Quick Answer

Yes, handling taxes on income from multiple countries starts with a line-by-line map of where income was earned and how it is sourced, then applying relief only when the rule clearly fits. For U.S. filers, build your default return position first, check treaty language carefully, and treat the saving clause as a limit that can block expected benefits. If a treaty article does not clearly cover an item, use normal U.S. return treatment and document why.

Start Here if You Earn in More Than One Country#

Start with a compliance objective, not a minimization objective. First identify where you may owe tax, then test relief only when a specific rule fits a specific income item. Keep records that will still make sense if the Internal Revenue Service (IRS) or a local authority later asks how you got there.

That sequence matters. If you begin by asking which rule lowers tax first, it is easy to force facts into a treatment before you have mapped the income correctly. A steadier process is to identify the filing footprint first, set the default return second, test relief third, and document the result in plain language you can explain later without rebuilding the file.

This article is for individuals earning across borders, especially freelancers and consultants. It is also useful for U.S. citizens and foreign residents with U.S.-linked income. It is not written for multinational structuring or intercompany design.

Before you calculate anything, lock these anchors in place:

- Define your taxpayer profile. Write one sentence that states whether you are filing as a U.S. citizen, a treaty resident, or a foreign resident with U.S.-source income.

- List each income item by country and type. Separate consulting income, dividends, and other categories before testing relief.

- Check treaty coverage conservatively. Use treaty tables for screening, then confirm the controlling language in the treaty text.

- Apply fallback treatment where coverage is missing. If no treaty applies, or a treaty does not cover that income type, use normal U.S. return treatment.

Write those anchors down in the same file you will use for the rest of the return. Then you can check every later choice against the same starting assumptions. If your taxpayer-profile sentence changes later, treat that as a signal to revisit the income map and relief analysis rather than quietly changing the return in isolation.

Keep one guardrail in view throughout the process: U.S. citizens and U.S. treaty residents are generally taxed on worldwide income, and saving clause limits can narrow treaty benefits. If you cannot map treaty coverage cleanly to each income line, document the assumption, use the most defensible fallback treatment you have, and keep moving through the file in order. The rest of this guide follows that same path: build the record, map where you may owe, determine your baseline filing obligations, then test and document relief.

If a line stays unresolved, do not bury it in a broad total. Keep it visible with a short explanation and continue working the rest of the file. An unresolved note is easier to defend than an unsupported shortcut because it shows exactly what still needs review before filing.

If you want location context while planning your year, see Tbilisi, Georgia: The Ultimate Digital Nomad Guide.

