Quick Answer

Yes - start a solo 401k crypto plan only after an eligibility screen confirms self-employment status and no disqualifying employee facts. Then create the IRS-compliant plan document, assign trustee authority, and open a checking account titled to the plan before moving money. Treat provider claims as unverified until rails, fees, and custody limits are confirmed in writing. Keep transaction records from the first order because IRS Notice 2014-21 treats virtual currency as property.

Start Here and Build This in the Right Order#

Set up your solo 401k crypto plan as a sequence, not a product search. Build plan structure first, verify provider claims in writing, then fund and transact.

Provider support is uneven. Support can vary by provider and platform. Treat marketing claims as unproven until you have written confirmation of what is supported and how it is administered.

Start with the setup steps that create a clean paper trail#

Use this baseline order before any funding or purchases, and confirm exact steps with your provider:

- Confirm you fit the Solo 401(k) profile for self-employed owners with no full-time employees.

- Set up an IRS-compliant Solo 401(k) plan document.

- Assign trustee responsibility clearly, since you manage assets on behalf of the plan.

- Open a dedicated checking account in the Solo 401(k) name, then move funds through that account.

Keep plan documents, trustee designation, and account naming aligned so ownership and activity are easy to trace.

Keep scope tight to U.S. tax treatment and execution#

This article is U.S.-oriented. The core tax anchor is that the IRS treats virtual currency as property, so recordkeeping and transaction controls should be in place from day one.

Policy posture can shift without removing your execution duties. In 2025, the Department of Labor moved to a neutral posture on crypto in retirement plans and withdrew earlier caution. Neutrality does not require every plan sponsor to offer crypto, and it does not replace account-level verification.

If your obligations are not fully U.S.-only, confirm cross-border implications before opening accounts.

Use provider names as comparison inputs, not trust signals#

You will see provider names in market comparisons. This is not a promotion of any one provider. Use these names as inputs, request written confirmations, and keep records that can survive review.

What a Solo 401(k) Crypto Setup Actually Is#

A solo 401k crypto setup is generally a self-directed Solo 401(k) arrangement where the retirement plan, not you personally, holds the crypto assets.

A Solo 401(k) is a retirement plan for self-employed individuals and small business owners. A Self-Directed Solo 401(k) can be used when you want crypto exposure. If you are not eligible for a Solo 401(k), a Self-Directed IRA can also hold crypto. It is a different account model and should not be treated as interchangeable.

The key boundary is ownership and benefit. The plan owns the assets. Prohibited transaction rules are designed so neither the participant nor the retirement account benefits from the other in ways the rules do not allow. For transaction review, this is where disqualified person risk under IRC Section 4975(e)(2) matters.

In practice, crypto exposure here means plan-owned positions in assets like Bitcoin and Ethereum inside the retirement account structure. For U.S. federal tax treatment, IRS Notice 2014-21 says virtual currency is treated as property, and general property-transaction principles apply.

| Option | Best fit | Key distinction |

|---|---|---|

| Self-Directed Solo 401(k) | Eligible self-employed owner | Crypto exposure can be added within a Solo 401(k) structure |

| Self-Directed IRA | Not eligible for Solo 401(k) | Can hold crypto, but governance differs from Solo 401(k) |

Want a quick next step for solo 401k crypto? Try the free invoice generator.

Run the Eligibility Screen Before You Compare Providers#

Run eligibility first. If your facts do not support a Solo 401(k), provider comparisons are a distraction.

| Worksheet item | What to capture |

|---|---|

| Business activity notes | Records tied to your self-employment |

| Workforce snapshot | Who is working in the business and whether any non-spouse employee exists |

| Owner or spouse role map | Who works in the business and who is compensated |

| Open questions | Any assumptions you still need confirmed |

A Solo 401(k), also called a one-participant 401(k), is for someone who is self-employed or owns a business with no employees other than a spouse. If you are not clearly self-employed, pause setup and validate eligibility before you spend on provider onboarding.

Use a one-page eligibility worksheet before provider calls:

- Business activity notes: records tied to your self-employment.

