Quick Answer

Choose a student card for durability first, then rewards second. For the best credit cards for college students, prioritize network fit, foreign transaction policy, and no annual fee, and confirm terms directly in issuer disclosures before you submit. Apply for one card, not several, and immediately set autopay for the full statement balance plus payment alerts. Keep spending tied to cash already in checking and review statements consistently so the account builds useful history instead of expensive mistakes.

The Best Student Credit Cards: Your First Strategic Financial Asset#

If you're comparing student credit card recommendations, do not chase the flashiest perk. Judge reliability, fee risk, and what happens after the student label stops mattering.

Your first card matters. The wrong pick can trap you in a product you outgrow fast. The right one gives you a clean base for building credit and making easier decisions later.

A useful starting split is simple: are you choosing a campus perk, or are you choosing a financial asset?

| Choice lens | Likely outcome | Main risk | Best fit |

|---|---|---|---|

| Perk-first card choice | You optimize for a headline feature like cash back or a promo label | You miss fees, weak long-term fit, or limited usefulness after school | You only want short-term value and plan to revisit the decision soon |

| Asset-first card choice | You optimize for durability, cost control, and future flexibility | You may pass on a slightly richer short-term perk | You want a card that still makes sense after graduation |

Before you compare cards, compare the sources recommending them. That sounds dull, but it is one of the fastest ways to avoid weak picks. Forbes marks its student card page as "Audited & Verified: Mar 3, 2026, 4:45am" and says partner-link commissions do not affect editorial evaluations. Money, published Mar 5, 2026, is also useful, but it states that research and financial considerations may affect how brands are displayed and that not all brands are included.

Do not dismiss either source for that alone. Just read the disclosure before you trust the ranking. Here is the lens the rest of this article builds on:

- Credit-building fundamentals

Start with staying power, not excitement. Labels like "No Annual Fee" and "0% APR" can help you narrow the field, but they are not the decision. The real checkpoint is whether the card still looks sensible after the promo appeal fades.

- Disclosure language and coverage limits

Read how the roundup explains incentives and scope. Statements like "commissions do not affect editorial evaluations" and "not all brands are included" should shape how much weight you give any ranking.

- Source accessibility

Treat any single list as incomplete. If you cannot cross-check a detail against current issuer terms or other major roundups, do not lean on it.

- Account management discipline

A strong card can still produce a bad result if your setup is sloppy. The common failure mode is choosing for perks, then never reviewing statements, payment settings, or fee disclosures. We will get to the habit side later, because the card and the way you manage it are inseparable.

That is the frame for the rest of the article. Think in decades, not semesters, then narrow down what actually makes a student card durable, usable, and low risk.

Why Your First Credit Card is a 10-Year Decision, Not a 4-Year Convenience#

If you can open a no-fee student card and manage it cleanly, starting earlier gives lenders a longer record to review later. The benefit is not a campus perk. It is more documented account behavior over time, without promising any specific score or approval result.

1. Start early only if you can run it well#

The clock starts when the account opens, and you cannot backfill that history later. What you can control is behavior from month one: on-time payments, clean account management, and no penalty events.

| Scenario | Lender signal | Borrowing flexibility | Likely upgrade path |

|---|---|---|---|

| Start now and manage responsibly | Longer, cleaner record of account behavior | More room to apply when you need bigger financial tools | Better odds of moving from a starter card to another no-fee or travel card if your issuer allows product changes |

| Wait until after graduation | Shorter visible record when you first need broader access | Fewer data points for lenders to evaluate | Upgrade path can still happen, but the timeline starts later |

| Start now but miss payments or trigger penalties | Negative early signals can outweigh the timing advantage | Flexibility may tighten while you rebuild consistency | Product upgrades are often delayed or less favorable |

2. Choose a starter card with a realistic next step#

Your first card should have a practical progression: starter card -> clean history -> product change or upgrade options (if offered). That is usually more useful than chasing a short-lived first-year perk.

Before you apply, confirm the annual-fee terms and whether the issuer offers a path into other cards later. Also save your application confirmation, first statement date, and autopay confirmation in one folder so you can verify account history if issues come up.

