Quick Answer

Start with a three-part setup for the best credit cards no foreign transaction fee decision: use one primary card for business purchases, keep a separate backup card for continuity, and reserve a specialist debit tool for ATM cash. Then run the operational checks that matter most: confirm backup access, default to local currency to avoid merchant-side conversion surprises, and verify each issuer’s current fee and cash-advance terms. This approach protects cash flow better than picking a single rewards card.

Your Strategic Playbook for Global Business Spending: More Than Just "No Foreign Transaction Fees"#

If one blocked card can interrupt your workday, you do not have a card strategy. You have a single point of failure. The Resilient Wallet is a practical way to avoid that. Its job is simple: keep you paying, protect cash flow, and stop one payment problem from turning into an operations problem.

| Role | Main use | Key differentiator | Important note |

|---|---|---|---|

| Primary spend card | Default for flights, software, hotels, and larger operating expenses | Cash flow role | A business card with revolving credit can carry part of the balance, but unpaid amounts accrue interest; a corporate charge card is due by the statement due date |

| Independent backup rail | Continuity card when the first one is unavailable | Reliability under stress | Keep it separate from daily spend, make one small test purchase before a trip, and confirm account access and support |

| Local currency access tool | ATM withdrawals and cash-only situations | On-the-ground access | Not your main credit card used as a cash advance, and it does not bypass legal restrictions |

Payment interruptions are worth planning for. A fraud review can lock your main card before hotel check-in. A merchant may not accept your first payment option. An urgent supplier invoice can hit while you are in transit and unable to wait for a card issue to clear. The OCC credit card lending handbook, Version 2.0 from April 2021, frames credit card lending as a risk-managed activity and includes account-management actions such as account closures, line increases and decreases, and over-limit authorizations.

In practice, your wallet needs to cover three separate jobs:

-

Primary spend card. This is your default for flights, software, hotels, and larger operating expenses. Key differentiator: cash flow role. If it is a business card with revolving credit, you can carry part of the balance, but unpaid amounts accrue interest. A $50,000 balance at 20% APR could cost $10,000 a year. If it is a corporate charge card, the full balance is due by the statement due date.

-

Independent backup rail. This is not your points chaser. It is your continuity card when the first one is unavailable. Key differentiator: reliability under stress. Keep it separate from your daily spend, make one small test purchase before a trip, and confirm you can actually log in, view the account, and contact support.

-

Local currency access tool. This is your tool for ATM withdrawals and cash-only situations, not your main credit card used as a cash advance. Key differentiator: on-the-ground access. It also does not bypass legal restrictions. In the cited OFAC sanctions FAQ (updated March 19, 2026), certain transactions are prohibited unless specifically authorized.

By the end of this guide, you should have three clear assignments: one workhorse, one real backup, and one local cash tool. If you finish with only a shortlist of cards that waive foreign transaction fees, you are still exposed. Related: The Best Travel Credit Cards for Digital Nomads.

Layer 1: How to Choose Your Primary Workhorse#

Choose a primary card that reliably handles your real business spend first; perks are secondary. If the value only works when you maximize every credit, portal, or promo, it is a weak main rail.

| Filter | What to check |

|---|---|

| Acceptance profile | Match the card to your highest-value and highest-urgency merchants, not to marketing copy |

| Issuer reliability | Stable account access, clear alerts, usable support, and a line that can handle uneven months |

| Protections you will use | Review current benefit terms and keep a dated copy of what you relied on |

| Expense-management fit | Confirm statement clarity, export quality, and authorized-user visibility for your bookkeeping workflow |

Use this quick filter in order:

- Acceptance profile: Match the card to your highest-value and highest-urgency merchants, not to marketing copy.

- Issuer reliability: Prioritize stable account access, clear alerts, usable support, and a line that can handle uneven months.

- Protections you will use: Review current benefit terms and keep a dated copy of what you relied on.

- Expense-management fit: Confirm statement clarity, export quality, and authorized-user visibility for your bookkeeping workflow.

Premium cards are a tradeoff: stronger perks, heavier annual fees. One premium card is often enough; stacking several can turn into fee drag (one cited scenario was over $1,600/year).

