Quick Answer

Yes. If you perform services while physically in Hawaii, treat those days as potentially Hawaii-sourced income and confirm payroll handling before work begins. Keep three decisions separate: sourcing, withholding, and filing status. Check your facts against Haw. Rev. Stat. § 235-4 and § 235-55(a), and review Form N-15 if you are nonresident or part-year. If payroll guidance is unclear, pause assumptions and get a written determination.

Assume Hawaii tax may apply, then verify#

If you physically perform services in Hawaii, use a safe default: assume Hawaii tax consequences may apply, then verify withholding and filing details before work starts.

This guide is for U.S.-based people working from Hawaii temporarily or part time, including mainland employees, freelancers, and consultants. It is not a permanent-move guide or an international residency guide. The focus is practical: what changes when your workdays happen in Hawaii, even if your employer, clients, or home base are somewhere else.

For employees, the first issue is often employer readiness. Hawaii's government telework guidance makes clear that telework is not an entitlement and participation is at the employer's discretion. If HR or payroll cannot support Hawaii handling, your plan can stall before day one.

Treat withholding as a core compliance item, not back-office trivia. Hawaii describes withholding as state income tax owed by employees that employers must withhold from wages and remit in trust for the State. Before you travel, confirm that payroll has reviewed your Hawaii facts and whether they need to use Booklet A (Employer's Tax Guide) or contact Hawaii DOTAX directly.

If you are self-employed, escalate unclear treatment early. Keep this guardrail in view too: if an employer-employee relationship exists, the worker must be treated as an employee, not an independent contractor, for withholding purposes.

Use public summaries as a starting point only. Hawaii's withholding brochures say they provide general information, not legal or professional advice, and that the law controls if a brochure conflicts with statute.

This guide gives you a sequence to separate sourcing, withholding, and filing, a document checklist to support your position, and practical points where professional advice is the safer move. If you need broader multi-state context beyond Hawaii, read A Guide to Filing Taxes in Multiple States as a Remote Worker. Related: Moving From Hourly to Project-Based Rates.

Start with the sourcing rule, then verify details#

Start with sourcing, then verify the exact Hawaii rule in the underlying legal text before you finalize treatment.

This guide does not restate the statute text. The legal checkpoints to verify are Haw. Rev. Stat. § 235-4 and Haw. Rev. Stat. § 235-55(a).

As you verify, build a simple file:

- Map each pay period to where the work was physically performed.

- Keep your travel timeline and exact Hawaii workdays.

- Keep a copy of your return, worksheets, and supporting documents.

For nonresidents and part-year residents, Form N-15 is Hawaii's individual income tax return form. That gives you a concrete Hawaii filing lane to review before you sort out bigger residency questions. A common failure mode is trying to resolve issues without complete records. Hawaii's instructions also note that issue resolution is faster when your return information is in front of you.

If your facts are incomplete, avoid final conclusions. Preserve records, then narrow the issue with a tax professional after checking Haw. Rev. Stat. § 235-4 and § 235-55(a) against your facts. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

Separate sourcing, withholding, and filing before you act#

Do not let one fact, like Hawaii workdays, answer three different decisions. Tax residency, state income tax withholding, and filing threshold are related, but they are not the same call and should be handled separately.

- Tax residency: your return status, resident, nonresident, or part-year resident

- State income tax withholding: what payroll withholds during the year

- Filing threshold: whether your facts create a Hawaii filing obligation

| Decision type | Who decides it | What triggers it | What evidence you need |

|---|---|---|---|

| Tax residency | You on the return, then Hawaii can review | Whether you took up or gave up Hawaii residence during the year | Travel timeline, address history, move dates, residency records |

| State income tax withholding | Employer or payroll based on facts and guidance | How payroll treats wages tied to your Hawaii work period | Written payroll guidance, approved work location, pay-period dates, workday log |

| Filing threshold | You and your preparer, under Hawaii rules | Income, Hawaii-source amounts, and Hawaii tax liability | Return workpapers, income statements, allocation support, status-specific instructions |

You can know income is Hawaii-sourced and still be unsure about withholding setup or the filing trigger. For personal-services income, Hawaii sourcing follows where the services are performed. The source materials here do not provide the exact withholding thresholds or filing-threshold amounts, so confirm those points in writing before treating payroll settings as final.

