Quick Answer

Start with three checks for singapore corporate tax: confirm your setup is treated as a company, map the correct Year of Assessment to its basis period, and align ACRA/BizFile+ records before filing. Then prepare Estimated Chargeable Income and the correct return path (Form C-S, Form C-S (Lite), or Form C). The core warning is practical: teams that confuse YA with the earning year often create late filings and weak evidence trails.

How Singapore Corporate Tax Filing Works#

Delays often come from mismatches between entity records, tax timing, and filing prep, not just the 17% rate. Start in this order: confirm whether your setup is treated as a company for income tax, map the correct Year of Assessment (YA), then verify core records before estimating anything.

In Singapore, Corporate Income Tax is assessed on a preceding year basis at a flat 17% of chargeable income. YA is the year income is assessed to tax, and the basis period is generally the 12 months before that YA. If your team tracks only the current year, you can end up planning against the wrong assessment year.

Use this anchor: income earned in financial year 2024 is assessed in YA 2025. Treat YA as an assessment label, not the year revenue was earned, so your books, planning, and tax prep stay aligned.

Entity classification is the next gate. For income tax purposes, company treatment covers Companies Act entities and foreign companies, but not sole-proprietorships or partnerships. If your structure is not treated as a company, do not apply company rules by default.

Before building filing calendars, run this checkpoint and keep evidence:

- Confirm ACRA entity particulars match internal legal and finance records.

- Confirm the financial year end is correct in BizFile+.

- If the financial year end changed, file the change with ACRA via BizFile+.

- Reconcile your basis period to the YA used in working papers.

IRAS updates its records from ACRA filings. If records are not updated in ACRA, your internal view may drift from what IRAS sees. Align records first, then move to filing steps and income classification.

Build the mental model before you touch filings#

Lock definitions and timing first, or everything downstream becomes harder to defend.

Corporate Income Tax is charged at 17% on chargeable income. YA is the year income is assessed to tax, and the basis period is the financial year used for that YA, usually a 12-month period. If these labels are inconsistent in your files, estimates and reviews become harder to reconcile.

Use this timing rule consistently: income from the preceding financial year is assessed in the current YA. Example: financial year 2024 maps to YA 2025. Keep YA separate from the year the work happened.

Next, separate legal form from tax obligations. For income tax, a company includes entities incorporated or registered under the Companies Act 1967 and foreign companies registered in Singapore, including branches. A sole-proprietorship or partnership is not treated as a company under these rules.

Before detailed computations, run one quick checkpoint:

- Match legal form in internal records to registration details.

- Confirm the chosen financial year end, since IRAS does not set it for companies.

- If the financial year end changed, file the update with ACRA through BizFile+.

- Confirm YA and basis period in your tax working paper match the latest ACRA-linked record.

This helps prevent a mismatch where your team prepares on one period while IRAS records reflect another. If the entity record, basis period, and YA do not align on one page, fix that before touching the forms.

Decide your entity path before you optimize tax#

Pick the entity path before you model tax outcomes. If local separation is a priority, a Singapore-incorporated company path may fit better. If you are extending an existing foreign entity, assess the branch path first.

This decision sets your filing baseline. Corporate tax filing applies to companies whether resident or non-resident. The headline rate is 17%, and assessment follows a preceding-year basis. Set structure and timing before preparing Estimated Chargeable Income (ECI).

| Path | What it means in practice | Practical signal | Better first fit |

|---|---|---|---|

| Singapore-incorporated company | Local incorporated company route in Singapore | Define filing ownership and timing early | You prefer an incorporated company path rather than a branch extension |

| Foreign branch | Extension of an existing foreign company in Singapore, not a separate legal entity | Parent company is fully liable for branch activities | You are extending an existing foreign entity |

Keep scope clean here: this comparison is for company paths only. If you are operating as a sole-proprietorship or partnership, do not reuse company filing assumptions without confirming the right treatment.

Before drafting ECI, run a quick verification:

- Confirm entity details match internal legal and finance records.

- Confirm the financial year end in your ECI working paper matches YA mapping.

