Quick Answer

Start by running your solopreneur economy plan as an operations sequence, not a motivation story: lock signed MSA/SOW terms, complete compliance gates before sensitive money actions, and reconcile every payment from invoice to ledger with dated evidence. Use public trend numbers as background only, then make growth decisions from your own monthly records. If you cannot pull contract, tax-form status, payout proof, and matching ledger detail quickly, fix controls before adding volume.

The solopreneur economy is big but this article is about operating it well#

Treat this as an operating guide, not a trend recap. Here, a solopreneur means one person running the business end to end, not occasional side work.

Market momentum matters as context, not as a promise for your niche. In secondary reporting published Feb 15, 2026, Inc cited 29.8 million solopreneurs, an estimated 82 percent share of U.S. small businesses (with variation across sources), and a 2022 contribution of 6.8 percent, or $1.7 trillion, of economic activity. The same coverage also says many freelancers are struggling with current-market uncertainty. Keep the warning in view: growth headlines and operating stability are different.

Use a simple test: can you add clients without creating contract disputes, compliance delays, or cash confusion? If growth still depends on memory, inbox threads, and disconnected tools, higher volume will expose gaps fast.

Use this basic sequence for the quarter:

- Contracts first: Start work only after signed core terms and scope are in place, including payment timing and change handling.

- Compliance next: Complete required identity, tax, and data-handling checks for your client type before sensitive financial activity.

- Cash movement third: Map invoice date, receipt date, payout date, and ledger posting so each payment has one traceable path.

- Records always: Keep one client evidence packet with signed terms, tax docs, billing contact, invoices, and reconciliation proof.

Keep the sequence strict when pressure rises. If payment is late or a client requests a rush start, do not skip steps and promise to clean it up later. Most cleanup comes from exceptions created in urgency.

Run one monthly checkpoint. For any active client, retrieve signed terms, tax form status, invoice number, payout receipt, and matching ledger line in under five minutes. If you cannot, pause acquisition experiments and fix record discipline first. One failure mode to watch is paid but not matched activity, where cash arrives but the accounting loop never closes.

Keep one distinction in mind: freelancers are often paid task by task, while solopreneurs may target more repeatable revenue. Use that as a decision lens, not a purity test.

Read the market signal without over-reading the hype#

Use market signals only when you can verify what they say and how reliable they are. If access is limited, the page is in an error state, or the claim is opinion-led, treat it as context rather than a planning input.

Apply this filter before any claim goes into your operating plan:

- Write the claim in one sentence.

- Label the source type as primary data, reported summary, or opinion.

- Mark access state as full text, member-only, or error page.

- Record the publication date.

- Set status as usable now, context only, or hold.

| Known facts | Unknowns to keep open |

|---|---|

| A Mar 15, 2026 Substack post is framed as "without hype or burnout," which signals guidance or opinion format rather than statistical reporting. | Failure rates in your exact niche. |

| A Feb 26, 2026 Medium piece is marked member-only, so detailed claim validation is limited from the excerpt alone. | Sector durability over the next 12 months. |

| The Entrepreneur page repeatedly shows an error state, and a partial "$75 million" snippet is not sufficient as stand-alone evidence. | Method quality and how well claims transfer to your audience. |

Before you change targets, run a quick verification check. Review three claims in your notes and confirm each has a clear origin, date, and usable access state. If any element is missing, downgrade that claim to context only and keep commitments tied to your own pipeline and results.

Keep a short claim log so review is fast. One line per claim is enough: claim text, source type, access state, date, status, and what decision it affects. If a claim cannot pass that test, it does not belong in your plan.

Define your business model before you pick tools#

Pick how you win work and deliver it before you choose software. In a one-person business, the bigger risk is mixing channels and operating styles until scope, pricing, and expectations drift.

A solopreneur is one person running a business without employees, often handling delivery, marketing, and customer service directly. CNBC describes this segment at 29.8 million solo entrepreneurs contributing $1.7 trillion, or 6.8 percent of U.S. economic activity, and notes California at 3,502,950 solo businesses in 2022. Keep those numbers as market context, not as a template for your offer.

