Quick Answer

Choose international health coverage when your family needs ongoing care, multi-country portability, or visa-ready proof; keep travel insurance for short, emergency-led trips. Screen plans with four checks: timeline fit, payment mechanics, catastrophic protection, and family-care terms. Verify direct hospital payment and preauthorization steps in writing, then confirm the certificate language matches your destination’s filing requirements, including Schengen short-stay rules when relevant.

The Global Professional's Playbook for Mitigating Family Health Risk#

Before you compare premiums, decide what problem you are actually buying to solve. For health insurance for nomad families, the first decision is not "which plan is cheapest?" Ask instead whether your risk profile is narrow enough for trip-focused cover or broad enough that you need ongoing international health coverage. Risk is impact and likelihood together, not price alone.

That distinction matters because the usual backstops are limited. The U.S. government does not pay medical bills abroad, and U.S. Medicare and Medicaid do not pay for care outside the United States. CDC also warns that care abroad often requires out-of-pocket payment at the point of service. So this is not just a reimbursement issue. It is an access and cash flow issue in real time.

1. Health continuity#

If your family needs ongoing care, emergency-only trip cover can be too thin. Routine pediatric visits, recurring prescriptions, pregnancy care, or follow-up for current conditions can point to continuity needs, not one-off travel incidents. Under U.S. regulation, travel insurance covers personal risks incident to planned travel. It is not the same as standalone major medical coverage.

Duration is a useful signal. CDC calls out travel health insurance as especially important when travel is more than 6 months, and the CDC Yellow Book notes that people planning more than 1 year abroad may need options beyond standard travel-policy framing.

Quick check. List expected appointments and medications for the next 12 months, then confirm in writing whether the policy is built for that pattern or only for unexpected illness and injury.

2. Financial protection#

Financial protection is about whether you can absorb both the size and the timing of a major event abroad. Medical evacuation is the clearest example. The U.S. State Department says air ambulance back to the United States can cost $20,000 to $200,000, and CDC says remote-area emergency transport to a high-quality hospital can exceed $100,000.

Policy design matters as much as headline limits. CDC notes that even where a country has nationalized healthcare, non-citizens may not be covered. Legal residence does not automatically mean healthcare access.

Treat pay-first structures as a serious risk. Travel.gc.ca notes that hospitals and clinics abroad may require immediate cash payment. If you cannot comfortably front large upfront payments, direct provider payment is part of core protection, not an extra feature.

3. Operational peace of mind#

Operational peace of mind means fewer failure points when something goes wrong. Ask three questions now. Who coordinates care at 2 a.m.? Who authorizes payment? What document do you present at admission?

CDC explicitly advises looking for a policy that pays hospitals directly. Verify the exact process in writing: after-hours assistance contact, preauthorization requirements, and how direct billing works in and out of network. Then confirm which hospitals in your likely locations actually accept that arrangement.

This pillar also depends on underwriting discipline. Disclose all current medical conditions for each family member, and confirm pre-existing-condition wording in writing. Travel.gc.ca is explicit that the agreement must include a stability clause.

A quick family risk profile check#

Before you compare plans, use this checklist to pin down the risk profile you are actually insuring:

| Profile area | Grounded cues |

|---|---|

| Destination pattern | Short trips are one profile. Repeated stays over 6 months, remote locations, or multi-country movement without a stable base are another. |

| Care needs | CDC flags pre-existing conditions, pregnancy, older age, and extended time abroad as profiles where specialized insurance may be especially beneficial. |

| Healthcare-system reliability | Country-level indicators are a starting point, not a guarantee. Validate city-level hospital options and non-citizen access rules before you rely on assumptions. |

- Destination pattern

Short trips are one profile. Repeated stays over 6 months, remote locations, or multi-country movement without a stable base are another. If you are still deciding where to base your family, The Best Cities for Digital Nomads with Families can help you assess schools and healthcare together.

