confirmation | You + plan/payroll provider | Contributions are mis-timed or poorly supported |

| California residency/sourcing | Needs current residency or sourcing threshold confirmation | Stay log, workday log, sourcing workpapers | You + state tax specialist (as needed) | Residency or sourcing position is weak |

| FBAR account controls | $10,000 at any time during the calendar year | Yearly maximum values, statements, FX source, spouse filing record | You or authorized filer | Filing misses, conversion errors, spouse handling errors |

Monthly compliance checkpoint:

- Reconcile payroll records to cash movement, then confirm distributions are separate.

- Confirm planned benefit/retirement funding posted and is documented.

- Update residency and workday logs; refresh California sourcing workpapers if relevant.

- Refresh foreign-account high-water values, FX-rate source notes, and Form 114a retention steps where applicable.

These are also the first controls worth automating in Pillar 3: payroll reminders, statement ingestion, contribution confirmations, and calendar/workday rollups. For a step-by-step walkthrough, see The Best Payroll Services for Small Agencies with US Contractors.

Pillar 3: How Can You Achieve Effortless Automation and Reclaim Your Focus?#

Automation should protect your attention, not add more software. The goal is simple: make sure your Pillar 2 compliance controls run on schedule without living in your head.

1. Pick one system of record and make everything else feed it#

Choose your system of record first, then decide which tools are allowed to write into it: payroll, banking, expense capture, and, if relevant, your MoR or invoicing layer. If you are comparing the best hris software for small business, the practical test is whether it can serve as that record or sync cleanly into it. Keep one required field set consistent across payroll, banking, and expenses: legal entity/person name, transaction date, amount, category, counterparty, and document link or receipt image.

Run a monthly sync check across payroll, bank activity, and expenses to confirm amount, date, and category still match. Watch for silent drift, where one system labels an item as payroll tax and another labels it as owner draw.

| Pattern | Best use | Setup complexity | Reliability | Maintenance load |

|---|---|---|---|---|

| Native integrations | Core records you need every cycle | Low to medium | Typically most stable | Low |

| Workflow tools | Conditional handoffs between apps | Medium | Flexible, but monitor regularly | Medium |

| Manual fallback | High-risk records or known flaky syncs | Low | Depends on your review discipline | Medium to high |

2. Automate cash rules and receipt capture#

Start with the automations that prevent expensive mistakes. Set a rules-based transfer from each incoming payment into a dedicated tax account. A common example is 25-30%, but keep your actual set-aside range flagged for tax-advisor confirmation until you know what applies to you.

Then make receipt handling repeatable: route digital invoices through one intake path, capture paper receipts the same way every time, post them into bookkeeping, and review uncategorized exceptions on a fixed weekly cadence. If a receipt does not match a bank line, leave it flagged for review instead of forcing a guess.

3. Start this week#

- Name your system of record and list the only tools allowed to sync into it.

- Lock your required shared fields so payroll, banking, and expenses stay reconcilable.

- Turn on one automatic tax set-aside transfer tied to incoming payments.

- Set one weekly exception review for uncategorized or unmatched receipts.

- Reconfirm payroll, owner distributions, and contribution records still follow the Pillar 2 compliance controls.

If you want a walkthrough, see How to Use Gusto for Payroll for a Small US-Based Agency.

A Practical Guide: Choosing Tools for Your Personal Operations Stack#

Choose your stack by failure risk, not feature count. Start with the job that can create the biggest operational or compliance problem if it breaks, then add tools around that core.

Use comparison content as input, not as a verdict. One published guide from March 19, 2026 reviewed 10 HR platforms and produced a top five, but it also discloses potential vendor-payment influence. Use it as a shortlist signal, then verify live pricing, export quality, and contract terms in-product before you commit.

Also, do not treat EOR, Contractor of Record, and Merchant of Record as interchangeable. Pick based on the exact responsibilities your agreement assigns, and confirm those responsibilities in writing before rollout.