Practical card examples and tradeoffs#

| Card example | Best fit when | Coverage style | Redemption flexibility | Accounting workflow fit | Main downside |

|---|---|---|---|---|---|

| Capital One Venture X | You want a simple everyday catch-all and can actually use portal-linked travel value. | Verify current protection terms before relying on them. | Cited example terms: 2X miles on all purchases; 10X hotels/rental cars and 5X flights through Capital One Travel. | Cited example allows up to 4 authorized users at no extra cost; verify current export/reconciliation experience. | Cited $395 annual fee; value depends on conditions like the $300 travel credit tied to Capital One Travel. |

| Chase Sapphire Preferred | You want to compare a mainstream transferable-points option before moving to higher-fee premium cards. | Current benefit terms pending issuer verification. | Current earning, transfer, and redemption terms pending issuer verification. | Verify statement detail and export format against your current process. | Can still be a poor primary rail if limits or workflow do not match your spend pattern. |

| The Platinum Card from American Express | You have spend patterns that consistently use premium travel-oriented benefits. | Current benefit terms pending issuer verification. | Current redemption and transfer terms pending issuer verification. | Verify merchant acceptance in your actual vendor mix and reconciliation workflow. | High-fee products underperform when your business does not naturally use the perk structure. |

Selection checklist before you apply#

- Test fit against your top merchants and biggest expense categories.

- Confirm which headline benefits are conditional (portal booking, specific channels, or other gates).

- Save the current fee and benefit terms you reviewed, with date.

- Validate statement/export quality and authorized-user visibility for your bookkeeping process.

- Stress-test for peak-month spend so this card can stay your default rail.

If this card passes the checklist, it can fill your primary slot. Next, set up your backup rail so one issuer issue does not stop operations.

We covered this in detail in The best business credit cards for earning airline miles. If you want a quick next step, try the free invoice generator.

Layer 2: Why Your Redundancy Card is Your Most Important Insurance Policy#

Your backup card is for continuity, not rewards. When your primary card is unavailable at the wrong time, this is the card that keeps your trip, software billing, and supplier payments moving.

Use this layer to reduce single-point failure risk. If your backup is untested, hard to access, or exposed to the same failure path as your primary, it is not real redundancy.

Use one operating rule#

Treat different network, different issuer as your working default. It is a practical way to reduce shared risk across both card rails and the bank behind them.

The network side helps when acceptance varies. The issuer side helps when the issue is account access, security review, or card replacement. Keep your filter tight for this role: no foreign transaction fee, low carrying cost, broad usability, and easy emergency access from abroad.

| Your primary setup | Backup target | Why this pairing is useful | Verify on issuer page now |

|---|---|---|---|

| Visa from Issuer A | Mastercard from Issuer B | Lowers concentration across both network and issuer | Foreign transaction fee, annual fee, support access, alert controls |

| Mastercard from Issuer A | Visa from Issuer B | Gives you a second route if one rail or issuer is disrupted | Current fee terms, lock/unlock controls, replacement process abroad |

| Amex from Issuer A | Visa or Mastercard from Issuer B | Improves day-to-day acceptance while separating issuer exposure | Network, fee terms, emergency access options, saved terms PDF |

Also verify terms directly with the issuer instead of relying only on roundups. During this refresh, one comparison page was inaccessible and showed "Sorry, you have been blocked" with Cloudflare Ray ID 9df616094c643019, so direct issuer checks are the safer source of truth.

Activate it before you need it#

- Activate the card and run one small test purchase.

- Store it separately from your primary card.

- Confirm remote access now: app login, support path, and card details you can retrieve securely while abroad.

- Turn on transaction and login alerts before travel.

The common failure is not "no backup," but "backup not ready." If you operationalize this now, this layer works when you actually need it.

This pairs well with our guide on The best business credit cards for hotel points.