- Care needs

Ongoing care needs can push you toward broader coverage. CDC flags pre-existing conditions, pregnancy, older age, and extended time abroad as profiles where specialized insurance may be especially beneficial.

- Healthcare-system reliability

Use country-level indicators as a starting point, not a guarantee. WHO reports the UHC service coverage index rose from 54 to 71 from 2000 to 2023, while about 4.6 billion people were still not fully covered in 2023. Validate city-level hospital options and non-citizen access rules before you rely on assumptions.

When travel cover is not enough#

Use these decision rules to decide when to stop shopping trip cover and start comparing long-stay plans:

| Signal | Trip-focused cover | Broader international health coverage |

|---|---|---|

| Stay length | stays are shorter | plan to be abroad more than 6 months; expect more than 1 year abroad |

| Care pattern | needs are mainly emergency-only; ongoing care is minimal | expect routine care across countries |

| Payment flow | you can absorb some out-of-pocket spend | need reliable direct billing |

| Immigration evidence | you do not need insurance documents for visa or residency processes | need policy evidence for immigration pathways |

| Coverage fork | trip-incident protection | ongoing healthcare continuity |

- Trip-focused cover may be enough when stays are shorter, needs are mainly emergency-only, ongoing care is minimal, you can absorb some out-of-pocket spend, and you do not need insurance documents for visa or residency processes.

- Broader international health coverage may be required when you expect routine care across countries, need underwriting for pre-existing conditions, plan to be abroad more than 6 months, expect more than 1 year abroad, need reliable direct billing, or need policy evidence for immigration pathways. Spain's digital nomad route requires an insurance certificate, and Japan's digital nomad route requires insurance documentation including medical-treatment compensation of JPY 10 million or more for the applicant and eligible spouse or children.

That is the key fork before plan shopping: trip-incident protection versus ongoing healthcare continuity. If you want a deeper dive, read The Crypto Cautionary Tale: Why Freelancers Should Be Wary of Crypto Payments.

The First Strategic Decision: Differentiating Travel Triage from True Global Healthcare#

Once you know your risk profile, match it to the right category of coverage. Choose based on your family's relocation timeline, not just price. Travel health insurance is for illness or injury during temporary travel. International health insurance is designed for longer periods abroad, where care needs may continue beyond an emergency.

1. Short trip#

If your plan is genuinely short-term travel, trip-focused cover can fit. This aligns with the Schengen short-stay frame of up to 90 days in any 180-day period, where applications may require travel medical coverage with at least 30.000 EUR. Use it as travel triage for unexpected illness, injury, and related logistics, not as your full family healthcare base.

2. Transition period#

Relocation is a phase where families can end up with the wrong type of plan. For stays of less than a year, short-term cover may still work in some cases, but only if your needs are mostly emergency-led and you have confirmed that your home-country insurance is not being over-assumed as backup.

In this phase, execution details matter: how claims are handled, and whether providers bill the insurer directly or bill you first.

3. Long-stay living abroad#

If you are living abroad for months or years, continuity of care becomes the priority. International plans are designed for longer periods overseas and can cover more than emergency treatment, including diagnosis, post-treatment care, and health checks. At that point, your policy becomes operating coverage, not a travel add-on.

| Decision point | Travel health insurance | International health insurance | What to verify now |

|---|---|---|---|

| Timeline fit | Short, temporary trips | Months to years abroad | Your real stay pattern |

| Continuity of care | Limited, trip-based | Built for ongoing care | Follow-up and diagnostics |

| Chronic conditions | Often restricted or plan-specific | Plan-specific | Underwriting terms in writing |

| Pediatric and routine care | Not a safe assumption | Varies by plan | Well visits, vaccines, prescriptions |

| Maternity/newborn pathway | Not a safe assumption | May be available on some plans, often with waiting periods | Whether 12 or 24 months applies |

| Mental health access | Varies by policy | Varies by plan or module | Benefit table and limits |

| Claims model and network usability | Plan and provider dependent | Direct billing may be available, but reimbursement can still happen | Which providers actually accept direct billing |

Red flags that usually mean travel cover is too thin for your situation:

- You need routine pediatric care, repeat prescriptions, or specialist follow-up.