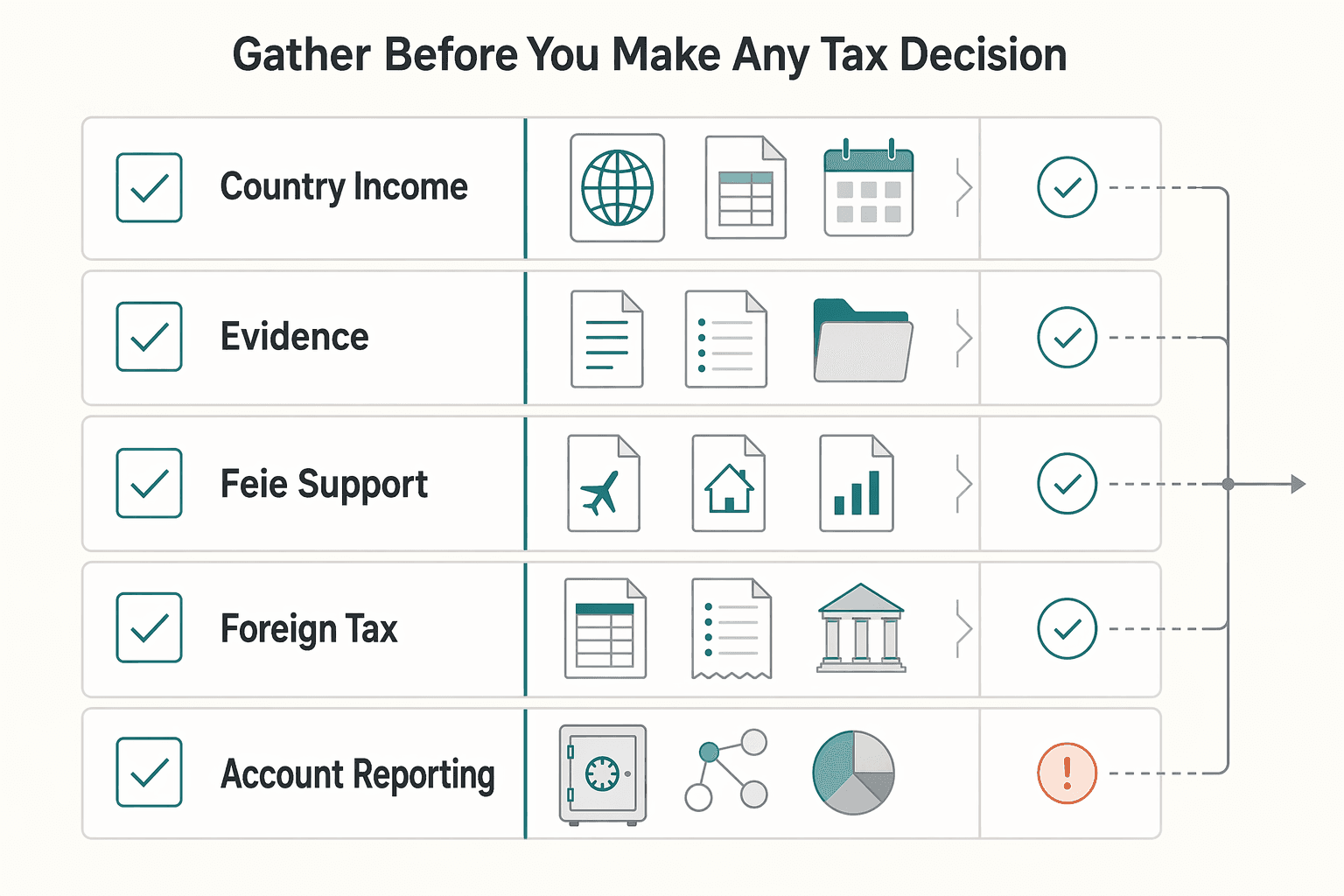

What to Gather Before You Make Any Tax Decision#

Do not choose FEIE or the foreign tax credit until your evidence pack is built. Good decisions here are record-driven, and most bad ones start with a missing document or an assumption nobody marked while the file was still manageable.

| Item | Key details | Folder/form |

|---|---|---|

| Country income map | Payer country, where work was performed, payment date, and a first-pass source tag | Income map |

| Core records | Contracts, invoices, payment statements, your prior U.S. tax return, and slips such as Form 1099-DIV | Core records |

| FEIE support | Proof of foreign earned income, foreign tax home, and travel records for physical-presence analysis | Form 2555 folder |

| Foreign tax credit support | Taxes sorted by income category and then by country, plus proof the tax was imposed on you | Form 1116 folder |

| Account-reporting inputs | Institution, account number, country, owner, and year statements | FBAR and Form 8938 checks |

Create one decision pack for the full year across all countries and income lines. Its job is simple: every line on the return should trace back to a record, and every important judgment call should have a note explaining why you made it. In practice, once this pack is clean, the FEIE-versus-credit choice usually gets much narrower.

- Build a country income map. Track payer country, where work was performed, payment date, and a first-pass source tag such as

U.S. source incomeorforeign-source income. - Pull core records. Collect contracts, invoices, payment statements, your prior

U.S. tax return, and slips such asForm 1099-DIV. - Prepare FEIE support. In your

Form 2555folder, keep proof of foreign earned income, foreign tax home, and travel records for physical-presence analysis. - Prepare foreign tax credit support in filing format. In your

Form 1116folder, sort taxes by income category, then by country, and keep proof the tax was imposed on you. - Prepare account-reporting inputs early. Track institution, account number, country, owner, and year statements for

FBAR(FinCEN) andForm 8938(FATCA) checks.