Keep channels distinct:

- Platform work, for example Fiverr or Upwork.

- Direct client acquisition, such as referrals or outreach.

- Social discovery paths, including TikTok.

Each channel brings different expectations. Social discovery channels can offer low-cost access to potential customers, but lead quality still depends on how clearly you define your offer.

Then choose your operating identity deliberately. If work is mostly ad hoc, freelancer-style positioning can fit. If scopes repeat, shift toward a solo company approach with standardized offers, repeatable onboarding, and clear written terms when appropriate.

Set one rule and apply it consistently: as a default, document scope and payment expectations in writing before delivery. Once the model is clear, tool choices become simpler because each one supports a defined way of working.

A simple check helps prevent tool sprawl: for every tool you keep, state the single decision it supports and who checks its output monthly. If you cannot answer both, remove that tool from the stack. You might also find this useful: The Best Project Management Tools for Freelance Developers.

Build the legal and contract spine before revenue scale#

Set your contract baseline before you scale revenue, or growth can expose preventable disagreements on scope, timing, and delivery.

| Term area | Written detail |

|---|---|

| Scope changes | How scope changes are requested and approved. |

| Invoicing and payment | When invoices are issued, when payment is due, and what happens if payment is late. |

| Accepted delivery | What counts as accepted delivery. |

| Ownership | When ownership transfers for paid work, and what is excluded. |

| Disputes | How disputes are handled if direct resolution fails. |

The risk is operational, not theoretical. Gusto reports that more than four in five U.S. small businesses have no employees, and that one in three new solopreneurs hired at least one contractor in 2024. Even in an owner-only model, complexity can rise as projects, collaborators, and client expectations expand.

Before kickoff, make these terms explicit in writing:

- How scope changes are requested and approved.

- When invoices are issued, when payment is due, and what happens if payment is late.

- What counts as accepted delivery.

- When ownership transfers for paid work, and what is excluded.

- How disputes are handled if direct resolution fails.

Add practical detail where disagreements usually start. Spell out what a valid change request looks like, who can approve it, and when the delivery date resets. Define acceptance in plain terms so both sides know when a milestone is complete.

Use one verification checkpoint for every new client file:

- Signed agreement documents covering core terms and project scope.

- Confirmed billing contact.

- Written acceptance of payment terms.

- Dated versions of key drafts and approvals so decisions are traceable.

If you see repeated scope renegotiation, pause new intake briefly and tighten your templates before taking more work. Speed can support growth, but clarity helps protect margin.

When a dispute does appear, document the exact clause, the version date, and the decision taken. The point is not legal theater. The point is making future disputes less likely.

Set money movement and reconciliation rules from day one#

Set money movement rules before volume rises. Choose your rails early, and keep one traceable path from invoice to payout to ledger so month-end close stays reliable.

Choose collection and payout rails early#

Use invoicing as the default collection rail, then add receiving options only when they remove real client friction. Virtual Accounts (VBA) may reduce friction where supported, but each added rail can increase the chance of mismatched references, fees, or settlement timing issues.

Apply a simple gate before adding another rail: if the current month still has unresolved payment matches, do not expand yet. A smaller setup with clean matching is stronger than a larger setup that needs constant manual cleanup.

Before you add a new rail, test it with your bookkeeping in mind:

- Confirm where the payment reference appears in your records.

- Confirm who checks fee deductions and timing differences.

- Confirm how exceptions are logged when references are missing.

Set the cross-border ownership line#

For cross-border sales, define up front who handles billing operations in practice. If this applies to your setup, decide when you will use Merchant of Record (MoR) support and when your own entity will handle billing responsibilities, then document that choice in plain language.

Make these roles explicit:

- Who issues the final customer charge.

- Who keeps billing records and handles exceptions.

- Who investigates mismatched settlements, and by when.

This decision needs one owner and one written rule. If ownership is unclear, exceptions can sit unresolved while each party assumes someone else is handling them.

