Quick Answer

For a stripe vs paypal international decision, the best choice for freelancers is the one that reduces coverage, FX, payout, and dispute risk for your real client corridors. The article’s guidance is to verify each route before invoice one, compare true total cost line by line, and use a repeatable checklist so cashflow stays predictable when holds, delays, or chargebacks happen.

Stop Guessing and Build a Safer Get Paid System#

For an international Stripe or PayPal choice, pick the payment gateway that cuts your cashflow exposure first, then optimize fees.

It is common for freelancers and small teams to compare headline transaction fees and stop there. That is how you end up pricing projects on assumptions instead of on how money actually moves. A posted domestic example like 2.9% + 30 cents does not tell you what international payments do to margin. Corridor rules, payout timing, withdrawal mechanics, and disputes all show up later.

The real failure point is often cashflow reliability.

You finish a project. You invoice on time. The client pays. Then a dispute reverses the funds while your payout schedule still runs, or a reserve reduces what you can withdraw. You did the work, but your operating cash shrinks at exactly the wrong moment.

Use this risk-first filter before you choose Stripe or PayPal:

- Map your client corridors first, then confirm platform availability in those exact countries.

- Classify each payment as domestic or international by platform rules, not by client intent.

- Break total cost into line items: transaction fees, international market-grouping effects, and payout or withdrawal friction.

- Check downside controls: dispute flow, reserve behavior, and reserve review timing.

Keep one guardrail in mind: never assume global availability, fee treatment, or policy controls stay constant across markets and programs. Stripe supports specific countries and regions, not every market. PayPal treats transactions as international when sender and receiver sit in different markets, and grouped markets can change how international rates apply. Stripe payout schedules vary by country and business profile. Card disputes can reverse funds immediately. PayPal can place reserves for dispute and chargeback risk, and reserves can be reviewed in 180 days.

| Risk area | What breaks if you guess | What to verify before each client engagement |

|---|---|---|

| Coverage | You cannot process or settle as planned | Country support, settlement path, account setup fit |

| Cost stack | Margin erodes after missed line items | International fee logic by market grouping, plus payout and withdrawal steps |

| Timing | Payroll and vendor timing slips | Expected payout schedule and withdrawal steps |

| Disputes and reserves | Available balance drops without warning | Evidence process, reserve triggers, and reserve review timing |

Which Platform Wins at a Glance for International Freelancers?#

For an international Stripe or PayPal decision, pick the payment gateway that fits your client mix and lowers operational risk, not the one with the loudest brand signal.

Here is the comparison that matters in real workflows: what happens after an invoice becomes a cross-border payment and you need the money to land predictably.

Both Stripe and PayPal can route major card payments. Day-to-day operations can diverge once country, currency, and dispute workflows enter the picture.

| Criteria | Stripe | PayPal | Wise (reference baseline) |

|---|---|---|---|

| Onboarding friction for freelancer payments | Useful when you want control over payment setup and can verify support by country and currency. | Checkout can include PayPal options, cards, and wallet-linked methods where available. | Useful benchmark for transfer-first setups focused on fee clarity. |

| Client trust at checkout | Supports global and local card networks. | Supports PayPal options plus debit and credit cards, with wallet-linked options in supported markets. | Use as a comparison point for transparency, not as a direct like-for-like checkout replacement. |

| FX handling visibility | Varies by payment method, country, and currency pairing, so verify each route before you invoice. | International treatment depends on market pairing, and method availability depends on country. | Positions pricing around upfront visible fees, which helps you sanity check transaction fees elsewhere. |

| Payout predictability | Verify country and currency support details before you depend on a timeline. | Verify country-level availability before you set cashflow commitments. | Gives a clean baseline for transfer costs, then you still validate route details. |

| Dispute workflow quality | You need fast response operations, since dispute deadlines are usually 7 to 21 days depending on card network. | You still need active merchant response operations within requested case timelines. | Baseline only for cost visibility, not your primary dispute workflow benchmark. |

One point people miss: Stripe and PayPal can both support major card payment paths. Differences often show up in risk tooling, response operations, and country or currency method availability.

If a new international client asks to pay this week, use the option you can verify end to end today. Then run one clean test invoice before wider rollout.

