Quick Answer

Start with a go-or-no-go screen: for a spain beckham law case, confirm relocation-for-work facts, role classification, and whether Form 149 can be filed inside the six-month window. Then split each income stream into confirmed, unconfirmed, or disputed, and keep one dated record set across contracts, registrations, and payment trails. If ownership, mixed income, or advisor views conflict, pause and get a written eligibility memo before submission.

Spain Beckham Law for Independents Who Want Fewer Tax Surprises#

Make the go or no-go call early, then test it against dated checkpoints and records you can defend. The goal is predictable compliance, not aggressive tax engineering.

This guide is for freelancers and consultants with cross-border income, especially UK-linked cases. The practical question is not whether the regime looks attractive in a summary, but whether your facts, timing, and records still make sense when someone reads the move, the work setup, and the filings together. If you wait until returns are due to decide whether this route fits, you usually create avoidable risk on both sides of the move.

A cleaner approach is to decide early what story the file has to tell, then check whether every later record supports that story. If a contract date, move date, or payment trail points in a different direction, resolve that conflict before you start comparing tax outcomes.

Start with a short triage pass before you commit:

- Build one timeline for where you lived, where work was performed, and which filings remain open.

- Create a deadline map by jurisdiction and assign one owner to each filing date.

- Keep an evidence pack from day one, including records such as bank statements or receipts.

That first pass is intentionally basic. Its job is to reveal whether you have a timing problem, a missing-document problem, or a structure problem before you spend time arguing about rates.

If your case touches the UK, treat HMRC checkpoints as hard controls rather than background admin:

- If you need to complete a tax return for the previous tax year, tell HMRC by 5 October.

- If you are filing online for the first time, register for Self Assessment before using the service.

- If you have an existing account, reactivate it before filing to avoid delays.

- Pay your Self Assessment bill by 31 January.

- Some cases cannot use the online service, including if you lived abroad as a non-resident.

One of the most common problems starts before any filing. People choose a business structure without understanding liability and the reporting consequences that follow. A sole trader is personally responsible for business debts, while limited company owners are generally responsible only up to their financial investment. Even if Spain is the main question, that distinction affects how the wider file fits together. If you cannot produce a clean, consistent file in one review pass, stop and get specialist help before filing.

If you want a deeper dive, read Tax Guide for Digital Nomads in Thailand.

What the Beckham Law Actually Changes#

The regime changes tax treatment, but the operational side matters just as much as the headline. Qualifying arrivals can be taxed as non-residents while living in Spain. In practice, the harder part is not the benefit summary, but proving that your timing, move-for-work story, and documents support the treatment you plan to claim.

You will see several labels used for the same idea, including Beckham Law, Beckham Rule, and Special Tax Regime for Inbound Workers. Use those terms as orientation, not as proof that your case fits. A familiar label can make a borderline case feel settled long before it really is.

Public explainers also do not always point to the same legal anchor. One common reference is section 93 of the Spanish Income Tax Act. If the references vary, do not assume the difference is harmless. Check the exact provision being cited and the interpretation being applied before you file. That extra step is not academic. It is often where a confident summary turns into a less certain real-world answer.

| Treatment path | Typical summary in explainers | Practical risk if you over-assume |

|---|---|---|

| Regime path | Often described as 24% on qualifying Spanish income up to EUR 600,000, for up to 6 years | You assume every income stream qualifies and miss category limits |

| Standard resident path | Progressive resident rates are often described as rising, with top ranges cited up to 47% | You compare headline rates only and miss deductions, exclusions, or documentation demands |

Those headline figures are useful for a first screen, but they are not enough to file on. The real tradeoff is predictability versus scope limits. Some explainers note that standard resident deductions may not apply under this regime. Foreign-income treatment is a regular conflict point. One account says it is usually exempt, while another describes broader exclusions. That is why each income type needs its own review instead of a single yes-or-no assumption.

So when you model the choice, keep two columns in view: headline benefit and proof burden. A regime path can still be the wrong path if the file needs too many assumptions to hold together from the move date through the first return.

Use these checkpoints before you make a go decision:

- Confirm the move is for work and that you are still within the commonly cited six-month application window.

- Split income into clear buckets and mark each as confirmed, unclear, or disputed.

