Quick Answer

Pick an account you can keep after student benefits expire, not just one with a temporary no-fee label. For the best bank accounts for college students, verify the disclosure for monthly charges, waiver conditions, and the exact post-student conversion path before opening. Then set overdraft behavior on purpose and confirm app controls, ATM practicality, and deposit timing so daily use stays predictable.

Your first bank account is more than a place to park student-loan funds and part-time pay. It quickly becomes the operating base for your financial life. It affects how you get paid, whether you avoid routine fees, and how you handle shortfalls. It also shapes how easily you can move into credit, freelance income, or more complex banking later.

A lot of student banking advice stops at one question: does the account have a monthly fee? That matters, but it is only the start. The better question is whether the account will still work when student terms expire and your money starts moving in different ways. This guide uses a simple three-step framework. First, secure what you need right now. Then stress-test the handoff after school. Finally, judge whether the account can support what comes next.

Step 1: Secure Your Present (The Non-Negotiable Checklist)#

Before you open anything, use a verify-first screen: read the disclosures, test the app, and get unclear terms confirmed in writing. If the fee, ATM, or overdraft language is vague, treat the account as a no.

- Verify disclosures before marketing claims

A monthly maintenance fee is a recurring charge per statement cycle unless you meet a waiver rule. A minimum balance requirement is the balance threshold tied to account conditions, often tied to fee avoidance. A fee-waiver condition is the specific rule that removes the monthly fee for that cycle.

Before opening, get the actual account disclosures and fee schedule. At minimum, confirm the monthly fee, minimum-balance rule, and fee-waiver condition in the disclosure itself. Marketing pages often gloss over the part that matters most. For example, Bank of America Advantage SafeBalance lists a monthly fee of $4.95 each month and includes a waiver condition tied to a $500 minimum daily balance.

Also verify that the product is still available on bank-owned pages. Chase's College Checking fee page states it is no longer available for new account openings, even though some third-party roundups still list it. Save dated proof - whether a PDF or screenshot - of the disclosure, fee page, and insurance status. Confirm FDIC coverage for banks or NCUA share insurance for credit unions. FDIC insurance covers $250,000 per depositor, per FDIC-insured bank, per ownership category, and NCUA share insurance covers individual accounts at federally insured credit unions up to $250,000.

- Treat app quality and ATM access as pass/fail

A student account that looks cheap on paper can still be a bad everyday account if the app is weak or cash access is inconvenient. Your app should help you prevent mistakes, not just show balances. You should be able to lock a missing card, set alerts, and verify deposit timing without digging.

An out-of-network ATM fee is what your institution may charge when you use an ATM outside its fee-free network. The ATM operator may charge a separate surcharge. Validate ATM access on your real routes - campus, home, work, internship, and transit, not just on network-size claims. For mobile deposit, confirm both support and the funds-availability and cut-off language. Mobile check deposits may follow a different timetable, and cut-off times matter; CFPB notes cut-off times can be no earlier than 2:00 p.m. at physical locations and noon at an ATM or elsewhere.

| Check | Pass | Fail |

|---|---|---|

| Required app controls | Card lock/unlock is available; alerts are configurable | No card controls, or alerts are missing/hard to find |

| Deposit reliability signals | Mobile check deposit is supported; funds-availability timing and cut-off policy are stated | Deposit is offered, but timing/cut-off detail is unclear |

| Campus-area cash access | Fee-free ATM access is practical near your regular locations | "Large network" claim, but weak local access |

| Reimbursement policy transparency | Disclosure clearly states reimbursement terms and operator surcharge treatment | ATM access is marketed, but reimbursement/surcharge rules are unclear |

- Use support/chat to close gaps in writing

If something is unclear, close the gap before you open. Ask for the exact disclosure section, not a summary. The key questions are straightforward: monthly maintenance fee, fee-waiver condition, minimum-balance requirement, out-of-network ATM fee, operator surcharge handling, mobile deposit cut-off, and general funds availability.