Reconcile from invoice to ledger with evidence#

Treat monthly close as a control checkpoint. If invoice data, payout data, and bookkeeping records live in different tools, close quality can drop unless you keep a consistent method to match each transaction across tools.

For each paid invoice, keep a clear link to one payout record and one ledger entry, with timestamped evidence in one place. QuickBooks Solopreneur is described as built for one-person businesses and as automatically importing and categorizing transactions after bank and card accounts are linked. Use that automation as a first pass, then review high-value or unusual items before close.

Use the same close sequence each month so problems are easier to spot:

- Confirm invoice status and collected amount.

- Match each payment to payout evidence.

- Post or verify ledger entries.

- Investigate unmatched items and assign ownership.

- Record final close notes with dated resolution details.

Prevent the same failure every month: paid but not matched with no owner assigned. Assign investigation ownership as soon as an exception appears, capture timestamped evidence, and log the resolution decision so your cash position stays trustworthy.

Add compliance gates early instead of retrofitting under pressure#

Set compliance checks before sensitive money actions so exceptions are handled early, not reconstructed later. In a one-person business, this is mostly operating discipline: clear gates, named owners, and dated decisions.

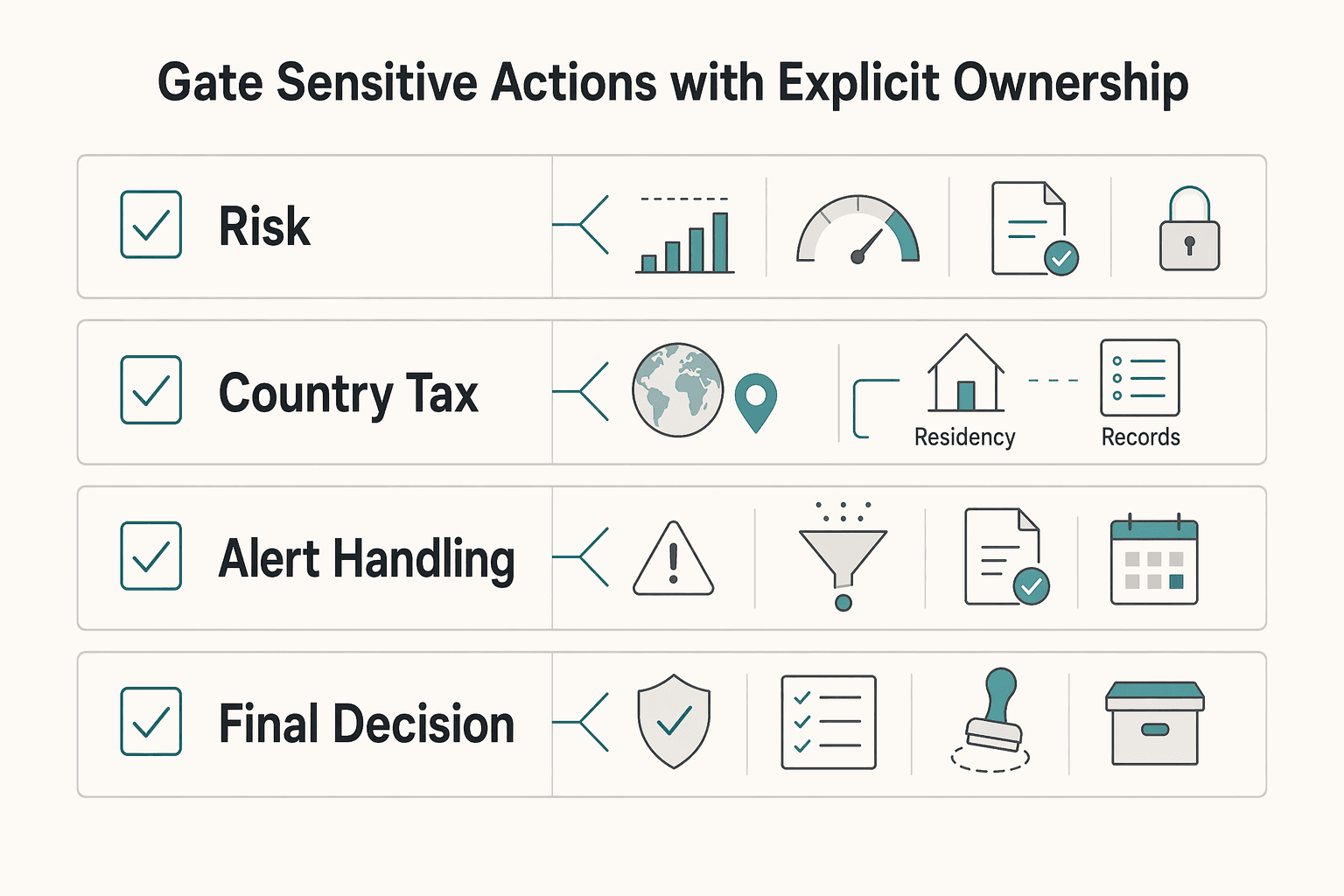

Gate sensitive actions with explicit ownership#

Use a clear internal sequence for sensitive actions that matches your policy and risk profile. This is an internal control rule for consistency, not a universal legal sequence.

| Approval record item | What to capture |

|---|---|

| Risk-check status | Required risk-check status with completion date. |

| Country and tax residency | Country of activity and declared tax residency. |

| Alert handling | Alert outcome, escalation owner, and resolution deadline. |

| Final decision | Final decision log with timestamped evidence. |

Require one checkpoint record per client or payee before approval:

- Required risk-check status with completion date.

- Country of activity and declared tax residency.

- Alert outcome, escalation owner, and resolution deadline.

- Final decision log with timestamped evidence.

If a risk alert is unresolved past deadline, pause payout until a named reviewer closes it. Keep the decision trail in one place, not across inboxes and chat threads. When review happens later, you should be able to see what was checked, who approved it, and what remained open at the time.