- Keep one evidence file with move-date records, contracts, and income records so filings stay consistent.

If your profile includes mixed consulting income and investments, or earnings near EUR 600,000, get written eligibility confirmation before filing. Once you are clear on what the regime changes in theory, the next question is whether your own facts make you a clean candidate in practice.

Fast Eligibility Check for Freelancers and Consultants#

Do the quick screen before you spend time modeling savings. If your timeline, relocation reason, and work setup do not stay fully consistent across your records, pause before treating this as a clean case.

Start by putting the core facts in one short file. The test is not completeness. It is whether the essentials are easy to date, explain, and compare against the rest of your records:

- Prior tax residency position in Spain.

- Why you are relocating now.

- How your work is structured today, including employer, clients, and ownership.

If those three points cannot be stated in a few plain sentences without hedging, that is already useful information. It usually means the case needs clarification before any benefit estimate is worth trusting.

Keep permit analysis separate from tax analysis. A Digital Nomad Visa route is not the same thing as a tax residency result, and visa labels are not interchangeable assumptions. Lock the permit track first, then assess tax residency on its own facts. This is a basic distinction, but it is one of the easiest places to build a confident plan on the wrong premise.

For Digital Nomad Visa cases, run a baseline check before you go further:

- Confirm you match the described profile, including non-EU/EEA status, age 18+, and remote work mainly for foreign employers or clients.

- Confirm Spanish-source income stays within the described limit of up to 20% of total income.

- Test tax residency separately using days in Spain plus economic and family-interest factors.

- Prepare evidence early, including documents that support your work setup, days in Spain, company activity, if relevant, and clean-record documents for Spain and prior-residence countries over the past five years.

Then compare that summary against your contract wording, invoice trail, and ownership records. The test is whether one reviewer would see the same operating story across all of them.

For independents, the weak point is often not whether the work is remote, but whether income sourcing, ownership, and the operating story still line up when someone compares the visa file, company records, and tax position side by side. That is where cases that looked simple in a summary often stop looking simple.

Use a hard if-then rule for borderline self-employment facts. If eligibility depends on uncertain income sourcing, mixed client geography, or ownership details, stop and get specialist validation before filing. That is especially important when the file can be read two ways and one version is much more favorable than the other.

Keep family planning in phase two. Confirm the principal applicant path first, then assess spouse or dependent implications once the main file is stable. If the principal file is still moving, adding household questions too early usually makes the decision harder to control rather than easier to finish.

Once the basic screen looks credible, the next step is to classify income line by line instead of assuming one answer covers everything.

What Income Falls Inside and Outside the Regime#

Income classification is not box-ticking here. It is one of the main controls that keeps a workable filing plan from turning into an assumption-driven one. Classify each stream before filing, and do not assume treatment for any line you cannot document.

For mixed-income freelancers, use a dual track for each bucket. First, note the possible treatment under the regime. Second, note any separate reporting duties that may still apply in another country. One bucket can be clear while another remains unsettled, and that is normal. The mistake is pretending the unsettled bucket is resolved because the rest of the file looks tidy.

| Income bucket | What you can confirm now | What stays uncertain until formal review |

|---|---|---|

| Service or employment income | Contracts, invoices, payment dates, where work was performed | Final inside or outside treatment under the regime for your facts |

| Rental or other non-trading income | Ownership records, statements, payment trail | Whether it follows the same treatment as service income |

| Capital gains or one-off disposals | Disposal date, cost-basis records, proceeds | Final classification and applicable tax treatment |

Do not merge buckets just because cash lands in the same account. The filing question follows the nature of the income and the records behind it, not the convenience of how you track payments day to day.

Keep one evidence file per bucket. At minimum, keep bank statements or receipts so Self Assessment returns can be completed correctly. A simple ledger works well here. Mark each line item as confirmed, pending review, or disputed. That one control makes it much easier to see which parts of the filing logic are solid and which parts still need a written position.

For UK-side compliance, keep Self Assessment separate from the Spain analysis. HMRC describes Self Assessment as the system used to collect Income Tax. Filing can apply to self-employed people, but also to people who are not self-employed, including some rental-income cases. HMRC also states that people and businesses with other income must report it in a Self Assessment tax return. The UK reporting clock does not stop just because the Spanish position is still under review.