By the end of this step, you should be able to answer the same questions for each income line: who paid, what type of income it was, where the work was performed, when the payment was made, what document proves it, and what filing question it affects. If you cannot answer those questions the same way across your spreadsheet, folders, and notes, you are not ready to choose a relief path yet.

Verification checkpoint: reconcile invoices to payment statements before you calculate anything. If a payment source is unclear, mark it unresolved instead of guessing. A clearly marked gap is workable. An unmarked assumption tends to spread through the return.

Use filenames that make review fast: country, date, and income type in each file name so you can trace each return line back to backup quickly. Log missing items as you find them, for example missing payment detail, an unsigned contract, or a date mismatch, so gaps are resolved deliberately before filing. Keep the same label for an income line across your spreadsheet, folders, and notes. If a contract, invoice, and payment statement describe the same work a little differently, add a brief note tying them together rather than renaming records as you go.

This is also the stage to separate evidence from assumptions. If you think a payment is foreign-source but the file does not yet show where work was performed, note that as an open verification step. If a foreign tax payment appears in a statement but you do not yet have proof it was imposed on you, keep it out of the credit file until that link is clear. That discipline makes the later choice between FEIE and the credit much cleaner.

Once the pack can answer sourcing and proof questions without guessing, turn it into a map of where you may owe. If you want a broader tax baseline, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

Map Where You May Owe Before You Calculate Anything#

Map potential filing exposure before you start calculating. If a country is tied to you through residency or tied to an income source, treat it as a possible filing jurisdiction until you rule it out on purpose.

This map is a decision tool, not a final return. It keeps every plausible filing connection visible long enough for you to test it. Lines that disappear too early are often the ones that turn into missed filing questions later.

- Flag each jurisdiction with a plausible trigger. Use two anchors: personal residency links and income source links.

- Sort income by type first, then by country. Treaty treatment can vary by specific income item, so avoid one broad foreign-income bucket.

- Mark lines with double-filing or double-tax risk. For each line, note which relief path you will test after mapping, for example treaty treatment or FEIE.

A common failure mode is collapsing several foreign payments into a single total before you know whether source, treaty coverage, or filing exposure differs by line. Another is claiming FEIE or a treaty position before this map is complete, then missing a filing duty in a second jurisdiction. Keep separate lines separate until the map is done and the connections are clear.

Do not delete uncertain lines or merge them into a generic bucket. Tag them unresolved and add a short reason. If a line touches more than one country connection, keep both connections in view until you confirm which treatment applies.

Add one state note while mapping. Federal treaty treatment and state treatment may diverge, and that difference can drive a later state filing decision. A short placeholder here prevents a clean federal answer from quietly becoming an unsupported state assumption later.

Once the map shows every plausible filing connection, you are ready to state the default filing position without building relief into the answer too early.

Determine Your Baseline Filing Obligations First#

Before you apply any relief, write down the return you would file if no relief applied. Baseline first, relief second. That simple discipline keeps the default rule separate from the exceptions you may eventually claim.

Write a short baseline memo in plain language. For U.S. citizens and resident aliens, that baseline generally starts with worldwide-income filing. Think of it as the return you would prepare if you had not yet applied FEIE, foreign tax credit, or treaty analysis. Once that default is clear, every later relief position becomes an explicit adjustment to the baseline rather than an assumption hidden in the workpapers.

- Record the default federal filing duty. Do this without FEIE, foreign tax credit, or treaty assumptions.

- Run a self-employment check early. If you are a consultant, flag

Schedule SEfor review before relief analysis. - Keep residency and filing exposure separate. A residency result in one place does not automatically remove obligations elsewhere.

- Layer FEIE only after the baseline is complete. Confirm foreign earned income, a foreign tax home, and qualifying status before relying on

Form 2555, and remember the income is still reported on the return. - Set up foreign tax credit mechanics as filed. Prepare separate

Form 1116filings by income category.

