Quick Answer

Choose software by workflow origin, not receipt speed. For the best expense management software remote team setup, reimbursement-first tools fit teams that pay first and submit later, while direct company-card spend usually needs broader controls, reconciliation, and invoice-status visibility. Keep compliance in scope by maintaining verifiable residency-day logs, foreign-account records, and cross-border invoice field checks so your close process stays reliable.

The Financial Command Center: Why "Expense Software" is the Wrong Tool for Your Global Business-of-One#

If you are choosing the best expense management software for a remote team, treat it as an operating decision, not just a receipt-tool purchase. You need a setup that shows money in, money out, approvals, reconciliation status, and potential risk signals early enough to act.

Expense tools matter, but they are usually built around employee-submitted expenses, approvals, reimbursements, and reconciliation. That covers one important workflow. It may not cover your full operating model when you also rely on client invoices, contractor reimbursements, vendor bills, and accounting data you can trust.

Brex, Ramp, and Expensify are all strong products. The practical question is scope. Do they only improve expense reporting, or do they support the broader flow you depend on to protect cash flow and reduce finance blind spots?

The five jobs your setup needs to handle#

| Job | Products mentioned | Grounded details |

|---|---|---|

| Money in | Expensify | Supports creating and sending invoices, receiving payments, and tracking status; invoicing help docs state a 2.9% processing fee per transaction for that payment flow |

| Money out | Ramp; Brex | Ramp positions its product across cards, travel, expenses, and accounts payable; Brex describes automation across cards, bill pay, travel, and reimbursements |

| Reconciliation | Expensify; Ramp | Expensify states end-to-end expense flow with accounting sync; Ramp reporting supports views across Cards, Reimbursements, and Bills |

| Policy enforcement and documentation | Brex | Brex's policy tooling and approvals coverage spans card expenses, reimbursements, and bill payments |

| Decision dashboard and integration fit | Brex; Ramp; Expensify | Brex promotes syncing across 1,000s of native integrations; Ramp emphasizes out-of-the-box integrations; Expensify lists major accounting and ops connections plus 45+ more |

- Money in

You need visibility into invoice creation, payment status, and collections progress. Expensify supports creating and sending invoices, receiving payments, and tracking status, and its invoicing help docs state a 2.9% processing fee per transaction for that payment flow.

- Money out

This is where these tools are often strongest. Ramp positions its product across cards, travel, expenses, and accounts payable, and Brex describes automation across cards, bill pay, travel, and reimbursements.

- Reconciliation

Spend capture is not enough if close is still manual. Expensify states end-to-end expense flow with accounting sync, and Ramp reporting supports views across Cards, Reimbursements, and Bills.

- Policy enforcement and documentation

You need rules that apply before money leaves. Brex's policy tooling and approvals coverage across card expenses, reimbursements, and bill payments shows how controls can span multiple payment flows.

- Decision dashboard and integration fit

You need dependable reporting and clean sync to your stack. Brex promotes syncing across 1,000s of native integrations, Ramp emphasizes out-of-the-box integrations, and Expensify lists major accounting and ops connections plus 45+ more.

Decision matrix for software selection#

| Capability | Expense-led tools | Spend platforms like Ramp or Brex | What your command-center setup still needs |

|---|---|---|---|

| Expense capture | Strong receipt capture, report submission, reimbursement flows | Strong, especially when card-linked | Reliable accounting coding and audit trail quality |

| Approvals | Typical manager approval workflows | Can be strong across cards, reimbursements, and bills | Approval logic that matches your real authority structure |

| AP/AR coverage | Some include invoicing, for example Expensify | AP is clear; native client AR is not established here | Clear tracking of invoice status and overdue cash |

| Multi-currency handling | Local-currency reimbursement support exists in some flows | Ramp states worldwide reimbursements and international vendor payments in 190+ countries; Brex supports local-currency reimbursement setup | Entity, country, and payee eligibility checks before rollout |

| Compliance monitoring | Documentation and policy checks | Policy enforcement and approval controls | Legal and tax obligations still require accounting or specialist handling |

| Reporting depth | Strong on expense reporting | Strong cross-flow spend reporting | Unified revenue, spend, and profit visibility |

| Integration fit | Broad accounting integrations are common | Broad finance and ops integrations | Ownership of sync rules and data mapping |

| Best fit use case | Expense-report-heavy teams | Teams needing cards, bills, reimbursements, and tighter spend control | Teams that also need money-in visibility and better cash-risk control |