That means you may need to keep moving on one filing track while pausing another. Operationally, that is normal. The risk comes from letting an unresolved Spanish analysis delay a UK step that has its own hard deadlines.

Use deadlines as hard controls while classification is still in progress. For the 6 April 2024 to 5 April 2025 tax year example, the stated notify date is 5 October 2025, and late notice can trigger a penalty. Online filing can be done on or after 6 April after year end, the Self Assessment bill is due by 31 January, filing can be delayed if an existing account is not reactivated, and some cases cannot use the online service, including people who lived abroad as a non-resident.

If any income bucket is still unclear near filing, pause and get written review before submission. No document, no assumption. That same discipline matters when you compare this route with standard resident taxation, because the better-looking headline is not always the safer answer.

Beckham Law Versus Standard Spanish Resident Taxation#

Do not compare these routes on headline rates alone. Choose the path you can defend with dated records and clear assumptions. If what you want most is stable planning, the better option is usually the one with fewer unresolved variables, not the one with the best-case spreadsheet.

Under the regime route, qualifying arrivals are described as taxed like non-residents while living in Spain. A common headline comparison is 24% on Spanish-sourced income up to EUR 600,000 versus standard resident IRPF rates that are progressive and can reach 47%. That comparison is useful, but only as a first pass. The practical tradeoff is that qualifying treatment may lower tax on eligible Spanish-sourced income, while standard deductions are described as unavailable or limited and some income types may be excluded. Foreign-income treatment is described inconsistently across secondary explainers, so it needs separate verification before you rely on it.

| Decision area | Beckham Law (Special Tax Regime for Inbound Workers) | Standard resident IRPF |

|---|---|---|

| Core treatment | Non-resident-style treatment for qualifying arrivals | Resident progressive treatment |

| Rate anchor in this guide | 24% on Spanish income up to EUR 600,000 | Progressive rates, with top exposure cited at 47% |

| Foreign-income certainty | Secondary explainers conflict, so verify before filing | Outside this special-regime comparison, confirm resident treatment separately |

| Deductions and assumptions | Standard Spanish deductions are described as unavailable or limited, and some income types may be excluded | Resident assumptions should be validated case by case |

| Key checkpoint | Move to Spain for work and apply within 6 months | The six-month application checkpoint is specific to Beckham treatment |

This guide does not provide regional comparisons for Madrid, Catalonia, or Valencia, so confirm local impact before you lock your forecast. That matters because a model can look clean in national-level summaries while still breaking down when local detail or exclusions are applied.

Use this decision rule:

- If your model depends on uncertain foreign-income treatment, pause and get a written position before filing.

- If you value stable forecasting, prioritize the route with clearer documentation tests.

- If you cannot prove move-for-work facts and six-month timing, do not plan around regime assumptions.

In practice, this is often where people discover they were comparing a clean special-regime scenario with a messy resident scenario, or the reverse. Compare realistic versions of each path, using only income lines and records you can actually support.

Keep one dated evidence folder with move-for-work support, application-timing documents, and the income-bucket ledger from the prior step, plus a short memo showing what is confirmed versus pending. The regime is often described as lasting up to 6 years, so early assumptions can carry across multiple returns. Once you choose the tax path you want to test, your work setup becomes the next variable that can change the answer.

Which Work Setup You Have and Why It Changes the Answer#

Your work setup changes the answer faster than many public summaries admit. Employee, independent consultant, director-shareholder, and mixed-role cases do not create the same filing posture, even when the move itself looks similar on paper.

You will often see this special regime discussed under the Beckham label and described as allowing non-resident taxation treatment for qualifying people in Spain. The file is still decided on provable facts, not on labels. If you are both a service provider and a company director, treat the case as high risk for DIY unless a specialist has already reconciled those roles in writing.

| Work setup | First checkpoint | Frequent failure mode | Evidence to prepare now |

|---|---|---|---|

| Employee, Spanish or foreign employer | Confirm an employment contract, Spanish or foreign employer, and move-for-work timeline | Assuming foreign-employer and local-employer cases always follow the same steps | Employment contract and dated move and work records |

| Independent consultant | Confirm whether a Digital Nomad Visa-linked exception is needed in your case | Assuming self-employed status qualifies by default | Visa and work-status records, plus consistent service documentation |

| Director-shareholder | Confirm ownership, including whether it is below the cited 25% threshold, and control before submission | Ignoring ownership and route-specific conditions tied to your path | Ownership and director records that support your filing position |

| Mixed role, consultant plus director | Confirm both role narratives are consistent | Using one story for tax and another for company records | One reconciliation memo across role, ownership, and filing logic |

A simple way to test this is to write one sentence describing your role and then see whether your contract, company records, invoices, and visa narrative all support that same sentence. If they do not, fix the mismatch before you file.

