Quick Answer

For U.S. expats, the best compliance-first investment approach is to fund only accounts and products you can clearly classify, document, and report each year. Start with reporting clarity, clean annual records, clear ownership, and an explainable U.S. filing path. If product structure, PFIC status, Form 8938, FBAR, or state residency is unclear, pause and escalate before funding.

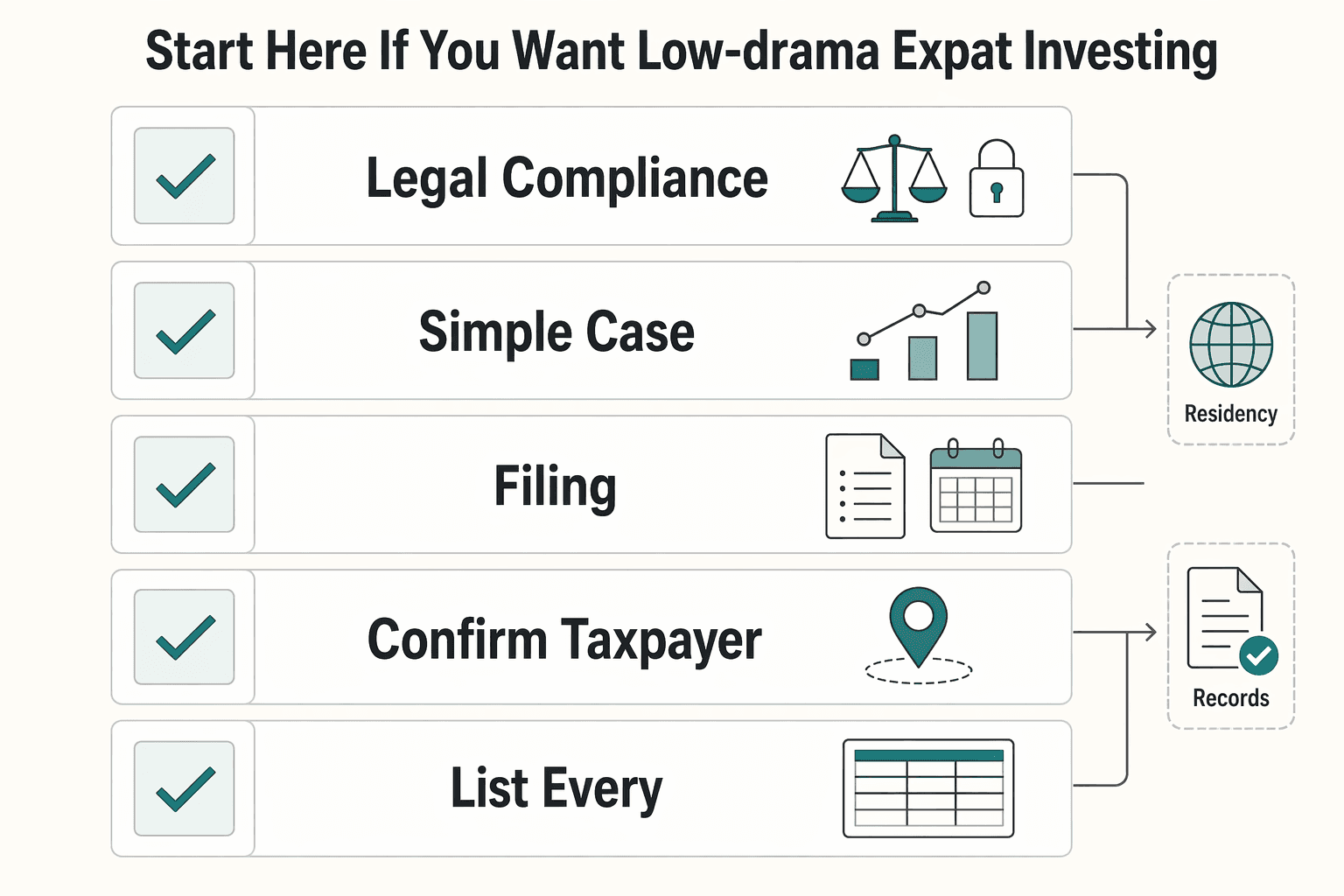

Start Here if You Want Low-Drama Expat Investing#

Low-drama expat investing works best in a fixed order: compliance first, operations second, optimization third. Choose us expat investment vehicles you can explain, maintain, and defend, then escalate when key facts are unclear.