- Workforce snapshot: who is working in the business and whether any non-spouse employee exists.

- Owner or spouse role map: who works in the business and who is compensated.

- Open questions: any assumptions you still need confirmed.

Share that worksheet with the provider or plan administrator and consider asking for written confirmation that your facts match the account type you plan to open. Treat this as a control step before opening a Solo 401(k). If the worksheet does not clearly support eligibility, stop and resolve that before comparing features.

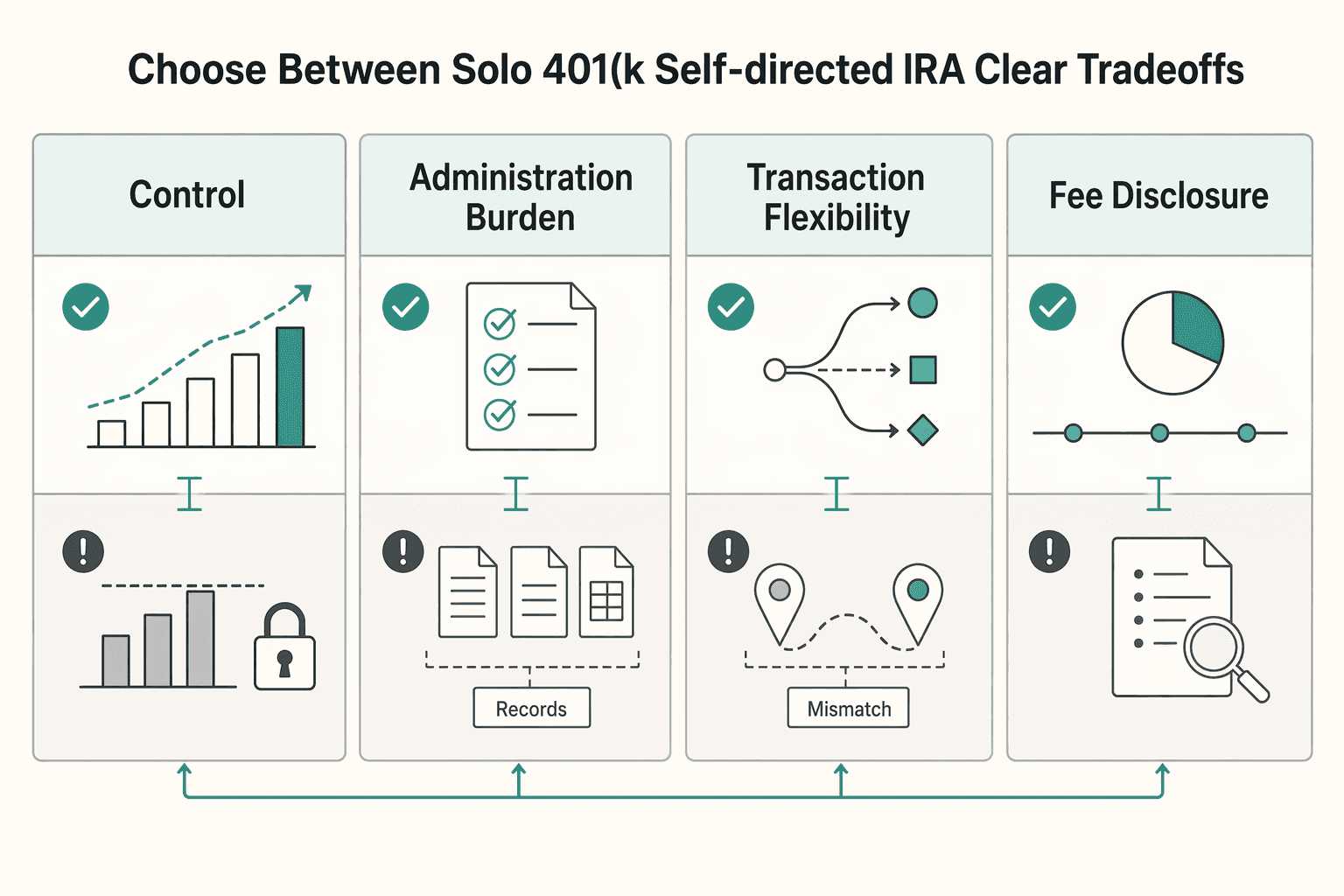

Choose Between Solo 401(k) and Self-Directed IRA with Clear Tradeoffs#

Choose on operating fit, not branding. The real decision is how much control you want and how much oversight work you can handle consistently.

