Quick Answer

Choose by sequence, not hype: screen for business usability first, then match rewards to your booking pattern, then confirm risk controls. For the best business credit cards for hotel points, the article’s checkpoint is simple: loyalty tends to fit when most stays cluster with one chain, while flexible points protect you when travel shifts by client city or rate. Before submitting an application, verify current issuer terms and set up receipt capture and expense labeling from day one.

Beyond Perks: A Strategic Framework for Choosing the Best Business Hotel Credit Card#

Choosing among the best business credit cards for hotel points is not just about perks. It is an operating decision: which card fits how you book travel and manage expenses when plans change.

| Tier | What it checks | Key differentiator |

|---|---|---|

| Foundation | Fit for your spending habits and overnight-stay patterns | Rules out cards that look strong on paper but add day-to-day friction |

| Engine | Whether a co-branded option or a flexible travel card matches how you travel | Separates a focused loyalty play from broader flexibility |

| Shield | Whether comparison risk is under control before you apply | Keeps a sponsored ranking from being mistaken for a complete shortlist |

That matters most if you are a freelancer, creator, or small team with uneven travel patterns. One month you might book three client-site stays, and the next month you barely travel. In that setup, the wrong card can create drag fast. You can end up with rewards tied to one chain, comparison pages shaped by partner compensation, or a choice based on a roundup that may not include every available offer.

A better way through that is to use a three-tier decision path instead of starting with bonus hype. You will use these same filters throughout the guide.

- Tier 1: Foundation

Start with whether the card works as a dependable business payment tool. Check fit against your actual spending habits and overnight-stay patterns, not just the marketing headline. Key differentiator: this tier helps you rule out cards that look strong on paper but add day-to-day friction once you start booking travel and reconciling expenses.

- Tier 2: Engine

Next, decide what kind of rewards engine matches how you travel. If your stays cluster around one brand, a co-branded option may make sense. If your trips are less predictable, a flexible travel card can be the better hedge. Key differentiator: this is where you separate a focused loyalty play from broader flexibility, including the fact that Marriott options are not limited to one issuer since Marriott cards are issued by both Chase and American Express, and a flexible travel card can still support Marriott stays.

- Tier 3: Shield

Last, check comparison risk before you apply. Hotel card roundups can be useful, but some explicitly disclose that compensation may affect placement and that they do not include every card on the market. Key differentiator: this tier keeps you from mistaking a sponsored ranking for a complete shortlist.

One practical checkpoint is freshness. If you are comparing cards in 2026, confirm the page was updated recently before you trust it. For example, one Marriott roundup is framed as a March 2026 comparison and shows an update date of Feb. 27, 2026. A Hilton guide shows Updated Jan 9, 2026 and marks itself Fact Checked. That does not make either source complete, but it is a better signal than an undated listicle.

A common risk is choosing a card because the hotel brand is familiar, then finding your stays are too mixed to get real value from that setup. So before you compare Marriott, Hilton, or any other program, start with Tier 1. It should eliminate bad fits before rewards enter the conversation.

If you want a deeper dive, read The Best Business Credit Cards for Freelancers. Want a quick next step? Try the free invoice generator.