Do not rely on "you should be fine" answers without a document link. Save the chat transcript or email reply with the referenced disclosure URL. If support cannot tie an answer back to the bank's own terms, that is usually a preview of avoidable friction later.

- Choose your overdraft risk deliberately

Your overdraft choice is not a minor setting. It changes how your account behaves when your balance is tight, so make the choice deliberately. Your overdraft setting controls whether ATM and one-time debit transactions can trigger overdraft fees based on your opt-in status. Under Regulation E, a bank cannot charge an overdraft fee for paying those transactions unless you opt in.

Even when bank overdraft item fees are not charged on an account type, low-balance transactions can still be declined or returned unpaid. Third parties may still assess penalties.

| Overdraft approach | What happens | Best if | Risk to accept |

|---|---|---|---|

| Decline or return unpaid | Transaction is declined/returned; account type may not charge bank overdraft item fees | You prioritize avoiding bank overdraft item fees | Payment can fail at the worst time; third-party penalties may still apply |

| Opt-in overdraft coverage for ATM and one-time debit | Eligible transactions may be paid; disclosed overdraft fee may apply | You want a backstop and can manage the fee risk | Small mistakes can become expensive; current policy detail pending bank verification |

| Optional backup transfer features (if offered) | Coverage behavior and fees vary by institution; verify current terms before relying on it | You keep a real buffer and have confirmed the exact terms | If terms are unclear, you can still face failed payments or unexpected costs |

Set your overdraft preference, then confirm the final setting in your app or account profile after opening. If you want help managing cashflow around that choice, see The Best Personal Finance Apps for Freelancers.

Step 2: Plan Your Transition (The Post-Graduation Stress Test)#

Now test whether the account still works when student treatment ends. Confirm whether the account converts into a new product or simply loses student fee treatment, when that trigger happens, and which fee rules apply right after.

1. Find the conversion account (if any)#

A conversion account is the non-student account your student product changes into after eligibility ends. Some banks convert you to a different account, while others may keep the same account and end age-based fee treatment. Do not assume the trigger is graduation. Banks use their own triggers, such as age or time since opening.

Use this checklist against each bank's current account agreement and fee schedule:

- Name the exact post-student account.

- Identify the exact trigger (age, years from opening, or another documented rule).

- Confirm whether conversion is automatic or requires you to choose an option.

- Save the disclosure page/PDF or screenshot.

| Bank example | Documented trigger | Post-student path to verify | Fee and waiver details pending bank verification |

|---|---|---|---|

| PNC Virtual Wallet Student | End of first six years from account opening | Converts to Virtual Wallet | Current monthly fee pending bank verification; waiver requirement pending bank verification |

| Chase High School Checking | After 19th birthday | Converts to Chase Total Checking if no other option is chosen | Current monthly fee pending bank verification; waiver requirement pending bank verification |

| Wells Fargo student/teen path | Age 25 can no longer be used to avoid monthly service fee | Verify whether the product stays the same and only the age-based waiver ends, or other terms change | Current monthly fee pending bank verification; waiver requirement pending bank verification |

| Bank of America student banking page | No monthly maintenance fee on listed accounts until age 25 | Verify exact account and standard fee rules after the age-based waiver ends | Current monthly fee pending bank verification; waiver requirement pending bank verification |

2. Map the new fee triggers#

This is where a reasonable student account can get expensive. A fee-waiver condition is the rule you must meet each fee period to avoid the monthly service fee. A qualifying direct deposit is the bank-defined incoming payroll, benefit, or income category that counts for that waiver test. A balance-based waiver means maintaining the stated minimum balance.

| Fee check | What to do |

|---|---|

| Monthly service fee | Copy the monthly service fee for the post-student account. |

| Waiver paths | List every waiver path exactly as written. |

| "Qualifying" deposits | Verify how the bank defines "qualifying" deposits. Do not assume any transfer counts. |

| Cashflow fit | Decide whether your likely early-career cashflow can meet those rules consistently. |

Then work through the post-student account line by line and match the waiver rules to your expected early-career cashflow, not to your current student routine.

