Quick Answer

Start by routing every client payment to a business account before your first invoice, then run company spending on business cards and post owner pay as salary or draw before personal use. For separate business personal finances, treat personal-card business purchases as documented exceptions and reimburse them in the same close cycle. Your monthly file should reconcile statements, receipts, and transfer notes so each money movement is traceable without detective work.

Separation is a weekly habit, not a one-time bank setup#

For an LLC, separating business and personal money is best treated as a weekly habit, not a one-time bank setup. It keeps records cleaner, cuts month-end cleanup, and creates clearer boundaries as the company grows.

A separate business checking account is more than bookkeeping hygiene. U.S. banking guidance from the FDIC links separation to limited personal liability support, and it aligns with IRS small-business owner-pay guidance. It is not a guarantee in every dispute, and it is not a universal global rule, but it is a defensible baseline.

When accounts are mixed, close cycles drag because you have to untangle personal and business transactions after the fact. The point here is to give you real-time rules you can use before the mess piles up.

Treat the first month as training for your normal rhythm. Review inflows, spending, owner transfers, and missing receipts every week so you catch problems while the context is still fresh. That habit can keep month-end from turning into a reconstruction project.

By the end, you should have three practical tools:

- A setup sequence for incoming client payments, business spending, and owner pay.

- A decision rule for gray-area transactions that are not clearly business or personal at first glance.

- A month-end evidence checklist to keep statements, receipts, and transfer categories consistent.

Use this day-one checkpoint: monthly and year-end statements should let you verify payments and receipts without detective work. If a line item cannot be matched to purpose and records, flag it and fix it in that close cycle.

Separation also improves access control as operations expand. You can authorize day-to-day banking help without exposing personal finances, and eligible business deposits at one insured bank may be insured up to $250,000 separately from owners' personal accounts.

Scope note: legal and tax treatment varies by country and by program. Use this as operating guidance, then confirm jurisdiction-specific points with a qualified advisor when you set owner pay, change entity structure, or add more complex account arrangements.

What separate finances means in practice#

Separate finances means each dollar has one lane: business activity stays in business accounts, and personal activity stays in personal accounts.

Commingling of funds is business money paying personal expenses, or personal money paying business expenses, in ways that blur ownership. Your business bank account should not function as a second personal checking account. Owner's draw and salary are both owner pay. Once that payout is made, the money is personal and should be spent from personal accounts.

Use three clean rails:

- Client payments go into business accounts.

- Business spending runs through business accounts and business-only payment methods, such as a business checking account or business credit card.

- Owner pay is recorded as a transfer, then personal spending stays personal.

If a charge starts in the wrong lane, treat it as an exception and document the fix. Do not normalize that exception as everyday behavior. One-off mistakes are manageable. Repeated lane-crossing without records creates confusion during tax prep and weakens financial clarity.

Common commingling examples:

- Depositing a customer check into a personal checking account.

- Paying for business supplies on a personal card.

- Paying for groceries on a business credit card.

- Keeping business and household money in one account.

- Using a personal card for business expenses without clear records.

When balances are mixed, even a simple amount like $2,800 becomes ambiguous. You cannot tell whether it is business profit or personal money not yet moved. That confusion makes tax filing harder and turns even basic questions into guesswork.

Keep one recurring checkpoint in mind: your statements should let you trace payments, receipts, and owner transfers without detective work. Transfers touching personal accounts should map to owner pay and be documented.

Why LLC protection fails when operations are sloppy#

LLC protection weakens when your records and money flow make the company look like an extension of you. An LLC can separate company risk from personal assets, but that protection is not absolute. Courts may disregard that separation when day-to-day operations ignore basic legal and financial formalities.

That is the core issue behind piercing the corporate veil. Commingling personal and business funds is a major red flag because it supports an alter-ego argument. If one account handles everything, or personal and business payments are mixed without clean records, your legal position gets weaker.

In practice, records do more than satisfy bookkeeping. They show whether the company was treated as its own entity. When statements, ledgers, and transfer notes all tell the same story, your position is easier to defend. When they conflict, you spend time explaining gaps instead of showing discipline.

The point is simple: legal separation is only as strong as daily operations. When records and financial behavior are sloppy, that separation is easier to challenge.

Use this rule whenever money moves through the business:

- If a payment cannot be clearly tied to a business purpose and records, pause and document it before treating it as a business transaction.

- Keep personal and business flows separated in both accounts and books.

- Keep a correction note with the transaction so the file shows what changed and why.