- Confirm ownership for Form C, Form C-S, or Form C-S (Lite) preparation well before deadline pressure.

Timing errors compound quickly. ECI is filed within three months after financial year end unless exempt. Form C, Form C-S, or Form C-S (Lite) is filed by 30 November of the YA. If the entity path, period mapping, and records drift apart, corrections and deadline misses can trigger penalties, fines, or audits.

Map income streams the way IRAS will examine them#

Start by classifying each contract into two buckets: income accrued in or derived from Singapore, and foreign-sourced income received in Singapore. That split gives you a cleaner path for review, tax computation, and filing.

That is the working frame used here. Income accrued in or derived from Singapore is generally treated as company income. Foreign-sourced amounts received in Singapore need an extra exemption check. Some foreign-sourced dividends, branch profits, and service income may qualify for exemption, so do not treat every foreign receipt as automatically taxable or automatically exempt.

Use Section 13(12) as a verification trigger, not a shortcut. IRAS provides an e-Tax Guide on exemption under Section 13(12), including examples of how foreign income may be received in Singapore. Use it to review edge cases instead of relying on a single ledger label.

| What to document for each contract | Why it matters | Common failure mode |

|---|---|---|

| Where work was delivered operationally | Keeps records tied to how activity occurred | Team labels everything by client location only |

| Which entity billed the customer | Prevents cross-entity mixing in tax files | Revenue posted under the wrong entity |

| When and how cash was received in Singapore | Supports review of foreign-sourced inflows | Remittance timing is not documented |

Use these as documentation fields, not as standalone legal source-of-income tests.

Scenario contrast: a digital service contract is signed abroad, invoiced by your Singapore company, and delivered through Singapore operations. If you classify it on one fact alone, your file is weak. Document the full fact pattern before choosing treatment.

For withholding tax, keep the check narrow. This pack supports one concrete point: there is no withholding tax on dividends. Do not extend that dividend treatment to every cross-border payment type.

Before filing, run this checkpoint:

- Reconcile revenue totals to the two income buckets and document the mapping rule.

- Tag foreign-sourced receipts received in Singapore for focused review.

- Flag non-resident payment flows for withholding tax review instead of assuming one treatment.

- Escalate Section 13(12) edge cases instead of forcing a fast classification.

If one contract has mixed facts, document first and classify second. Quick assumptions here usually become slow corrections later. Related: The 'Compliance Moat': Why RegTech is a Defensible Strategy.

Pick the right exemption lane without wishful thinking#

Use a conservative base case. If Start-up Tax Exemption Scheme (SUTE) eligibility is not fully confirmed, model downside using Partial Tax Exemption (PTE) first.

Start from what is confirmed. Corporate Income Tax is 17% of chargeable income for local and foreign companies. IRAS also states that companies may receive rebates and exemption schemes, including for new start-up companies, so treat benefits as provisional until your facts match current IRAS wording.

| Eligibility checklist point | Partial Tax Exemption (PTE) | Start-up Tax Exemption Scheme (SUTE) |

|---|---|---|

| What this pack confirms | Exemption schemes exist | New start-up relief exists |

| What this pack does not confirm | Full thresholds and percentages are not provided here | Full eligibility criteria and explicit exclusions are not provided here |

| Safe planning stance | Use as default downside lane when facts are incomplete | Keep out of base-case budget until eligibility and exclusions are confirmed with IRAS |

Keep rebates, cash grants, and exemptions separate in your model. For YA 2026, IRAS states a 40% CIT Rebate for all taxpaying companies, with total benefits from the rebate plus the CIT Rebate Cash Grant capped at $30,000. A minimum benefit of $1,500 may be given in the form of a CIT Rebate Cash Grant for eligible companies that made CPF contributions to at least one local employee in calendar year 2025, with disbursement by the second quarter of 2026. Treat these as year-specific measures, not a permanent baseline.

Before you finalize the forecast, run this checkpoint with the Inland Revenue Authority of Singapore:

- Confirm current-year PTE and SUTE conditions on IRAS pages.

- Confirm whether company facts match published SUTE eligibility wording and exclusions.

- Keep any unconfirmed benefit out of the base case.