Guidance is described as expanded from January 1, 2023 to include some people employed by foreign companies, but that does not remove the need for careful classification. It simply means you should not assume older summaries still capture the current scope without checking your own facts.

Treat the Digital Nomad Visa and Entrepreneur Visa as potentially different compliance paths, not interchangeable labels. People often compress them into one story because both involve relocation and work, but that shortcut can create contradictions in the record that are difficult to unwind later.

Before filing, verify these points:

- The six-month application window from your move-for-work date.

- Any abroad-work share you rely on against the stated 15% limit in this guidance.

- Internal consistency across contract, visa, and company records.

After submission, the Spanish Tax Agency reviews the request, so your pack should read as one coherent story with dated documents and clearly flagged open points. Once that story is set, put dates against it immediately. Good classification without good timing still fails in the real world.

Related: The Best High-Yield Savings Accounts for Freelancers.

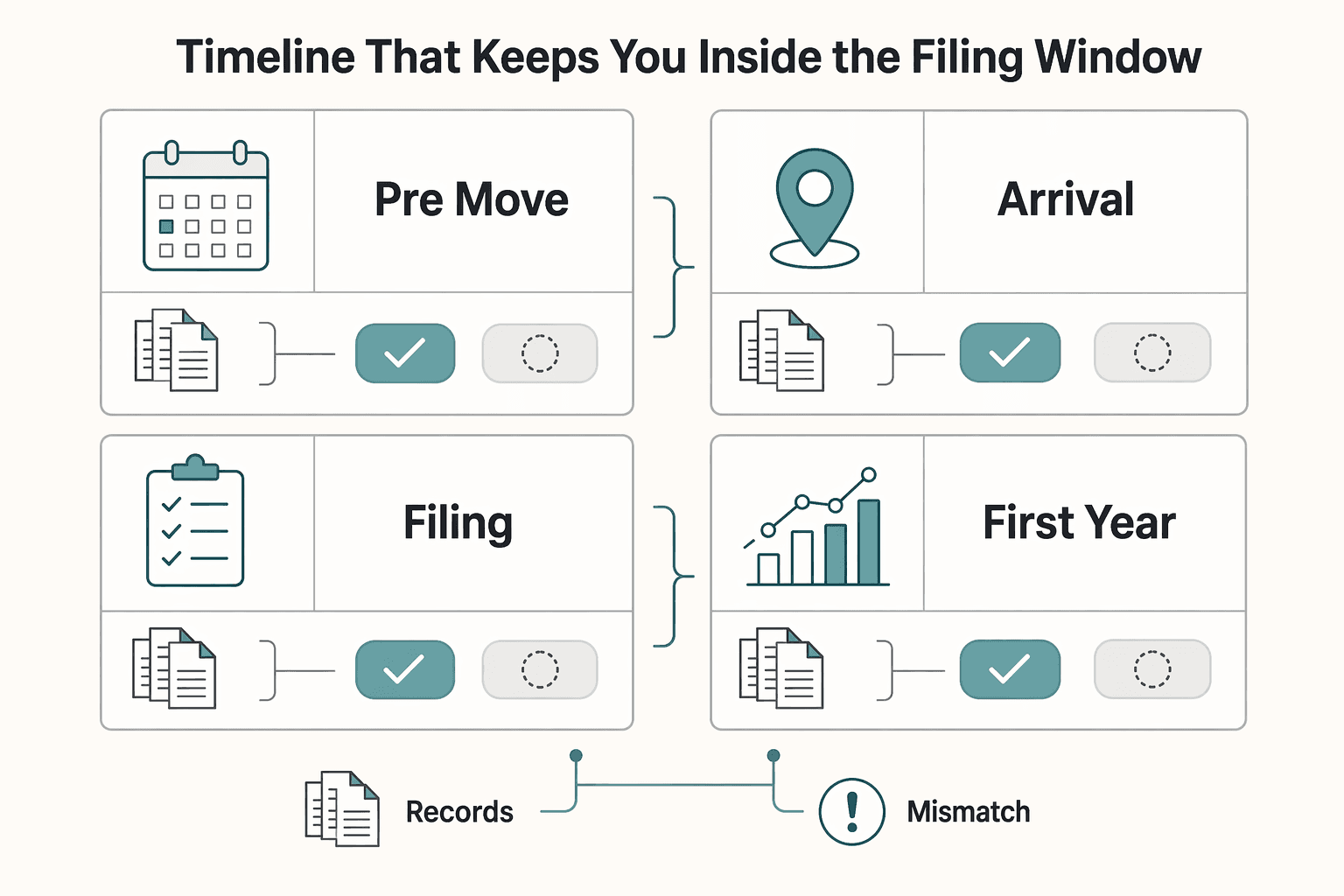

Timeline That Keeps You Inside the Filing Window#

At this stage, calendar discipline matters as much as technical interpretation. Keep one dated timeline, assign one owner, and mark each date as confirmed or pending. Do not build your filing plan on pending dates, especially if those dates control eligibility, registration, or a separate home-country return.

Use the same date format everywhere and record the source of each date. A date copied from a contract, a portal acknowledgment, and a personal note may look identical, but they do not carry the same weight if questions arise later.

The point of the timeline is simple. It forces every task, document, and filing decision into one sequence so you can see where assumptions are still doing too much work. If dates live across emails, chats, and personal notes, it becomes much harder to tell what is actually ready.

Use the timeline by phase:

| Phase | Practical action | Verification checkpoint | Common failure mode |

|---|---|---|---|

| Pre-move | Open one timeline file, map relocation dates, and assign document owners | Each item has an owner, due date, and status | Deadlines sit across chats and no one owns them |

| Arrival | Complete Social Security and local registration tasks and capture dated evidence | Each step has a saved receipt or timestamp | Tasks are done, but proof is missing |

| Filing prep | Build the package early and leave correction buffer | Assumptions are logged as confirmed versus unconfirmed | Assumptions are presented as settled facts |