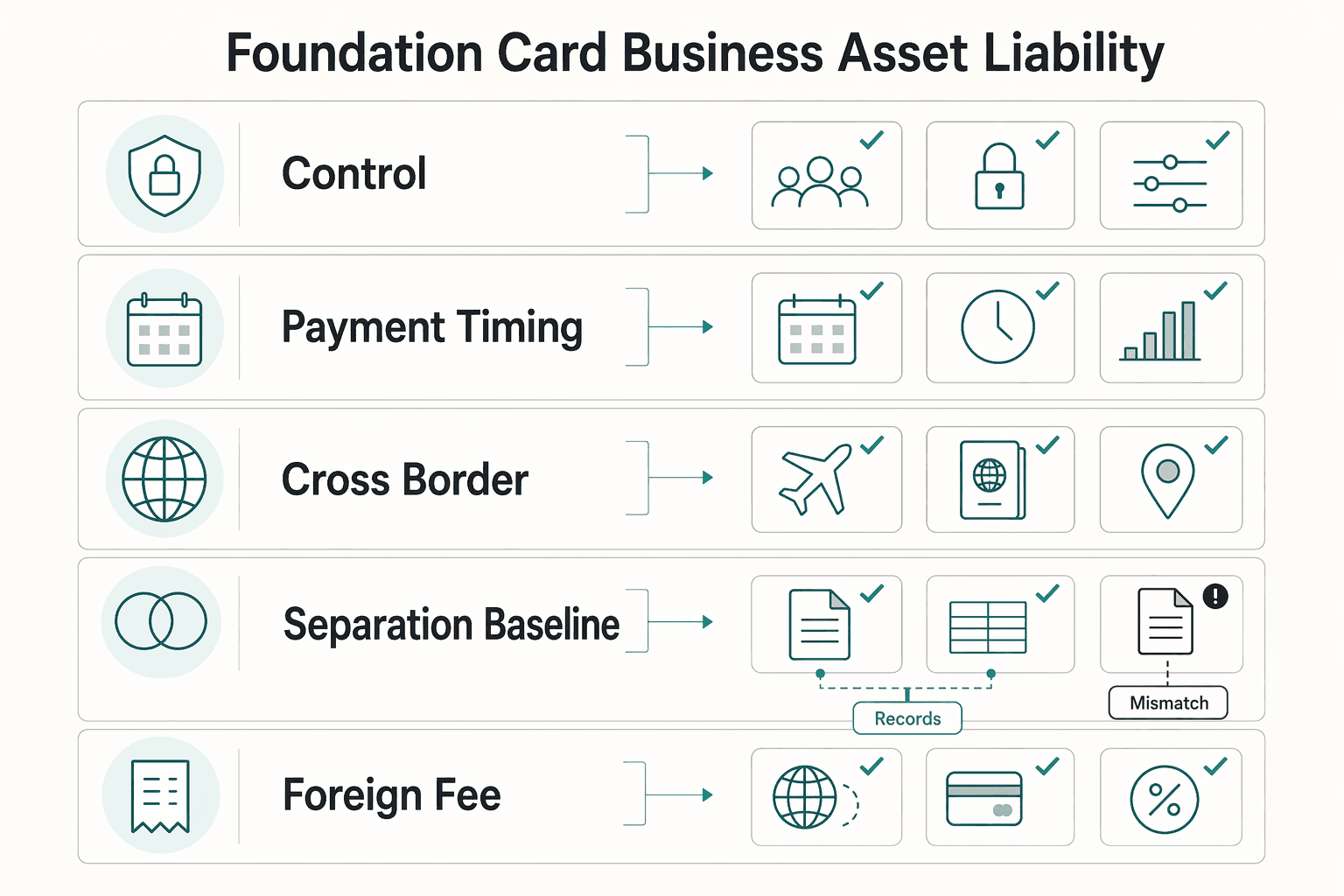

Tier 1: The Foundation - Is Your Card a Business Asset or a Liability?#

Tier 1 is a pass/fail screen: if a card slows bookkeeping, strains cash flow, or blurs business and personal spend, eliminate it before you compare rewards.

| Check | What to verify | Why it matters |

|---|---|---|

| Expense controls | Receipt capture, category editing, clean export, and employee user access if other people book travel | Reduces cleanup and shortens month-end |

| Payment timing | Statement-close logic, due-date options, autopay controls, and any due-date-change process | Protects working capital when travel spend arrives before client payments |

| Cross-border checks | Foreign fee policy, usable statement detail, dispute workflow, and travel support | Helps prevent surprises on international travel and when charges go wrong |

| Separation baseline | Dedicated business use, whether qualification depends on personal credit, and whether a personal guarantee is required | Keeps cleaner records and supports business credit development; it does not by itself guarantee legal protection |

- Expense controls that shorten month-end

Your card should reduce close work, not create cleanup. Check whether you can capture receipts, apply useful categories, sync or export cleanly into your accounting workflow, and control who can spend. If other people book travel for you, confirm whether the card allows employee user access, since some small-business cards do.

Key differentiator: verify these features in real product docs or app flows, not just marketing copy. Confirm receipt attachment, category editing, export quality, and permissions before you apply.