Build your annual filing sequence and stick to it#

Use one documented filing workflow with named owners and sign-off at each stage.

Set the order first, then apply it consistently. In IRAS guidance for Form IR21 e-filing, users must be authorised as either a Preparer or an Approver, with a clear draft-to-review-to-submission handoff.

| Workflow control | What to set first | Evidence to prepare | Red flag |

|---|---|---|---|

| Role authorisation | Confirm the filer is authorised as a Preparer or Approver | Access/authorisation confirmation | No one can confirm who is authorised to prepare vs submit |

| Review handoff | Preparer prepares and submits forms and documents to Approver for review | Draft package and review notes | Work stalls in draft with no approver action |

| Session discipline | Plan filing work so sessions are not left idle | Team checklist with active-session checkpoints | Session is left idle and expires |

| Submission confirmation | Treat saved drafts as temporary only | Submission acknowledgement and final status check | Team assumes a saved draft is already submitted |

Form distinctions matter. If controls are unclear, filing complexity turns into errors and missed deadlines.

Done means done only when owner, evidence, and sign-off are explicit for each stage:

- Role confirmed. Owner: filer. Evidence: authorisation as Preparer or Approver. Sign-off: correct role access is verified before work starts.

- Draft prepared and reviewed. Owner: preparer, then approver. Evidence: draft form and supporting documents routed for review. Sign-off: approver review is completed.

- Submission completed. Owner: approver. Evidence: final portal status and submission acknowledgement. Sign-off: status confirms submitted, not just saved.

Final control: treat saved drafts as unfinished. In IRAS e-filing guidance for Form IR21, drafts can be retained for 21 days and idle sessions can expire after 20 minutes. A saved draft is not a submission. Use that discipline and verify exact behavior in the portal you file through.