Layer 3: Mastering Local Currency with a Specialist Tool#

Use your credit cards for most spending, and reserve a multi-currency debit tool for local cash and true local-balance needs. This keeps your purchase flow stable while reducing avoidable cash-access friction.

| Reference | Stated fee detail | Other stated note |

|---|---|---|

| Wise | 2 free withdrawals each month when total withdrawals stay within 100 USD, then 1.5 USD per withdrawal and 2% of any amount over 100 USD | Says it uses the mid-market rate, positions its card for spending in 40+ currencies, and treats ATM use at the account level each month |

| Revolut US Standard | Out-of-network ATM withdrawals can cost up to 2%; adding money by domestic personal credit card can cost up to 3%, with possible extra issuer charges | Says exact fees are shown in-app, lists a last-updated date of November 18, 2025, and says the Cardholder Agreement governs if terms conflict |

| Multi-currency account provider | Should show conversion cost clearly and exact fees before you confirm | Should support local withdrawals |

| Use case | Primary tool | Why | Failure risk if misused |

|---|---|---|---|

| ATM cash | Multi-currency debit card/account | Helps you avoid treating an ATM withdrawal as a credit-card cash advance and lets you plan around provider ATM rules | Credit-card ATM use can trigger separate fee/interest mechanics; ATM operator or network fees may still apply |

| Card-present purchases | Primary credit card | Keeps day-to-day spend on your main purchase rail and preserves local balance for cash-only moments | Using debit for everything can drain local balance before you need cash |

| Online spend | Primary credit card | Avoids unnecessary funding hops when local cash access is not the goal | Funding wallets or other accounts through debit rails can trigger extra charges |

| Emergency fallback | Multi-currency debit with a small funded balance | Gives you another live rail if a credit card is blocked or you need immediate cash | Empty balance, unverified limits, or an untested app can still leave you stuck |

The key warning: a credit card at an ATM is usually the wrong tool. A no-foreign-transaction-fee card can still handle cash withdrawals under separate cash-advance terms, with different fee and interest treatment than purchases. Verify current cash-advance terms in your cardholder agreement and pricing page before departure.

Think in provider category first, then brand. Wise and Revolut are useful examples, but the practical standard is a multi-currency account provider that shows conversion cost clearly, supports local withdrawals, and shows exact fees before you confirm. Wise says it uses the mid-market rate and positions its card for spending in 40+ currencies; its ATM treatment is account-level and monthly. On the US fee page, that includes 2 free withdrawals each month when total withdrawals stay within 100 USD, then 1.5 USD per withdrawal and 2% of any amount over 100 USD.

Revolut's US Standard fee page reinforces why live-term checks matter. It says out-of-network ATM withdrawals can cost up to 2%, and adding money by domestic personal credit card can cost up to 3%, with possible extra issuer charges. It also states exact fees are shown in-app, lists a last-updated date of November 18, 2025, and says the Cardholder Agreement governs if terms conflict.

Run a simple local ops checklist#

- Fund before you fly.

Move money from your bank account ahead of time, not via last-minute credit-card top-up.

- Convert when you can review the numbers calmly.

Handle conversion in-app when rate and fees are visible, not at an airport ATM under time pressure.

- Plan withdrawals by month, not one transaction at a time.

If your provider tracks ATM treatment monthly, batch and time withdrawals deliberately, and verify current provider limits in official provider records before you set a withdrawal plan.

- Keep a small contingency buffer.

Hold enough for taxis, tips, or cash-only vendors, but not so much that a card-loss or app-access issue creates unnecessary exposure.

For a step-by-step walkthrough, see The Best Debit Cards with No Foreign Transaction Fees.