Safe default recommendation: choose the option with lower operational risk for your current international payments mix, then re-evaluate as your corridors, client behavior, and volume change.

If you want a deeper dive, read The Future of Work is Freelance: Trends to Watch in 2026.

What Does International Cost Really Look Like After Headline Fees?#

True international cost includes processing fees, FX effects, payout friction, and dispute leakage, so compare Stripe and PayPal line by line before you set price.

| Source | Cost element | Article detail |

|---|---|---|

| Stripe | Domestic card baseline | 2.9% + 30 cents |

| Stripe | International cards | +1.5% |

| Stripe | Currency conversion | +1% when conversion is required |

| PayPal | Domestic commercial pricing | Domestic commercial fees apply before international uplift |

| PayPal | International commercial percentage | 1.50% listed for commercial transactions |

| PayPal | Currency conversion | Conversion includes a retained spread |

| Stripe Connect | Payout example | 0.25% + 25 cents per payout |

| Stripe | Refund fee treatment | Processing, Connect, and conversion fees from the original transaction are not returned on refunds |

To make a decision you can defend, do route-level math. Treat every quote as an operations decision, not a branding choice.

Headline transaction fees only show the first layer. Stripe shows a domestic card baseline of 2.9% + 30 cents. It then adds +1.5% for international cards and +1% when currency conversion is required. PayPal states domestic commercial fees apply, then adds an extra international commercial percentage, with 1.50% listed for commercial transactions. It also states currency conversion includes a spread retained by PayPal.

| Cost line item | Known now | Unknown you must verify per route |

|---|---|---|

| Transaction fee base | Stripe publishes a domestic baseline. PayPal applies domestic commercial pricing before international uplift. | Exact program and method for your account and client payment type. |

| International uplift | Stripe lists +1.5% for international cards. PayPal lists an additional international commercial percentage. | Whether your specific corridor falls under grouped market treatment that changes effective rate logic. |

| FX conversion | Stripe lists +1% when conversion is required. PayPal states conversion includes a retained spread. | Effective exchange path, invoice currency vs settlement currency impact, and final conversion cost for your corridor. |

| Payout or withdrawal costs | Stripe Connect shows a route-specific payout example of 0.25% + 25 cents per payout. | Your actual payout method, country path, and timing-related cost. |

| Dispute and refund leakage | Stripe states processing, Connect, and conversion fees from the original transaction are not returned on refunds. | Your dispute frequency and leakage rate by client segment. |

Build a simple worksheet with two tabs and update it for every international payment engagement:

- Corridor tab: client country, your entity country, invoice currency, settlement currency, payment method, known fee inputs, unknown checks.

- Client margin tab: project revenue, full fee stack, expected leakage buffer, net margin after payment costs.

If a client asks to pay in one currency while your costs sit in another, run the worksheet before you approve terms. That single step helps protect margin and cash flow.

Use Wise Business and Tipalti as benchmarks for FX category design and visibility language, then verify final costs on the exact route you will use. Recommendation: if unknown fields remain, pause the quote or add a risk buffer until you confirm the route.

Which Option Protects Cashflow Better When Holds or Chargebacks Hit?#

Choose the option that lets you respond fastest when money gets stuck, not the one with the lowest headline transaction fees.

This is the part most people skip. Cost matters, but cashflow failure is what breaks a business-of-one. International payments amplify that risk because a single blocked payout can choke your working cash for days.

| Failure mode | Stripe severity for solo freelancer | Stripe severity for small team | PayPal severity for solo freelancer | PayPal severity for small team | Why this matters |

|---|---|---|---|---|---|

| Holds | Medium | Medium | High | Medium to high | PayPal notes rare holds can run up to 21 days, and release timing can depend on delivery confirmation flows. |

| Disputes and chargebacks | High | Medium to high | High | Medium to high | Disputes run on card network rules. Stripe states you usually get 7 to 21 days to respond, and missing the deadline loses the case. |

| Payout delays | Medium | Medium | Medium to high | Medium | Stripe separates payout schedule from payout speed, so even daily payouts can still arrive on a multi-day payout speed. |

Dispute pressure depends on network timelines and your response quality. Mastercard guidance highlights compelling evidence and typical merchant response windows. Visa documentation includes longer issuer timing examples for specific scenarios.