Use this checkpoint before you move on: if your baseline memo already depends on treaty language, FEIE qualification, or foreign tax credit mechanics, it is not a baseline memo yet. Strip those assumptions out, restate the default filing position, and then add relief in a later layer. Review gets much easier when the default rule and the exception are not mixed together.

Red flag: if your baseline says foreign tax paid means no U.S. filing, pause and correct that before you go further.

A strong baseline memo is short and specific. It should say who is filing, what income is in scope, what filing duties are in view, and what still needs follow-up before any relief is applied. Keep it operational by linking each item to your income map and document folders so a reviewer can follow the logic without recreating the file. If a baseline conclusion cannot be tied back to the map or the records, fix that drafting problem before you calculate anything else.

With the baseline written down, treaty analysis can do its real job: test whether a specific exception applies to a specific item.

Use Treaty Rules Carefully and Assume Gaps Until Confirmed#

Treaties help only when the match is exact. Unless you can tie a specific treaty article to a specific income item and confirm any limits, keep normal treatment in place.

| Step | What to check | Key note |

|---|---|---|

| Treaty coverage | Check United States income tax treaties, use Tax treaty tables for effective-date context, then read Treasury Department tax treaty documents | Confirm treaty coverage before analysis |

| Article match | Match one income item to one article | Test each item line by line |

| Saving clause | Treat the saving clause as a gate, not a footnote | It can limit treaty-based positions for U.S. citizens or residents |

| Missing coverage | If no treaty exists or no article covers the item | File under normal U.S. tax return instructions |

Treaty review works best as a short chain: country, income item, treaty article, saving-clause check, and filing treatment. If any link in that chain is missing, treat the gap as real and keep the default rule until you close it. That is slower than making a broad country-level assumption, but it is much easier to defend later.

- Confirm treaty coverage before analysis. Check

[United States income tax treaties](https://www.irs.gov/businesses/international-businesses/united-states-income-tax-treaties-a-to-z), useTax treaty tablesfor effective-date context, then read the controlling text inTreasury Department tax treaty documents. - Match one income item to one article. Treaty treatment varies by country and by income type, so test each item line by line.

- Treat the

saving clauseas a gate, not a footnote. Most treaties include one, and it can limit treaty-based positions for U.S. citizens or residents. - Use fallback treatment when coverage is missing. If no treaty exists or no article covers the item, file under normal

U.S. tax returninstructions.

Do not let a country-level treaty conclusion spread across all income from that country. A treaty answer for dividends does not automatically answer consulting income, and the reverse is also true. Keep the article match tied to the line item you are actually analyzing.

Verification checkpoint: every treaty position in your file should tie to one country, one article, and one income item. If that chain is incomplete, keep default treatment until it is clarified. Also keep federal and state treatment separate, since some states do not honor treaty provisions.

A practical way to document treaty positions is to keep a brief note for each one you plan to use. It does not need to be long. It only needs to show the country, the income line, the article you are testing, the saving-clause check, and the fallback treatment if the position does not hold. If you cannot write that note clearly, the treaty position probably is not ready to file.

Once treaty positions are sorted, the remaining federal choices usually narrow to FEIE, the foreign tax credit, or normal return treatment.

Decide Between FEIE and Foreign Tax Credit With a Written Rule#

Do not make this choice from memory or instinct. Use a written rule for each income stream and document why it fits.

| Method | What to confirm | Filing note |

|---|---|---|

| FEIE | Confirm foreign earned income, a foreign tax home, and qualifying status, including the physical presence path when relevant | Use Form 2555, and keep sourcing logic consistent with the fact that worldwide income is reported on a U.S. return |

| Foreign tax credit | Build Form 1116 by income category from the start | Categories are filed separately |

| Mixed or unclear facts | If treatment is unclear across countries or streams | Pause optimization and escalate to a qualified preparer before filing |

This matters most in a multi-country year, where the same return can contain income that appears well supported for Form 2555, income better organized for Form 1116, and income that still needs follow-up. A written rule keeps those differences visible. It also prevents a broad "use FEIE" or "use the credit" mindset from overriding the actual facts of a particular line.