3. Check the transition mechanics#

Once you know the post-student setup and fee rules, check how the handoff actually works. Favor transition mechanics that are simple and easy to verify in writing. For example, Chase states that in this transition the account number and debit card number remain the same, which can reduce autopay disruption risk.

Use this keep-or-switch rule:

- Keep if terms are clear, transition steps are mostly automatic (or clearly defined), and waiver rules match how money will actually arrive in your account.

- Switch before the trigger if terms are vague, the transition creates operational friction, or the waiver rules are unlikely to fit your cashflow pattern.

For a step-by-step walkthrough, see The Best Bank Accounts for Kids and Teens.

Before you commit, run your top account options through a simple fee scenario so you can see which one stays easiest to manage after graduation: Compare payment fees.

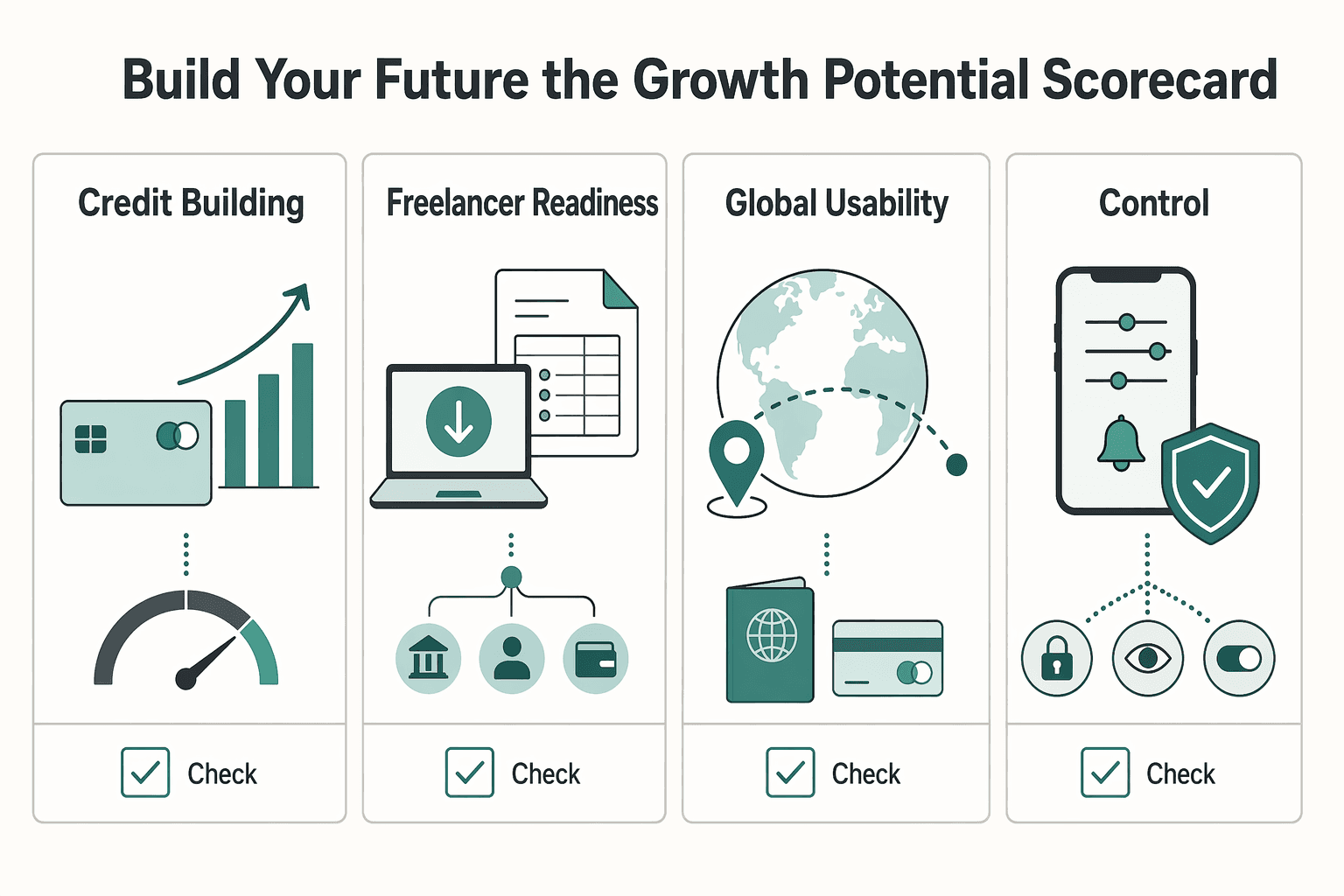

Step 3: Build Your Future (The Growth Potential Scorecard)#

Once an account passes the present and post-student checks, judge it on what it supports next. If two options look similar on fees, choose the one with a clearer credit path, smoother incoming-payment operations, lower cross-border friction, and stronger account controls. Use disclosures and published terms before you open. Use the same four lenses for every option so your comparison stays consistent.

| Lens | What to check | Why it matters | What to verify in disclosures |

|---|---|---|---|

| Credit-building path | Student card, secured card, or both | Shows whether you have a realistic first-credit option | Age and eligibility language; whether a cash deposit is required; current fee detail pending bank verification |

| Freelancer readiness | ACH credits, inbound wires, payment-app compatibility, business-account progression | Income flow only works if payments arrive predictably and post clearly | Posting timing, inbound wire terms, account-use limits; current fee detail pending bank verification |

| Global usability | Debit-card travel terms, ATM access, wire reach, currency support | Travel or overseas payments can create avoidable delays and fees | Foreign-use terms, ATM/wire fees, cutoff times; current fee detail pending bank verification |

| Money-management tooling | Alerts, auto-transfers, categorization, card controls, overdraft handling | These controls reduce missed bills, shortfalls, and avoidable fees | Low-balance alert options, card lock, overdraft language; current fee detail pending bank verification |

1. Credit-building path#

Treat this as an eligibility check, not a marketing check. A college student credit card is a specific Regulation Z category. A secured card usually requires a cash deposit around the credit limit.