If you are a U.S. citizen or resident alien, moving abroad does not reset your baseline. U.S. filing and estimated-tax rules generally still apply, and worldwide income remains in scope.

Low drama has a practical meaning. You are not trying to eliminate effort. You are trying to avoid preventable surprises such as last-minute document hunts, unclear account ownership records, and position changes made under deadline pressure. When you choose with reporting in mind, filing season is mostly verification instead of reconstruction.

Use three outcomes to screen every decision so each new account is judged the same way before money moves and before annual filing pressure starts:

- Legal compliance: file correctly and handle required foreign account reporting to the U.S. Treasury when it applies.

- Simple ongoing operations: keep records easy to track so annual prep does not depend on rebuilding transactions from scattered apps and inboxes.

- Defensible documentation: if the IRS asks questions, you can quickly produce statements, ownership details, and filing support.

Before funding any new position, run this checkpoint and save the result in your records so the decision is easy to explain later:

- Confirm taxpayer status.

- List every foreign financial account.

- Verify what annual records each institution provides.

- Keep documentation for FBAR and Form 8938 if those filings apply.

- Make sure return amounts can be reported in U.S. dollars.

Add one practical step to that checklist: create a short intake note for every new account. Include account owner, institution, opening date, account purpose, and where statements will be stored. This small note prevents confusion later when multiple accounts look similar.

Do not assume local tax payment means U.S. filing can wait. For many Americans abroad, FEIE or the Foreign Tax Credit is available only if a U.S. return is filed, and foreign account reporting can still apply even when an account has no taxable income.

If account classification, reporting obligations, or documentation gaps are still unclear after this pass, pause and escalate to a cross-border tax professional before investing.

Build the Mental Model Before You Pick Any Vehicle#

Before choosing any vehicle, map three tax layers at the same time: U.S. worldwide reporting, host-country compliance, and double-taxation mitigation.

- Worldwide taxation: U.S. citizens report global income to the IRS regardless of where they live.

- Ongoing U.S. filing: Americans living in Europe still file an annual U.S. return on Form 1040 after establishing local residency.

- Host-country rules still apply: local tax obligations still apply alongside U.S. filing.

- Double-taxation mitigation exists: the Foreign Tax Credit and FEIE can help mitigate double-taxation risk.

The goal of this model is not theory. It is decision speed. If you can map each account across all three layers before funding, you can reduce rework and lower the risk of filing issues.

Use a one-page map per account with five fields: account name, owner, likely income type, where it fits on your U.S. filing, and what local filing questions remain open. If any field is unclear, mark it as unresolved and treat that as a hold condition.

Use this lens before money moves. If you cannot explain how an account fits both U.S. and local filing, stop and get review before funding. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

Choose Vehicle Types in the Right Order#

Pick vehicle types in two passes. First, confirm reporting clarity. Second, compare products.

For U.S. citizens and resident aliens abroad, worldwide income is still subject to U.S. tax, and U.S. filing requirements still apply even when FEIE or the Foreign Tax Credit may lower liability.

Start with vehicles you can track and report every year without guesswork. If you cannot explain how the account and income flow onto your U.S. return, do not fund yet.

Then compare options by documentation quality and operating simplicity. Prefer the option you can support with clean recurring records over one that looks better in a one-time projection.

When choices feel close, this comparison grid helps you evaluate record quality and maintenance burden before focusing on projected outcomes:

| Decision criterion | Prefer | Red flag |

|---|---|---|

| Annual documentation | Predictable statements and clear tax documents | Gaps you have to reconstruct yourself |

| Ownership clarity | Account owner and account purpose are obvious | Shared or unclear ownership records |

| Reporting path | You can explain treatment in plain language | You need assumptions to explain basics |

| Ongoing maintenance | Repeatable yearly handling | High manual effort every filing cycle |

After the grid, run this pre-funding check so nothing gets missed between product selection and execution:

- Confirm you can clearly identify the account and investment in your records.

- Confirm you expect complete annual tax documents from the provider.

- Confirm you can describe the U.S. reporting path in plain language.

- If anything is unclear, hold and get review before money moves.

If a product's U.S. tax treatment is unclear, place it in a review first queue and resolve treatment before funding. Keep the queue visible and dated so unresolved items do not quietly turn into funded positions.