| First year | Run internal periodic evidence checks and update your file notes | Short dated notes record what changed | Records drift from what was filed |

For cross-border Social Security, work from what is concrete. Totalization agreements assign coverage to one country and exempt Social Security taxes in the other country. A Certificate of Coverage is the proof document. Employers and self-employed people can request certificates online and track status by control number. Build buffer into the timeline around that process. Follow-up is requested after 90 business days, and if a certificate is issued, mailing can take up to two more weeks. Treat this as documentation planning only, not proof of regime eligibility or Spanish tax outcomes, and not evidence of any specific filing deadline under the regime.

Use these rules when time pressure starts to build:

- If a required field is missing, stop and complete it before submission because the request will not transmit.

- If a key document is still pending near your target date, escalate in writing and log the decision path.

- If transmission risk is a concern, remember web transmission cannot be guaranteed against interception or decryption, submit only required data, and archive copies immediately.

A good timeline is more than a calendar. It is the control that keeps filing order tied to issued proof rather than expected proof. Once the dates are under control, the next job is to build a document pack that supports the same sequence.

Document Pack You Should Build Before You File#

Build one internal document pack before you file so your dates, role description, and payment trail stay consistent under review. This is preparation discipline, not a guarantee of approval and not an official list of required documents.

A solid pack should let someone else follow your logic without guessing which version is current. That is the practical test. If a reviewer has to infer your move date, business role, or income source from scattered files, the pack is not ready yet. You want a file that tells one story, with each document reinforcing rather than weakening the others.

Think of the pack as a working file, not a static folder. As soon as one date changes or one document arrives, update the index and check whether any other file now needs the same correction.

Build four working files and keep them aligned#

Use these four working files as your consistency check:

- Core identity and setup file: key ID details, relocation timeline notes, and administrative records you may need to reference.

- Work evidence file: agreements, assignment records, and role descriptions that match your filing narrative.

- Income trace file: invoices, payment records, and account records that reconcile to what you report.