- A family member has a pre-existing condition and the wording is still unclear.

- You may need maternity benefits and have not confirmed waiting periods.

- Some visa routes require broader insurance evidence for the full authorization period.

- You cannot comfortably front a large hospital bill if direct billing is unavailable.

If two or more red flags apply, move to long-stay provider comparison next, not bargain trip cover. For a step-by-step walkthrough, see How to Get Health Insurance in Portugal as a Digital Nomad.

Your Decision-Making Framework: A 4-Point Scorecard for Choosing the Right Partner#

After you pick the right coverage category, screen providers with the same standard. Use this as a pass or fail test, not a pricing exercise. If a quote fails any one pillar, reject it and move on.

1. Policy fit for your real living pattern#

If the policy does not match how you will actually live, nothing else matters. Pass only if the policy is built for sustained living abroad and your frequent destinations are inside the stated area of cover.

- Pass if: policy documents describe international health insurance for relocation or long-stay use, and area of cover matches your route.

- Fail if: wording is short-trip, emergency-only, seasonal, or excludes a country you regularly use.

- Ask for: benefit schedule, membership guide, and definitions and exclusions pages.

International health insurance is designed for sustained relocation. Travel cover is typically emergency-focused for shorter trips. If your family needs repeat prescriptions, follow-up specialists, or routine care across countries, this pillar must pass in writing.

2. Network and payment mechanics you can actually use#

A broad benefit table does not help if the payment flow breaks when you need care. Pass only if the provider can clearly explain authorization and payment flow in the countries you actually use.

- Pass if: they can show where direct billing is available, when reimbursement applies, and which services require preauthorization.

- Fail if: payment flow is vague, weekend or emergency escalation is unclear, or they cannot confirm practical hospital pathways.

- Ask for: direct billing provider list for your route, preauthorization rules, emergency contact flow, and out-of-network penalty terms.

Use these definitions during calls:

- Direct billing: the insurer pays eligible provider invoices directly, but you may still owe deductible, excess, or co-pay.

- Reimbursement: you may pay first and claim covered costs back.

- Preauthorization: the insurer confirms medical necessity before care. It is not a guarantee of payment.

- Continuity of care: coordinated care over time across your destinations.

This matters because many locations may require payment or a deposit before treatment, and network penalties can materially change total cost. Cigna, for example, describes a 20% reduction in one out-of-network U.S. scenario.

3. Catastrophic readiness you verify, not assume#

This is the part you should verify line by line, not infer from sales language. Pass only if the quote states both a current annual maximum and clear evacuation terms.

- Pass if: annual inpatient and daypatient maximum is explicit, and evacuation scope is specific.

- Fail if: either is vague, missing, or framed only in marketing language.

- Ask for: the exact annual maximum stated in the quote and the evacuation destination or return terms stated in the policy wording.

Market references can help you calibrate, but do not treat them as universal thresholds. Published Cigna examples show variation from $1,000,000 for Silver to $2,000,000 for Gold, with Platinum described as Paid in Full for inpatient and daypatient treatment. Travel.State.gov also notes that air ambulance can be very expensive and that many plans do not pay to bring you back to the U.S. Confirm destination, trigger, and who arranges transport.

4. Family-care pathways that survive relocation#

Family coverage often fails in the details, not the headline promise. Pass only if the policy supports your real care pattern across moves.

- Pass if: pediatric routine care, pre-existing or ongoing-condition handling, maternity and newborn pathway, and mental-health access are confirmed in your actual quote terms.

- Fail if: these items are assumed from marketing pages without written policy detail.