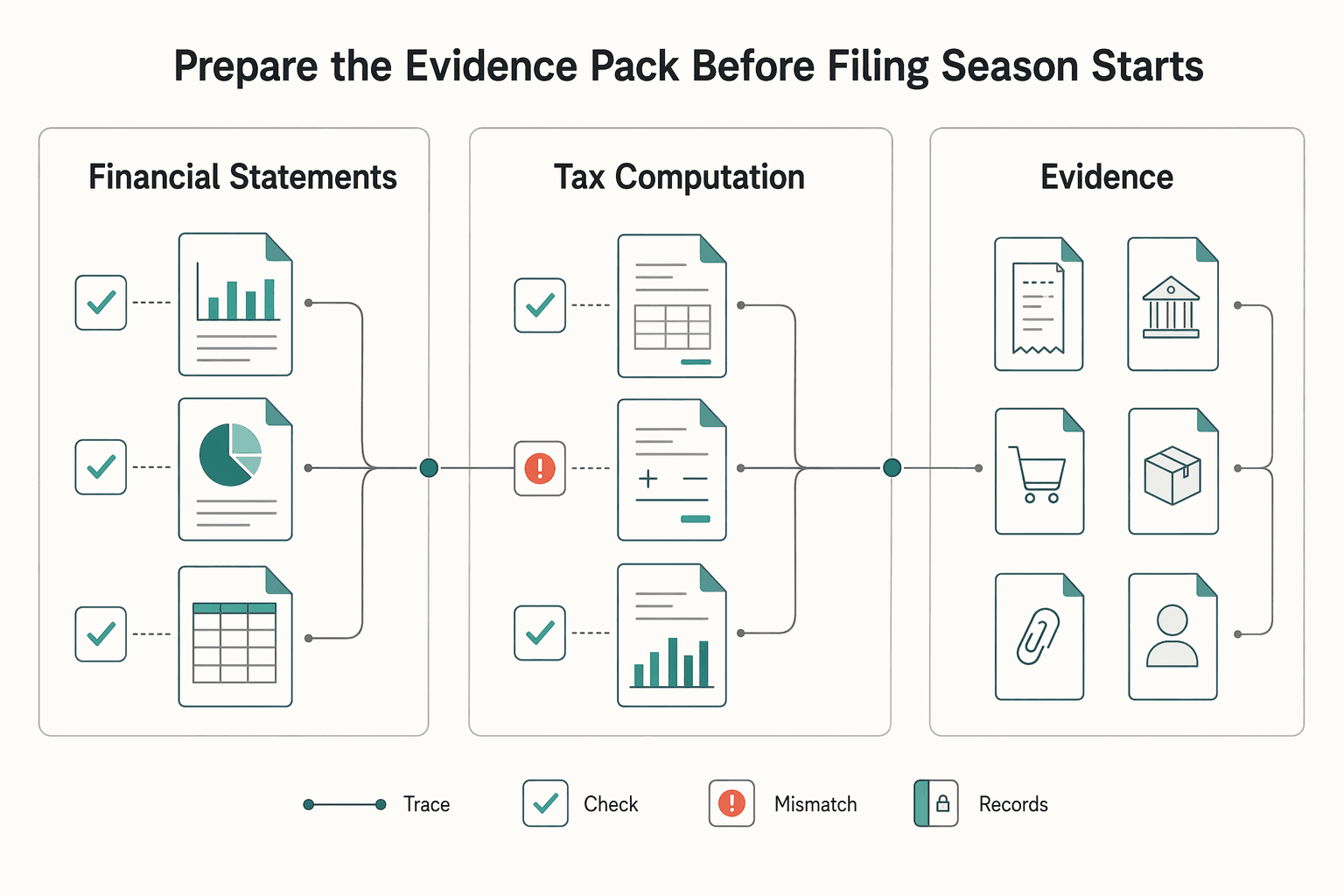

Prepare the evidence pack before filing season starts#

Prepare evidence before filing windows get crowded. Filing is faster and safer when every number can be traced from return figures to tax computation and underlying records.

| Item | Use in filing | Article note |

|---|---|---|

| Financial statements | Keep ready before completing Form C-S, Form C-S (Lite), or Form C | For the filing period |

| Tax computation | Prepare it for the return | Return figures should trace to a labeled tax computation line |

| Supporting documents | Needed to complete Form C-S, Form C-S (Lite), or Form C | Confirm the intended form path and required supporting documents |

| Source documents, accounting records, schedules, and bank statements | Let transactions be explained without rework | Keep the full pack for at least 5 years from the relevant Year of Assessment |

Before completing Form C-S, Form C-S (Lite), or Form C, keep financial statements, tax computation, and supporting documents ready. Store records in a systematic order so you can explain transactions tied to income, business expenses, and purchases without rework.

Use this minimum pack before filing:

- Financial statements for the filing period.

- Tax computation prepared for the return.

- Supporting documents needed to complete Form C-S, Form C-S (Lite), or Form C.

- Source documents, accounting records, schedules, and bank statements organized so transactions are easy to explain.

Run a consistency check across your filing records before drafting returns. This catches avoidable mismatches early.

Set a fixed pre-filing checkpoint:

- Confirm the intended form path and required supporting documents.

- Confirm whether annual revenue of $200,000 or below supports choosing Form C-S (Lite).

- Anchor the calendar to the 30 Nov filing deadline, and use the lead time from account close (at least 11 months) to close evidence gaps.

Use one internal rule: if a number cannot be traced to source records in two steps, it is not filing-ready.

- Step 1: trace from the return figure to a labeled tax computation line.

- Step 2: trace from that tax computation line to supporting documents and accounting records.

- If either step fails, hold the package and fix the trail first.

Keep the full pack, including source documents, accounting records, schedules, and bank statements, for at least 5 years from the relevant Year of Assessment.

Avoid the mistakes that trigger preventable pain#

Most preventable pain starts when teams file on assumptions instead of verified facts. Run a short red-flag check twice: before ECI and before annual filing.

| Red flag | What it looks like | Article action |

|---|---|---|

| Deadline trap | No named owner for ECI timing and the 30 November filing date | Pause filing and clear it first |

| Evidence trap | Unresolved numbers or weak backup for material figures | Pause filing and clear it first |

| Version trap | Teams are editing near deadline without one clear final file | Pause filing and clear it first |

| No-activity trap | Assuming no filing is needed when activity is zero | Treat the excerpt as a warning that returns may still be required |

| Small-error trap | Treating filing mistakes as harmless | Treat the excerpt as a warning they can trigger audits |

From the non-official excerpts in this pack, treat timing and penalty figures as risk signals only. ECI is listed as due within 3 months of financial year-end, and corporate tax filing is listed by 30 November. Missed filings are described with possible penalties in a $200 to $5,000 range, with some larger examples. Use this to set urgency, then confirm current requirements directly in official guidance before submission.