Use this framework for the rest of your evaluation. The next three pillars look at compliance protection, profit visibility, and operational control, not receipt capture alone. If you want a related comparison, see The Best Business Credit Cards for Freelancers.

Pillar 1: The Compliance Shield - Mitigating Risks You Don't Know You Have#

A useful tool helps you catch compliance risk before it turns into rework. If it cannot surface risk signals and keep a defensible record, it is not acting as a real control layer.

For a remote team, use a simple loop: identify, assess, act, repeat. In practice, that is usually more reliable than dealing with problems one by one after they surface.

- Presence tracking

Track days by jurisdiction with evidence, not just travel spend. Keep one record that shows where you were and when, then set a buffer alert before any verified rule you monitor. If your control file is missing the current rule, mark the current threshold as pending official/advisor verification before relying on alerts.

Run a monthly reconciliation against at least two evidence sources, for example calendar, bookings, or border records where available. When reviewing software, check whether it supports alerts, dated edit history, and exportable logs.

- Foreign account reporting exposure

Track foreign account balances in one base currency, including an aggregate view, so you can compare against your verified trigger. In your control notes, mark the filing trigger wording and threshold as pending official/advisor verification until confirmed.

In product reviews, test whether the tool can produce consistent cross-account snapshots with timestamps and exports. If it cannot, plan to run this control outside the tool.

- Cross-border invoicing

Validate invoice fields before sending. The risk is delay, corrections, and weak records when required fields are incomplete or inconsistent.

Add a send-block or approval check for missing core fields, for example legal names, addresses, issue date, invoice number, service date or period, currency, and tax identifiers if applicable. For jurisdiction-specific wording, keep local wording pending official/advisor verification before relying on the template. In software evaluation, prioritize template controls, approval checkpoints, and invoice version history.

| Compliance need | What to monitor | Alert to set | Capability to evaluate |

|---|---|---|---|

| Presence tracking | Days by jurisdiction plus evidence links | Buffer alert before verified rule | Configurable alerts, editable travel log, exportable records |

| Foreign accounts | Aggregate and account-level balances | Early warning before verified reporting trigger | Cross-account snapshots, conversion record, exportable snapshots |

| Cross-border invoicing | Required fields and local wording | Send-block or approval prompt for missing fields | Template controls, approval checks, invoice version history |

A compact control loop you can run#

If a product is strong on expense reports but weak on these controls, keep looking. For remote finance, compliance value comes from early warning, clean records, and exports you can defend later. Keep the process simple and repeatable:

| Cadence | Control | Action |

|---|---|---|

| Weekly | Capture travel data | Update locations, attach evidence, review alerts |

| Monthly | Aggregate account balances | Pull balances, convert to base currency, save the timestamped snapshot |

| Before send | Validate invoice fields | Use locked templates and a pre-send checklist |

| At close | Export records | Keep travel logs, balance snapshots, and invoice versions together |

For a step-by-step walkthrough, see The Best Expense Tracking Apps for Freelancers.