Form N-15 is the key filing checkpoint here. Hawaii states that nonresidents with Hawaii tax liability file Form N-15. Part-year residents also use Form N-15. So if your facts point to nonresident or part-year status, you are already in a defined filing lane.

Treat form details as controls, not trivia. On Form N-15, the nonresident or part-year oval at the top must be completed. Hawaii says leaving it blank may cause incorrect processing and delays. For part-year status, the tax-year residency period line also matters. Missing it can disallow certain Hawaii resident credit claims.

For allocation review, remember the Column A and Column B split on Form N-15. Column A is total income regardless of source, and Column B follows Hawaii-source rules. Hawaii's example says wages earned outside Hawaii while nonresident should not go in Column B.

Use this as a checkpoint. If any one of the three decisions is uncertain, pause payroll assumptions and get written guidance. The main failure mode is letting a payroll setting stand in for your residency or filing position without a documented facts check.

We covered this in detail in A Guide to the 'Look-Back' Rule for US Tax Residency.

Split the path by worker type on day one#

Use worker type as your first operational split. For planning, treat employees as a payroll-handling path and freelancers/consultants as an allocation-and-documentation path. If your employer or client cannot clearly support Hawaii handling before travel, renegotiate location or timing first.

| Decision area | Employee | Freelancer or consultant |

|---|---|---|

| First operational burden | Employer HR, payroll, and tax teams | You and your preparer |

| What to lock before Hawaii work starts | Approved work location, payroll handling for Hawaii work period, written scope of company support | Contract or SOW dates, invoice timing, service-location tracking, method to separate Hawaii work from other states |

| Ongoing records | Pay-period dates, workday log, written payroll guidance, address and travel timeline | Daily location log, contracts or SOWs, invoices, travel timeline, state allocation workpapers |

| Common failure mode | Payroll settings become your tax position without a facts check | Year-end reconstruction that is hard to support |

Employer restrictions are often about operational risk and administrative load when work moves across states.

FTB guidance helps illustrate why location detail matters. It says California-source income includes services physically performed there. Its remote-work example says a relocated worker who still performs services there has California-source income for those service days, and that California-sourced portion is reported on Form 540NR. FTB also describes residency determinations as fact-specific.

Hawaii is similarly record-driven. For nonresidents and part-year residents, the filing lane is Form N-15, and Hawaii's instructions emphasize keeping your return, worksheets, and supporting documents. For employees, the checkpoint is whether payroll can handle Hawaii workdays without guesswork. For independents, it is whether your records tie each work period or invoice to where services were performed.

When California is also in play, FTB's checkpoint CA Workdays / Total Workdays = % Ratio is a useful reasonableness test, but not a universal rule. FTB notes that special rules can apply to deferred or equity-based compensation, so escalate those cases instead of forcing a simple day-ratio approach.

In practice, if the payer cannot explain the handling before the first Hawaii workday, treat that as a planning blocker, not a paperwork detail. For a step-by-step walkthrough, see The Tax Implications of Receiving RSU's from a US Company While being a Tax Resident in the UK.