Your monthly file should make three things easy to show: separate banking, separate books and records, and documented business decisions. When that discipline slips, legal complexity can work against you.

State law is the final variable. Veil-piercing standards vary by jurisdiction, so outcomes are not uniform. In California, attorney analysis cites a 2010 appellate decision and California Corporations Code § 17705.03 to argue that if a charging order will not satisfy a judgment, foreclosure of an LLC membership interest may be allowed. Treat that as California-specific, not a universal rule.

If you want a deeper dive, read Sole Proprietorship vs. LLC: The Definitive Guide for Global Freelancers.

Set up your account stack before money starts moving#

Set this up before you send your first invoice. Doing it early helps prevent commingling and supports the integrity of the corporate veil. An incorporated business is treated as separate, so your banking and spending rails should reflect that from day one.

Use this sequence as a practical control, not a universal legal mandate:

- Treat the incorporated business as separate from your personal finances.

- Open a small business bank account and keep your personal checking account separate.

- Open and use a business credit card for business charges.

- Move recurring operating bills into the company's name early, including utility accounts.

- Verify invoice payment details route to business accounts before you send invoices.

Before the first payment arrives, confirm client funds land in a business account, not personal checking.

Build a setup you can reconcile cleanly each month and explain without ambiguity.

This makes tax-time bookkeeping and accountant review easier because business activity is separated at the source. As you grow, supplier credit in the company's name can fit this setup, sometimes with terms like net 10 to net 60 days.

Related: The Best Business Bank Accounts for Freelancers.