- Ask for: pediatric benefit schedule, underwriting decision for pre-existing conditions, maternity waiting period, newborn enrollment and document steps, and cross-country access details.

Provider examples are useful prompts, not proof for your policy. Cigna advertises pediatric routine-care benefits and maternity and newborn wording that includes the first 90 days. Allianz states a 12-month waiting period for listed maternity benefits and says it underwrites pre-existing conditions in its described offering. Treat all of that as a prompt, then confirm your own contract terms.

Use one table so every quote is scored the same way and the evidence request stays consistent:

| Provider | Policy fit pass/fail | Network/payment pass/fail | Catastrophic readiness pass/fail | Family pathway pass/fail | Evidence requested |

|---|---|---|---|---|---|

| Provider A | Benefit schedule, membership guide, area-of-cover terms | ||||

| Provider B | Direct billing map, preauthorization flow, evacuation wording | ||||

| Provider C | Pediatric schedule, pre-existing underwriting terms, maternity and newborn documents |

If a quote fails any pillar, stop comparing premiums. If two quotes pass all four, move to compliance checks next: visa or residency fit and other country-specific legal paperwork requirements.

We covered this in detail in How to Get Health Insurance in Spain as a Digital Nomad.

Before you compare policy options, align your insurance timeline with relocation paperwork using Gruv's Digital Nomad Visa Cheatsheet.

The Compliance Blind Spot: How Insurance Impacts Your Visas, Residency & Taxes#

A good policy can still fail at filing time. Once a quote passes the coverage test, run a compliance test before you submit anything. Your policy can affect your visa filing, renewal paperwork, and tax records.

| Compliance area | What to check | Keep or request |

|---|---|---|

| Policy validity window | Check that coverage dates match the legal period you are applying for. For Schengen short stays, insurance must cover the full intended stay or transit. | For multiple-entry visas, show coverage for the first planned visit and acknowledge that you need coverage for later stays. |

| Territorial coverage and minimum benefit checks | For Schengen short-stay processing, territorial validity across Member States and full-trip validity are explicit checks, and one official source states a minimum of 30.000,00 EUR. | Verify the current residency insurance requirement with the destination country's official embassy or consulate checklist. |

| Insurer document format for filing | Ask for a filing-ready certificate or confirmation letter, not a brochure. | Confirm insurer legal name, insured family members' full names, policy number, effective dates, territorial scope, and emergency or repatriation wording where requested. Check legalization or apostille, plus official translation where applicable. |

| Tax and renewal evidence trail | Keep policy schedule, invoices, payment confirmations, renewals, and dependent endorsements. | If you are U.S. self-employed, Form 7206 is used to determine any self-employed health insurance deduction. |

- Policy validity window

Check that coverage dates match the legal period you are applying for. For Schengen short stays, insurance must cover the full intended stay or transit. For multiple-entry visas, you must show coverage for the first planned visit and acknowledge that you need coverage for later stays. For long-stay routes, verify whether the destination requires coverage for the full authorization period.

- Territorial coverage and minimum benefit checks

Treat area of cover as a filing requirement, not marketing language. For Schengen short-stay processing, territorial validity across Member States and full-trip validity are explicit checks, and one official source states a minimum of 30.000,00 EUR. It also states that claims must be recoverable in Schengen Member States. For long-stay or digital nomad routes, verify the current residency insurance requirement with the destination country's official embassy or consulate checklist. EU-level pages are general overviews, and some locations use harmonized supporting-document lists.

- Insurer document format for filing

Ask for a filing-ready certificate or confirmation letter, not a brochure. Confirm it includes the details the consulate asks for, such as insurer legal name, insured family members' full names, policy number, effective dates, territorial scope, and emergency or repatriation wording where requested. Also verify document mechanics early. Some consulates require legalization or apostille, plus official translation where applicable. Check the exact consulate page before submitting.