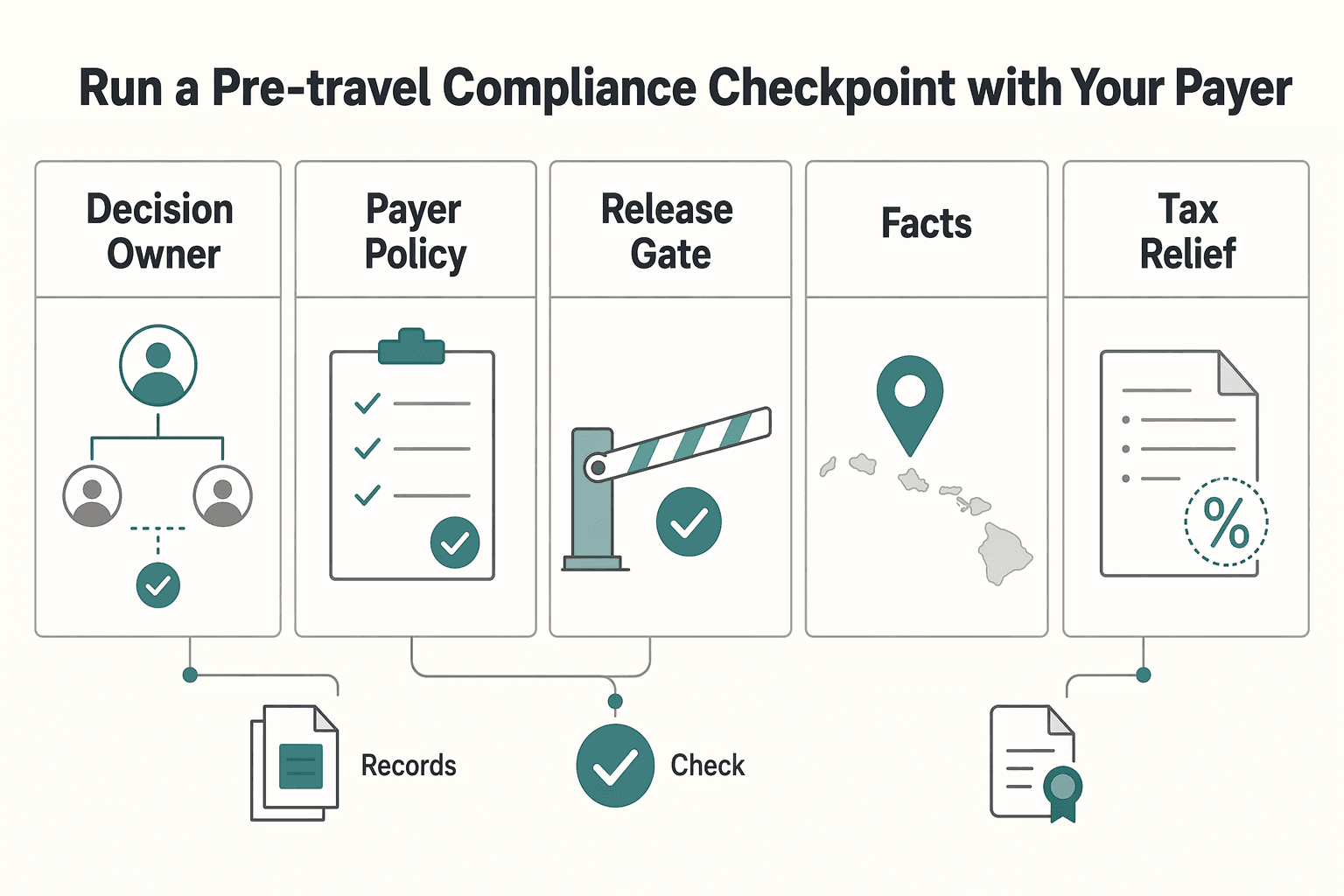

Run a pre-travel compliance checkpoint with your payer#

Before your first Hawaii workday, get documented approval and handling from the payer, not just a manager-level yes. If no one can clearly confirm who owns the decision, how location approval works, and how withholding will be handled, treat it as an unresolved compliance issue.

| Checkpoint | What to get in writing |

|---|---|

| Decision owner | Require a named owner and a written answer for each item. |

| Payer policy | Confirm the payer's policy for temporary work from Hawaii. |

| Dates and location | Confirm approval for your exact work dates and location. |

| Withholding handling | Ask how withholding will be handled, or what additional facts they need before deciding. |

| Tax-relief assumption | Ask whether any tax-relief assumption is being used. |

| Payer scope | Confirm what the payer will do and what it will not do. |

| Record before day one | Keep responses in a durable record before day one. |

Keep the list short on purpose. You want written answers on policy, dates, location, withholding handling, any tax-relief assumption, and what the payer will and will not do before day one.