Use this red-flag screen before sign-off:

- Deadline trap: no named owner for ECI timing and the 30 November filing date.

- Evidence trap: unresolved numbers or weak backup for material figures.

- Version trap: teams are editing near deadline without one clear final file.

- No-activity trap: assuming no filing is needed when activity is zero; one excerpt in a GST context warns returns may still be required.

- Small-error trap: treating filing mistakes as harmless; one GST excerpt warns they can trigger audits.

If any red flag is open, pause filing and clear it first. That stop rule is usually cheaper than late corrections under deadline pressure.

Know when advanced regimes matter and when they do not#

For most founder-led businesses, advanced regimes belong on a watchlist, not in day-one tax design.

Group Relief and the Mergers and Acquisitions Scheme are usually more relevant once decisions involve related entities or real transaction activity. If you run one company with no near-term restructuring, they are often lower priority than core filing execution.

| Business profile | What matters now | What can wait |

|---|---|---|

| One entity, founder-led, no acquisition plan | Clean books and accurate, on-time core filings | Detailed design around Group Relief or the Mergers and Acquisitions Scheme |

| Multi-entity setup or active restructuring | Early review of group-level tax interactions and transaction structure | None, advanced review should start before commitments are signed |

| Cross-border group with expanding footprint | Monitor Pillar 2 timing from financial-year start dates and confirm scope | Assumption-based planning without documented scope checks |

The direction is clearer than it first looks. Singapore has affirmed implementation of the Income Inclusion Rule and Domestic Top-up Tax under Pillar 2 for financial years starting on or after 1 January 2025. It has reserved its position on the Undertaxed Profits Rule for now. Treat Pillar 2 and the Global Anti-Base Erosion Rules as context to monitor, not as a reason to redesign a small operation without a scope change.

Keep the Multinational Enterprise (Minimum Tax) Act 2024 in this same advanced bucket. Monitor it, then verify scope before acting.

Use one quarterly checkpoint note:

- Has the business moved from one entity to a group structure or started an acquisition path?

- Do financial years now begin in a period where Income Inclusion Rule or Domestic Top-up Tax timing could matter?

- Are planning decisions relying on assumptions about Undertaxed Profits Rule adoption that Singapore has not confirmed?

Set up compliance operations that scale with your business#

Clean compliance at scale comes from consistent monthly controls, not year-end scrambling.

Set a repeatable monthly cadence now: close books, reconcile key accounts, and assign clear preparer and approver ownership for filing inputs. These obligations can apply to Singapore-incorporated companies and foreign companies carrying on business in Singapore, and filing requirements can become more detailed as the business grows. Treat ACRA and IRAS obligations as ongoing tasks, not once-a-year events.

Build one monthly cycle that feeds filing season:

- Complete month-end close with locked exports and reviewer sign-off.

- Reconcile key accounts to source records and track exceptions to resolution.

- Keep dated approval logs for material tax classifications.

- Maintain a rolling file of ECI inputs, since ECI may need submission within three months after financial year-end.

- Track turnover so potential GST registration needs are visible as annual turnover approaches S$1 million.

| Control area | Minimum evidence to keep | Failure signal |

|---|---|---|

| Monthly close | Locked ledger export, period-end journal log, reviewer sign-off | Figures change after approval without documented reason |

| Reconciliation checkpoint | Reconciliations tied to source records, exception list, resolution notes | Material balances remain unresolved across closes |

| Filing input approvals | Named preparer and approver, dated approval log, final version marker | Multiple final files or unclear ownership |

| Tax classification history | Change log for key classifications and rationale | Team cannot explain treatment changes between periods |

Choose software for traceability, not convenience. Keep exportable period reports and clear links between ledger entries and supporting records. Maintain change history for classifications used in ECI and corporate income tax return preparation.