Run this escalation playbook the same day a contested invoice appears:

- Open a case file immediately and log the response deadline.

- Build an evidence packet: signed scope, invoice, delivery proof, approval messages, and change requests.

- Assign one owner for merchant responses, even if you are a team of one.

- Send a client note that states facts, delivery status, and next checkpoint date.

Use this short client message template:

- "We flagged a payment dispute and submitted delivery evidence today. We will share the next update by [date] and keep work status transparent while the case moves through review."

Preventive controls reduce risk before disputes start:

- Write clear invoice terms, acceptance criteria, and refund boundaries.

- Bill by milestone so one dispute cannot freeze the full project value.

- Keep payment method policy consistent per client so evidence and dispute history stay clean.

- Tighten pricing and scope together using Value-Based Pricing: A Freelancer's Guide.

Stop-loss rule for a business of one: pause new high-risk client work when active holds or disputes threaten core operating cash. Resume only after payout reliability stabilizes for the next billing cycle.

Do Stripe and PayPal Support the Same Countries and Currencies?#

No, Stripe and PayPal do not support the same countries, currencies, or payout corridors, so you must verify each client route before you send an invoice.

This choice can fail before fees even matter. Coverage is not one box to tick. Country access, presentment currency, settlement currency, and payout capability describe different parts of the flow.

| Coverage metric | Stripe | PayPal | What you must verify |

|---|---|---|---|

| Country and market footprint | Documents charge support in over 135 currencies. | States availability in more than 200 countries/regions and support for 25 currencies. | Confirm your exact client country pair and account program before quoting. |

| Presentment currency | Defines presentment currency as the currency the customer pays. | Supports multiple currencies, with availability varying by market. | Check the invoice currency your client sees at checkout. |

| Settlement currency | Defines settlement currency as the currency your destination bank receives. | Settlement and withdrawal behavior can differ by market and account setup. | Confirm the currency that lands in your bank, not just checkout currency. |

| Cross border payouts | Limits self-serve cross-border payouts outside listed regions in the cited program context. | Payout and withdrawal paths depend on country and program. | Validate payout corridor availability before you promise timing. |

| Compliance gates | Uses risk-based KYC and AML checks that vary by account and jurisdiction. | Uses CIP identity checks and may request business documents during onboarding or account review. | Prepare identity and entity documentation early to prevent payout interruptions. |

Run this verification checklist on every payment setup:

- Map client country, your entity country, invoice currency, settlement currency, and payout destination.

- Mark each line as verified or unverified and add a date stamp.

- Flag a hard warning when coverage varies by market or program.

- Confirm KYC and AML requirements for your exact account profile.

- For team or agency structures, collect KYB-ready files, including core entity records and business licenses where required.

If a client wants to pay in their local currency while your team needs settlement in another currency, run this checklist before you approve terms. That one step protects margin, payout timing, and client trust.

What Should You Check Before Sending the First International Invoice?#

Run a pre-invoice control check that confirms cost, compliance, and evidence before you send any cross-border invoice.

| Item | What to confirm | Article detail |

|---|---|---|

| VAT logic | Client country pair | Tax rules vary by jurisdiction |

| U.S. tax form | Payer and payee status | Collect W-9 or W-8BEN |

| 1099-K reconciliation | Platform records and books | Reconcile payment platform records with your books so 1099-K reporting does not surprise you later |

| FEIE planning | Advisor review | Qualification is case specific |

| FBAR tracking | Foreign account balances | Filing can apply when aggregate value exceeds $10,000 and runs through FinCEN Form 114 |

Platform choice only matters if your execution is tight. Before your first invoice in a new corridor, verify the cost path and document what you will need in a dispute. Get your paperwork logic straight so payment operations stay predictable.

| Pre-invoice checkpoint | What to verify | What to save for audit readiness |

|---|---|---|

| Fee stack | Base transaction fees, international uplifts, and any payout or withdrawal charges in your exact route | Pricing screenshots, account fee settings, and the quote you used |

| FX path | Invoice currency, settlement currency, and conversion method; include the fact that some conversions include a provider spread | Conversion screen captures, rate timestamp, and confirmation emails |

| Payout timeline | Expected payout timing for your account profile; confirm that schedule settings do not change pending funds availability | Payout settings capture, support confirmation, and first test payout reference |

| Dispute workflow | Response owner, required evidence packet, and internal response deadline buffer against card network timelines | Dispute checklist, template responses, and delivery proof standards |

Use this reusable checklist before every new client corridor:

- Confirm VAT logic for the client country pair, because tax rules vary by jurisdiction.