Do not rely on shorthand tax assumptions. Ask directly whether any relief assumption is being used for wages tied to work performed in Hawaii, and escalate if the answer is vague. The provided excerpts do not establish Hawaii-specific withholding thresholds or reciprocity rules.

The written confirmation does not need to be a legal memo. A clear email that covers approved dates, location, handling approach, and escalation contact is usually enough to create an audit trail. If the payer will not handle certain steps, get that stated explicitly.

A practical benchmark is whether the organization already uses role-based, documented approval controls. The U.S. Department of Commerce Travel Policy Handbook shows that pattern. It supplements federal travel rules, requires annual training for travelers, preparers, and approvers, assigns bureau-level responsibility to ensure completion, and includes a noncompliance section, "Failure to Abide by these Regulations." Different context, same lesson: approvals should be explicit, documented, and verified.

If the payer cannot confirm the approval path and handling plan before day one, pause or narrow work in Hawaii until they can.

Build an evidence pack that can survive scrutiny#

Your file needs to answer two separate questions: where you physically performed services, and what supports your residency position. Keeping those questions separate makes your position easier to explain and defend.

FTB guidance is a useful operating model for that separation. It treats compensation as sourced to that state to the extent services were physically performed there, while residency is a facts-and-circumstances determination. The FTB also states it will not issue written residency opinions for a specific period. The practical takeaway: your documentation has to carry the analysis.

Keep the core artifacts from day one#

Use a small, durable set of records that prove date, place, and amount:

- Work-location log: date, city and state, worked or not, and payer or client

- Travel timeline: entry, stay, and exit dates across Hawaii and other U.S. locations

- Contracts, SOWs, and change orders: service scope and period

- Invoice dates and support, or payroll-period records: what was paid and when

- Proof of where services were performed in the United States: calendar entries, meeting records, time tracking, or similar business records tied to location

A useful standard is bidirectional traceability. You should be able to go from paycheck or invoice to work location, and from workday and location back to compensation.

Label records by decision, not just date#

Tag each document by the decision it supports:

State-sourced income allocation (including Hawaii, if applicable): records that tie work to physical location and periodTax residency position: records that support your broader year pattern and facts

For Hawaii-specific thresholds, withholding triggers, form requirements, or allocation formulas, treat them as unknown in this section unless you verify them separately.

Do not assume one document proves everything. An invoice can show billing, but not necessarily work location. A travel receipt can show movement, but not necessarily services performed on those dates.

Map each compliance question to proof#

| Compliance question | Decision it supports | Strongest proof | Common fallback when records are thin |

|---|---|---|---|

| Which days did you physically work in each location, including Hawaii if applicable? | State-sourced income allocation | Day-by-day work-location log plus calendar plus travel timeline | No contemporaneous day-level log |

| What compensation maps to those days? | State-sourced income allocation | Payroll or invoice-period records tied to day-level work records | Invoice total with no day-level tie |

| Where were services performed in the United States? | Sourcing position | Work records with location evidence plus travel timeline | Lodging or travel receipt alone |

| What supports your residency position for the period? | Tax residency position | Full-year timeline with consistent supporting records | Single address document treated as conclusive |

| What work was approved and for what period? | Scope and consistency check | Approval email, contract, SOW, or change order | Informal message without dates |

If California is also in scope, day-level records become even more important operationally. FTB publishes a workday ratio method, CA Workdays / Total Workdays = % Ratio, then % Ratio x Total Income = CA Sourced Income, and points nonresident and part-year filers to Form 540NR. Do not apply those mechanics to Hawaii by default. Use them as a signal for how disciplined your documentation should be.

Reconcile monthly, not at year-end#

Do a monthly reconciliation across your work-location log, travel timeline, and payroll or invoice records. Waiting until year-end can make it much harder to connect specific days, locations, and compensation periods clearly.