Pillar 2: The Profit Engine - Analyzing Your Business's True Health#

Margin trouble shows up before the cash balance makes it obvious. When revenue and spend live in separate tools, you can miss the early signal on weak projects, category drift, and FX leakage. That is the real difference between tracking receipts and protecting profit.

| Focus | Signal to watch | Decision it unlocks |

|---|---|---|

| Project profit view | Profit by project, based on total invoiced less total project cost | Where to reprice, where to change scope, and which engagements to renew |

| Rule-based categorization | Category drift: uncategorized items, repeated manual recoding, and project or client miscoding | Cleaner margin tracking and fewer close-cycle corrections |

| Multi-currency leakage | The gap between quoted and booked value after conversion and transfer handling | Which rail to use next time, when to invoice in local currency, and when to avoid corridors that keep trimming margin |

Use this lens when comparing tools: project-level profitability, rule-based categorization controls, FX transparency, card and transfer reconciliation, and export quality.

- Build a real project profit view

Connect invoices, project costs, and tracked time in one place. The signal to watch is profit by project, based on total invoiced less total project cost. That tells you where to reprice, where to change scope, and which engagements to renew.

Keep the data complete. Project profitability stays reliable only when tasks, expenses, staff time, and invoices are all recorded to the same project. When reviewing tools, separate spend visibility from true profit visibility. Real-time spend across cards, reimbursements, and bills is useful, but it is not a full P&L by itself.

- Use rule-based categorization you can trust

Connect card transactions, reimbursements, bills, and accounting mappings so coding stays consistent. The signal to watch is category drift: uncategorized items, repeated manual recoding, and project or client miscoding. The decision it unlocks is cleaner margin tracking and fewer close-cycle corrections.

Compare rule depth, GL mapping controls, edit history, reconciliation paths, and export quality. Ramp supports preset accounting rules, and Brex maps its default 48 categories to GL accounts. Expensify supports export to CSV or accounting integrations, which matters when you need downstream checks in your accounting file.

- Catch multi-currency leakage early

Connect original-currency spend, settlement amounts, transfer receipts, and net received value in your base currency. The signal to watch is the gap between quoted and booked value after conversion and transfer handling. The decision it unlocks is which rail to use next time, when to invoice in local currency, and when to avoid corridors that keep trimming margin.

Expensify states conversion uses the daily average rate on purchase date and supports linked-card reconciliation with 10k+ banks. For rails, compare full quote-to-settlement behavior, not headline pricing alone.

| Method | Visible fee types | Rate transparency | Settlement clarity | Net received value check |

|---|---|---|---|---|

| Card payment priced like Stripe | 2.9% + 30¢ domestic, +1.5% international, +1% currency conversion | Published fee components; full outcome still depends on setup | Published processor fees are clear, but banking settlement timing is separate | Sample calculation pending finance review. |

| PayPal currency conversion | Fee policy states a conversion spread is included on a base exchange rate | Review marketing language and fee policy together | Checkout can appear simple, but quote-to-settlement checks still matter | Sample calculation pending finance review. |

| Mid-market transfer model like Wise | Live mid-market rate plus upfront fee; discount stated above 25,000 USD equivalent | High when model is stated directly | Quote clarity is stronger, but corridor-specific results still need testing | Sample calculation pending finance review. |

| Intermediary bank transfer model like OFX or bank wire | Quoted fee may not be the only deduction | Rate basis can be less explicit | Intermediary or receiving bank deductions can reduce delivered value | Sample calculation pending finance review. |

This pillar connects directly to cash flow. If you catch margin erosion early, you can switch rails and adjust pricing before small losses stack up over a quarter. If you want a deeper dive, read Value-Based Pricing: A Freelancer's Guide.