- Collect the right U.S. tax form for payer and payee status: W-9 or W-8BEN.

- Reconcile payment platform records with your books so 1099-K reporting does not surprise you later.

- Track potential FEIE planning items with your tax advisor; qualification is case specific.

- Track foreign account balances during the year, because FBAR filing can apply when aggregate value exceeds $10,000 and filing runs through FinCEN Form 114.

Imagine a U.S.-linked client asks to pay in one currency while you need settlement in another. If you skip this checklist, you can lose margin on FX, misclassify tax paperwork, and scramble during a dispute window. If you run it, you control risk before cash moves.

For Stripe, PayPal, and any international payments flow, the safest default is simple: do not send invoice one until each checklist row is verified and documented.

Which Setup Should You Choose for Your Current Stage?#

For most teams, start with PayPal for immediate client trust, move to Stripe for workflow control, and adopt a modular stack once risk starts draining margin and time.

Make the stage-based choice based on your current bottleneck: trust at checkout, control over workflow, or resilience under compliance and payout pressure.

Stage-based setup comparison#

| Scenario | Recommended setup | Why it fits now | Risk note |

|---|---|---|---|

| Solo freelancer optimizing trust and speed | PayPal first, with strict terms and a fallback payment path | Clients often recognize PayPal quickly, setup can be fast, and its large active-account network supports familiar checkout behavior. | A payment hold can still interrupt cash access. Withdrawal choice changes speed and cost, so define your fallback before you invoice. |

| Creator or growing team needing control | Stripe first, with payout schedule checks | Stripe lets you configure payout workflows with more control, including payout frequency choices and faster payout options when enabled. | Do not assume identical payout timing across countries or industries. Validate payout behavior in your actual routes. |

| Operations-heavy team | Modular stack for collection and payout, with KYC and compliance gates defined upfront | You can route collection through the payment gateway that fits client trust, then handle downstream payouts through specialized rails where supported. | Compliance requirements change over time, so your team must update KYC and compliance controls continuously, not once. |

- If you are a solo freelancer, choose PayPal first. Risk note: lock tighter invoice terms, define dispute response ownership, and prewrite a backup pay link flow.

- If you are a creator or a growing team, choose Stripe first. Risk note: test payout timing in your real international payment routes before you scale volume.

- If you run operations-heavy workflows, choose a modular stack. Risk note: assign one owner for KYC refreshes, compliance checks, and reconciliation standards.

Move when triggers appear#

Use this migration trigger list when a single tool starts creating operational drag:

| Trigger | Operational effect |

|---|---|

| Dispute or hold events show up often enough | They disrupt weekly cash planning |

| Payout delays | They force delays to contractor or supplier payments |

| Reconciliation overhead | It keeps climbing across fees and payout records |

| More entities | The team starts missing compliance checks |

If several of these show up at once, it is time to change the setup.

Imagine a small creator studio that closes global clients quickly, then loses focus every week to payout follow-ups and ledger cleanup. That is your signal to move from one tool to a structured stack.

Related: How to Write a Privacy Policy for Your Freelance Website. Want a quick next step? Try the free invoice generator.