If you keep one habit, make it this: maintain a contemporaneous day-by-day location log and match it to compensation as you go. Related reading: A Guide to TDS (Tax Deducted at Source) for Payments to Indian Freelancers.

Track days and locations with an order of operations#

Use a simple cadence: capture location daily, reconcile weekly, and lock monthly. In remote-work tax questions, the weak point is often not the rule itself. It is whether your records clearly show where you worked on specific dates and whether those facts may have approached a possible Withholding threshold, Filing threshold, or broader multijurisdictional tax issue.

| Stage | Timing | Action |

|---|---|---|

| Capture daily | Same day | Log city and state, full or partial day status, and the employer, client, or contract tied to that work; if you worked across locations in one day, record the split. |

| Reconcile weekly | Once a week | Compare your day log, travel timeline, and payroll or invoice period; check accumulated Hawaii workdays, processed compensation, and possible withholding or filing decision points. |

| Lock monthly | Month-end | Freeze the log version, store supporting records, and note any unresolved assumptions in writing. |

Capture daily#

Log work location the same day. For each workday, record city and state, full or partial day status, and the employer, client, or contract tied to that work. If you worked across locations in one day, record the split.

As a practical proof standard, track where you were during agreed work-availability windows and keep the calendar trail. Hawaii's state telework guidance defines "Core Hours" as scheduled hours when a teleworker must be available for contact at the remote work site. That guidance is for executive-branch state employees, but the recordkeeping discipline is still useful. A dated work log tied to actual work activity can be stronger than travel receipts alone.

Reconcile weekly#

Once a week, compare your day log, travel timeline, and payroll or invoice period. Weekly reconciliation can catch errors while details are still fresh.

Use this checkpoint list:

- How many Hawaii workdays have accumulated in the current pay period, invoice period, and month?

- Has any compensation already been processed that still needs location support?

- Are you nearing any possible withholding or filing decision point in Hawaii or another state?

- Did work span multiple states in the same month, raising allocation questions?

Do not guess thresholds from summaries. If day counts or related pay are moving, confirm applicable rules with payroll or a tax adviser before payroll closes or invoices are finalized.

Lock monthly#

At month-end, freeze the log version, store supporting records, and note any unresolved assumptions in writing. This is a documentation control, not a claim that Hawaii law requires a formal month-end lock.

Weak day tracking can make a narrow allocation question harder to resolve and raise broader employer risk questions. NCSL notes that remote work in a state can trigger multiple, sometimes unexpected tax issues, especially when work occurs in a state where the employer had not previously done business. If your timeline spans multiple states, increase rigor before month-end: daily capture, weekly reconciliation, and immediate escalation if a withholding or filing trigger may be in range.

Before month-end, use the Tax Residency Tracker to keep a defensible day-and-location log across states.

Address Hawaii-specific friction points competitors gloss over#

Once your day tracking is in place, start with Hawaii-specific sourcing and payroll rules. Treat rankings, reciprocity talk, and legal headlines as background.

| Topic | Useful for | Not a substitute for |

|---|---|---|

| ROAM ranking | Policy context and general friction | Your Hawaii tax result |

| Reciprocity tables | Informational review after verifying current rules directly with the relevant revenue authority | A fallback assumption for Hawaii planning |

| New Hampshire v. Massachusetts | Background | A nationwide rule that resolves your Hawaii facts |

| Convenience-of-the-employer analysis | Cases where a state actually uses it, such as New York | A shortcut for Hawaii sourcing |

Rankings are background, not a tax position#

Use the ROAM Index for policy context, not for personal tax decisions. NTU frames ROAM as a state-by-state ranking of remote-worker treatment, which can signal general friction but does not determine your Hawaii tax result.

For Hawaii, the operative rule is more direct: nonresident tax treatment turns on Hawaii-source income, including services performed in Hawaii under Haw. Rev. Stat. § 235-4. If work happened physically in Hawaii, that is a key part of the sourcing analysis.