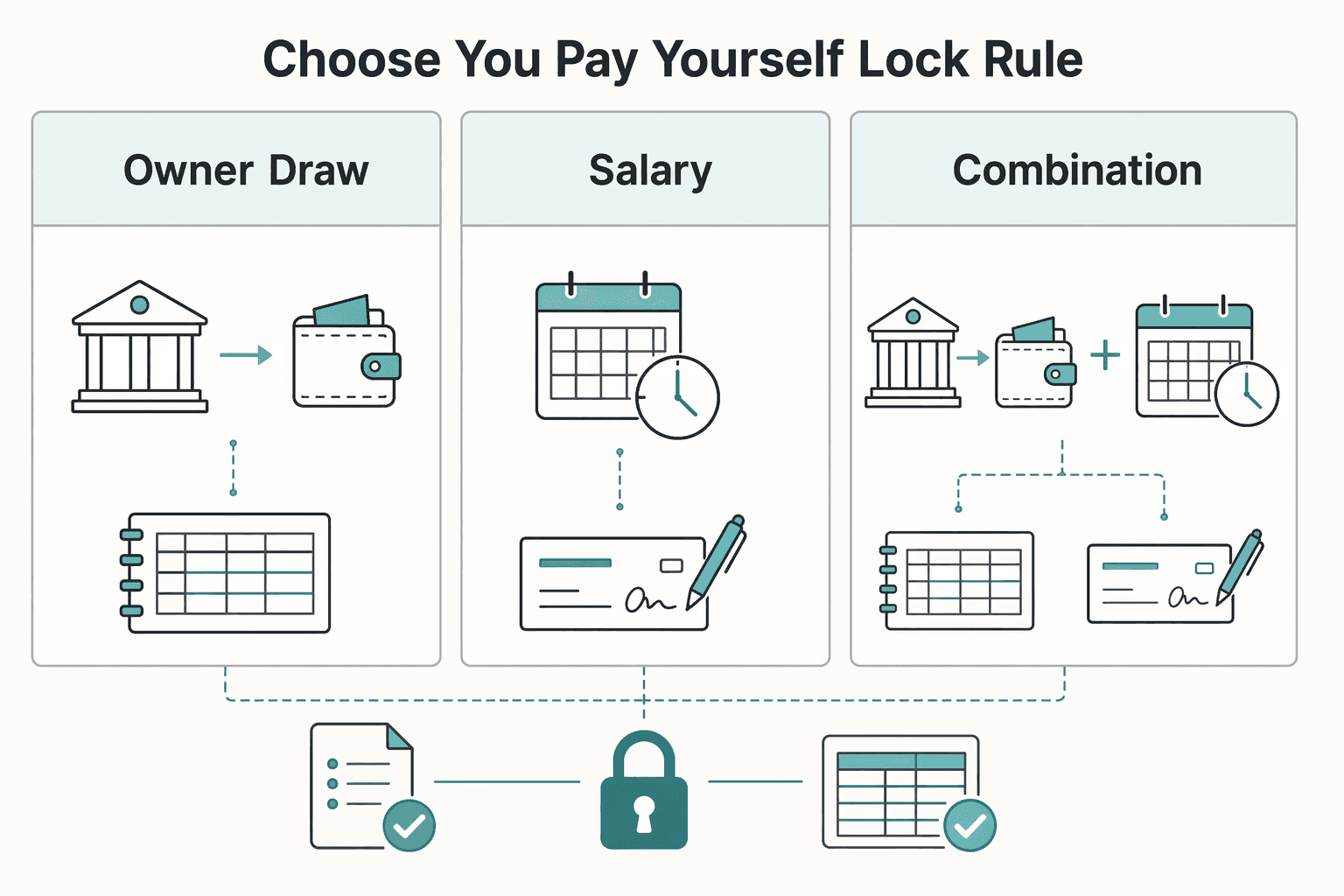

Choose how you pay yourself and lock the rule#

Pick your owner-pay method based on your business structure and tax treatment, then apply it consistently. This is where separation often breaks down, so set the policy early and keep personal spending out of business accounts.

| Method | Best fit | Key note |

|---|---|---|

| Owner's draw | Income is volatile | Use draws based on a documented internal rule; tax handling can be less predictable during the year and can create pressure at year-end. |

| Salary | You need predictable household cash flow | Set a fixed cadence such as weekly, bi-weekly, or monthly; it supports consistency but requires steady cash flow. |

| Combination | You need both consistency and flexibility | Use salary plus draws tied to your cash plan; it can work if documentation stays strict. |

An Owner's draw is money taken from the business for personal use. A Salary is a set amount paid each pay period, typically through payroll. If your business is taxed as a corporation, officer pay is generally treated as employee wages, and pay should be commensurate with duties. Confirm jurisdiction-specific treatment before finalizing your method.

Use a written if-X-do-Y rule so you are not deciding this on the fly:

- If you need predictable household cash flow, set a fixed salary cadence, such as weekly, bi-weekly, or monthly.

- If income is volatile, use draws based on a documented internal rule.

- If you need both consistency and flexibility, use a combination method: salary plus draws tied to your cash plan.

Keep the tradeoffs explicit. Salary supports consistency but requires steady cash flow. Draws are more flexible, but tax handling can be less predictable during the year and can create pressure at year-end. A combination can work if documentation stays strict.

Write your pay policy in plain language and keep it where bookkeeping decisions are made. Include cadence, approval steps, and what happens when cash is tight. The goal is not legal prose. It is a rule someone can follow on a busy day without improvising.

In your bookkeeping system, require every owner-pay event to record the date, pay type, and period under your internal policy. Use consistent labels to distinguish salary from draw. This is an audit and bookkeeping control, not a claim that specific software fields are legally required.

Your rule should be simple: pay personal bills from personal accounts only, after the pay event is posted. If a transfer cannot be tied to a recorded pay event, treat it as a red flag and correct it in the same close cycle.

Use a transaction decision rule for gray-area spending#

Make the call at the moment of purchase, not at month-end. Real-time decisions keep mixed transactions from piling up and making your books harder to classify correctly. Business costs go through business rails, personal costs stay personal, and exceptions are documented.

Use this three-question check before you charge or code anything:

- Is this exclusively business? If yes, use your dedicated business card and keep the receipt with a short purpose note.

- Is there a clear business receipt and purpose? If no, hold it in an exception queue until documentation is complete.

- Is this mixed-use? If yes, apply your internal allocation policy and document how you classified the business and personal portions.

If a personal card is used for an urgent business purchase, reimburse it from the business account only after the receipt and purpose note are in place.

Keep the exception queue simple: transaction date, amount, payment method, what support is missing, current status, and owner. That keeps gray items visible and prevents a silent backlog. It also gives you a clean handoff if your bookkeeper or accountant asks how each exception was resolved.

| Gray-area spend | Decision path | Evidence to retain |

|---|---|---|

| Software used for work and personal life | Keep fully business tools on business rails. For mixed tools, follow your documented allocation approach. | Invoice, allocation note, category rationale |

| Travel upgrades | Separate required business travel costs from personal add-ons under your policy. | Itinerary, receipt, approval or policy note |

| Shared phone plans | Reimburse only the documented business portion under your internal rule. | Carrier statement, allocation note |

| Recurring business subscriptions, payroll, or vendor payments | Move recurring business spending into business rails within a 30-day window. Use temporary exception coding until moved. | Invoice or bill, migration date, exception-log entry |

A common failure mode is delaying cleanup until later. That creates an uncategorized backlog, increases mislabeling and missed reimbursements, and can weaken liability shielding if your books are challenged.