Intake tax forms before cash leaves#

Collect tax forms during onboarding, not as quarter-end cleanup. For U.S.-connected payments, keep required tax documentation status in the same approval record.

Add a recurring reporting-readiness review so filing decisions are made from complete records. If you cannot show who validated the documentation and when, quality drops and rework rises.

Treat missing or expired tax documentation as a blocked state, not a reminder item. Keep a visible status for each payee so payout decisions and documentation status cannot drift apart.

Keep an international review calendar for FEIE and FBAR#

Put international reviews on a calendar because eligibility and reporting details can change by year and by facts. For FEIE, current limits are $130,000 for 2025 and $132,900 for 2026 per qualifying person, with housing-expense limits generally tied to 30 percent of the FEIE maximum, or $39,000 for 2025 and $39,870 for 2026. FEIE applies to qualifying individuals and to foreign earned income from services performed in a foreign country, so treat qualification as an active check.

For FBAR tracking, keep the mechanics consistent all year: record a reasonable approximation of each account's maximum value during the calendar year, convert non-U.S. currency using the Treasury rate for the last day of the year, and round up to the next whole U.S. dollar, for example $15,265.25 becomes $15,266.

A simple year-end prep routine helps. Verify each account's maximum value record. Verify currency conversion basis. Verify the rounding method in your worksheet before filing work begins. Confirm exact applicability before acting.

Choose growth path with explicit tradeoffs#

Compliance gates do not choose your staffing model. Keep core delivery solo first, use specialist contractors when demand spikes, and consider hiring only when demand is consistently stable enough to carry fixed payroll.

Use market signals as context, not command#

Trend data can support either path, so treat it as context, not a decision rule. A 2024 Forbes piece described a shift away from team scaling toward solo entrepreneurship, and a 2025 trend report said it surveyed over 1,000 solopreneurs while referencing nearly 30 million solo-run businesses in the U.S. Useful signals, but not a hiring trigger.

Separate market narrative from day-to-day reality: broad trends show momentum, while your pipeline, margins, and delivery rhythm are better guides for whether fixed headcount is sustainable.