- Write a one-page choice memo. For each income stream, note source (

U.S.orforeign), proposed path (Foreign Earned Income Exclusion (FEIE)orforeign tax credit), and the record that supports that call. - Apply FEIE gates before using

Form 2555. Confirm foreign earned income, a foreign tax home, and qualifying status, including the physical presence path when relevant. - Apply credit mechanics upfront. Build

Form 1116by income category from the start, since categories are filed separately. - Reconcile the method with filing obligations. Keep your sourcing logic consistent with the fact that worldwide income is reported on a U.S. return, including income connected to FEIE treatment.

- Add a recovery rule for mixed facts. If treatment is unclear across countries or streams, pause optimization and escalate to a qualified preparer before filing.

The memo should stay brief, but it needs to answer the questions that matter later: what the income is, why the proposed path fits, what record supports that conclusion, and what issue would push you back to normal treatment. If your approach changes during review, update the memo before you change the forms so the reason for the change is preserved in the file.

Practical red flag: do not rely on memory for FEIE annual limits. Confirm the filing-year amount from the instructions you are actually using and record that value in your memo.

When facts are mixed, clarity matters more than speed. If one stream is ready and another is not, keep them separate in your workpapers. A clean written rule for part of the return is more useful than a vague yearwide conclusion that does not survive line-by-line review. The point is not to force one answer across the whole file. The point is to make each answer traceable to its own facts.

Once the federal method is set, run state exposure on its own track rather than assuming the same answer carries over.

Treat U.S. State Tax as a Separate Risk Track#

Do not let a clean federal answer carry your state analysis. State tax risk stands on its own and needs its own worksheet, conclusions, and supporting facts.

California is a common friction point because residency is a facts-and-circumstances determination, not a single bright-line test, and the FTB will not issue written residency opinions for a specific period.

Do not use your federal workpapers as a substitute for state analysis. Use them as inputs, then write a separate state conclusion. That separation is what keeps a clean federal treaty narrative from quietly becoming an unsupported state position.

- Split federal and state analysis. Build a state worksheet for each place with a plausible connection.

- Classify California status by period. Use resident, part-year resident, or nonresident, then map income by period and source.

- Apply sourcing rules by status. Part-year residents are taxed on worldwide income while resident and on California-source income while nonresident; nonresidents are taxed on taxable income from California sources.

- File protectively when facts are ambiguous. Document your timeline and sourcing logic early instead of waiting for certainty.

For California, most of the work is timeline work. State your status by period, map income to the correct period and source, and keep the narrative short enough that a reviewer can compare it to the return without guessing what changed and when. If the timeline is muddy, the conclusion will usually be muddy too.

Verification checkpoint: if filing as nonresident or part-year resident, confirm your calculation follows California's prorated method by applying an effective tax rate to California taxable income.

A common mistake is carrying a clean federal narrative into state filings without first testing state facts. Start from the state timeline and state sourcing rules, then document any federal-state differences so they are intentional and reviewable. Protective filing can help here because it forces you to write the timeline and sourcing logic while the file is still organized, rather than after the return is already built around an assumption.

After the positions are set at both levels, switch from analysis mode to proof mode.

Build an Audit-Ready Evidence Pack and Filing Calendar#

At this point, you are not deciding what the position is. You are proving it. Build one evidence pack and one dated filing calendar so every return position is traceable, reviewable, and closed before filing.

A good evidence pack lets you move from a return line to the supporting record quickly. It should not require a reviewer to dig through every file you saved during the year. Keep it focused on what proves the positions you actually took, not on every document that passed through your inbox.

- Build the minimum evidence pack. Include treaty support notes, your FEIE or foreign tax credit rationale, a residency timeline, and copies mapped to each U.S. return line.