- Payment timing that protects working capital

If travel spend hits before client payments arrive, timing matters more than points headlines. Business cards can support cash flow through short-term financing, but only if you manage statement timing and payment controls around your invoicing cycle.

Key differentiator: review current payment due dates and terms before you apply. Business cards may have weaker regulatory protections than personal cards, so confirm statement-close logic, due-date options, autopay controls, and any due-date-change process in current issuer terms. If timing details are unclear, treat that as a yellow flag and re-verify directly with the issuer because published offer details can go stale.

- Cross-border checks that prevent surprises

For hotel travel, check more than rewards and fees. You need clarity on foreign-fee policy, statement detail, dispute handling, and support channels when bookings or charges go wrong.

| Checkpoint | What to verify for each candidate card | Why it matters |

|---|---|---|

| Foreign fee policy | Current foreign transaction fee in the latest terms or pricing page; verify current terms | Helps prevent margin loss on international travel spend |

| Settlement clarity | Whether statements show usable merchant, currency, and posted transaction detail; verify | Makes reconciliation and charge explanation easier |

| Dispute workflow | Where disputes start, required documentation, and status tracking; verify | Improves response when hotels overcharge or post duplicates |

| Travel support | Whether travel-related support is listed and how to reach it; verify | Helps when reservation or billing issues need fast action |

Key differentiator: use this as a live checklist for each card, not a mental note.

- Separation as a risk-control baseline

A dedicated business card helps you keep cleaner records, maintain a clearer boundary between business and personal spend, and support business credit development. It does not, by itself, guarantee legal protection.

Key differentiator: set expectations correctly. Qualification often depends on your personal credit, and a personal guarantee is commonly required. Use the card to improve control and documentation, not to overclaim legal outcomes.

If a card fails any Tier 1 check, stop there. If it passes, move to Tier 2 and choose your rewards engine: loyalty concentration or flexibility hedge. Related: The Best Travel Credit Cards for Digital Nomads.

Tier 2: The Engine - The 'Loyalty Play' vs. The 'Flexibility Hedge'#

Your rewards engine should match how predictable your bookings are. Use the 70% rule: if about 70% of your hotel spend lands with one brand, a co-branded loyalty path is usually stronger; if your stays move by client city, rate, or availability, a flexibility hedge is usually safer.

1. Loyalty play#

Choose loyalty when your travel pattern is stable enough to compound value inside one program. In practice, that means your core cities and client trips repeatedly line up with one chain, and you will actually use day-of-travel benefits that reduce friction on real trips.

For the common co-branded options, fit matters more than marketing headlines:

| Card path | What it is best at | Practical tradeoff to verify |

|---|---|---|

| Marriott Bonvoy Business | Broad footprint convenience in many markets | Award value and availability can vary; do not assume footprint equals redemption quality |

| Hilton Honors Business | Broad footprint and easy point accumulation | One source describes easier earning but weaker redemption leverage in many scenarios |

| World of Hyatt Business | Higher potential redemption value in the right use case | Smaller footprint can limit where the value is usable in your actual routes |

One source estimates Marriott and Hilton at nearly 9,000 properties each, versus about 1,500 for Hyatt (less than 20% of Marriott's count). The same source also cites rough value ranges of 2.0 cents (Hyatt), 0.7-0.8 cents (Marriott), and 0.5 cents (Hilton), which are directional, not guaranteed.

Use a quick reality check before committing: group your last 12 months of stays by brand and city, then mark where your preferred chain failed on price, location, or usable inventory. This catches the footprint fallacy early.

| Decision framework | Loyalty | Flexibility | Hybrid |

|---|---|---|---|

| Network fit | Best when one brand covers about 70% of stays | Best when stays shift by client, city, or timing | Best when one brand is useful but not dominant |

| Redemption control | Bound to one program's award rules and availability | More optionality across partners, with transfer friction | Keep one hotel base while preserving options |

| Fee tolerance | Verify the current fee against actual brand concentration | Verify the current fee against the flexibility you will use | Verify both fees against the overlap you will actually use |

| Operational risk | High balances can still underperform if redemption quality is weak | One-way transfers and partner mismatch can strand value | Split spend and duplicate fees can complicate reconciliation |

2. Flexibility hedge#

Pick flexibility when you need protection against unpredictable routing and uneven hotel availability. A flexible-points card lets you decide later, trip by trip, instead of pre-committing every stay to one network.