3. Focus on account behavior this year, not scoring theory#

A card account shows how you manage an open credit line over repeated billing cycles. You do not need model-level scoring theory to execute the basics: pay the full statement balance on time, keep the reported balance modest at statement close, and avoid late payments, returned payments, and over-limit problems.

That behavior-first approach is consistent with the bank-side framing in the OCC Credit Card Lending booklet (Version 2.0, April 2021), which includes Scoring Models and account-management topics such as Over-Limit Authorizations and Account Closures (with a March 20, 2025 update note referencing Bulletin 2025-4). In short: approval is step one; ongoing account handling is the long game.

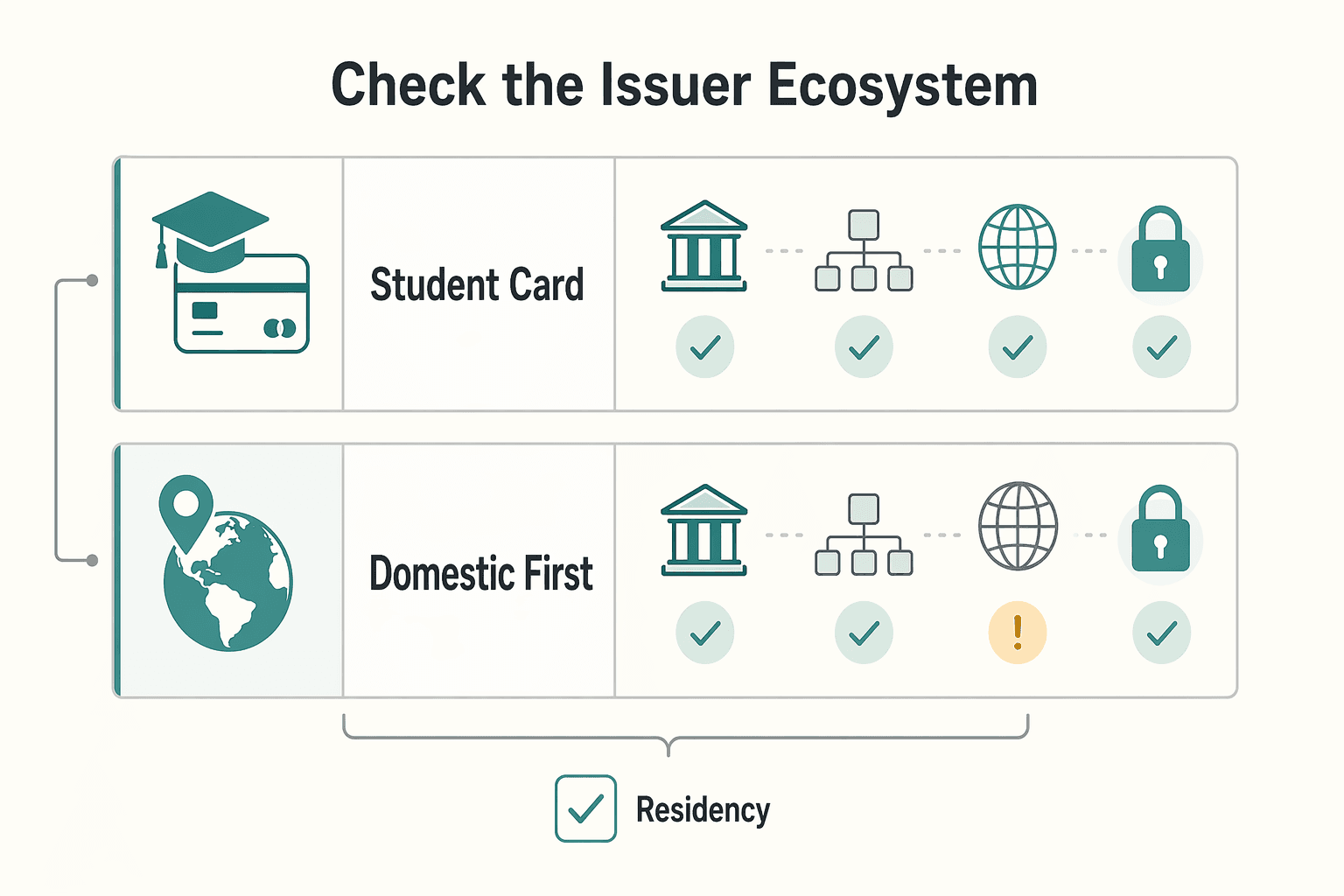

The 'Global-Ready' Checklist: Choosing for a Career in Berlin, Not Just the Campus Bookstore#

If international use is even moderately likely for you, choose a student card by fit for your real spending pattern, not by a generic ranking. Some cards are strong for mostly domestic use and less convenient for international use, and that can still be the right choice depending on your plan.