Use a 60-Minute Decision Sequence Before Funding Anything#

Treat this hour as a funding gate. If you cannot state your tax status, filing jurisdictions, and likely forms, do not proceed.

| Step | What to confirm | Key note |

|---|---|---|

| Step 1 | U.S. citizen, resident alien, or another category the IRS treats as a specified individual; list all active jurisdictions | If you do not have to file a U.S. income tax return for that year, Form 8938 is not required. |

| Step 2 | You can open and maintain the account in your current situation | Keep the provider documentation you relied on. |

| Step 3 | What you are buying and how it is documented | If unclear, treat that as a stop condition and move it to review before funding. |

| Step 4 | Build a filing map before money moves | Form 8938 does not replace FBAR (FinCEN Form 114). |

You can run the hour in four blocks. Confirm status and jurisdictions first, then account eligibility, then product clarity, then reporting map. The sequence matters because each step narrows risk before cash moves.

- Step 1: confirm taxpayer status and jurisdictions. Confirm whether you are a U.S. citizen, a resident alien for any part of the tax year, or another category the IRS treats as a specified individual, then list all active jurisdictions. For Form 8938, start with whether you are a specified individual, which includes U.S. citizens and resident aliens. If you do not have to file a U.S. income tax return for that year, Form 8938 is not required.

- Step 2: confirm account eligibility before funding. Verify you can open and maintain the account in your current situation, and keep the provider documentation you relied on.

- Step 3: confirm product structure is clear enough to explain. If you cannot clearly identify what you are buying and how it is documented, treat that as a stop condition and move it to review before funding.

- Step 4: pre-map likely annual reporting. Build a filing map before money moves. Form 8938 is attached to your tax return when specified foreign financial assets exceed the applicable threshold, and thresholds are not one-size-fits-all. Filing Form 8938 does not replace FBAR (FinCEN Form 114), which may still be required separately.

When you finish Step 4, write a short decision note with three lines: proceed, hold, or escalate. Include why you chose that path and what document supports the decision. This note becomes useful evidence later if facts are questioned.

Decision rule: if product structure or reporting is unclear after this pass, do not fund until a cross-border tax professional reviews it. For decision-note structure, see How to Build a 'Second Brain' for Your Freelance Business, and for immediate implementation support, Browse Gruv tools.

Avoid PFIC and Foreign Fund Traps Without Guessing#

After the one-hour gate, run a separate PFIC stop check. Do not fund a non-U.S. pooled fund until its U.S. tax treatment is clear in writing.

A U.S. citizen or resident abroad is generally still required to file U.S. returns, report worldwide income, and follow U.S. tax rules. Foreign financial accounts may need U.S. Treasury reporting even with no taxable income, and some taxpayers may also need Form 8938. In practice, account location and product structure should be treated as compliance decisions, not admin details.

One common trap is local convenience. A fund may be easy to buy where you live, but that does not remove U.S. filing obligations. Problems can start when performance drives the decision and tax classification is deferred until after funding.

A common failure sequence can look like this: you open a local account quickly, buy a pooled fund because access is easy, then discover classification uncertainty during filing prep. At that point, your options may be narrower and cleanup may be harder because the transaction already happened.

If a local advisor recommends a non-U.S. pooled fund, request written analysis before proceeding. Ask for a short memo that confirms:

- Exact legal fund name and domicile from fund documents.

- Whether PFIC treatment may apply to a U.S. person, with assumptions stated.

- Which annual tax documents you should expect, and which gaps you must handle.

- A clear recommendation to proceed, pause, or choose a different vehicle.

Do not rely on verbal comfort alone. If the memo uses assumptions, keep those assumptions visible in your records and verify whether they still hold before adding more capital.

The tradeoff is clear: local access may be easier, while U.S. filing complexity can increase. Final rule: if product structure or PFIC status is still unclear after review, do not fund. Keep an evidence file with the advisor memo, product documents, and your decision note.

Handle Brokerage and Jurisdiction Constraints Early#

Treat account continuity and California tax status as pre-trade gates, not cleanup after positions change. If either point is unclear, pause major allocation moves until your position is documented in writing.

| Status | Tax treatment | Note |

|---|---|---|

| Resident | Taxed on income from all sources | Residency is a facts-and-circumstances determination, not a single-factor test. |

| Part-year resident | Taxed on worldwide income while resident and on California-source income during nonresident periods | If your move happened mid-year, split records by pre-move and post-move periods in the same file. |

| Nonresident | Can still owe California tax on taxable income from California sources | Physically performing services in California can create California-source income during nonresident periods, to the extent services are performed in California. |

Handle account operations and tax classification on separate tracks. Confirm your account can support your current setup and planned move, then maintain a clean funding trail so transfers and ownership are easy to explain later.