The core tradeoff is control versus responsibility. In participant-directed 401(k) structures, you carry more of the portfolio decision load. Wider investment choice can help, but it can also raise risk when records, approvals, and periodic reviews are weak.

| Decision factor | Solo 401(k) | Self-Directed IRA |

|---|---|---|

| Control model | Confirm where you direct investments and where provider approval still applies. | Confirm which decisions are custodian-led versus investor-led in your setup. |

| Administration burden | Confirm what you must track once options expand. | Confirm what admin tasks are handled for you versus left to you. |

| Transaction flexibility | Validate channels and limits before assuming broad access. | Validate processing steps and limits before assuming simplicity. |

| Fee and disclosure clarity | Request written disclosure of window features and any individual-level fees, where applicable. | Request a complete written fee schedule, including transaction-related charges. |

Use a practical decision rule. Map each option's written terms to your control preference and administration capacity. Neither is a default winner until written terms show how it works in your case.

Before you choose, run one verification checkpoint:

- Ask for written disclosure of any individual-level fees.

- Ask who executes each transaction step and who signs off.

- Ask whether any brokerage window or similar feature changes available options, disclosures, or fees.

- Ask for a plain-language summary of what is included versus billed separately.

Keep tax questions separate from structure mechanics. Confirm control, administration, and fee disclosures first, then make tax elections based on your specific situation.

If key facts are missing, wait. Pause when income is volatile, staffing plans may change, or contribution behavior is still unclear, then rerun the comparison with written terms.

Related: Using a Data Processing Agreement (DPA) with Subcontractors.

Understand Tax Treatment Before You Place the First Trade#

Before the first trade, treat crypto activity in a Solo 401(k) as property-based reporting work, not simple cash movement. In the guidance used here, crypto is treated as property, so compliance posture and records should be set before trading starts.

| Time | Reporting point | Article detail |

|---|---|---|

| January 1, 2025 | 1099-DA start | Brokers are described as required to issue 1099-DA for applicable digital asset sales and exchanges starting on this date |

| Early 2026 | 2025 broker sales reporting | 2025 broker sales are described as reported in early 2026 |

| January 1, 2026 | Cost basis addition | Brokers are described as adding cost basis for crypto purchased on-platform starting on this date |

| Early 2027 | Updated reporting | Updated reporting is described as distributed in early 2027 |

Property treatment makes complete transaction records important from day one. Keep core details, including dates, quantities, proceeds, fees, and basis information when available, aligned with plan records so you are not reconciling gaps under filing pressure.

Form 1099-DA creates a practical reporting timeline. Brokers are described as required to issue 1099-DA starting January 1, 2025 for applicable digital asset sales and exchanges, and 2025 broker sales are described as reported in early 2026. From January 1, 2026, brokers are described as adding cost basis for crypto purchased on-platform. Updated reporting is described as distributed in early 2027.

Before first trade, run this checkpoint:

- Build and use a transaction-level record process before placing orders.

- Add 1099-DA timing to your reporting calendar for the trade year.

- Capture transfer details when assets move between venues so basis context is not lost.

- Reconcile your records against broker reporting on a regular schedule.

A practical risk is assuming transfer history carries over cleanly across platforms. When basis details are missing on transferred crypto, brokers may apply FIFO from the transfer date, which can produce results that differ from internal assumptions.

Caveat box for staking and edge cases#

Staking, advanced structures, and mixed-venue activity are where thin summaries usually fail. The guidance used for this draft describes staking reward treatment as detailed and warns that incorrect handling can create liability. If your plan includes staking or more complex transaction paths, get case-specific tax review before execution.