1. Check the network first#

Before you compare rewards, confirm the network and ask a practical question: would you trust this card as your primary card for the places and merchants you are most likely to use? Treat this as a pre-application verification step on the issuer page and card agreement, not an assumption based on campus use. If your spending is mostly domestic, a domestic-first fit may be fine. If you expect travel or internationally billed merchants, prioritize network fit earlier in your filter.

2. Check foreign-use cost, including subscriptions#

Your second test is the foreign transaction policy for any charge that may be processed outside the US, including recurring subscriptions. Do not guess here; verify the current terms in the card agreement.

If you are planning Germany or study abroad, keep your process current. The CSU Germany Participant Guide includes a Money Matters & Banking section and notes that the guide is revised annually, while the available excerpt is from 2014-2015. Re-verify both program and card terms each cycle. Keep your card agreement and fee screenshot with your program documents so checkpoints like Bank Statement and Vollmacht (Power of Attorney) are easier to handle on deadline.

3. Check the issuer ecosystem, not just the starter card#

Your first card is also your entry into an issuer relationship, so verify whether the issuer has a realistic path you can use after the student phase. You are not predicting an exact future product today. You are avoiding avoidable friction later.

| Card profile | Network | Foreign-use cost | Travel-readiness | Upgrade path within issuer family |

|---|---|---|---|---|

| Student card from a large issuer (Visa) | Verify exact product network | Verify current foreign transaction fee in the terms | Best fit if your plan may include travel or internationally billed merchants, after you verify your likely acceptance points | Verify whether the issuer offers no-fee non-student options you could keep later |

| Student card from a national issuer (Mastercard) | Verify exact product network | Verify current foreign transaction fee in the terms | Best fit for mixed domestic and international scenarios when your specific use points check out | Verify whether the issuer has a clear post-student card path |

| Domestic-first student card profile | Verify exact product network | Verify current foreign transaction fee in the terms | Best fit when your spending is mostly domestic and international use is limited or secondary | Verify long-term options before applying |

How to use this checklist: rank your likely use in this order, domestic spending, travel, subscriptions billed internationally. Then choose the card that minimizes avoidable friction and avoidable fees for that mix.

Related: The Best Travel Credit Cards for Digital Nomads.

The Bulletproof Credit System: Automate Good Habits, Eliminate Risk#

After you pick the card, the goal is operational: set controls that reduce avoidable mistakes and review them consistently. Use these three actions as a weekly system, not a one-time setup.

1. Turn on autopay for the full statement balance#

Start by enabling autopay for the full statement balance from the checking account you actively use. Confirm the exact autopay option before saving, then verify your due date and add a reminder 5 to 7 days before it to check cash and account status.

| Stage | Checks | Follow-up |

|---|---|---|

| Before saving | Confirm the exact autopay option before saving; verify your due date; add a reminder 5 to 7 days before it | Check cash and account status at that reminder |

| After the first statement generates | Confirm a payment is scheduled, alerts are on, and the payment account is still valid | Treat autopay as untrusted until you recheck it if anything changes |

| If anything changes or a payment fails | Examples in the section are a bank switch, failed link, or low balance | Make a same-day manual payment and then fix the setup |

After your first statement generates, confirm a payment is scheduled, alerts are on, and the payment account is still valid. If anything changes (bank switch, failed link, low balance), treat autopay as untrusted until you recheck it. If a payment fails, make a same-day manual payment and then fix the setup.

2. Spend only what your checking account can cover this week#

Use checking-account reality as your spending limit, not the card limit. Each week, review checking first, account for bills due before your next review, then compare what is left with your current card balance and planned spend.