- Household context file, if relevant: personal records tied to household circumstances and timeline.

If details conflict across files, resolve them before submission. In practice, the conflict is often small, such as a date variation, a role description that drifted, or a payment label that does not match the contract. Small conflicts matter because they make a larger filing position look less reliable than it may actually be.

This is also the stage where version control matters. Keep one current file owner, note the last update date, and avoid parallel drafts that quietly introduce new inconsistencies.

Keep Social Security documentation on a separate track#

For cross-border cases with possible U.S. coverage, totalization agreements assign Social Security coverage to one country and exempt contributions in the other. The U.S.-Spain agreement has been in force since April 1, 1988. When U.S. coverage applies, a U.S. Certificate of Coverage is proof of exemption from foreign Social Security taxes. That certificate supports Social Security treatment only, not regime eligibility.

Employers and self-employed applicants can request certificates online. Complete all required fields, since incomplete fields block transmission, and missing information may prevent an accurate and timely decision. Track the case through statuses like Received, Pending, and Completed, and archive the final notice sent by mail or email.

Plan buffer time instead of assuming the document will appear when you need it. Follow up after 90 business days, and mailing can take up to two weeks if a certificate is issued. Because web-submission confidentiality cannot be fully guaranteed, submit only required information and save copies immediately.

Before filing, keep a dated residency log so your timeline, registrations, and travel days stay consistent: Use the Tax Residency Tracker.

A clean pack helps, but it does not solve conflicting public guidance by itself. You still need a safe way to decide which explanations are relevant and which are not.

Where Public Explainers Conflict and How to Verify Safely#

Conflicting explainers are a risk signal, not a reason to guess. Verify relevance first, then depth, before you act. This is a screening process, not a shortcut to a legal conclusion.

Short summaries often miss material scope and detail, and fragmented write-ups can produce very confident advice built on different assumptions. That is why two explainers can sound equally certain while pointing in different directions. A page can look official and still tell you almost nothing about the filing question you actually have.

The safest response is usually slower and narrower: identify the exact claim you want to rely on, strip away the marketing language around it, and verify only that point first.

Relevance check before legal check#

Start by confirming the source is really about your question. Off-topic results — such as cookie-consent pages or general technology-policy pieces — do not provide filing detail for this regime and should be set aside before you draw any tax conclusion.

That first filter saves time. It also reduces the temptation to treat any official-looking text as support when it is really just noise.

Verification loop#

For each public claim, run one repeatable pass:

- Write the claim in one sentence and label it

confirmedorunconfirmed. - Read the full underlying document, not only a summary, and check any recommendations section it points to.

- Note what the text does not resolve, especially conditions, exclusions, and definitions.

- Treat references to other authorities as pointers until you verify the underlying text directly.

- Save a short note on why you accepted or rejected the claim.

Keep the notes short enough that you will actually maintain them. The goal is not to build a research archive. It is to preserve the reason you relied on one interpretation and set aside another.

Disagreement rule before you file#

If interpretations still differ, pause filing prep until both positions are in writing. Ask for the fact pattern used, the interpretation applied, and the remaining uncertainty, then compare both against your document pack. If assumptions still differ, keep the item unconfirmed until those assumptions are resolved.

This matters most in the first year, because process mistakes compound quickly when timing, classification, and cross-border records all move at once. The cost of waiting for one written clarification is usually much lower than the cost of filing around a guess.

Expensive Mistakes to Avoid in the First Year#

Most first-year losses come from process errors rather than one dramatic legal surprise. Keep confirmed separate from unconfirmed, and do not file on assumptions just because the deadline is getting closer.

Think of the first year as three risk lanes that need to stay separate: Social Security coverage proof, income-scope conclusions under the Beckham Rule, and document control. If you blur them together, one delay can create a second problem somewhere else in the file.

Mistake 1 Planning around unissued Social Security proof#

Do not treat coverage proof as optional or immediate. Under totalization agreements, coverage is assigned to one country, and the other country's Social Security taxes are exempted for employer and employee. For U.S.-Spain coordination, the Certificate of Coverage is the core proof document, and the agreement date anchor is April 1, 1988.

The main failure mode is operational, not theoretical. Incomplete required fields block submission, and missing information can delay accurate processing. Track status checkpoints, Received, Pending, and Completed, in a dated log so your filing sequence reflects current reality rather than what you hoped would arrive.