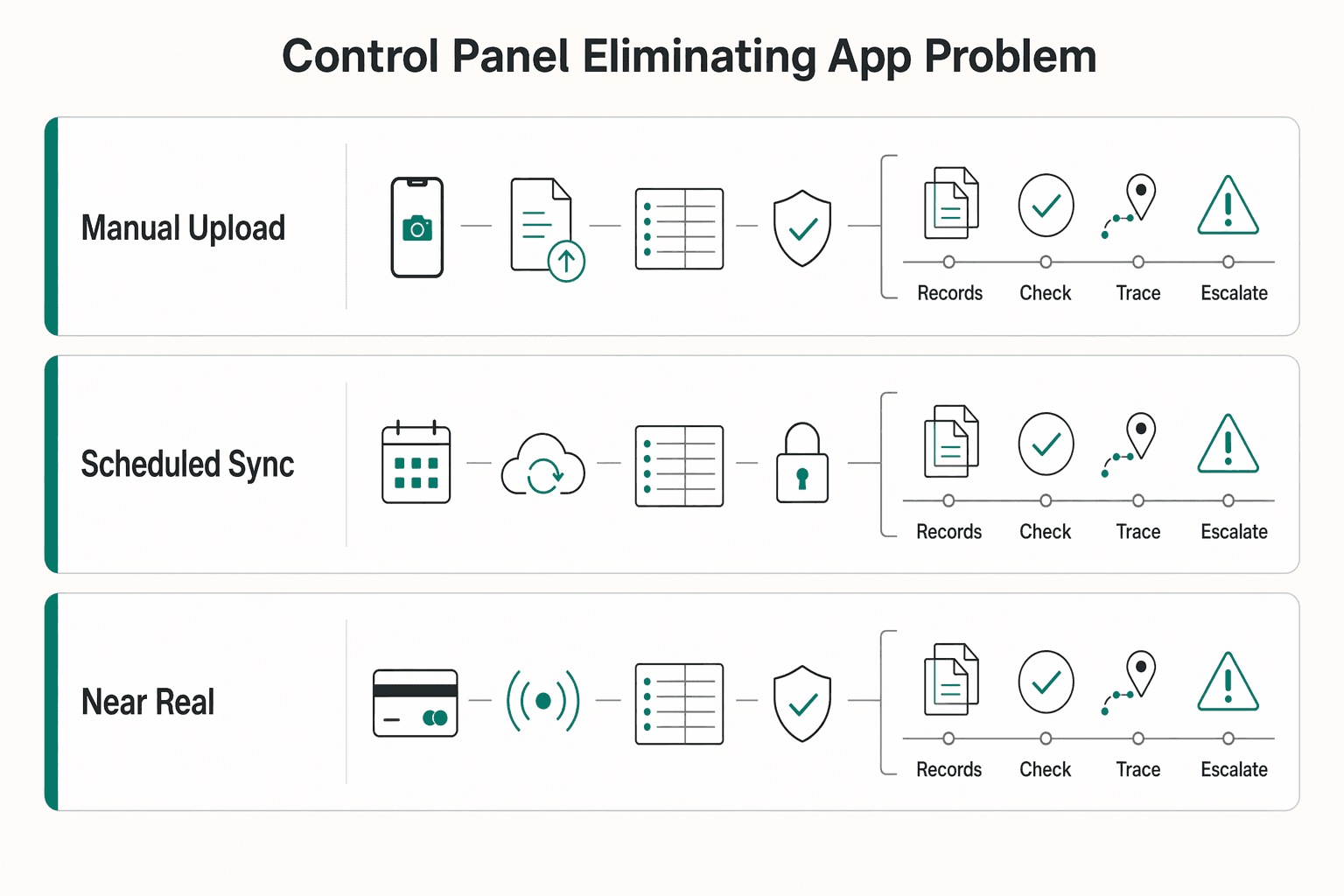

Pillar 3: The Control Panel - Eliminating the "15+ App Problem"#

A practical way to cut admin drag is to work from one operating hub. You want a Financial Command Center that connects income, expenses, invoicing, card activity, cross-border movement, and compliance obligations. Then you can act from one view instead of bouncing across disconnected tools.

- Set up receipt capture that actually closes the loop

Receipt capture only matters if the record stays usable later. During setup, check how receipts are captured, including mobile capture, how they are matched to transactions, whether policy controls are applied, and whether receipt records stay attached through reconciliation.