Set simple category caps for the week (for example: food, transport, fun) and pause card use in any category once you hit the cap. This keeps day-to-day card use tied to cash you can cover now, not cash you expect later.

3. Control the balance that gets reported#

Use a verified process, not a fixed rule you picked up online.

Track your statement closing date and check your balance a few days before it. If needed, make a manual payment before closing, then confirm when it posts and what balance appears on the statement. Because issuer behavior can differ, verify the timing in your account details or with support instead of assuming one pattern.

| Common failure mode | Early warning signal | Immediate corrective action |

|---|---|---|

| Autopay set incorrectly or turned off | No scheduled payment appears after statement generates | Re-enable full statement balance autopay and make a manual payment if needed |

| Checking account cannot cover payment | Balance looks tight 5 to 7 days before due date | Transfer funds, cut discretionary spend, and recheck autopay source |

| Statement balance is higher than planned | Closing date arrives with more balance than expected | Track closing date, make an earlier manual payment, and confirm posting timing |

When these controls run consistently, your card supports cleaner financial habits and sets up the long-term outcomes in the next section.

From Campus to Corporation: Your Professional Launchpad#

If you run your student card with the same discipline every month, you do not get guarantees, but you do improve your odds of better options after graduation. Think of this as a practical upgrade path, not a status move.

| Trigger | Action | Record |

|---|---|---|

| Repeat client expenses | Split the flows | Receipts matched to invoices |

| Reimbursable purchases | Split the flows | Receipts matched to reimbursement requests |

| Side-income costs | Split the flows | Receipts matched to expense categories |

- Keep your first card as a clean history anchor.

- Add or upgrade only when your work needs change (for example, regular travel or reimbursable expenses).

- Choose for protections and flexibility you will actually use, not prestige.

Before any new application, verify the current annual fee, protections, and core terms. If you see hard approval-score claims online, treat them as unverified unless you can confirm them. That caution matters because credit card lending is risk-managed, and issuer account management can include line increases or decreases, over-limit decisions, repricing, and closures.

Separate personal and business spend as soon as business charges are recurring. The trigger is simple: once you have repeat client expenses, reimbursable purchases, or side-income costs, split the flows.

Use one payment method for personal spending and one for business activity. Keep receipts matched to invoices, reimbursement requests, or expense categories. That makes reporting cleaner and supports your first business-card application with records you can defend, even though approvals remain conditional and issuer criteria vary.

Formal card programs reinforce this boundary: P-Cards are business-only, and policy violations can lead to revoked card privileges and disciplinary action. Treat any future corporate or commercial card the same way: business-only spend, reconciled quickly.

A clean card history can also support credibility outside bank products, including housing or insurance decisions, but only as one part of a broader file. It will not override income, reserves, deposits, or other underwriting factors.

Keep the downside in view, too. The GAO's historical $2,000 at 19 percent repayment example is a reminder that revolving debt can erase progress quickly, and the same report noted limited student-card research. So treat post-grad outcomes as improved odds, not promises.

That sets up the next practical questions, like whether to keep your first card open, when to request a limit increase, and when a second card is useful. The FAQ covers those directly.

We covered this in detail in The Best Bank Accounts for College Students.

Your First Executive Decision#

Treat this as a pick-and-commit decision: verify terms, choose one card, and run it with tight controls.

| Step | What to do | Details |

|---|---|---|

| Shortlist candidates | Keep it practical: everyday spending, possible travel, and rewards you will actually redeem | Shortlist two candidates you would realistically use |

| Verify the official disclosure | Open each card's Rates & Fees link | Capture Network, Foreign transaction fee, Annual fee, and APR range from that page |

| Check approval fit | Use current eligibility language, not forum myths | Common prerequisites include being 18+, being enrolled in school, and having enough independent income to cover monthly payments |

| Apply once and set controls | Set autopay and payment alerts in the app, add a spending cap you can cover from cash, and confirm card-lock and $0 Fraud Liability language | The bigger risk is late payments or maxing out your line, not missing an extra 1% to 5% in rewards |

-

Shortlist two candidates you would realistically use. Keep it practical: everyday spending, possible travel, and rewards you will actually redeem. As one baseline example from a Mastercard student listing, Capital One Quicksilver Student shows 1.5% cash back, $50 after $100 in the first three months, 18.49% to 28.49% (Variable) APR, and $0 annual fee with no foreign transaction fees. Recheck the current issuer page before you apply.