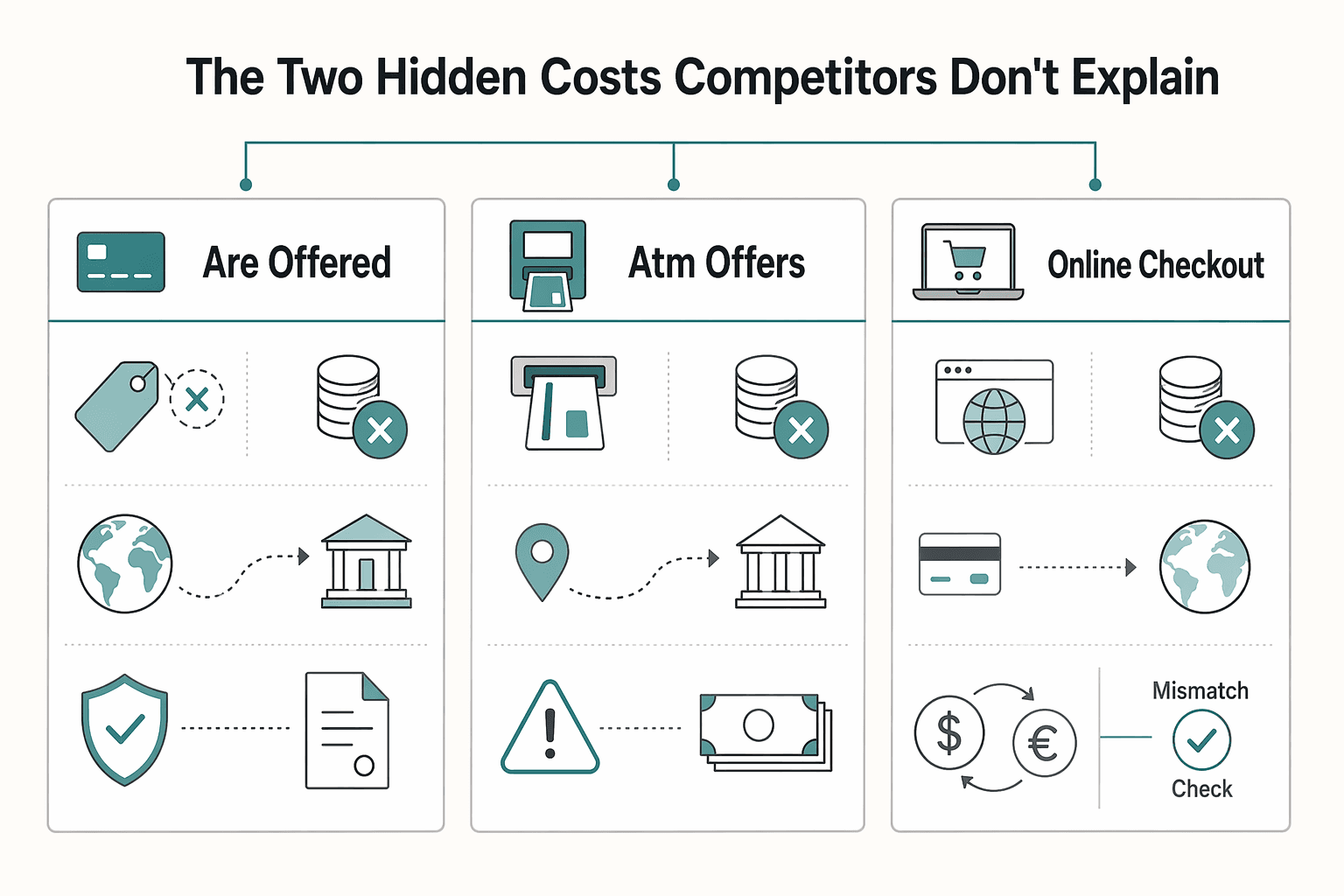

Beyond "No Fees": The Two Hidden Costs Competitors Don't Explain#

"No foreign transaction fee" only removes one cost layer. You still need to manage two separate risks on every international purchase: issuer fees and conversion-path costs.

- Issuer fee is not the same as conversion cost

A no-foreign-transaction-fee card removes the issuer surcharge on international purchases (commonly described as about 2-3% or around 3%). That matters because issuer fees can compound fast if you spend internationally.

But conversion still happens on non-USD purchases, and that conversion path may include a margin. So before you travel, verify both lines in current terms: foreign transaction fee and currency conversion fee/rate language; any spread range needs official issuer or network verification before use.

- The conversion choice at checkout can change your cost control

The second trap is the currency choice at payment. If a card terminal, ATM, or checkout flow offers your home currency, accepting it can shift conversion control away from your card network.

That does not mean home-currency conversion is always worse in every case. It does mean this is the highest-risk decision point for avoidable conversion costs and weaker rate transparency. Your default should be to stay in local currency unless you have a verified reason not to.

| Prompt shown | Who controls rate | Likely outcome | Your action |

|---|---|---|---|

| You are offered local currency vs. home currency at a card terminal | Home-currency choice: merchant-side processor; local-currency choice: card-network path | Home-currency option can reduce rate transparency and increase conversion cost | Choose local currency; confirm currency on the receipt |

| An ATM offers to convert the withdrawal to home currency | ATM operator if you accept conversion | You may add conversion cost on top of an already sensitive cash transaction | Decline conversion and continue in local currency when available |

| Online checkout offers a converted home-currency total | Merchant or checkout provider if you switch | Cleaner-looking total, but less control over conversion path | Keep local currency; save confirmation details |

Use this rule set on every trip:

- Default to local currency.