Run the California checkpoint before changing positions. The FTB treats residency as a facts-and-circumstances determination, not a single-factor test. California residents are taxed on income from all sources. Part-year residents are taxed on worldwide income while resident and on California-source income during nonresident periods. Nonresidents can still owe California tax on taxable income from California sources.

Do not assume an address change ends California-source taxation. In the FTB remote-work scenario, physically performing services in California can create California-source income during nonresident periods, to the extent services are performed in California.

Use one pre-trade file so your decisions are defensible, and keep it in one place so advisor review and year-end prep rely on the same record:

- Residency timeline by month, including where you lived and where you physically worked.

- Year classification as resident, part-year resident, or nonresident, with a short rationale.

- Income mapping for California-source versus non-California-source treatment.

- Account operations log covering transfers, ownership, and purpose.

- Open questions for advisor review before large rebalances.

Add two practical fields to that file: the document that supports each classification call, and the date each call was last reviewed. These two fields make later handoffs faster because your advisor can see both reasoning and recency at a glance.

If your move happened mid-year, split records by pre-move and post-move periods in the same file. That simple split reduces confusion when account activity spans different residency treatment periods.

FTB states it will not issue written residency opinions for a specific period, so evidence quality is your control point. Decision rule: no major allocation change until account continuity and California status are both clear enough to explain in writing.

Build an Audit-Ready Reporting Pack as You Invest#

Build your reporting pack while you invest, not at filing time. That can help keep IRS-facing and FinCEN-facing records aligned.

Keep a practical annual pack for each account so the support file is ready before filing:

- Account statements.

- Trade confirms.

- Any Form 1099 you receive.

- A holdings snapshot grouped by domicile.

- File labels that include account owner, account number, and institution name.

Store those files in a consistent structure by tax year, then by institution, then by account. Consistency usually matters more than format preference. The point is fast retrieval when a figure needs support.

For foreign accounts, keep separate tracks because FBAR (FinCEN Form 114) and Form 8938 are separate filing obligations:

- FBAR support files for FinCEN Form 114, filed with FinCEN, not the IRS.

- Form 8938 support files for specified foreign financial assets when you are a specified person and exceed the applicable reporting threshold. Form 8938 is attached to your income tax return and does not replace FBAR.

Keeping those tracks separate early can reduce last-minute confusion about what supports which filing.

Handle thresholds carefully and document which threshold logic you used for that year before filing decisions are finalized:

- The IRS cites aggregate value exceeding $50,000 for certain taxpayers, but that is not universal.

- Higher thresholds can apply for joint filers or taxpayers living abroad.

- If you are not required to file an income tax return for the year, Form 8938 is not required for that year.

- Record which rule you relied on for that year.

Use one reconciliation log tying money in and out, transfer date, sending account, receiving account, account owner, and tax-year treatment.

A useful practice is to add a status column to that log: verified, pending document, or needs review. That status view can help you spot weak points early instead of finding them during return prep.

Before filing season, run one verification pass that checks every major match across statements and filing workpapers:

- Institution names and account numbers match across statements, FBAR workpapers, and Form 8938 workpapers.

- Each foreign account in your FinCEN files has matching balance support.

- Your domicile snapshot matches the Form 8938 assets you plan to report.

- Your Form 1099 set is complete for U.S. accounts, with missing items flagged for follow-up.

Decision rule: if you cannot reconcile ownership, accounts, and balances confidently, pause and fix the pack before filing.

Set Your Annual Compliance Cadence and Checkpoints#

A fixed annual cadence can help keep Form 8938 and FBAR obligations separate and catch scope changes before filing.

| Checkpoint | Review | Output |

|---|---|---|

| Q1 closeout | Whether Form 8938 applied and each reportable specified foreign financial asset mapped to supporting records early | A short gap list that assigns unresolved items to you or your advisor |

| Mid-year check | Foreign financial accounts or other foreign financial assets that may be reportable if you added or changed them | Update records while details are still easy to verify |

| Pre-move checkpoint | Reporting scope before a country move, account access continuity, statement delivery method, and whether document language or format changes after the move | Flag unclear classification or reporting treatment and resolve it before year-end |

| Year-end decision point | Reporting scope, documentation completeness, and the latest Form 8938 materials | Keep your current setup or simplify it so reporting is easier to maintain |

A cadence is useful only if it triggers action. Tie each checkpoint to a clear output such as an updated account list, a revised scope note, or a confirmed filing position.