-

Verify the terms in the official disclosure before you submit. Open each card's Rates & Fees link and capture the exact details from that page: Network, Foreign transaction fee, Annual fee, and APR range.

-

Check approval fit from current eligibility language, not forum myths. Common prerequisites include being 18+, being enrolled in school, and having enough independent income to cover monthly payments. Also remember that credit score alone does not guarantee approval.

-

Apply for one card, then install risk controls this week. Set autopay and payment alerts in the app, add a spending cap you can cover from cash, and confirm card-lock and $0 Fraud Liability language in your account terms. The bigger risk is late payments or maxing out your line, not missing an extra 1% to 5% in rewards.

Today: finalize your shortlist and verify terms. This week: apply once and set controls. Monthly: review your statement and stop comparing.

For implementation, continue with How to Build Credit in College. Keep The Best Credit Cards with No Foreign Transaction Fees and business/travel card paths for later, when your spending actually changes. If you need program-level confirmation, Talk to Gruv.

Frequently Asked Questions

Am I even eligible for a student card?

Yes, a first card can still make sense if you have limited credit history and plan to manage it responsibly. Start with one card, not several, and read the issuer’s Truth in Lending Act disclosures before you apply so you understand the core costs and terms. The mistake to avoid is overspending.

What improves my approval odds?

No one can promise approval, and you should ignore claims about guaranteed score cutoffs. A safer approach is to start with one card rather than trying several at once, and confirm current eligibility language on the issuer page before you submit.

What actually helps me build credit once I’m approved?

The most important behavior is simple: pay on time, every time. MyFICO’s student guidance is blunt that one late payment can hurt someone with a short file, so keep balances low, review each statement, and do not spend just to “show activity.” If you want a deeper setup, see How to Build Credit in College.

Should I care more about fees or rewards?

Treat “best card” lists as a starting point, not a final answer. Verify the current annual fee, foreign transaction fee policy, and rewards structure in the issuer terms.

How do I choose between two good options?

Use a simple tie-break: spending pattern, travel use, statement discipline, and how much complexity you will actually manage. If one card has simpler rewards and you know you will not track categories, pick simplicity. If you travel, verify network acceptance and foreign-fee policy directly on the issuer page before deciding.

What should I do if I’m denied, or after I get approved?

After a denial, do not panic-apply elsewhere. Review the reason given and fix the issue you can fix. If your current limit later feels too tight, ask the existing issuer for a credit line increase instead of rushing into a second card. Once approved, pay on time, keep balances low, and review the account regularly before you consider bigger steps.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- babson.edu/business-and-financial-services/procurement/...trusted

- blogs.missouristate.edu/bearsfamilies/2017/10/23/ask-the-experts-bes...trusted

- csuip.calstate.edu/_customtags/ct_FileRetrieve.cfmtrusted

- dcf.wisconsin.gov/manuals/w-2-manual/Production/assets/pdf/W2M...trusted

- detroitmi.gov/sites/detroitmi.localhost/files/2025-11/2025...trusted

- digitalcommons.chapman.edu/cgi/viewcontent.cgitrusted

- ecfr.gov/current/title-2/subtitle-A/chapter-II/part-2...trusted

- files.consumerfinance.gov/f/201512_cfpb_report-the-consumer-credit-car...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Best Business Credit Cards for Freelancers

Pick for reliability first. For a freelancer, the right business card is usually the one that keeps recurring bills moving, keeps records clean, and avoids extra costs when income swings from month to month. Rewards still matter, but they sit on top of those basics. They do not replace them.

The Best Travel Credit Cards for Digital Nomads

Build a three-part card setup (primary, spend, backup) so one failure is less likely to derail your trip or your work. Forget the myth of "one perfect card." You want a system that still works when a terminal declines your card, a transaction gets flagged, or a merchant won't take your usual option.

How to Build Credit in College

Forget the usual advice about "student" credit. You are not just looking for a starter card. You are building the financial track record for a business of one: you. That profile shapes how lenders, landlords, and card issuers deal with you long after school.