Keep the mechanics clear: partner transfers can add friction, and transfers may be one-way. One source notes Hyatt's cleaner links with Chase and Bilt, while Marriott spans Amex, Chase, and Bilt but can lose value in conversion. So flexibility helps most when you confirm the partner path before moving points, not after.

3. Hybrid stack#

If your travel is mixed, use a two-card operating model: one card for earning flexibility, one hotel card for baseline in-program benefits where you stay most.

Use one simple rule:

- Put in-chain hotel stays on the hotel card when you want program-linked benefits and cleaner stay tracking.

- Put everything else (including out-of-chain hotels) on the flexible card.

Before Tier 3, confirm these risk controls:

- You validated the 70% rule with real spend data, not memory.

- You rechecked current terms, partner lists, and benefit details.

- Your statements preserve a time-stamped audit trail for cross-border and compliance workflows.

- Your team has a written card-usage rule by purchase type so reconciliation stays clean.

You might also find this useful: A Guide to Notion for Freelance Business Management.

Tier 3: The Shield - Mitigating Risk and Compliance Anxiety#

Before you optimize rewards, make sure your setup can withstand review. If your process creates mixed spending, weak records, or tax guesswork, the card becomes operational risk instead of an asset.

1. Classify rewards before tax season#

Classify rewards as you earn them: spend-based rewards, welcome incentives tied to required spend, and referral or other promotional payouts. This keeps year-end review cleaner and stops you from treating every points deposit or credit the same way.

Do not decide filing treatment from memory or roundups. Confirm current treatment in issuer terms and year-end documents, then review with a qualified tax professional before filing. For unusual promotions, log placeholders to verify later: [current issuer reporting trigger], [form type if issued], [tax treatment to confirm].

When you validate compliance references, start with official HTTPS .gov sources. For Truth in Lending context, use the Federal Reserve FRRS page for CFPB official staff commentary on Regulation Z; Sections 1026.1 and 1026.2 are practical orientation points. Use that as source validation, not as a shortcut for tax treatment.

2. Build a record set, not just a statement archive#

Treat statements as one layer of a time-stamped audit trail, not the whole file. For deduction support and any residency or travel-date substantiation, keep records that align across documents.

| Record element | What to keep | Why it matters |

|---|---|---|

| Merchant detail | Statement detail that shows the merchant, not only a generic processor label | Helps preserve a clean link between the charge and the related trip |

| Purpose tag | A business-purpose tag for each charge, such as client meeting, conference, lodging, or transit | Supports clearer classification and deduction records |

| Supporting receipt | Attach the receipt when available, especially on higher-value travel expenses | Strengthens substantiation when the statement alone is not enough |

| Monthly storage | One consistent storage location each month, preferably connected to the accounting workflow | Supports a time-stamped audit trail |

Use a minimum quality checklist:

- merchant detail visible on the statement (not only a generic processor label)

- purpose tag for each charge (for example: client meeting, conference, lodging, transit)

- supporting receipt attached when available, especially on higher-value travel expenses

- one consistent storage location each month, preferably connected to your accounting workflow

The common failure pattern is simple: the charge exists, but there is no receipt, no purpose tag, and no clean link to the related trip.

3. Treat separation as a control, not a preference#

Use a dedicated business card as your default financial firewall. Keep business hotel, airfare, software, and client-related travel on that card, and keep personal spending off it unless you apply a documented exception process.

If mixed expenses happen, define the handling path in advance: split, reimburse, or reclassify, then reconcile on a fixed cadence (for example, at statement close). That recurring check catches coding errors, missing receipts, and personal charges before they accumulate.

Before final card selection, require three controls: classified rewards, a usable audit trail, and a dedicated-card policy with regular reconciliation. If a card setup cannot support those basics, do not optimize it yet.

We covered this in detail in The Best Tools for Tracking Your Credit Card Points and Miles.

Your Card is Your Co-Pilot: Making the Final Decision#

Make your final call in this order: confirm your operating baseline, match the rewards model to your real booking pattern, then verify risk controls before you apply.

Foundation#

Treat the card as an operating tool first. A business credit card should help you manage expenses and extend purchasing power, not add avoidable friction to your workflow.