When someone says a ranking is favorable, ask what filing, withholding, or payroll step it changes. If it changes nothing, keep working from your location records, payroll treatment, and threshold review.

Reciprocity is not a fallback assumption#

Do not assume reciprocity applies. Reciprocity agreements exist in limited state pairings and are meant to reduce two-state filing complexity for cross-border workers, but they are not a nationwide default.

For Hawaii planning, treat reciprocity tables as informational and verify current rules directly with the relevant revenue authority before relying on them. If your payroll team says, "you only pay where you live," ask for the exact authority and whether it applies to Hawaii wages.

Also keep concepts separate. A resident credit for taxes paid to another jurisdiction under Haw. Rev. Stat. § 235-55 is different from reciprocity. A credit may help offset tax paid elsewhere in some cases, but it does not by itself resolve sourcing or withholding decisions up front.

Legal headlines can distract from the Hawaii decisions you actually need#

New Hampshire v. Massachusetts was about Massachusetts taxing nonresident remote work outside Massachusetts, and the U.S. Supreme Court denied leave to file on June 28, 2021. Treat that as background, not as a nationwide rule that resolves your Hawaii facts.

For Hawaii operations, focus on questions you can act on now:

- Were services physically performed in Hawaii?

- Are you treated as an employee or an independent contractor?

- Has payroll reviewed Hawaii withholding administration, including Form HW-7 and its "more than 60 days during the calendar year" trigger?

Use the convenience rule only where it belongs#

Apply convenience-of-the-employer analysis only when a state actually uses it. New York is the common example: out-of-state days are treated as non-New York only when the out-of-state work is required by employer necessity, not employee convenience.

That can matter if a convenience-rule state is trying to source your wages while you work from Hawaii. It is not a shortcut for Hawaii sourcing, and it should not be treated as one here. If your facts involve Hawaii days plus a convenience-rule state, get written allocation guidance or review A Guide to Filing Taxes in Multiple States as a Remote Worker.

This pairs well with our guide on The 'First Year Election' for US Tax Residency: A Deep Dive.

Handle multi-state overlap without panic#

When Hawaii days are part of your year, use parallel analysis, not a one-state shortcut. Treat Hawaii and your home state as separate reviews, and let your records drive the position.

Hawaii plus your home state#

Assume overlap is possible until your facts indicate otherwise. If you worked in Hawaii and still have home-state residency ties, you may need separate sourcing, filing, and withholding reviews instead of forcing one state to "cover" the other.

Your documentation is the control point. Keep a day-by-day location log, travel confirmations, pay or payout records, and work evidence tied to place and date, such as calendar entries, contracts, statements of work, or invoice support.

Hawaii plus California#

Start from complexity, then simplify only if the records align. The practical risk often is not a single Hawaii-California shortcut; it is conflicting facts across residency history, withholding setup, and year-end reporting.

Run the Hawaii review and the other state's review separately. If your day log, withholding records, and tax forms point in different directions, get allocation help before filing rather than trying to "net it out" informally.

Frequent travel across the United States#

If you worked in Hawaii and several other states, fragmentation can become the real risk. Documentation is generally more defensible when logs are contemporaneous and payer reporting is consistent. It is less reliable when records are reconstructed after year-end or forms collapse multiple work locations into one state.

Also verify authority quality before relying on online summaries. For legal research, FederalRegister.gov says to confirm against an official Federal Register edition on govinfo.gov rather than relying on the web or XML rendering alone.

| Fact pattern | Default position | When to seek allocation help | Minimum records |

|---|---|---|---|

| Hawaii work period plus clear home-state ties | Treat overlap as possible until records are reconciled | If either state position depends on assumptions rather than records | Location log, travel dates, pay records, residency support |

| Hawaii plus California with conflicting withholding or mixed residency facts | Treat as higher-risk overlap | Before filing, when forms and work-location history do not match | W-2 or payer reports, withholding detail, prior-year filings, day log |

| Hawaii plus several short work periods across U.S. states, with clean records | Documentation may be enough if records stay consistent | If any mismatch appears during return prep | Contemporaneous log, calendar, invoices or work papers, state-by-state earnings support |

| Hawaii plus multiple states with reconstructed records | Treat correction risk as elevated | Early, before taking a final allocation position | Remaining records plus a dated timeline of gaps and reporting differences |