Escalate for case-specific review when:

- You cannot map a complete basis trail after transfers.

- Your approach includes staking or other advanced features with unclear treatment.

- Broker forms and your internal records are already inconsistent.

If you want a deeper dive, read Japan Digital Nomad Visa: A Guide to the New 2025 Program.

Pick a Provider Using Evidence, Not Marketing Claims#

Pick a provider only after written evidence confirms operations, cost, and compliance support. This is a documentation test, not a branding decision.

That standard matters. In its November 2024 report, GAO said available industry data and stakeholder interviews suggest crypto assets are a small part of the 401(k) market, while total 401(k) savings were more than $6.7 trillion in 2022. GAO also noted that, as of October 2024, legislation had been introduced but no bill had become law, so treat policy discussion as evolving rather than a settled operating rule.

| Provider | Custody options to verify in writing | Supported rails to verify in writing | Fees to verify in writing | Admin support to verify in writing | Documentation depth to verify |

|---|---|---|---|---|---|

| Nabers Group | Account title, control model, and who can initiate moves | Whether centralized exchange, decentralized wallet, and over-the-counter (OTC) routes are supported, plus limits | One-time setup, recurring, transaction, and admin charges | Who handles setup, who reviews exceptions, and escalation contact | Sample onboarding packet, policy summaries, and change-notice format |

| Broad Financial | Account title, control model, and who can initiate moves | Whether centralized exchange, decentralized wallet, and over-the-counter (OTC) routes are supported, plus limits | One-time setup, recurring, transaction, and admin charges | Who handles setup, who reviews exceptions, and escalation contact | Sample onboarding packet, policy summaries, and change-notice format |

| Carry | Account title, control model, and who can initiate moves | Whether centralized exchange, decentralized wallet, and over-the-counter (OTC) routes are supported, plus limits | One-time setup, recurring, transaction, and admin charges | Who handles setup, who reviews exceptions, and escalation contact | Sample onboarding packet, policy summaries, and change-notice format |

| IRA Financial | Account title, control model, and who can initiate moves | Whether centralized exchange, decentralized wallet, and over-the-counter (OTC) routes are supported, plus limits | One-time setup, recurring, transaction, and admin charges | Who handles setup, who reviews exceptions, and escalation contact | Sample onboarding packet, policy summaries, and change-notice format |

Before opening an account, require one evidence pack per provider:

- Written confirmation of rail support and any restrictions on exchange, wallet, or OTC usage.

- A dated fee schedule that includes every charge category, not just headline pricing.

- A plain-language compliance note covering approvals, records, and exception handling.

- A statement clarifying whether referenced tax guidance is draft or final, since IRS draft forms are not for filing and drafts may change before final release.

Apply one red-flag rule: if a provider promises broad asset access but will not provide compliance process detail in writing, treat it as higher operational risk. Do the same when costs are partial or unclear. If you cannot calculate first-year total cost from written documentation, you do not have enough evidence to choose.

Execute Setup in Sequence So You Do Not Create Fix-Later Problems#

A prudent move is to document your setup before money moves, so authority, ownership context, and records stay aligned from day one. Treat this as an internal control, not a universal legal mandate.

A practical workflow can include plan records, trustee responsibility documentation, account opening, and then documented funding and transactions. The exact order can vary, but your file should show who acted, in what role, and for the plan context rather than personal activity.

DOL updates effective September 23, 2024 define when a person is giving investment advice for compensation and apply to Code plans, including IRAs, alongside amendments tied to prohibited transaction exemptions. If compensation, advice, and control are unclear in records, prohibited-transaction risk can increase.

Execution checklist artifact#

Keep one setup packet before the first trade and use it as your standing evidence file. A practical packet can include:

- Plan setup records with dates.

- Trustee role and authority records.

- Account-opening confirmations showing plan-context ownership and control.

- Signature or approval records for key setup actions.

- First-funding proof: source, date, amount, and receiving account confirmation.

- Storage and access notes showing where assets are held and how authorized access works.

Before funding, run one control check: account paperwork, authorized actor, and funding trail should all tell the same ownership and authority story. If records conflict, pause, correct in writing, and only then place the first trade.