- Check the charged currency line before you leave checkout.

- If auto-converted, ask to void and rerun in local currency, then keep the receipt or screenshot.

For a fuller breakdown, read The Best Credit Cards for College Students.

Integrating Your Wallet: Accounting & Compliance for the Business-of-One#

Treat your wallet as an accounting system, not just a payment stack. When each card has one job, you reduce recoding, lower the chance of missing business expenses, and make month-end reconciliation easier.

When personal and business spend are mixed, rework usually shows up in three places: recategorizing charges, missed business expenses, and weaker documentation when you need to support a transaction later. Keep separation as an operating rule, but verify deduction, bookkeeping, and record-retention requirements in your jurisdiction before you lock policy.

| Tool | Best use | Accounting impact | Compliance notes | Common mistake to avoid |

|---|---|---|---|---|

| Business card | Flights, software, contractors, client meals, work subscriptions | Cleaner categorization, easier receipt capture, simpler export to accounting tools | Review issuer terms for international fees, late-payment penalties, and onboarding requirements | Putting personal spend on it "just once" |

| Personal no-FTF card | Groceries, personal transport, tourism, non-business travel | Keeps personal spend out of your business ledger | Do not rely on memory to split mixed charges later | Putting reimbursable client costs on this card |

| Specialist debit for cash | ATM withdrawals and local cash-only purchases | Keeps cash activity in a narrow, reviewable lane | Keep ATM receipts or app records because cash needs stronger support | Using cash for routine business spend without a receipt trail |

If your business card includes card-level controls and receipt matching, turn them on. These features support faster reconciliation and fewer uncategorized transactions. The tradeoff: some business or corporate-style programs can involve heavier approval, added fees, or limits that may not fit early-stage operating needs.

Use this mini-playbook this week:

- Define lanes: business card for business spend, personal card for personal spend, specialist debit for cash.

- Tag accounts: mirror those lanes in your accounting categories from day one.

- Document exceptions: for shared costs, reimbursables, and client travel, save a note, receipt, and who-benefited record.

- Review monthly: reconcile statements, chase missing receipts, and re-check local compliance checkpoints against current official guidance.

If you want a deeper dive, read The Best Business Credit Cards for Freelancers.

Conclusion: You Are Now the CFO of Your Global Business#

Keep it simple: give each payment tool one clear job, and check that job regularly. If you cannot explain what happens when your primary payment method fails, your setup is not finished.

The real win is not chasing one card headline and calling it done. It is building continuity when a payment is declined, cleaner records when you reconcile, and better control when you decide how to pay across borders. One last caution: the support behind this guide is not card-specific, so verify your issuer's current fee disclosures and cardmember terms before you travel.

- Primary spend lane

Use one main payment method for business travel, software, lodging, and other work spend. Its job is clean records first, which means you save the invoice, receipt, and purpose note the same day. If a charge mixes business and personal use, split it at checkout when you can or document the allocation immediately.

- Independent backup lane

Keep a second payment method that is operationally independent from your primary setup. Its job is continuity, not optimization. Before every trip, run a small test transaction, confirm account access, and verify you know your lock/freeze and support steps if something goes wrong.

- Local-cash lane

If you expect cash-only situations, keep a separate tool for withdrawals. Its job is to isolate cash activity so it does not blur into your main ledger. Save the withdrawal record or alert, and avoid using this lane as your everyday default.

Next step: review your current setup, assign each tool a role, write down fallback steps, and verify issuer support details before you leave. This is a reusable spending setup for protecting cash flow and reducing payment risk, not a one-time card pick.

You might also find this useful: A Guide to Notion for Freelance Business Management.

Frequently Asked Questions

What is the difference between a no foreign transaction fee card and the exchange rate?