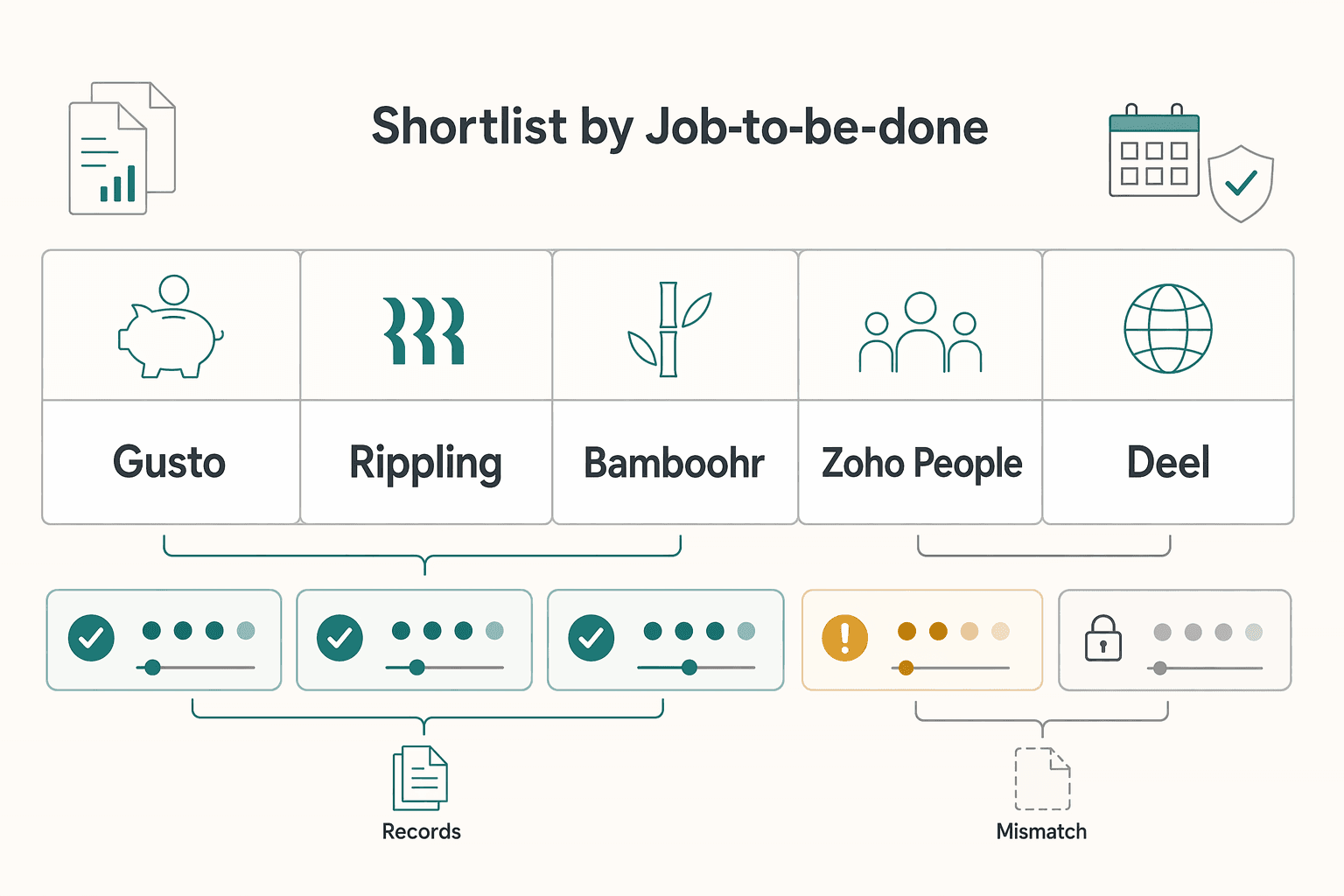

Shortlist by job-to-be-done#

| Tool | Best-fit use case | Core compliance job | Integration depth (verify in trial) | Solo-operator limitation | Ideal business stage |

|---|---|---|---|---|---|

| Gusto | Early employer setup with payroll as the first hard requirement | Payroll workflow reliability | Confirm payroll data reaches accounting and bank reconciliation cleanly | Can be premature if you do not need payroll yet | First payroll event or early employee stage |

| Rippling | Teams prioritizing workflow automation across admin tasks | Operational control as processes expand | Validate your exact approval paths and app handoffs | Easy to overbuy while needs are still simple | When admin handoffs are multiplying |

| BambooHR | Teams needing broader HR records and employee self-service | HR record structure as headcount grows | Check whether core records are covered without adding too many extra tools | Often better once onboarding/policy workflows repeat | As headcount starts to climb |

| Zoho People | Budget-conscious teams formalizing HR basics | Basic HR process standardization | Verify what remains outside scope, especially payroll/finance handoff | Lower cost can miss core risk if payroll is your main issue | Small team formalizing HR admin |

| Deel | Included in your candidate set for cross-border evaluation | Confirm responsibility boundaries in contract | Verify integration depth directly | Source here does not support detailed fit claims | Use only after documented cross-border requirements |

Pricing guardrails from the same March 2026 comparison: Gusto starts at $6/employee + $49 base, Rippling at $8/employee + $40 base, and BambooHR at $10.25/employee. Zoho People is positioned as budget-conscious in that source, but no starting price is supported here.

Decision checklist you can run now#

- Define your risk profile first. If your structure requires payroll, treat it as non-negotiable and keep any current payroll requirement flagged for advisor confirmation.

- Map required workflows. List what has to work now: payroll, onboarding, records, approvals, and document storage.

- Filter by must-have integrations. Drop any option that cannot reliably pass data to your accounting, banking, and document trail.

- Run a limited trial. Test one live scenario with real documents and one approval chain, then save the exports and contract notes.