Q1 closeout#

Use Q1 as an internal closeout to confirm whether Form 8938 applied to you for that tax year. A U.S. citizen is a specified individual, but filing still depends on the applicable threshold and asset rules, and $50,000 is only one cited level for certain taxpayers.

If Form 8938 applies, map each reportable specified foreign financial asset to supporting records early. Form 8938 is attached to your annual income tax return, and filing it does not replace a separate FinCEN Form 114 requirement when FBAR is otherwise required.

If you operate through an entity, also check whether specified domestic entity rules applied for that year, then close Q1 with a short gap list that assigns unresolved items to you or your advisor.

Mid-year check#

Run a mid-year scope check on foreign financial accounts or other foreign financial assets that may be reportable if you added or changed them. The point is to identify possible Form 8938 impact early and update records while details are still easy to verify.

Use this check after concrete changes, not just on the calendar. New account openings, ownership changes, country moves, and custody changes are all reasons to refresh scope notes and supporting files.

Pre-move checkpoint#

Before a country move, run a focused reporting-scope review so records stay consistent through the transition. If classification or reporting treatment is unclear, flag it and resolve it before year-end.

During this checkpoint, confirm account access continuity, statement delivery method, and whether document language or format changes after the move. Getting that sorted early can reduce record gaps across the transition period.

Year-end decision point#

At year-end, complete a final pass on reporting scope and documentation completeness, then confirm you are using the latest Form 8938 materials. The instructions are continuous-use and updated as needed, so verify current IRS materials before finalizing next year's process.

Then make one operational choice for the next cycle: keep your current setup or simplify it so reporting is easier to maintain.

Make that choice explicit in writing. If you are keeping the setup, note why it still works. If you are simplifying, list which account or process changes will reduce filing friction.

Know Exactly When to Stop DIY and Escalate#

Set a hard DIY cutoff. If you cannot explain what gets reported, where it gets filed, and which records support each number, escalate.

Escalate now if any of these conditions are true and you cannot resolve them with clear documentation:

- You hold or are being offered a foreign-domiciled fund and cannot confidently determine how it should be reported.

- You are unsure whether your filing picture requires Form 8938, FBAR (FinCEN Form 114), or both.

- Your state residency position is unclear after an international move.

- Your records are incomplete enough that you cannot produce a coherent audit trail for your return.

Form 8938 and FBAR are separate tracks. Form 8938 is attached to your annual income tax return, while FBAR is filed with FinCEN, not the IRS. Depending on your facts, you may need one or both.

If thresholds are where the process breaks down, treat that as an escalation trigger. IRS comparison guidance shows different Form 8938 levels for different filing categories, including $50,000 / $75,000 and $100,000 / $150,000 in certain U.S.-resident cases. If you cannot identify your category confidently, stop DIY before filing.

One more hard stop: if you are not required to file an income tax return for the year, you do not file Form 8938 for that year. If that conflicts with your current plan, escalate and resolve the full filing picture before you submit anything.

When you escalate, bring a compact evidence pack so the handoff is fast and the advisor can focus on decisions instead of document cleanup:

- Draft return facts and filing-status assumptions.

- Form 8938 support showing why assets were included or excluded.

- FBAR support records and account list matched to owner and institution.

- Move-date and residency notes relevant to your filing position.

Add one page called open decisions. List each unresolved issue, the decision needed, and which document is missing. Advisors can move faster when unresolved points are explicit instead of buried inside attachments.

A strong handoff can also reduce back-and-forth. Clear inputs help your advisor focus on decisions instead of document cleanup.

Keep Operations Simple With a Documented Money Trail#

Keep operations simple: decide first, move money second, and log both immediately. That separation can keep intent clear and make filing-season records easier to review.

Use the same sequence every time. Record the allocation decision and purpose, then execute the transfer. If treatment or classification is unclear, pause funding and log the hold instead of moving cash and trying to rebuild intent from memory.

Cross-border administration is complex by default, and many people end up improvising. Over time, that improvisation can create hidden cleanup work. Basic structure now can make reconciliation easier later.

Treat each transfer as two linked records: decision record and movement record. The decision record states why the transfer happened. The movement record shows what happened. Keeping both helps reduce ambiguity when multiple transfers occur close together.

Keep one ledger for cash movement#

Use one running ledger for invoices, FX conversions, payouts, and investment funding. Keep it consistent. A short field set is enough:

- Date and local time.

- Sending and receiving accounts.

- Currency and conversion details used.

- Reference ID from the bank, broker, or payment provider.