Run a formal quarterly verification: confirm current filing guidance for your return path, re-check that classifications still match business facts, and confirm records are review-ready. Record who checked what and when.

Confirm known unknowns before acting on any template#

A template is useful only after you list what is still unknown and verify it against current official material.

| Unknown | What the pack leaves open | What to verify |

|---|---|---|

| Full eligibility criteria | One of the three unknowns the excerpts still leave open | Confirm current Inland Revenue Authority of Singapore guidance for your filing path |

| Exact deadlines | One of the three unknowns the excerpts still leave open | Record the version status date on each primary page you rely on, plus the date you checked it |

| Step-by-step procedures for each filing path | One of the three unknowns the excerpts still leave open | Confirm the source is official first and save a compact evidence note |

From the excerpts, three unknowns still matter: full eligibility criteria, exact deadlines, and step-by-step procedures for each filing path. You do have clear evidence that published guidance changes over time. The Income Tax Act page shown is current as at 16 Mar 2026. The MAS Notice 626 guidelines excerpt shows a last revision date of 1 July 2025, and ACRA states its guidance may be amended.

Use this verification checklist before locking any position:

- Confirm the source is official first. Singapore government sites use .gov.sg, and non-government commentary should be treated as secondary until verified.

- Record the version status date on each primary page you rely on, plus the date you checked it.

- If guidance says it should be read in conjunction with a notice, read both together and note that relationship in your decision record.

- Confirm current Inland Revenue Authority of Singapore guidance for your filing path.

- Save a compact evidence note with page title, version date, copy or screenshot, reviewer name, and interpretation.

When wording is ambiguous, use conservative treatment and document why. Escalate for professional advice when entity structure is borderline, cross-border income classification is unclear, or exemption eligibility depends on close judgment calls.

Do not carry rules across tax regimes. For example, IRAS GST guidance mentions penalties up to 200% of tax owed and a correction window within one year from the GST F5 filing deadline. That is not a corporate income tax filing rule.

Conclusion#

Tax mistakes often come from sequence mistakes, not hidden rules. Decide entity status first, classify income next, then file in the right order with records another reviewer can follow quickly.

Start with scope. For income tax, a foreign company registered in Singapore, including a branch, is treated as a company, while sole proprietorships and partnerships are not. If status is unclear, stop and confirm it before modeling exemptions or rates.

Then lock the calculation frame. Corporate Income Tax is assessed on a preceding year basis, so basis period and Year of Assessment must align before preparing figures. The basis period is generally the 12 months before the YA, and tax is charged on chargeable income, not gross revenue. The headline rate is 17%, and final tax can depend on correct treatment of exemptions, rebates, and source of income.

A practical closeout check before filing:

- Confirm financial year end in ACRA records. Changes must be filed via BizFile+, and IRAS updates from ACRA filings.

- Prepare both annual return tracks: Estimated Chargeable Income and one of Form C-S, Form C-S (Lite), or Form C.

- Keep one evidence pack per YA with reconciliations, classification notes, and final submitted return version.

Treat cross-border income classification as a control point. A common summary is that Singapore-sourced income is taxed when it arises, while foreign-sourced income can be taxed when received in Singapore. Non-residents may also face withholding tax on certain payment types, so cash planning and documentation matter.

Treat exemptions and rebates as conditional, not automatic. Start-up relief is not universal, and some company types are excluded. For YA 2026, IRAS states a 40% corporate tax rebate, with benefit limits and conditions. Minimum tax rules under the MMT Act are effective for financial years starting on or after 1 January 2025, so monitor them as part of planning.

Use one pressure test: if a tax position cannot be traced to entity status, income classification, and filing evidence, it is not ready. Keep that discipline, and the work stays manageable instead of turning into recurring cleanup.

Frequently Asked Questions

What is Singapore corporate tax and how is **Corporate Income Tax** calculated in practice?