- Tax and renewal evidence trail

Keep compliance records from day one: policy schedule, invoices, payment confirmations, renewals, and dependent endorsements. If you are U.S. self-employed, Form 7206 is used to determine any self-employed health insurance deduction, and IRS recordkeeping rules require documents that support deduction or credit items. Tax treatment is not automatic. Verify the current rule with a licensed cross-border tax professional for your tax residency. If you are a U.S. citizen or resident alien abroad, do not assume living abroad removes filing obligations.

Use this checklist to avoid double-coverage mistakes before you file or renew:

- Home-country obligations: Confirm whether domestic coverage should stay active, be suspended, or be canceled.

- Destination-country mandates: Save the exact embassy or consulate checklist and filing-date version you relied on.

- Renewal or audit file: Keep one folder with certificate, policy wording, receipts, translations, legalization or apostille records if used, and a short note explaining your coverage choice.

If you are still comparing options before filing, Digital Nomad Health Insurance Comparison for Visa-Ready Moves can help. Bring in an immigration adviser when consulate wording is unclear, citizenship mix complicates requirements, or translation and legalization rules are uncertain. Bring in a broker when certificate wording or territorial terms are ambiguous. Bring in a cross-border tax professional when you plan to deduct premiums, keep two policies, or change tax residency mid-year. You might also find this useful: Digital Nomad Health Insurance Comparison for Long-Stay Moves.