The real tradeoff#

Simplifying early can save time and effort in the moment, but those same shortcuts can create later rework. Use a simple rule: if records are clean and state positions are consistent, documentation may be enough. If two states can both plausibly assert a position or your forms conflict with your logs, treat professional allocation help as risk control. These issues can arise in both self-managed filings and cases handled with tax professionals.

Know the red flags that require professional advice now#

If your facts, Form N-15 entries, and sourcing logic do not line up, pause and get professional advice before you file.

Escalate now when any of these show up:

- Your records do not clearly show where services were physically performed.

- Payroll or internal records conflict on Hawaii versus out-of-state work location.

- You took up or gave up Hawaii residence during the year, but your draft return is not clearly set up as part-year on Form N-15.

- Late-year edits changed work-location records or income allocation, and you cannot reconcile the changes.

- Reported income does not align with your Hawaii nonresident or part-year tax position.

Form setup is a key checkpoint. Form N-15 is the Hawaii return for nonresidents and part-year residents, and you must mark the correct nonresident or part-year oval at the top. Part-year filers also need to complete the Hawaii residency period line. On that return, Column B is Hawaii AGI, so sourcing errors tend to surface there quickly.

One concrete test is this: wages earned outside Hawaii while you were a nonresident are out-of-state source and should not be reported in Column B. If your records show work performed outside Hawaii but your draft return puts all wages into Hawaii AGI, treat that as a red flag to investigate before filing.

Red flags are investigation signals, not automatic proof that your position is wrong. Bring the records behind your work-location and income-allocation entries when you speak with an advisor. A basic setup error, including the wrong oval on Form N-15, can lead to incorrect processing and delay.

You might also find this useful: A Deep Dive into the Tax Implications of Moving from California to Texas.

Keep records audit-ready with tooling that reduces friction#

The goal is simple: tie each personal-service income line to where the work was physically performed, then check that logic against Form N-15.

For personal services, sourcing follows where the services are performed, so your records should align location history with transaction history, not just payment timing. In practice, that means structured invoices with service period, payer, and amount, plus payout logs and a regular reconciliation against bank or payroll records.

Use Column B on Form N-15 as a control check. Column B is Hawaii AGI, so if your records show work performed outside Hawaii while you were a nonresident, that income generally should not appear in Column B. The same record discipline also supports your residency narrative when you file as nonresident or part-year resident, complete the filing-status oval, and, if part-year, enter your Hawaii residency period.

Two habits can reduce filing mismatches:

- Reconcile your location log, invoices, and payouts monthly, not just at year-end.

- Keep reviewed support files locked or versioned so later edits are visible and explainable.

Reconstruction is the failure mode to avoid. An invoice date or payout date does not, by itself, prove where services were performed. Keep one evidence pack: location log, travel confirmations, invoices or contracts, payout reports, and your allocation worksheet.

If you use Gruv, structured invoicing and payout visibility can reduce operational friction where enabled. Keep the tax judgment with you: tooling should support your sourcing analysis, not replace it.

Conclusion#

Treat physical work in Hawaii as a potential tax event, not a casual location change. For nonresidents, Hawaii-source income is based on days physically present in Hawaii, so day-level records are the foundation of a defensible allocation.

Keep sourcing, withholding, and filing analysis separate, and confirm withholding handling early. Hawaii residents are taxed on income from all sources, while nonresidents are taxed only on Hawaii sources, so reconstructing facts months later creates avoidable risk.

A practical closeout looks like this:

- Before travel or your first Hawaii workday, get written guidance from payroll, HR, or the client on how they plan to handle your setup.

- Track location at the day level and reconcile it regularly against travel records, calendar history, and payment records.