If your team still has to hunt across systems to match receipt, charge, and ledger entry, the process is still fragmented.

- Map your system before you trust integrations

Before you rely on sync, map the lanes that matter: expense tool, invoicing, card activity, banking activity, and accounting ledger. The real test is exception handling. When sync issues or coding errors happen, someone needs to own the fix in each lane.

When time and expenses connect cleanly to billing, invoicing moves faster. Invoice-status tracking also gets easier to manage in the same flow.

| Integration maturity | What it looks like | Reconciliation pace (typical) | Cashflow visibility (typical) |

|---|---|---|---|

| Manual upload | CSV or file imports with manual checks | Can be slower, with issues found near close | Can be partial and delayed |

| Scheduled sync | Data moves on a set cadence | Can improve pace, but exceptions may sit between runs | Can be more complete, with lag |

| Near real-time sync | Transactions and status updates appear quickly | Can help teams catch and clear exceptions sooner | Can improve day-to-day visibility |

- Use the dashboard as a daily decision panel

A dashboard should drive action, not just display data. Monitor four control signals every day: cash position, invoice status, spend anomalies, and compliance obligations. Tie each one to an immediate next step.

If cash is tightening, review unpaid invoices and upcoming obligations now. If invoice status stalls, follow up or correct billing data. If spend or policy controls flag issues, verify the transaction, receipt, and coding before close. If compliance issues appear, check the underlying record the same day.

For a related workflow example, see The Best Property Management Software for Landlords. Before you lock in a stack, run your current card, FX, and transfer paths through the payment fee comparison tool to review potential leakage.

Conclusion: You're Not Managing Expenses, You're Managing an Enterprise#

For a remote business, the real decision is not receipt speed. It is the control model: reimbursement-first tracking or integrated spend control. That choice determines whether your workflow stays clean as volume grows.

Expense management software is built to track, approve, and reimburse expenses digitally. If spending usually starts with someone paying first and then submitting a receipt, a reimbursement-first tool like Expensify can be a good fit. If spending mostly starts on company cards or inside a broader spend flow, you will likely need more than expense reports.

| Decision criterion | Reimbursement-first tool | Unified spend platform or command-center setup |

|---|---|---|

| Goal | Capture receipts, route approvals, reimburse accurately | Control spend earlier and keep cards, expenses, reimbursements, and reporting connected |

| Data visibility | Visibility into submitted expenses after submission | Wider visibility across transactions, syncing, and reconciliation |

| Risk controls | Policy checks on submitted claims | Documentation and controls across spend and accounting workflows |

| Workflow fit | Best when people pay out of pocket first | Best when spend starts through company cards, bill pay, or linked accounts |

| Reporting output | Expense reports and reimbursement records | Reporting plus reconciliation and accounting-ready records |

Use a simple test: review your last 30 transactions. If most start with receipt capture and submission, reimbursement software is still a practical choice. If most start as direct company spend, prioritize real-time visibility and accounting integration. Manual email approvals and disconnected tools are harder to scale and create visibility gaps.

Treat Brex and Ramp as fit-by-use-case examples, not universal picks. A unified spend platform can make sense when you want cards, expenses, reimbursements, and related finance activity in one system. A command-center setup is often a better fit when your monthly close depends on transaction syncing, stronger documentation and controls, and reporting outputs you can reuse in accounting review.

Next step: lock your terms and map how spend actually starts. Then validate documents and accounting sync on one sample month, and run a weekly check plus a month-end review to keep the risk-first rhythm from this guide.

Also useful: How to Use Brex for a Venture-Backed Startup with a Remote Team.

If you want one workflow to collect, track, and pay out with clearer controls, review Merchant of Record for freelancers. Then confirm fit for your markets.

Frequently Asked Questions

How do I manage expenses for taxes as a remote operator?