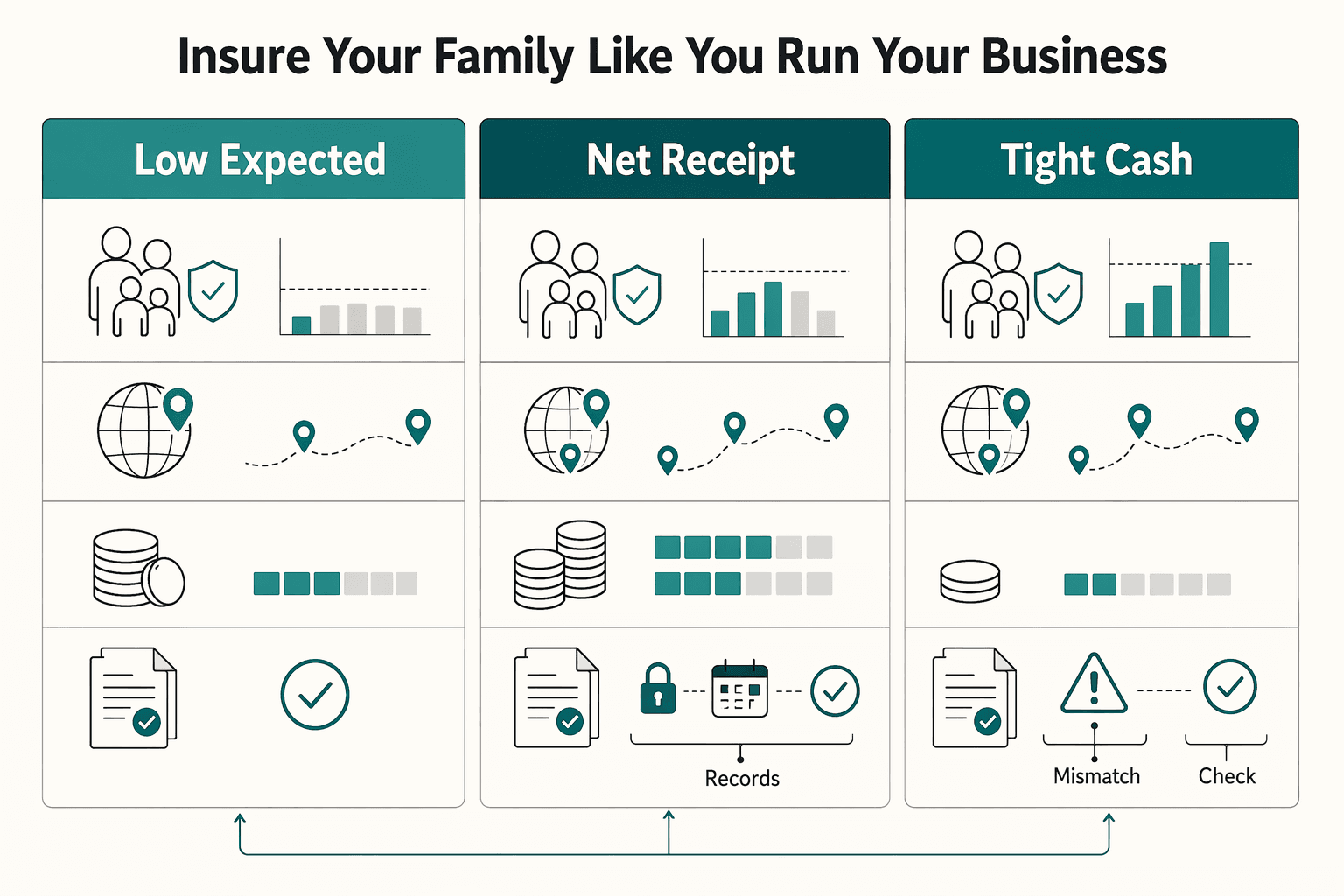

Your Final Mandate: Insure Your Family Like You Run Your Business#

The point is simple: run this decision as risk management, not price shopping. Define your family risk profile, choose the cost structure you can carry, verify policy wording against destination rules, and turn the policy into paperwork you can actually use.

- Define your family risk profile

Estimate next year's likely care use: doctor visits, pediatric care, prescriptions, ongoing conditions, and where you will actually live. If you are living abroad for a sustained period, international health insurance is generally a better fit than short-term travel cover, which may exclude routine and other non-emergency care. Decision lever: this tells you whether you are buying mainly for expected use, catastrophic protection, or both.

- Choose the cost tradeoff on total exposure, not premium alone

Your premium is the recurring monthly payment to keep coverage active. Your deductible is what you pay for covered services before the insurer pays. Your out-of-pocket risk is the unreimbursed exposure you may still carry through deductibles, copays, coinsurance, and non-covered care. If your family expects regular care, a higher premium with a lower deductible can be the lower total-cost option.

| Family situation | Can be a better fit | Main tradeoff |

|---|---|---|

| Low expected care use, few prescriptions, cash reserve available | Higher deductible, lower premium | Lower fixed monthly cost, higher out-of-pocket exposure if care is needed |

| Regular pediatric visits or predictable prescriptions | Higher premium, lower deductible | Higher monthly cost, lower year-to-year cost volatility |

| Tight cash flow during relocation | Higher premium, lower deductible | Higher monthly cost, potentially fewer surprise bills |

- Validate wording against the exact destination checklist

For visa or residency, do not rely on general guidance alone. Match policy wording to the current consulate checklist line by line. Spain's London consulate, for example, requires the original and a copy of the insurance certificate from an insurer authorized to operate in Spain, and states that the policy must cover risks covered by Spain's public health system. Failure mode to avoid: a valid policy that is still rejected for your application.

- Operationalize the policy before departure

Your operational continuity is your ability to keep essential family operations functioning during a health event or relocation disruption. Build your file now: insurance certificate, full policy wording, receipts, dependent endorsements, renewal notice, and claims instructions or app screenshots. For visa or residency, include the exact checklist used, plus legalization or apostille and official translation where required. For U.S. self-employed taxes, retain premium records and run deduction eligibility through Form 7206 and Schedule 1, line 17 for you, your spouse, and dependents.

Before departure, confirm all of the following:

- your risk profile is written and includes expected care and prescription use

- your shortlist compares premium, deductible, and out-of-pocket exposure

- policy wording is matched to the current consulate requirements

- your visa file includes certificate, full wording, and any required translation or legalization

- your tax file includes premium records and jurisdiction-specific review questions

Related: A Deep Dive into FinCEN's Beneficial Ownership Information (BOI) Reporting and Gruv's tools library.