Corporate Income Tax is calculated on chargeable income, not on gross revenue. Chargeable income is taxable revenue after allowable expenses and allowances. One excerpt states a 17 percent headline rate on that base, with reliefs or exemptions potentially affecting the final amount. Use that as a working estimate and verify eligibility before filing.

What does flat 17% apply to, and what exactly counts as **chargeable income**?

The 17 percent headline figure applies to chargeable income. In the cited summary, chargeable income means taxable revenues after allowable expenses and other allowances. The same source states that the first SGD200,000 of chargeable income may receive full or partial exemption. Confirm eligibility before assuming that treatment.

How does the **Year of Assessment** differ from the financial year and **basis period**?

The basis period is the financial-year period used to assess tax in the following Year of Assessment. The cited summary states that income from the preceding financial year is assessed in the following Year of Assessment. Keep these labels separate so records map to the right tax cycle.

What do I need to file each year: **Estimated Chargeable Income**, **Form C-S**, **Form C-S (Lite)**, or **Form C**?

This pack does not provide official form selection criteria, procedural steps, or filing deadlines for each path. Confirm current IRAS requirements before filing, especially when facts are borderline.

How are foreign-sourced receipts treated, and when does **withholding tax** become relevant?

A common summary describes Singapore as a territorial tax approach where income accrued in or derived from Singapore and foreign-sourced income remitted to Singapore can be in scope. Withholding tax can become relevant in cross-border payment scenarios, especially where treaty relief is claimed. IRAS states that payers must submit a Certificate of Residence for lower or reduced treaty rates, and late COR submission can lead to additional withholding tax and late-payment penalties. In the cited IRAS FAQ, COR claim timing is by 31 Mar of the following year for current-year claims, or within three months from the withholding tax submission date for preceding-year claims.

What is the difference between the **Partial Tax Exemption Scheme** and **Start-up Tax Exemption Scheme**?

In non-government summaries, they are presented as separate exemption lanes with different eligibility conditions. One non-government FAQ says start-up exemption is limited to the first three years and not available to a foreign company or its Singapore branch, while another says the first SGD200,000 of chargeable income may receive full or partial exemption. Verify current IRAS conditions before relying on these points.

Do small foreign-founded companies need to care about **Multinational Enterprise (Minimum Tax) Act 2024** now?

This pack does not support a firm yes-or-no answer. It does not provide scope thresholds or a definitive applicability test for the Act. Treat it as a monitoring item and verify against current official guidance during planning cycles.

Try a related tool

Tomás breaks down Portugal-specific workflows for global professionals—what to do first, what to avoid, and how to keep your move compliant without losing momentum.

With a Ph.D. in Economics and over 15 years of experience in cross-border tax advisory, Alistair specializes in demystifying cross-border tax law for independent professionals. He focuses on risk mitigation and long-term financial planning.

Sources

Includes 5 external sources outside the trusted-domain allowlist.

- accountx.in/corporate-tax-compliance-in-singapore-deadli...external

- heysara.sg/singapore-corporate-tax-frequently-asked-que...external

- singaporecompanyincorporation.sg/faqs/singapore-corporate-taxationexternal

- taxsummaries.pwc.com/singapore/corporate/taxes-on-corporate-incomeexternal

- waterandshark.com/en-sg/blog/why-singapore-corporate-tax-syste...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Sole Proprietorship vs LLC for Global Freelancers in 2026

For most freelancers in 2026, the practical default is still simple: use the simplest structure you can run cleanly, then formalize when risk actually rises. If your work is still in validation mode and the downside is contained, a sole proprietorship is often the practical starting point. When contract exposure, delivery stakes, or dispute risk starts climbing, forming an LLC deserves earlier attention.

Why RegTech Becomes a Defensible Compliance Moat

RegTech becomes a moat only when it makes compliance decisions easier to execute and defend. The buying decision comes down to one question: does this investment create durable capacity, or does it add overhead your team must carry?

DAO for Freelancers Who Need Payment Certainty

Treat any **dao for freelancers** opportunity as unconfirmed income until you verify who releases funds and how that release happens. A passed vote, active Discord, or busy forum thread may look encouraging, but none of it guarantees payment.