Plan timelines conservatively. SSA asks requesters to allow 90 business days before follow-up, and issued certificates may still take up to two weeks to arrive by mail. If your plan depends on a certificate that is still Pending, re-sequence instead of forcing assumptions.

Mistake 2 Treating scope under the Beckham Rule as automatic#

Do not decide income treatment from headline summaries; a blanket position on which non-Spanish income categories fall inside or outside the regime is not defensible.

Review income category by category, and keep each one marked confirmed or unconfirmed until you have a written rationale. If a category is still unconfirmed, do not present it as settled in your filing draft. This is where people often talk themselves into certainty because one income stream is clear and the rest look similar. Similar is not the same as confirmed.

A common practical error is letting one favorable interpretation spread across the whole file. Resist that. The right way to handle uncertainty is to isolate it, label it clearly, and decide whether it needs specialist review before submission.

Mistake 3 Letting records drift after filing prep starts#

Weak evidence hygiene can turn manageable questions into expensive rework. Keep one dated working file and update related records as soon as any material fact changes.

Drift usually starts with something small, like a revised contract label, a new payment reference, or a late-added travel note. If nobody updates the master file, the inconsistency tends to show up only when you are already drafting the return.

Use simple controls:

- Log each material document with date, owner, and status.

- Keep unresolved items marked

unconfirmeduntil resolved in writing. - Reconcile payment records against reporting drafts before submission.

- Escalate any pending document that can change filing order.

These controls do not determine eligibility by themselves, but they do keep the first-year file coherent and reduce avoidable corrections. If you are already missing one or more of these controls, that is often the point where specialist help stops being optional and starts being efficient.

When to Bring in a Tax Professional Immediately#

Bring in a professional as soon as key facts stay unconfirmed across structure, classification, or filing route. If your case can reasonably be read more than one way, get specialist input before you submit anything.

Good advice should reduce ambiguity, not hide it. If you leave a conversation with more confidence but no written logic, no checklist, and no clear owner for open items, you probably did not get what you actually need.

Trigger 1 Mixed income and ownership complexity#

Mixed income plus ownership and control is an immediate escalation signal. In UK terms, choosing sole trader versus limited company affects both tax treatment and legal responsibilities, and directors have specific rules when taking money out of a company.

If you are unsure whether your activity counts as trading, contact HMRC for advice before filing. Do not lock in a return while core classification is still unclear. This matters even more when the same facts are being used to support both a Spanish position and a UK one.

Trigger 2 Cross-border overlap with filing constraints#

Escalate quickly when cross-border facts collide with filing mechanics. UK Self Assessment online filing requires a UTR, and some people cannot use that online service, including people who lived abroad as a non-resident. In those cases, you may need commercial software or other forms.

Use hard checkpoints, not memory. For the 6 April 2024 to 5 April 2025 tax year example, notify HMRC by 5 October 2025 if you need to file, and pay by 31 January. If your residency position is still shifting near those dates, escalate so filings stay consistent.

Trigger 3 Director status or conflicting professional views#

Director status adds complexity because ownership, control, and withdrawal decisions can change how your position is handled. If professionals give conflicting advice on classification or filing approach, treat that as a stop sign.

Ask for each view in writing with assumptions clearly stated, then resolve the conflict before submission. Conflicting professional advice is not just annoying. It is evidence that your facts or the legal interpretation need tighter framing.

Ask for deliverables, not broad reassurance#

When you do bring someone in, ask for outputs you can execute and audit:

- A written memo separating confirmed facts, assumptions, and open questions.

- A filing checklist with each document, filing channel, owner, and due date.

- An annual review calendar tied to deadlines and major fact changes.

- A recordkeeping list, including bank statements and receipts.

These deliverables are practical controls, not formalities. They can reduce late-filing risk and help you avoid interest or penalties tied to late filing or payment.

The Practical Next Step for a Low-Stress Decision#

For a low-stress decision, use a simple sequence: decide, prepare, then verify. Most avoidable friction comes from unresolved or conflicting facts, so anchor each step to evidence you can actually produce.

- Run a go or no-go screen.