Match capacity to volatility#

Use one simple rule tied to demand volatility:

| Demand shape | Better first move | Main cost of that choice |

|---|---|---|

| Spiky or seasonal demand | Stay solo and add contractors by project | More coordination and quality review effort |

| Stable, repeatable demand | Evaluate a hire | Higher fixed cost and admin load in slower months |

| Mixed demand with uncertain sales cycle | Keep a hybrid model | Slower standardization across delivery |

This reflects a human-scale constraint: one person has finite energy. A solo model can protect flexibility but still bottleneck throughput. Hiring can raise delivery capacity but also increase break-even pressure and management overhead. Contractor capacity can sit between those options, with better elasticity and more handoff risk. One solo-operator perspective also warns that importing industrial growth logic into one-person work can lead to exhaustion.

When contractors are part of capacity planning, protect quality with the same contract and acceptance discipline used for client work. Hand off clear scope, define review points, and keep one owner accountable for final delivery.

Run a monthly proof check before changing structure#

Before you change structure, run a monthly checkpoint and save the evidence in one dated file:

- Pipeline volatility by week, including delayed starts and canceled work.

- Delivery load versus available personal capacity.

- Margin after contractor spend for the same month.

- Rework or late-delivery incidents tied to capacity gaps.

- A one-page decision note with owner, decision date, and next review date.

If demand remains uneven, keep contractor capacity as the pressure valve. If demand stays stable across repeated reviews and work is becoming process-heavy, test a hiring plan with conservative assumptions. A frequent risk is hiring to solve a short spike, then carrying fixed cost when demand normalizes.

Review the last few decision notes before each structural change. If the same warning appears repeatedly and remains unresolved, fix that issue first instead of adding headcount. In a solo business, stronger growth decisions come from matching cost structure to operating evidence, not from copying headline trends.

Avoid the seven failure modes that sink durable solo businesses#

Most failures are avoidable when you catch them early and assign clear ownership. Use this as a monthly risk screen, not a one-time checklist.

Seven failure modes to catch early#

| Failure mode | Why it matters |

|---|---|

| Starting delivery before a signed MSA and SOW | Scope and payment disputes can be harder to unwind once work has started. |

| Treating Fiverr or Upwork cash flow as equal to direct contracted revenue quality | Channel volume can hide weak client quality. |

| Ignoring compliance until payout friction appears | Late remediation can create deadline pressure. |

| Letting tax and FBAR records drift across tools and inboxes | Missing ownership turns routine admin into cleanup mode. |

| Using CNBC or Forbes headlines as proof of demand in your niche | Market narrative is not the same as repeatable paid demand. |

| Handling FBAR account values loosely | For multiple accounts, each account must be valued separately, then converted and rounded correctly. |

| Applying special FBAR deadline relief to everyone | The April 15, 2027 extension applies only to certain people with signature authority and no financial interest. For other people with an FBAR obligation, the due date remains April 15, 2026. |

- Starting delivery before a signed MSA and SOW. Scope and payment disputes can be harder to unwind once work has started.

- Treating Fiverr or Upwork cash flow as equal to direct contracted revenue quality. Channel volume can hide weak client quality.

- Ignoring compliance until payout friction appears. Late remediation can create deadline pressure.

- Letting tax and FBAR records drift across tools and inboxes. Missing ownership turns routine admin into cleanup mode.

- Using CNBC or Forbes headlines as proof of demand in your niche. Market narrative is not the same as repeatable paid demand.

- Handling FBAR account values loosely. For multiple accounts, each account must be valued separately, then converted and rounded correctly.

- Applying special FBAR deadline relief to everyone. The April 15, 2027 extension applies only to certain people with signature authority and no financial interest. For other people with an FBAR obligation, the due date remains April 15, 2026.

Failure mode six is where small math habits create avoidable risk. FinCEN describes maximum account value as a reasonable approximation of the highest value during the calendar year. For foreign-currency accounts, convert with the Treasury Financial Management Service year-end rate, then report in U.S. dollars rounded up to the next whole dollar, for example $15,265.25 becomes $15,266.

When any failure mode appears, contain it before you optimize anything else:

- Stop creating new exceptions of the same type.