A no-foreign-transaction-fee card removes the issuer's foreign-use surcharge. It does not lock in a special conversion rate, so the posted exchange rate can still affect your total. When the charge settles, compare the receipt currency and the statement currency.

Should you use a personal or business credit card for international business travel?

Many operators put business spend on a business card and personal spend on a personal card to keep records clearer. If one purchase mixes both, note the split promptly so the record is easier to support later.

What is the simplest resilient wallet setup for a solo operator?

One practical setup is a primary card for business spend, an independent backup card, and a separate debit option for local cash access. Using a backup from a different issuer, and ideally a different one of the four major networks, can reduce single-point dependence. Before a trip, test the backup with a small purchase and confirm you can log in to both card apps. Here is a quick comparison: | Tool | When to use it | Accounting and compliance impact | Failure mode to watch | | --- | --- | --- | --- | | Business credit card | Flights, hotels, software, client meals, work subscriptions, reimbursable travel | Can keep business charges in one clearer record | Mixing in personal spend and needing cleanup later | | Personal no-FTF card | Personal meals, family travel, tourism, private transport | Helps keep non-business charges separate from business records | Using it for work-related costs you need to reconcile later | | Specialist debit tool | ATM withdrawals, cash-only merchants, small local cash needs | Keeps cash activity in a separate lane for review | Treating it like a full replacement for your credit-card setup or skipping ATM records |

Should you use a credit card or a multi-currency debit tool abroad?

A common setup is to use a credit card for most purchases and a debit tool for ATM cash or cash-only situations. The CFPB's 2023 consumer credit card market report has a dedicated section on cash advances, so verify your card's cash-advance terms before using it at an ATM.

How do you avoid Dynamic Currency Conversion?

Check the final posted currency and conversion details on your receipt and statement. If a transaction posts with an unexpected conversion, keep the receipt and contact your issuer through its dispute process. The CFPB's 2023 report includes a dedicated dispute resolution section.

What should you do if your primary card is lost or stolen abroad?

Lock or freeze the card in the issuer app or contact the issuer as soon as possible. Switch to your backup card so travel and work can continue, then review recent transactions and keep records for any disputes.

How should you document mixed-purpose travel purchases?

Split business and personal bookings at checkout whenever you can. If one charge covers both, keep the invoice, itinerary, receipt, and a short note showing who benefited, the business purpose, and how you allocated the cost. Add that note to your accounting record the same day.

How should you use ranked lists when comparing cards in March 2026?

Treat ranked lists as a shortlist, not a final answer. As of March 2026, ranked lists of no-foreign-transaction-fee cards can help you screen candidates, but your core checks are still practical: confirm the fee disclosure, review cash-advance terms, review the dispute process, and make sure the card fits the role you want it to play. If a card looks strong on paper but weakens your backup or bookkeeping setup, skip it.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- congress.gov/event/119th-congress/house-event/LC75086/texttrusted

- dccourts.gov/sites/default/files/matters-docs/FY-2018-Bud...trusted

- dcf.wisconsin.gov/files/publications/pdf/4024.pdftrusted

- dhs.dc.gov/sites/default/files/dc/sites/dhs/page_conten...trusted

- dot.ca.gov/-/media/dot-media/programs/research-innovati...trusted

- fdic.gov/resources/supervision-and-examinations/exami...trusted

- federalreserve.gov/boarddocs/supmanual/cch/cch.pdftrusted

- files.consumerfinance.gov/f/documents/cfpb_consumer-credit-card-market...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Best Business Credit Cards for Freelancers

Pick for reliability first. For a freelancer, the right business card is usually the one that keeps recurring bills moving, keeps records clean, and avoids extra costs when income swings from month to month. Rewards still matter, but they sit on top of those basics. They do not replace them.

The Best Travel Credit Cards for Digital Nomads

Build a three-part card setup (primary, spend, backup) so one failure is less likely to derail your trip or your work. Forget the myth of "one perfect card." You want a system that still works when a terminal declines your card, a transaction gets flagged, or a merchant won't take your usual option.

A Guide to Notion for Freelance Business Management

If your workspace feels busy but fragile, you do not need more pages. You need one connected system. Treat your freelance business like a business-of-one and use Notion as the control layer that connects client decisions, delivery, and billing in one place.