| Path | Requirement or constraint | What it tells you |

|---|---|---|

| Student card | A college student credit card is a specific Regulation Z category. | No clear student-card path is a friction signal. |

| Secured card | Usually requires a cash deposit around the credit limit. | No visible secured option is a friction signal. |

| Under-21 approval | Issuers generally cannot issue cards to most people under 21 unless independent repayment ability is shown. | Do not assume standard approval will be straightforward. |

If you are under 21, do not assume standard approval will be straightforward. Issuers generally cannot issue cards to most people under 21 unless independent repayment ability is shown. In that case, a secured option may be the more practical first step. Score the friction signals directly: vague eligibility language, no visible secured option, or no clear student-card path.

Also pay attention to core score drivers. In the common FICO framework, payment history and amounts owed carry the largest published weights (35% and 30%), so steady behavior usually matters more than rewards branding.

2. Freelancer readiness#

Freelancer readiness is about whether the account matches how your money will actually move. Start with ACH support, since ACH is the nationwide network banks use for batch electronic credits and debits.

| Rail or feature | What the article says to verify |

|---|---|

| ACH credits | Start with ACH support, then check incoming ACH credits. |

| Inbound wires | Check the inbound wire workflow. |

| Business-account progression | Check for a clear path from personal checking to a business account if your work scales. |

| Zelle for small business | Zelle for small business is bank- and account-type dependent, and Zelle advises using it only with people you know and trust. |

| PayPal payment type | Choose payment type deliberately because protection treatment differs between personal payments and goods/services flows. |

| Form 1099-K records | Keep records aligned with Form 1099-K reporting for service payments. |

Then check the operating details: incoming ACH credits, the inbound wire workflow, and a clear path from personal checking to a business account if your work scales. Review payment rails carefully. Zelle for small business is bank- and account-type dependent, and Zelle advises using it only with people you know and trust. If clients pay through PayPal, choose the payment type deliberately because protection treatment differs between personal payments and goods/services flows. Keep records aligned with Form 1099-K reporting for service payments.