Frequently Asked Questions

What is the real difference between travel insurance and global health insurance for families?

Use travel insurance for emergency-only events, not full family healthcare abroad. It is designed for short-duration trips and emergency treatment, while international health insurance is structured for comprehensive ongoing care over a sustained period. If you need continuity across countries, treat portability as a must-have and focus on global plans.

How should you shortlist plans for health insurance for nomad families?

Shortlist by policy fit, not brand name. In the policy wording, confirm direct hospital payment options, evacuation handling, claims workflow, and how the area of cover maps to where you will actually live. Then verify area of cover line by line, and for visa use confirm the destination’s current rule directly with the consulate.

What should you check about evacuation and claims before you buy?

Treat evacuation terms as a core risk-control decision because air ambulance costs can run from $20,000 to $200,000, and CDC guidance notes remote-area evacuation can exceed $100,000. Before you buy, check how emergencies are reported and how claims deadlines are set. One insurer asks for emergency notification within 48 hours, and another allows submission up to six months after the end of the Insurance Year. If reimbursement is the only path and timing is unclear, treat that as a warning sign.

Will your policy satisfy visa or residency requirements?

Assume nothing until the policy wording matches the exact immigration checklist. For Schengen short stays up to 90 days in any 180-day period, coverage must include repatriation, urgent medical attention, emergency hospital treatment, or death-related costs. For long-stay or digital nomad routes, confirm country-specific requirements and keep a complete evidence file with certificate language, policy wording, receipts, any consulate-required translations, and the checklist version you used.

Can you deduct premiums on your taxes?

If you are U.S. self-employed, you may be able to, but verify before filing. The IRS says Form 7206 is used to determine any self-employed health insurance deduction and includes coverage for you, your spouse, and your dependents. Keep substantiation records from day one, and have a cross-border tax professional review your case if residency or overlapping coverage changed during the year.

What documents should you keep after you enroll?

Keep a complete compliance file, not just an insurance card. Save the certificate, full policy wording, insurance card and claim forms or app screenshots, invoices, payment confirmations, and renewal notices. This helps keep claims timelines and tax substantiation organized. If schooling is part of your move plan, A Guide to the Best International Schools in Lisbon can help you align location choices with family logistics.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- cdc.gov/yellow-book/hcp/health-care-abroad/travel-in...trusted

- cdc.gov/yellow-book/hcp/health-care-abroad/what-to-d...trusted

- cms.gov/medical-bill-rights/help/plan/new-health-plantrusted

- csrc.nist.gov/glossary/term/risktrusted

- ecfr.gov/current/title-45/subtitle-A/subchapter-B/par...trusted

- healthcare.gov/glossary/preauthorizationtrusted

- healthcare.gov/glossary/cost-sharingtrusted

- irs.gov/businesses/small-businesses-self-employed/wh...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Freelance Crypto Payments That Protect Cashflow and Reduce Disputes

Crypto payments make sense only when they improve how reliably you get paid after you plan conversion, compliance, and recordkeeping up front. They can reduce friction in some international setups where traditional platforms add fees, restrictions, or extra steps. They also move risk onto conversion timing, exchange-fee exposure, and documentation quality, so use a simple acceptance test before you agree:

Beneficial Ownership Reporting in 2026 for FinCEN BOI Decisions

Use this as an execution guide, not a legal memo. Your job is to make a current BOI decision, document why you made it, and avoid cleanup later. The outcome is straightforward: confirm whether your entity is in scope, prepare what you need if it is, and keep dated proof of the basis you used.

Choosing the Best International Schools in Lisbon for Your Family

Start with a one-page decision brief, not a school list. Done well, it gives you a usable filter for your Lisbon international school search before you email a single admissions office, and it saves you from rebuilding your shortlist later.