Use one page with three buckets: confirmed, unconfirmed, and conflicting. Put each key fact on one line, attach the evidence you already have, and assign an owner for missing proof. If core facts are still unconfirmed or conflicting, treat that as a no-go for filing this week. Add an IMPORTANT DATES grid with named checkpoints, decision lock, document freeze, specialist review, and planned submission, so deadlines stay visible.

- Assemble the document pack before final advice.

Make sure each claim maps to one document you can retrieve quickly. Keep a short index with file name, last-updated date, and owner. Include the notes and assumptions that still need confirmation. Capacity limits are a real execution risk. When time or ownership is tight, small gaps turn into deadline problems very quickly.

- Schedule one focused specialist check before submission.

Ask for a targeted review, not a full rewrite. Share your go or no-go sheet, document index, and the few decisions you need cleared. Ask for written outputs: what is ready, what must change, and what is unresolved. If guidance conflicts, pause and resolve that conflict in writing before submitting anything.

In practice, this is mostly about fit, deadline control, and clean records. For broader mobility context, read The Ultimate Digital Nomad Tax Survival Guide for 2026, then complete the three steps in order. When facts are complex, a light-touch consult is a practical guardrail.

The aim is not to produce a perfect file on day one. It is to reach submission with fewer moving parts and a clearer record of what you knew, what you verified, and what you escalated.

If your setup spans multiple countries and clients, align your payment operations with audit-ready records early: Talk to Gruv.

Frequently Asked Questions

What is Spain’s Beckham Law in one sentence?

Spain’s Beckham Law, officially the Special Tax Regime for Inbound Workers, can let qualifying people living in Spain be taxed as non-residents. The current definition is referenced in Article 93 of the Personal Income Tax Act. You may also see it called the Beckham Rule.

Who usually qualifies for the Beckham Rule and who usually does not?

The profile most often described is someone moving to Spain for work through a local employment contract or an international transfer. Self-employed workers are generally outside the regime, so freelancers should be careful about self-classifying too quickly. Directors or shareholders, including majority or sole shareholders, may qualify if the company is not patrimonial.

How long does Beckham Regime Spain treatment usually last?

One description puts the duration at up to 6 years. Another notes 2023 updates, including a change described as reducing a prior non-residency requirement from 10 years to 5 years. Treat this as a planning baseline and confirm your exact timeline before relying on it.

What income is generally treated under the special regime and what is commonly outside it?

The regime can involve limitations, including loss of standard Spanish deductions and exclusion of some income types. Available sources also conflict on foreign-income treatment, with one saying usually exempt and another saying completely excluded. Use that conflict as a signal to map income category by category instead of assuming one rule covers everything.

Does having a Digital Nomad Visa automatically mean I qualify?

No, it does not automatically mean you qualify. One source says digital nomads with foreign employment contracts became eligible as of December 2023, which is narrower than automatic qualification for all visa holders. The same material points to Form 149, supporting relocation and fiscal documentation, and a six-month filing window after moving to Spain and starting professional activities.

Can spouse and children be included under the same treatment?

This grounding set does not establish automatic family inclusion. Treat family coverage as a separate eligibility question. Get a written position tied to your household facts before filing.

What are the fastest signs I should stop DIY and hire a specialist?

Stop immediately if your eligibility view changes depending on how your role is classified, or if director and ownership facts are unresolved. Escalate when professional opinions conflict on qualification or filing approach. Also escalate if your Form 149 window is running and your relocation or fiscal documentation is still incomplete.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 3 external sources outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Thailand Tax for Digital Nomads Without Residency Mistakes

The most expensive mistakes here happen before anyone opens a tax return. People pick a visa, assume the tax answer comes with it, then try to rebuild the year from scraps after the fact. By then, the damage is usually not one dramatic error. It is a pile of small gaps: an unverified day count, a transfer with no clear purpose note, invoices that do not line up cleanly with payments, and assumptions nobody wrote down when the facts were still fresh.

The Best High-Yield Savings Accounts for Freelancers

Start with access fit, not yield. For a freelancer, the right savings account is the one you can open, fund, and keep using with self-employed income, not the one with the loudest APY banner. You are not choosing a trophy rate. You are choosing a place for reserve cash that will still make sense when payments arrive in bursts, a client pays late, or tax money needs to sit untouched for a while. That is where a big promotional number can pull people off course.