Record each expense when it happens with the original currency amount, USD translation, and the exchange-rate date used. Verify that every deductible item has supporting documents attached, such as a receipt, invoice, canceled check, or similar record, and confirm your translations follow the rate in effect when you receive, pay, or accrue the item. Automate category rules, receipt capture, and multi-currency records, but treat FEIE as conditional, not automatic, until your foreign tax home and the applicable filing-year exclusion amount are verified. Next step: audit your last 20 transactions and fix any line missing original currency, USD amount, rate date, or backup document.

What is the best software to track days for tax residency?

Use a tracker that handles FEIE and Schengen counting together, not just a basic travel diary. Verify each day log against your travel records (for example, passport stamps, boarding passes, calendar entries, and lodging records), since FEIE physical presence uses 330 full days during any period of 12 consecutive months and Schengen short-stay policy is 90 days in any 180-day period across the 29-country area. Automate daily location capture and alerts for missing exit dates or approaching limits. Next step: backfill the last 180 days of travel before relying on forward-looking totals.

Is Expensify or SAP Concur good for a solo freelancer or small remote team?

Choose based on workflow fit, not a universal "best" tool. Pick Expensify when your core workflow is reimbursement, where people pay out of pocket and submit expenses for repayment. Pick SAP Concur when you need a connected employee-initiated travel, expense, and invoice workflow, then verify that this matches how spend actually starts in your business. If most spending is direct company-card or business-account spend, automate controls in a spend-management system built for real-time visibility instead of forcing a reimbursement-first tool into that role. Next step: tag your last 30 transactions as reimbursement or direct company spend, then choose the tool category from that split.

How can I track foreign bank accounts to stay on top of FBAR?

Build and maintain a register of every foreign financial account where you have a financial interest or signature or other authority. Verify each account’s highest balance during the year and monitor the aggregate total, because the FBAR trigger is based on aggregate value crossing $10,000 at any point in the reporting year, with a due date of April 15 and automatic extension to October 15. Automate USD conversion, periodic balance snapshots, and alerts for new accounts or sharp balance increases. Next step: create or update your register with institution, country, account suffix, owner or signer status, and highest known balance.

What matters more than receipt capture in an expense app?

Prioritize filing-risk controls first, and treat receipt capture as supporting evidence. Verify that each transaction ties cleanly to the receipt, ledger entry, currency conversion record, and any travel-day data used for FEIE or Schengen tracking. Automate missing-receipt reminders, but also automate travel logs, multi-currency conversion records, and foreign-account monitoring so month-end review catches issues that affect filings. Next step: add one weekly check for missing documents and one weekly check for residency or account-threshold alerts.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 5 external sources outside the trusted-domain allowlist.

- irs.gov/businesses/small-businesses-self-employed/re...trusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- sec.gov/Archives/edgar/data/1476840/0001628280210201...trusted

- alertmedia.com/blog/risk-management-frameworkexternal

- brex.com/spend-trends/expense-management/best-expense...external

- brex.com/support/expense-managementexternal

- expensify.comexternal

- g2.com/categories/expense-managementexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Value-Based Pricing for Freelancers Under Real Payment Risk

Value-based pricing works when you and the client can name the business result before kickoff and agree on how progress will be judged. If that link is weak, use a tighter model first. This is not about defending one pricing philosophy over another. It is about avoiding surprises by keeping pricing, scope, delivery, and payment aligned from day one.

The Best Business Credit Cards for Freelancers

Pick for reliability first. For a freelancer, the right business card is usually the one that keeps recurring bills moving, keeps records clean, and avoids extra costs when income swings from month to month. Rewards still matter, but they sit on top of those basics. They do not replace them.

How to Use Brex for a Venture-Backed Startup with a Remote Team

**Short answer:** If you are evaluating **brex for remote startups**, make this decision early. Use Brex as your operational finance layer, not as your only compliance layer. A resilient setup has two parts: one for spend control and clean accounting, and another for worker classification, tax documentation, and tax-presence review before payment.