Before you trust any ranking, check the issuer page directly for current rates, fees, and terms. Comparison pages can help you shortlist, but disclosure language varies, so use them as inputs, not as your final decision-maker.

Engine#

Pick the path that fits how you actually book hotels.

| Path | Best fit | Verify before applying | Tradeoff |

|---|---|---|---|

| Brand-loyalty card | Most stays concentrate with one hotel program | Offer is still live, current terms, and fit for your business budget | Stronger program alignment, less flexibility if travel patterns change |

| Flexible-points card | Stays vary by client, city, or price | Current redemption/transfer options, live offer timing, and terms | More flexibility, fewer hotel-program-specific advantages |

Offer timing matters. Limited-time promotions and persistent offers are often mixed together, so confirm what is live right now before you submit an application. Recency checks like "Updated March 2, 2026" or "Audited & Verified: Mar 3, 2026, 4:47am" help, but issuer terms are the final source of truth.

Shield#

Do not apply if you are already carrying debt, and do not charge more than you can pay off immediately just to chase rewards.

Choose the card type that matches your booking reality. Verify live terms and fees on the issuer page. Set up receipt capture and clear expense labeling on day one. Review your first two statements to catch friction early and confirm the card is actually helping operations.

For a step-by-step walkthrough, see The best business credit cards for earning airline miles.

Frequently Asked Questions

Are the best business credit cards for hotel points always co-branded hotel cards?

No. Hotel business card value depends heavily on where you actually stay. If your hotel spend is scattered across brands, a single loyalty card may be less useful than perk headlines suggest.

How should I choose between a co-branded hotel card and a transferable-points card?

Choose a co-branded hotel card when your stays consistently cluster with one chain and you will use hotel perks like free stays, elite status, or room-upgrade benefits. If your travel is less predictable, compare broader options and evaluate the card as part of your full expense system, not rewards alone. Confirm current issuer terms and recent March 2026 comparison pages before you decide.

Do foreign transaction fees matter for business travel cards?

They can, depending on the card and where you spend. Verify the exact fee policy in the issuer’s current pricing and terms instead of assuming a travel card waives it. Check the latest disclosure and how any fees flow through your bookkeeping.

Should I keep hotel spend on a business card even if I already have a strong personal travel card?

Yes, if you want cleaner records and easier reconciliation. Keeping lodging, airfare, and client travel on a business card can reduce mixing business and personal charges and make statement lines easier to match with receipts and trip records.

Can a big bonus or premium perk set hurt cashflow?

It can, especially if you choose mainly by rewards rates and annual-fee optics instead of operational fit. Stress-test the card against your normal billing cycle and payment reliability first. A 200,000-point headline, a 1-5X earn range, or even an $895 annual fee only works if it fits your cashflow discipline.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 6 external sources outside the trusted-domain allowlist.

- federalreserve.gov/frrs/regulations/consumer-financial-protecti...trusted

- in.gov/doe/files/2024-2025-High-School-Course-Title...trusted

- alabar.org/members/benefitsexternal

- brex.com/spend-trends/corporate-credit-cards/best-bus...external

- businessinsider.com/personal-finance/credit-cards/best-small-bus...external

- eplaneai.com/es/news/credit-card-rewards-compete-with-air...external

- finance.yahoo.com/personal-finance/credit-cards/article/best-b...external

- forbes.com/advisor/credit-cards/best-business-credit-cardsexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Best Business Credit Cards for Freelancers

Pick for reliability first. For a freelancer, the right business card is usually the one that keeps recurring bills moving, keeps records clean, and avoids extra costs when income swings from month to month. Rewards still matter, but they sit on top of those basics. They do not replace them.

The Best Travel Credit Cards for Digital Nomads

Build a three-part card setup (primary, spend, backup) so one failure is less likely to derail your trip or your work. Forget the myth of "one perfect card." You want a system that still works when a terminal declines your card, a transaction gets flagged, or a merchant won't take your usual option.

A Guide to Notion for Freelance Business Management

If your workspace feels busy but fragile, you do not need more pages. You need one connected system. Treat your freelance business like a business-of-one and use Notion as the control layer that connects client decisions, delivery, and billing in one place.