3. Global usability#

Global usability matters if your payments, travel, or clients cross borders. What you want here is not broad marketing language but exact terms on wires, card use, ATM access, timing, and fees.

A useful benchmark is disclosure detail like this: wire reach in 140+ currencies and 200+ countries, a 5 p.m. Eastern domestic wire cutoff, domestic wires typically same day on business days, international timing of 1 to 5 business days, and a possible $15 inbound wire fee. The point is not that one bank is universally best. It is that clear terms let you judge operational risk before you commit.

4. Money-management tooling#

Only count the tools you'll actually turn on in week one. The value is in controls that reduce mistakes and protect cashflow, not extra features you never use.

Use this checklist:

- Low-balance and unusual-activity alerts

- Scheduled checking-to-savings transfers

- Monthly spending categorization review

- Card lock/freeze controls

- Clear overdraft handling language

A concrete example of transparent controls is SafeBalance. Published terms include a $4.95 monthly fee, an age-based waiver for eligible account holders under 25, no overdraft item fees, and declines when funds are insufficient. Whether that tradeoff fits you is a personal call, but it is much easier to judge when the fee and behavior terms are explicit.

If you want a deeper dive, read Automating Your Freelance Finances: A Zapier Workflow for Connecting Stripe.

Conclusion: Choose Your First Strategic Asset#

Choose the account you can still use when student terms end. In practice, a strategic account comes down to four things: predictable ongoing cost, clear overdraft/decline behavior, a clear post-student fee path, and waiver rules that match how your money will actually arrive.

Utility account versus strategic account#

| Account type | What it looks like | Where it breaks | What makes it strategic |

|---|---|---|---|

| Utility account | You picked it for the student label or a short-term offer. | Problems start when monthly maintenance fees return or waiver conditions no longer match your deposit pattern. | It only works long-term if you already verified post-student terms in writing. |

| Strategic account | You verified fee rules, waiver triggers, and overdraft handling before opening. | It still fails if you treat "no overdraft fee" as "no downside"; declined payments can still create merchant penalties. | You know the post-student fee path, the fee-waiver requirements, and whether your expected deposits can meet them. |

If you can summarize your choice in one sentence, you are close. A good test is: "I can keep this account at low cost, I understand how it handles low balances, and it still works for my post-school income pattern."

Current terms show why the stress test matters. Chase College Checking materials describe a student-fee window up to the expected graduation date, with a five-year maximum. One post-student path shows a $15 monthly fee unless a waiver is met, for example, $500 in qualifying electronic deposits or a $1,500 average ending day balance. Bank of America SafeBalance shows a $4.95 monthly fee with a waiver for owners under age 25. Wells Fargo Clear Access shows a $5 monthly service fee with a waiver tied to $250 or more in qualifying electronic deposits. Verify live availability and disclosures at opening, especially if pages conflict.

Before you open#

- Request the account disclosure and fee schedule, then confirm monthly and ATM-related fees and the exact fee-avoidance rules.

- Confirm the exact post-student fee path and any standard account terms you would move into.

- Check overdraft behavior: an overdraft is a transaction that exceeds available funds, and declined payments can still have outside costs.

- Verify deposit insurance status (FDIC bank coverage or NCUA credit union coverage) and the stated $250,000 limit context.

- Match waiver rules to your likely deposit flow (for example, qualifying electronic deposits), not your current student routine.