Fund the Account Without Breaking Operating Cashflow#

Keep retirement funding separate from day-to-day invoice spending, then use a repeatable cadence instead of ad hoc transfers. This can make transfers easier to track before you place trades.

If revenue is uneven, choose a contribution rhythm you can sustain. Industry commentary often describes retirement contributions as set-it-and-forget-it, but treat that as a discipline cue, not autopilot. Recheck cadence against current business obligations and adjust contribution size as needed.

Before the first crypto purchase, consider keeping one funding-source file so each transfer is traceable. Example fields include:

- Rollover records: prior account details, transfer instructions, receiving-account confirmation, and dates.

- New contribution log: amount, transfer date, and source account.

- Internal authorization notes, where applicable: who approved funding and in what role.

- Pre-trade check: funding ledger and provider cash balance align before placing orders.

- Exception log: reversals, corrections, or timing delays documented clearly.

Keep funding records aligned with your contribution categories. If you use more than one funding type, track inflows in separate lines so classifications stay consistent over time.

Buy and Hold Crypto with Explicit Custody Rules#

Set custody rules before the first trade. Pick an execution path, define who can authorize asset movement, and keep records for every position change that can be verified later.

Treat permissions as provider-specific and subject to change. A U.S. executive order released on August 7, 2025 described broader access to alternative investments, including digital assets, in ERISA-governed plans. It was explicitly not self-executing and called for Department of Labor clarification within 180 days. Use that as policy direction, not automatic approval for any specific execution rail.

| Potential execution path | Practical upside | Main tradeoff | What to confirm before first buy |

|---|---|---|---|

| Centralized exchange | Can simplify order flow and account management | Custody and withdrawal behavior may be platform-controlled | Current plan-account asset access and withdrawal or transfer behavior in writing |

| Decentralized wallet | Can provide direct control over wallet keys and on-chain movement | Higher key-management burden and greater access-error risk | Documented key ownership, backup handling, and approval roles before funding |

| OTC provider | Can provide a structured workflow for negotiated execution | More onboarding, settlement coordination, and documentation | Execution steps, settlement records, and approval authority for each instruction |

If you choose a cold storage hardware wallet, document key governance before moving funds. Record who initializes the wallet, where backups are held, who approves outgoing transfers, and how access is recovered if a signer is unavailable.

Use the same checkpoints for each crypto position change:

- Pre-trade approval: date, account, asset, order type, and authorized signer.

- Post-trade confirmation: same-day execution evidence and filled quantity.

- Ledger reconciliation: periodic tie-out between order records and account statement movement.

- Exception log: canceled orders, partial fills, failed transfers, and corrections.

Expect operational constraints even when marketing language sounds broad. Asset availability and withdrawal behavior may not match promotional language, and whether crypto assets are securities remains contested in legal commentary. If provider policy changes mid-cycle, pause new buys, log the notice, and update your custody decision before resuming.

Avoid the Mistakes That Trigger Compliance and Audit Pain#

Compliance and audit pain usually starts when records cannot prove who made each decision and how it was approved. Keep ownership and control boundaries explicit in documents and platform logs so each transfer, trade, and approval is traceable.

Boundary problems are easier to prevent than unwind later. If wallet access, notes, or transaction history make asset ownership or control unclear, you create avoidable exposure.

Common errors usually appear in three places:

- Weak ownership documentation: account titles, signer records, and wallet-control notes do not clearly match the legal owner.

- Missing transaction trail: pre-trade approvals, execution confirmations, and statement tie-outs are incomplete or scattered.

- Casual handling of compliance rules: decisions are made informally, with little written rationale, then cleaned up only after a provider flags a problem.

Reporting pressure makes these gaps more expensive. For certain 2025 sales or exchanges on centralized exchanges, Form 1099-DA is described as starting in early 2026. Some centralized brokers are described as potentially issuing on a later timeline into early 2027. Mismatched or missing reporting can trigger IRS notices such as CP2000, so if your internal ledger cannot explain what a form reports, contemporaneous documentation is stronger than reconstruction from memory.