- Build one evidence pack with your daily work-location log, travel confirmations, contract or statement of work, invoices or payout reports, and allocation worksheet.

- Escalate early if Hawaii overlaps with another state or if guidance conflicts.

Broader debates about physical presence, residence-based taxation, or cases like New Hampshire v. Massachusetts are useful background, but they do not replace your own allocation file. Use a safe default: if you physically worked in Hawaii, assume those facts may matter there, document them as they happen, and resolve unclear points before payroll closes or before you file.

If your payroll or contractor flow still has unresolved edge cases, contact Gruv to confirm which compliance-gated controls and audit trails are supported for your setup.

Frequently Asked Questions

If I work remotely from Hawaii for a mainland company, is that income taxable by Hawaii?

Generally yes for the days you physically perform services in Hawaii. The general state-tax rule is that nonresidents are taxed on income earned while physically working in a state, so a mainland employer does not automatically prevent Hawaii sourcing. If you worked across multiple states, allocate by work location and check that treatment against Form N-15.

Do nonresidents owe Hawaii tax on income earned while physically working in Hawaii?

That is the default posture. Hawaii provides a nonresident and part-year resident filing path through Form N-15, Individual Income Tax Return (Nonresidents and Part-Year Residents). The key check is whether your allocation matches where services were actually performed.

Why do some mainland employers refuse remote work from Hawaii?

Usually because of payroll and compliance risk. State withholding is tied primarily to where services are performed, and cross-state remote work can create employer exposure. If withholding is missed when it should have occurred, a state may pursue the employer for unpaid tax.

Does Hawaii have a reciprocity agreement that simplifies multi-state tax filing?

Do not assume reciprocity solves this. Some states do have reciprocity agreements that allow withholding in one state, but the materials here do not establish Hawaii’s reciprocity status. If payroll says only one state applies, ask for that position in writing before you begin working from Hawaii.

How many days can I work from Hawaii before withholding or filing changes?

Do not import another state’s day count into Hawaii. Temporary-presence rules vary widely, and common examples like 14 or 30 days, 12 days or $3,000, or 20 days come from other states. Get a written payroll determination for your Hawaii work period instead of relying on general summaries.

What records should I keep to support state tax allocation if I work in multiple states?

Keep contemporaneous location, work, and payment records, along with your allocation worksheet. Hawaii’s Form N-15 instructions also say to keep a copy of your return, worksheets, and supporting documents. Reconcile location and payment records monthly so you are not reconstructing facts at year-end.

Does Transient Accommodations Tax affect remote workers staying in Hawaii?

Possibly, but not under the income-tax rules covered in this section. The materials here do not establish whether Hawaii’s Transient Accommodations Tax applies to your lodging setup. Treat lodging tax as a separate question and confirm terms and tax treatment directly for your arrangement.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- commerce.gov/sites/default/files/ofm/DOC_Travel_Policy-Oc...trusted

- dhrd.hawaii.gov/wp-content/uploads/2023/04/State-Telework-Pr...trusted

- dhrd.hawaii.gov/wp-content/uploads/2023/12/unit-3-contract-2...trusted

- downloads.regulations.gov/NOAA-HQ-2020-0058-0018/content.pdftrusted

- eutf.hawaii.gov/wp-content/uploads/2025/04/2025-Active-Emplo...trusted

- federalregister.gov/documents/2026/02/03/2026-02131/exercise-of-...trusted

- files.hawaii.gov/tax/legal/taxfacts/tf97-4.pdftrusted

- files.hawaii.gov/tax/forms/2024/n15ins.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Moving From Hourly to Project Rates Without Hurting Cashflow

The right pricing model matches uncertainty and cashflow risk. It should fit how clearly the work can be defined, approved, and defended, not just what you are used to selling. Hourly billing gives you room to work while requirements are still moving. Fixed project pricing gives the client stronger budget clarity once deliverables are stable enough to pin down.

Filing Taxes in Multiple States as a Remote Worker Without Guesswork

If you worked from more than one state during the year, the safest path is a documented, state-by-state process, not a shortcut.