- Purpose tag such as invoice settlement, account funding, or rebalance.

- Link or filename for supporting confirmation.

For transfers with more than one leg, record each leg separately and link them with a shared reference note. That makes it easier to trace funds from source to destination when an intermediary account is involved.

Review the ledger on a regular cadence. Spot-check entries and confirm each one traces from cash source to final destination. If a link is missing, fix it before the next transfer batch.

Prefer exportable records and visible status history#

Where supported, choose tools with exportable records and clear status history. Raw transaction data, stable IDs, and timestamps can reduce manual rework and make reconciliation easier.

If a provider only offers limited history views, download records regularly and store them in your annual folder structure. Do not wait until filing season to check whether prior periods are still available.

Do not treat any provider as a compliance guarantee. Your records support the process, but reporting decisions still sit with you and your advisor. If treatment is unclear, confirm specifics with a qualified CPA or attorney.

Keep PII out of day-to-day notes#

Keep operating notes useful but minimal. Store only what you need to identify each transaction and purpose, and keep sensitive tax documents in protected storage.

When sharing records for review, send a compact evidence pack with redacted notes plus source files from protected storage, not scattered across chat threads.

Use plain naming conventions so files remain searchable without exposing sensitive details in filenames. Good names can speed review while limiting unnecessary data exposure.

The Practical Bottom Line#

Low-drama expat investing comes from choices you can classify, document, and report each year. The durable plan is the one you can explain at filing time without rebuilding decisions from memory.

Use the same annual compliance pass every year:

- Decide whether you must file Form 8938, FBAR, or both.

- Keep them separate: Form 8938 goes with your income tax return, while FBAR (FinCEN Form 114) is filed directly with FinCEN, not with the IRS.

- Match account and ownership details across tax-return support files and FinCEN support files.

- Escalate before filing if classification, threshold selection, or reporting scope is still unclear.

On thresholds, avoid one-size-fits-all assumptions. The $50,000 and $75,000 figures are examples for certain taxpayers, not a universal rule. Apply the threshold logic that fits your filing situation and record that reasoning for the year. If you are not required to file an income tax return for the year, Form 8938 is not required for that year.

Keep the process grounded in three habits: decide in writing before funding, maintain records as activity happens, and escalate when classification is unclear. Those habits protect decision quality more than any one product choice.

If ambiguity remains after this checklist pass, stop DIY and escalate before filing.

Frequently Asked Questions

What are the lowest-risk investment vehicles for U.S. expats who prioritize compliance over optimization?

There is no universal lowest-risk list. The safer baseline is accounts and products you can classify and report clearly, with clean records and no guesswork at filing time. If two options look similar, prefer the one with better annual documentation and easier ongoing maintenance.

Why are **U.S.-domiciled investment products** often preferred over **foreign-domiciled funds**?

They are often preferred for reporting simplicity rather than expected returns. Foreign-domiciled funds can increase classification and reporting burden, and unresolved treatment is often enough reason to choose a simpler structure. Cleaner reporting paths can reduce filing risk and rushed fixes later.

What is a **PFIC**, and when is it most likely to become a problem?

A PFIC is a U.S. tax classification that can apply to some foreign-domiciled funds. It becomes a problem when you invest first and sort out classification later. A conservative approach is to get written classification analysis before funding and keep it with your records.

Can I still owe U.S. tax if I already pay tax where I live now?

Yes. U.S. persons may still need to report non-U.S. income to the IRS, and U.S. tax can still be due depending on the facts. The Foreign Tax Credit and FEIE may reduce exposure, but they are not an automatic full shield.

What is the first checklist I should run before opening or funding a new account abroad?

First confirm whether you are a U.S. person for tax purposes, because that drives filing obligations. Then map the money trail before moving cash, including source account, transfer path, currency conversion, destination account, and the records you will keep. Also confirm what annual documents the provider will give you, and pause if any part is unclear.

When should I stop DIY and hire a cross-border advisor?

Stop DIY when your tax status, reporting duties, or income treatment is unclear across jurisdictions. Escalate if thresholds, exceptions, or required filings such as Form 8938 and FBAR are uncertain, or if your state residency position is unclear after a move. Escalate earlier if your records are incomplete and you cannot produce a coherent audit trail.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

How to Build a Second Brain for Your Freelance Business

If you want to build a second brain for freelance work, do it before scattered notes and missed follow-through start to feel normal. A second brain is a personal knowledge-management system for storing and retrieving what matters when work gets noisy.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.