- Assign one owner and one dated next action.

- Capture the root cause and the template or rule change that prevents repeat errors.

Run one month-end checkpoint to contain these issues: contract status for active clients, revenue channel mix, unresolved compliance exceptions, and tax-document status in one dated record. If foreign accounts are in scope, add an FBAR worksheet and verify per-account valuation, conversion, and rounding before close. Related: Digital Nomad Health Insurance: A Comparison of Top Providers.

Use a monthly operator review to stay compliant and bankable#

Run one fixed monthly review on a single cutoff date, then make a clear continue-or-pause decision using criteria you define internally.

Use three packets so open issues are easy to scan:

- Financial packet: booked revenue, receivables aging, cash timing, and unresolved payout exceptions.

- Compliance packet: open verification actions, pending tax-validation checks, and missing client or vendor tax forms.

- Contract packet: renewals, expiring master-agreement terms, change-order count, and repeat scope-dispute patterns.

Build the packets before the meeting, not during it. If data is still being assembled while decisions are being made, unresolved items can drift into the next cycle.

For every open item, assign one owner and one dated next step before you close the review. If exceptions are rising, consider pausing new acquisition experiments until control gaps are addressed.

If an external reference for this topic is unavailable, use your own dated monthly records as the decision source.

Keep prior-month carryover visible. A short list of unresolved items from the last review makes trend direction clearer and prevents repeated discussion without resolution.

Execute a 30-60-90 day buildout with concrete deliverables#

Run this as a gated 30-60-90 plan, not a calendar checklist. Move forward only when work is documented, owned, and measurable under real conditions.

Treat the first 30 days as listening and learning. Use the rest of the 90 days to apply standards and test whether the setup holds up in live work.

Phase gates#

| Phase | Build focus | Verify before moving on | Common failure signal |

|---|---|---|---|

| Days 1-30 | Listen, learn, and map how work actually moves end to end. Define your operating standards and owners. | You can pull dated records for each key step without guesswork. | You start optimizing before the baseline process is clear. |

| Days 31-60 | Run the standards in live work and log exceptions in a consistent format. | You can trace work items end to end and show who owns each open issue. | Exceptions pile up, but ownership and next actions stay unclear. |

| Days 61-90 | Complete the 3-month test and decide what to keep, tighten, or pause. | You can show trend lines for completion, exceptions, and lag, then make a clear keep-or-change decision. | New work is added before unresolved gaps are closed. |

Treat the full period as a 3-month test, not a guaranteed outcome. The point is measurement discipline: if you cannot measure completion, exception volume, and lag, you cannot manage them.

If a gate is not met, extend the phase and fix the gap before moving ahead. Advancing on schedule with unresolved gaps can create the same rework later at a larger scale.

End-of-quarter output#

Produce one operating binder with your current standards, dated evidence logs, process records, and an unresolved-risk list with owners and next steps. Add a short decision memo on what changed, what is still failing, and what is paused next quarter.

Keep the binder useful for future review. Use clear version dates, keep one source of truth for each checklist, and archive replaced versions so past decisions remain auditable.

Build for durability not just momentum#

Durability should be the default, not momentum. Trend stories can signal direction, but they are not your operating approach.

For a solo company, disciplined execution is the stronger posture: motivation helps you start, but it does not reliably carry the work. The pattern throughout this guide is the same: discipline, time management, and independent follow-through matter more than momentum.

That is why your systems and review cadence matter. They are not guarantees, and they are not a substitute for legal or tax advice. They are practical controls that keep decisions visible, repeatable, and easier to audit before you expand.

Evidence discipline is part of the same approach. If a claim cannot be retrieved or verified, do not treat it as planning input.

Use this next-step sequence to keep growth options open while reducing avoidable surprises:

- Complete the 30-60-90 checklist and document progress with dated evidence.

- Run one monthly review packet cycle so decisions are documented, not carried in memory.

- Re-check key assumptions and evidence before expanding.