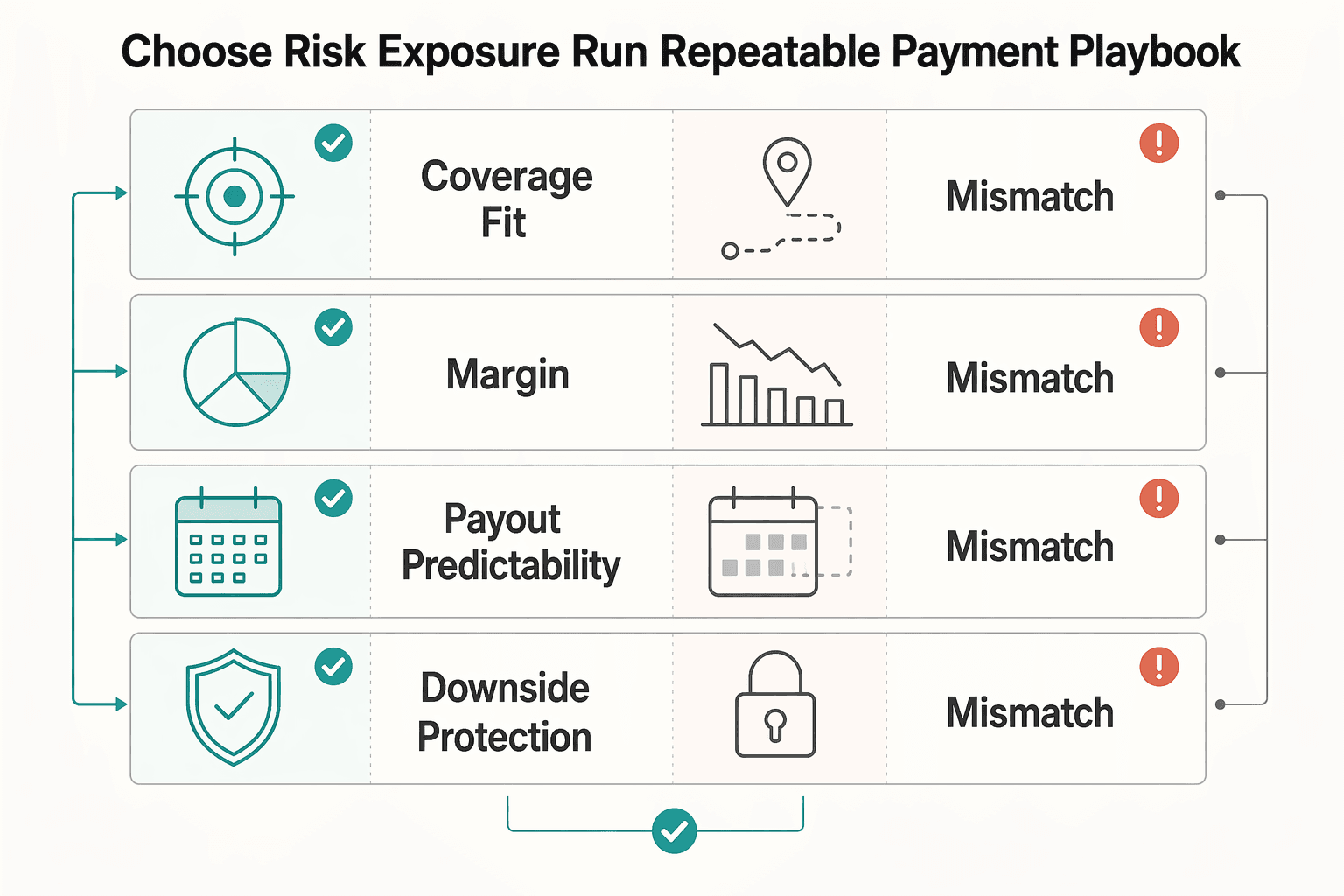

Choose by Risk Exposure and Run a Repeatable Payment Playbook#

Choose the platform that reduces combined coverage, FX, payout, and dispute risk for your real client corridors, not the one with the strongest brand signal.

At this point you are not "choosing Stripe vs PayPal." You are choosing a repeatable get paid system you can run under pressure.

| Control layer | Stripe check | PayPal check | Decision rule |

|---|---|---|---|

| Coverage fit | Confirm your business country support, then verify charge currency and settlement currency for each corridor. | Treat country and currency headlines as starting signals, then confirm receive and withdraw capability for that route. | If corridor support stays unclear, do not invoice yet. |

| FX and margin | Map where conversion happens when charge and settlement currencies differ. | Include conversion spread impact, and factor transfer method into expected bank-arrival timing. | If the FX path is opaque, choose the route with clearer net outcomes. |

| Payout predictability | Validate payout schedule for your country and industry, including initial payout timing. | Validate transfer method and expected bank arrival behavior for that market. | If cash timing is critical, run a low-risk test transaction first. |

| Downside protection | Plan for disputes that can immediately reverse payment and add fees. | Plan for holds, reserves, and dispute-fee exposure on eligible disputes. | If downside events break weekly cashflow, move to a more structured stack. |

Run the same reusable system on every new project:

- Use your at-a-glance matrix to pick a default payment gateway by corridor.