Choose the account that fits how you will bank after school, not just how you bank today. If you're thinking ahead to freelance work, you might also find A Guide to Creating a Freelance 'Press' or 'Featured In' Page useful. And if you want your banking choice to fit a future freelance workflow, review the setup options for getting paid and managing payouts in one place: Gruv for freelancers.

Frequently Asked Questions

What happens to your student account after graduation?

Bank policies vary. A student account may convert to a different account type after you no longer meet student eligibility, but the timing and terms are bank-specific. Before you choose, verify the exact post-student account name, its monthly fee terms, and how notice is delivered, whether by email, app, or statement. Also confirm how the bank defines a qualifying deposit for fee waivers, since definitions can differ by institution.

Is a national bank or an online bank better?

Choose based on how you actually move money, not on brand familiarity. The FDIC’s 2023 nationally representative household survey tracks methods banked households use to access accounts, which is a useful reminder that cash access, branch access, ATM access, and app access are separate decisions. Use the survey for trend context, then confirm each item in current bank disclosures before opening. | Use case | National bank | Online bank | What to verify before you choose | | --- | --- | --- | --- | | Cash deposits | Current feature detail pending bank verification | Current feature detail pending bank verification | Cash deposit method, limits, posting time, and any fee | | Branch help | Current feature detail pending bank verification | Current feature detail pending bank verification | Branch availability, support hours, and document services | | App-first workflow | Current feature detail pending bank verification | Current feature detail pending bank verification | Mobile deposit limits, alert options, card lock, and transfer controls | | Travel and ATM use | Current feature detail pending bank verification | Current feature detail pending bank verification | Fee-free ATM network, out-of-network ATM fee, and foreign-use terms | When reviewing ATM terms, check your bank’s out-of-network disclosures and any ATM-operator fee notice.

What financial habits should you build first?

Start with safeguards: turn on low-balance alerts, schedule an automatic savings transfer, and use card lock/freeze controls quickly when activity looks wrong (if available). Keep personal spending and freelance cashflow separate so you can see whether client income actually covers obligations. For credit goals, verify a product’s credit-reporting behavior first, including whether it reports to consumer reporting agencies and under what conditions.

Can you use a student bank account for freelance income?

Possibly, for occasional work, but confirm the payment operations before you rely on it. Verify incoming ACH support, inbound wire terms, payment-app compatibility, posting timing, and any personal-account use limits in the account agreement. If freelance volume becomes steady, consider moving to a separate checking workflow and keep your invoices, payout records, and bank activity organized from day one.

What do you need to open a student account?

Treat this as a verification checklist, not something to guess at. On the bank’s account-opening and identity-verification pages, confirm accepted ID types, age rules, whether student-status proof is required, and opening deposit terms (if any). Match your legal name and address exactly across documents to help reduce avoidable application failures.

Does a student bank account build your credit score?

Do not assume checking-account activity will build credit history unless a product disclosure says so. If your goal is to build credit history, verify whether you can qualify for a student or secured card and confirm that card’s reporting language, eligibility terms, and any required security deposit. Keep product rules separate when reviewing disclosures: a secured-card deposit and a checking opening deposit can be different requirements.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

Automating Your Freelance Finances: A Zapier Workflow for Connecting Stripe, QuickBooks, and Wise

Cleaner books and fewer month-end fire drills come from sequence, not software. Run this in the right order: structure, compliance, accounting architecture, then automation.

The Best Personal Finance Apps for Freelancers

If you are choosing among the best personal finance apps freelancers can use, start with payment risk, not popularity. The goal is simple: keep cash flow visible enough to act early when income slows or bills stay fixed.

Build a Freelance Press Page Clients Can Verify

Your freelance press page should do two jobs at once: help prospects assess your credibility quickly, and keep weak, inflated, or poorly sourced claims off your site. Treat it as a short evidence archive on your website, not a brag wall.