- Tie form mechanics to evidence. Keep

Form 2555support with FEIE files, and maintain separateForm 1116trails by income category. - Log account-reporting decisions. Track

FBARandForm 8938in a decision log with status fields such asdecision,reason,prepared,submitted, andconfirmation saved. - Run a dated filing calendar. Track draft, review, filing, confirmation receipt capture, and a post-filing issue log for corrections.

The evidence pack and the calendar should work together. If an item is still open, the calendar should show who owns it and when it needs to be resolved. If it is closed, the evidence pack should show why. That pairing keeps open questions out of memory and out of scattered messages.

Use the calendar to force closure: every open item needs a due date and a clear status. If you use Gruv where supported, reconcile payout and transaction exports to invoices, receipts, and reported income before filing. If a line changes during review, update the support note and the file link at the same time so the evidence pack does not drift away from the return.

The FAQ below covers the decision points that still trip people up even when the file is otherwise organized.

Use This Final Checklist Before You File#

The last pass is a consistency check, not a fresh round of theory. The goal is not to reopen every decision. It is to confirm that each decision is stated the same way everywhere it appears across federal, treaty, state, and account-reporting workpapers.

- Reconcile your country map to the draft return. Each return line should tie to a mapped income item and a baseline filing note.

- Re-check treaty support in primary treaty documents. Keep a short note on how each treaty position applies and whether any saving-clause limit affects it.

- Confirm your FEIE or foreign tax credit path is evidence-backed and consistent. If you use FEIE, make sure your return reports the income and your

Form 2555support matches your tax-home and qualifying-path analysis; if you use credits, ensureForm 1116is prepared by income category. - Review state exposure separately. State conclusions should be documented independently from federal treaty logic.

- Close account-reporting decisions. Record your

FBAR,FinCEN,FATCA, andForm 8938decisions and filing status. - Run escalation triggers before submission. Pause and escalate if treaty coverage is unclear, sourcing or residency facts conflict, or your FEIE-year references are inconsistent across your materials.

Before submission, do one contradiction check across memo language, form entries, and supporting files for each disputed item. Read the issue from the source record through the memo and into the return, then compare that same issue across federal, treaty, state, and account-reporting files. If they do not align, resolve it before filing. If one disputed item needs more than a short explanation, escalate to a qualified preparer.

Frequently Asked Questions

Can I be taxed by two countries on the same income?

Yes, it can happen. Map each income line by country and type, then test relief item by item so you do not apply the wrong path.

Do tax treaties eliminate tax completely?

No. A treaty may adjust treatment for specific income, but it is not a blanket zero-tax rule. Treaty outcomes are line-specific and need treaty-text review for the income at issue.

What happens if there is no treaty between my country and the United States?

No treaty does not remove U.S. filing duties by itself. Use normal U.S. return rules, then test other relief paths that fit your facts.

What if a treaty exists but does not cover my income type?

Use standard U.S. return treatment for that item unless another supported relief path applies. Document why treaty treatment was not applied.

Does U.S. state tax still apply when I claim treaty benefits federally?

It can. Federal and state outcomes are not automatically aligned, so state exposure needs separate, state-specific analysis and sources.

How should I think about FEIE vs foreign tax credit if I earn in multiple countries?

Test FEIE qualification requirements first (foreign earned income, foreign tax home, and a qualifying status/test such as physical presence). Then test foreign tax credit mechanics by income category, since Form 1116 is prepared separately by category (with one category box checked per form). If IRS materials show conflicting annual FEIE references for the same year, document the filing-year value and source you rely on in your workpapers before submission.

What should I do when one income line remains unclear near the filing deadline?

Keep the line visible, keep your fallback treatment explicit, and document why the issue remains open. If the explanation is no longer short, escalate before filing instead of forcing a weak assumption.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Tbilisi Digital Nomad Guide for 2026 Long Stays in Georgia

Start with sequence, not excitement. If your income depends on delivering work on schedule, secure your legal footing, assemble your documents, and keep month one reversible before you optimize comfort.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.