- Keep a full cost worksheet that captures transaction fees, FX effects, payout timing, and dispute leakage.

- Complete your pre-invoice checklist before delivery starts.

- Apply your stage-based scenario playbook and upgrade setup when trigger signals appear.

Imagine you onboard a new client, and they want to pay in one currency while your account settles in another. Your worksheet shows tighter margin and slower fund access on your current route. You switch collection flow before sending invoice one. That is the right move.

Next steps are simple. Read the docs for your top two corridors, request access where controls are limited, and talk to sales when coverage details stay ambiguous. Then tighten your pricing rules with Value-Based Pricing: A Freelancer's Guide.

Frequently Asked Questions

Is Stripe or PayPal cheaper for international freelancers in real-world use?

No single winner stays cheapest across every corridor. Compare the full stack for each route: transaction fees, FX conversion, and withdrawal or payout cost. Stripe publishes a domestic card baseline of 2.9% + 30¢, but your real total in international payments can change with currency path and payout method.

Which platform is safer for cashflow when account holds happen?

Hold risk can still affect cashflow, so your operating rules matter. PayPal states payments can be held, and in one flow you should get your money 7 days after confirming the order status as Completed. Protect yourself with milestone billing, fast evidence collection, and a backup collection path before you start delivery.

When should I use PayPal for trust and when should I use Stripe for control?

Use PayPal when client checkout preference is the deciding factor. Use Stripe when your deciding factor is how currency path and settlement affect your margin on a specific route. In a stripe vs paypal international decision, match the tool to your current bottleneck, then review the choice every quarter.

Do Stripe and PayPal support the same countries and currencies?

No, and this is where teams make costly assumptions. Stripe highlights charging support in over 135 currencies, while PayPal highlights coverage across over 200 global markets and 140 different currencies. Treat those as starting signals, then verify presentment currency, settlement currency, and payout corridor for your exact client route.

What should I verify before accepting an international client payment?

Run a five point check every time: fee stack, FX path, payout or withdrawal timing, presentment versus settlement currency, and tax form logic. Define presentment currency as what the client sees at checkout, and settlement currency as what lands in your bank account. Save screenshots, confirmations, and transaction IDs so you can reconcile freelancer payments quickly when issues appear.

How do FX and withdrawal steps change my true margin on a project?

They can shift margin quickly. If charge currency and settlement currency differ, conversion moves your net before you even review transaction fees. Then withdrawal choice changes outcome again, for example a faster PayPal transfer can add a fee while a 1-3 day transfer can avoid that fee.

What records should I keep for VAT, W-8 or W-9, and year-end reporting?

Keep one audit pack per client and platform cycle. Store VAT records, collect W-9 when a payer needs U.S. taxpayer details, collect W-8BEN when a payer or withholding agent asks for foreign status documentation, and reconcile monthly platform exports to your books. Pull year-end forms such as 1099-K from platform dashboards when available.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Value-Based Pricing for Freelancers Under Real Payment Risk

Value-based pricing works when you and the client can name the business result before kickoff and agree on how progress will be judged. If that link is weak, use a tighter model first. This is not about defending one pricing philosophy over another. It is about avoiding surprises by keeping pricing, scope, delivery, and payment aligned from day one.

Future of Freelance Work in 2026 for Cross-Border Hiring Decisions

Before you scale cross-border freelance hiring, make one decision first: are you working from evidence you can actually use, or from broad trend claims that sound bigger than they are? That matters more than the headline. If your records are weak, fast sourcing can turn into compliance gaps or classification risk long before it becomes useful capacity.

How to Write a Privacy Policy for Your Freelance Website

A [privacy policy](https://freelancersunion.org/privacy-policy) is easier to defend in client due diligence when each statement traces to real behavior. Treat it as a working record, not footer filler: what personal data you collect, how you use and manage it, and how someone can raise a concern.