- Review quarterly. What works at a very small size can break as headcount grows.

If you want a deeper dive, read Value-Based Pricing: A Freelancer's Guide.

The Goal Isn't Software, It's Peace of Mind#

Use this as your final filter: you are not buying the biggest feature set; you are buying tighter control over payroll accuracy, compliance visibility, and day-to-day operations.

| Tool lane | Add when | Check in evaluation |

|---|---|---|

| Payroll engine | Pay accuracy is your biggest risk | Confirm automated tax filing for federal, state, and local taxes |

| Payment layer | Your operational pain is client billing or getting paid across borders | Evaluate cross-border compliance needs and, where relevant, EOR integration |

| Workflow hub (HRIS) | You need a centralized employee data hub to improve accuracy and reduce compliance risk | Check for practical self-service and 24/7 support |

| Decision lens | HRIS-first mindset | Operations-stack mindset |

|---|---|---|

| Starting question | Which platform has the most features? | Which risk hurts most if it fails? |

| Buying trigger | Broad HR scope from day one | A specific job-to-be-done (payroll, billing, or records) |

| Day-to-day result | More configuration, blurred ownership | Clear owners, cleaner execution, fewer surprises |

Keep each tool in its lane:

- Payroll engine: Start here when pay accuracy is your biggest risk. In the demo, confirm automated tax filing for federal, state, and local taxes.

- Payment layer: Add this when your operational pain is client billing or getting paid across borders. For multi-country operations, evaluate cross-border compliance needs and, where relevant, EOR integration.

- Workflow hub (HRIS): Add this when you need a centralized employee data hub to improve accuracy and reduce compliance risk. Check for practical self-service and 24/7 support.

The common failure pattern is operational drift: information gets misplaced, deadlines get missed, and manual admin quietly becomes unreliable. Next step: define your top risks, map one tool to each, and validate the setup with a live scenario before you commit.

We covered a similar evaluation approach in The Best E-Discovery Software for Small Businesses.

Frequently Asked Questions

Do you need an HRIS if you are still a one person business?

Usually no. A full HRIS makes more sense once you have employee records to centralize, deadlines to track, and repeat HR tasks that should not live in spreadsheets and inboxes. If it is just you, start with the tool that handles your real exposure first, usually payroll or client payment operations.

What is the practical difference between an HRIS, an EOR, a MoR, and a payroll provider?

They do different jobs. An HRIS centralizes employee data and routine HR processes, a payroll provider runs payroll in a specific tax jurisdiction, an EOR supports hiring arrangements across borders, and an MoR covers customer billing responsibilities only as defined by the provider contract. The contract and local rules still decide what each provider is actually taking on.

If you are comparing payroll first, which signal matters most?

Match the tool to the risk. If paying people correctly is the main compliance job, a payroll-first provider is the strongest signal. The article uses Gusto as a useful checkpoint when payroll is your first hard requirement.

What if you run a U.S. S Corp and need to pay yourself?

Use payroll, not generic HR software, if you run a U.S. S Corp and need to pay yourself. Verify current S Corp payroll requirements with your accountant or tax advisor, then confirm the provider can support filings, year-end documents, and clean payroll exports. If the demo does not show the actual payroll and document trail, keep looking.

Can you just take owner draws instead of running payroll?

Do not rely on draws alone without verification. If you operate as an S Corp, confirm current payroll expectations with your accountant or tax advisor first. Then make sure your payroll provider can produce the records your books and tax file will need.

If you work globally, should you use one tool or two?

Use two tools if you work globally. Choose one tool for collecting client payments and another for paying yourself in your home tax jurisdiction with the right payroll records. Do not buy a global hiring product just because it sounds international if your real job is simply getting paid by clients.

How much should you trust ratings and “top tools” lists?

Use ratings and top-tools lists as a shortlist, not a verdict. The article notes that some rating sites tend to run higher than complaint-driven feedback sites, so your real check is a live scenario plus saved exports, pricing screenshots, and the service agreement. Verify the product directly before you commit.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

Value-Based Pricing for Freelancers Under Real Payment Risk

Value-based pricing works when you and the client can name the business result before kickoff and agree on how progress will be judged. If that link is weak, use a tighter model first. This is not about defending one pricing philosophy over another. It is about avoiding surprises by keeping pricing, scope, delivery, and payment aligned from day one.

How to Use Gusto for Payroll for a Small US-Based Agency

Gusto is a strong primary payroll system when your agency mostly runs U.S. payroll. Once you start paying people outside the U.S., it becomes one part of a broader stack, because sending money and carrying compliance responsibility are different jobs.

Self-Employed Benefits: Build Your Own Health, Retirement, and PTO Safety Net

You are not getting useful answers because guidance on "employee benefits" often assumes an employer-run setup, not a business you run yourself. In that model, the employer defines the role, sets the schedule, and offers extras around the job.