If you want a deeper dive, read GDPR for Freelancers: A Step-by-Step Compliance Checklist for EU Clients, or, to confirm what is supported for your specific country or program, Talk to Gruv.

Frequently Asked Questions

What is the difference between a solopreneur and a freelancer in day-to-day operations?

Freelancing is generally working without a long-term commitment to one employer, often by providing specialized services. A solopreneur runs the business as a whole. Day to day, that can mean client delivery plus business operations, not delivery alone. If your calendar is mostly project execution, you are operating closer to freelancing. If your time is split between delivery and running operations, you are operating more like a business-of-one.

How reliable are current solopreneur economy statistics from the U.S. Census Bureau and SBA for planning my own business?

Use broad statistics as context, not as a direct forecast for your next quarter. In this section, those specific datasets are not provided, so validate the original source and method before relying on them. Separate reported data from contributor analysis, then make final decisions from your own operating results. A practical rule is simple: let public statistics shape questions, then let your own conversion rates, delivery capacity, and cash timing shape commitments.

Can I build a durable business-of-one without hiring employees?

It can be possible to build a durable business-of-one. Common pressure points include isolation, financial instability, and time management. Durability usually depends on how early and consistently you manage those risks. A practical approach is to separate growth effort from control effort each month. Keep one block for pipeline and one block for operations and reconciliation, so one side does not erase the other.

When do I need KYC, KYB, and AML checks as an independent professional?

This section does not provide legal trigger points for KYC, KYB, or AML checks. Requirements can vary by jurisdiction and provider, so confirm obligations with the relevant platform, payment partner, or advisor. Plan for verification early so onboarding does not stall operations. When uncertain, decide your internal sequence first and document exceptions. That keeps reviews consistent while you confirm exact obligations.

Which tax documents should I collect first for U.S. and cross-border clients?

This section does not include a country-by-country tax document list. Start with what your payer, client, and jurisdiction require, ideally before first payment, and collect it during onboarding. If anything is unclear, confirm before invoicing. Keep status visible in the same client record you use for approval so payout decisions and tax documentation stay aligned.

How do I decide between platform work, direct contracts, and Merchant of Record support?

There is no single rule in this section that makes one route best for everyone. Pick one primary route per offer, run it for a defined period, and track friction, exceptions, and payment flow. Keep what performs reliably, then adjust with evidence. Try not to change channels at the same time you change pricing or scope. Isolate one variable so you can see what actually improved.

What signals tell me to keep operating solo versus adding contractors or employees?

Stay solo when workload and quality remain stable without chronic strain. Repeated isolation, financial instability, or time-management breakdowns can signal that the current setup is under pressure. Make expansion decisions from trends over time, not one stressful week. If pressure looks temporary, contractor support can be a lower-commitment first response. If pressure repeats across multiple review cycles with stable demand, a hiring test may make sense.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaefiling.fincen.gov/docs/XMLUserGuide_FinCENFBAR.pdftrusted

- entrepreneurship.asu.edu/blog/2025/07/09/the-gig-economy-your-path-as...trusted

- fincen.gov/system/files/2025-12/FBAR-FBAR-Filing-Requir...trusted

- irs.gov/instructions/i2555trusted

- irs.gov/individuals/international-taxpayers/figuring...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

GDPR Compliance Checklist for Freelancers Working With EU Clients

Start by separating the decisions you are actually making. For a workable **GDPR setup**, run three distinct tracks and record each one in writing before the first invoice goes out: VAT treatment, GDPR scope and role, and daily privacy operations.

Digital Nomad Health Insurance Comparison for Long-Stay Moves

Use focused time now to avoid expensive mistakes later. Start with a practical `digital nomad health insurance comparison`, then map your route in [Gruv's visa planner](/tools/visa-for-digital-nomads) so we anchor policy checks to your real plan before pricing pages pull you off course.

The Best Project Management Tools for Freelance Developers

Freelance delivery gets more predictable when planning and client updates follow one clear setup instead of improvised tickets and scattered chat threads. In practice, project management for developers means planning, scheduling, and organizing software work so scope, time, quality, and stakeholder expectations stay aligned.