Use a short internal incident-response checklist when a control breaks; treat it as an operations baseline, not a complete legal notification map:

- Preserve evidence first: freeze edits to affected ledger entries, export account activity, save trade confirmations, and capture who had access at the time.

- Notify role owners: administrator or recordkeeper, custody provider, and tax preparer.

- Remediate in order: stop affected transactions, reconcile ownership and transaction history, then document corrections with dates and approver names.

- Track unresolved items: note pending provider items and your decision point for resuming activity.

If ownership proof and transaction proof disagree, pause activity until they match. Keep advisors and counsel involved for case-specific obligations. Clean evidence now is cheaper than fixing problems under audit pressure.

Keep an Evidence Pack That Survives Scrutiny#

Keep one evidence pack that proves ownership, approvals, and reporting logic without rebuilding history later. Consistent records turn audits, advisor questions, and filing reviews into a clean tie-out instead of a reconstruction exercise.

| Evidence item | What to keep |

|---|---|

| Plan documents | Executed plan paperwork, signer or trustee authorizations, and amendments |

| Account statements | Monthly statements for each plan-related account |

| Funding records | Contribution and rollover support, plus transfer confirmations |

| Trade confirmations | Order details and execution records for each transaction |

| Custody logs | Where assets are held, who has access, and any permission changes |

| Policy notes | Short decision memos, exceptions, and rationale |

Use a fixed minimum pack every month so gaps are obvious:

- Plan documents: executed plan paperwork, signer or trustee authorizations, and amendments.

- Account statements: monthly statements for each plan-related account.

- Funding records: contribution and rollover support, plus transfer confirmations.

- Trade confirmations: order details and execution records for each transaction.

- Custody logs: where assets are held, who has access, and any permission changes.

- Policy notes: short decision memos, exceptions, and rationale.

Keep a reporting watchlist in the same file. Form 8938 is used to report specified foreign financial assets above the applicable threshold and, when required, is attached to the annual income tax return. Thresholds vary by filer profile, and filing Form 8938 does not replace a separate FBAR filing (FinCEN Form 114) when FBAR is otherwise required. If no income tax return is required for the year, Form 8938 is not required for that year. Keep FBAR (FinCEN Form 114) and Form 8938 as checkpoints, and document why each did or did not apply.

Treat filer profile and entity structure as gating factors. Reporting obligations can differ by filing status, residency, entity type, and account setup, so confirm filing obligations with qualified tax and legal advisors before filing.

Run one monthly control routine and log completion:

- Reconcile statements, funding records, and trade confirmations, then resolve mismatches.

- Validate custody status, including current asset location and transfer authority.

- Review watchlist checkpoints against current account facts.

- Update the exception log with corrections, pending items, owners, and deadlines.

If you cannot trace an entry from source document to filed position in one pass, pause and fix the record before the next trade cycle. If custody access controls still feel unclear, run a personal security audit before scaling activity.

Take the Next Step with a Risk-First Setup Checklist#

Treat the next move as a sequence decision, not a provider popularity contest: confirm fit, choose structure, verify claims in writing, complete setup in order, then trade with controls. When guidance differs across providers, rely on documented confirmations tied to your account terms.

A Solo 401(k) is plan-owned, not personally owned, and the trustee manages assets on behalf of the plan. Keep that boundary explicit in account titling, funding, and transaction records.

- Confirm eligibility first.

Use eligibility as a hard gate before fees or account opening. Provider materials describe a no full-time W-2 employee limit with a spouse exception; if your case is unclear, pause and get written confirmation.

- Choose plan structure before feature comparisons.

Document which plan/account structure you are using and why, based on written plan and provider documents. Keep tax treatment assumptions explicit in records: in this context, crypto is treated as property, which raises recordkeeping discipline from day one.

- Verify provider claims with evidence, not sales copy.

Get written confirmation of supported execution rails, fee schedules, and reporting support. If one provider lists specific setup or annual fees, treat those as provider-specific terms, not a market benchmark.

- Execute setup in the correct order.

Set up the plan with an IRS-compliant plan document, assign trustee responsibility, then open a dedicated checking account in the Solo 401(k) name. Fund through documented paths such as rollovers or new contributions only after ownership details match plan records.

- Trade only after controls are documented.

Before the first trade, define who approves transactions, where proof is stored, and how tax reporting, prohibited-transaction risk, and security responsibilities are handled. Use extra caution with staking-related activity, since tax handling mistakes can create liabilities.

Before moving funds, complete a one-page decision sheet and store it in your evidence pack:

- Solo 401(k) type selected and who approved the decision.

- Execution rail selected for initial activity (for example, exchange, wallet, or OTC provider) and what you rejected.

- Evidence-pack owner and storage location for plan documents, account confirmations, funding proof, and trade records.

If business cashflow records are still messy, evaluate money-movement tools that provide clear audit trails and status visibility so retirement funding decisions stay separate from operating cash.

Frequently Asked Questions

Who qualifies for a Solo 401(k) if I’m self-employed and have a spouse helping in the business?

This evidence pack does not define Solo 401(k) eligibility or spouse participation rules. Treat eligibility as a gating check and get classification documented in writing by your plan administrator and tax advisor before opening or funding the plan.

Is crypto treated as currency or property inside a Crypto Solo 401(k) under IRS rules?

This section’s grounding does not establish that tax characterization rule. Use the IRS treatment your return relies on, and keep labels consistent across records and filings.

What is the practical difference between a Self-Directed Solo 401(k) and a Self-Directed IRA for crypto?

Make the decision from written plan and provider documents that match how you intend to hold assets and handle reporting.

Can I buy any coin I want, or do provider and platform limits still apply?

Confirm supported assets, transfer behavior, and restrictions in writing before funding or trading.

What are the biggest compliance mistakes that can jeopardize account integrity?

A common mistake is treating Form 8938 and FBAR as interchangeable when they are not. Another is assuming Form 8938 works the same for everyone, even though thresholds can vary and some accounts are excluded.

What should I verify before trusting provider claims on fees, custody, and operational support?

This section does not validate provider-specific claims for you. Require current terms in writing, keep those records in your evidence pack, and confirm what reporting support is included before relying on marketing language.

Do cross-border tax and disclosure rules like FBAR or Form 8938 apply to my situation?

They can apply, but not universally. Form 8938 applies to specified persons who meet the applicable threshold for specified foreign financial assets, and thresholds can be higher for joint filers or taxpayers abroad. Filing Form 8938 does not replace a separate FBAR filing when FBAR is otherwise required, and some accounts are excluded from Form 8938 reporting.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- irs.gov/businesses/corporations/basic-questions-and-...trusted

- irs.gov/pub/irs-access/p4012_accessible.pdftrusted

- sec.gov/newsroom/speeches-statements/uyeda-remarks-d...trusted

- taxpayeradvocate.irs.gov/wp-content/uploads/2024/12/ARC24_MSP.pdftrusted

- solo401k.com/blog/solo-401k-crypto-staking-strategyexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Japan Digital Nomad Visa 2026: Six-Month Planning Runbook

Treat this as your operating model: identify the right mission first, commit to one route, and keep dated records before you make irreversible plans. That is what keeps the rest of your timeline, paperwork, and decisions coherent.

Using a Data Processing Agreement with Subcontractors

Put your data processing agreement in place before a processor or sub-processor gets access to personal data. If you use a processor, UK GDPR guidance requires a [written contract or other legal act](https://ico.org.uk/for-organisations/uk-gdpr-guidance-and-resources/accountability-and-governance/contracts-and-liabilities-between-controllers-and-processors-multi/when-is-a-contract-needed-and-why-is-it-important). Set that contract boundary before support logins, shared folders, or troubleshooting access turn into live processing.

How to Conduct a Personal Security Audit as a Freelancer

A freelancer-grade personal security audit should end with a ranked action plan, not more anxiety. In one focused pass, you should spot the highest-risk gaps, decide what can wait, and leave with fixes you can start this week.