Build a month-end close that proves separation#

Your close should make the boundary between business and personal activity obvious from the records alone. If another reviewer cannot follow owner pay, expenses, and transfers quickly, the process is too loose.

Use one short checklist in your main ledger each close cycle:

- Review business account activity and clear unmatched items.

- Flag charges without a clear business purpose.

- Confirm every owner-pay event is recorded through your formal process, such as Owner's draw or Salary.

- Confirm receipts are retained for business spending.

- Document how shared expenses were tracked.

Maintain an exception log for uncategorized items and unresolved business-personal transfers. For each item, record date, amount, account, status, and missing documentation so open items do not drift.

Use a consistent close sequence so nothing gets skipped when timing gets tight: review core accounts, review owner transfers, resolve or park exceptions with notes, and finalize period files.

For transfers involving a personal account, document the classification as part of close. If documentation is missing, keep the item in exceptions until resolved.

The long-term risk is letting mixed items sit unresolved. Blurred records make tax prep harder, weaken the distinction between business and personal money, and can increase risk to personal assets.

Turn this checklist into action this week with one practical template from the Gruv tools library.

Fix commingling mistakes fast without creating new risk#

Correct mixed transactions quickly and document each fix so one-off errors do not turn into a visible pattern. You do not need perfect books in one pass. You need a record showing the issue was identified, resolved, and less likely to repeat.

Use a consistent internal checklist for each flagged item:

- Identify the mixed transaction: record account, date, amount, and why it appears mixed.

- Classify the likely cause: wrong payment method, missing receipt, unclear business purpose, or incorrect category.

- Post a correcting entry: move it to the best-supported classification in your ledger.

- Attach supporting evidence: for example, the receipt, the bank or card line, and a short explanation note.

- Document a preventive rule change: state what should reduce the same error next cycle.

If you cannot support business purpose with evidence during close review, consider classifying the item as personal for now rather than forcing a weak business claim. That is a conservative risk-control choice, not a legal rule. If better support appears later, reclassify with a dated note explaining what changed.

When you correct an item, preserve traceability. Keep the original transaction reference, the corrected category, and the reason for the change together so a reviewer can follow the chain without guesswork. The point is transparent correction, not quiet relabeling.

Keep each correction in a compact review pack so another person can follow your logic quickly. A practical pack can include the transaction line, support document, explanation note, and updated category in your bookkeeping record. This keeps ledger changes traceable from source to final classification.

Timeliness matters. When errors sit unresolved, commingling starts to look structural rather than incidental, which increases risk and weakens the separation narrative.

Build business credit while keeping personal spend separate#

Build credit in the company name so routine expenses stay on business accounts, not personal cards. The goal is a business credit history that stands apart from your personal profile while reinforcing clean separation of funds and records.

For U.S. businesses, a common path is straightforward:

- Get a DUNS Number, a widely used business identifier.

- Open relevant vendor or supplier trade credit accounts and use company information on each credit application.

- Route ongoing operating spend through a business credit card, the primary tool for separating business and personal charges.

- Pay on agreed terms and keep records consistent so repayment activity stays tied to the business.

Trade credit can include terms like net 10 to net 60 days, which can help with short-term payment timing. Use those terms deliberately so flexibility supports operations without blurring business and personal activity.

Your discipline here is straightforward: if a vendor account is in the company name, pay it from company funds and record it in company books. If consistency slips, tighten payment and bookkeeping routines before you add more credit lines.

When evaluating new financing, keep the tradeoff clear: added credit can support purchases, and lenders may still review owner-level creditworthiness and whether the business is in good standing. Keep separation visible in every account choice to protect personal assets and support corporate-veil integrity.

Handle cross-border and tax-reporting caveats without overcomplicating#

Keep your money-separation approach consistent across borders, then treat reporting as a separate checklist. The operating rule does not change, but U.S. taxpayers may have added filing duties when foreign accounts or assets are involved.

For U.S. reporting, keep these terms distinct: FATCA, Form 8938, FBAR, and FinCEN. The IRS page for Form 8938 scope and filing cues is a practical starting checkpoint. Form 8938 is attached to your annual income tax return. FBAR is FinCEN Form 114 and is filed separately, not with the IRS. One does not replace the other, so evaluate both requirements every year.

| Filing item | Where it is filed | Trigger cues to verify |

|---|---|---|

| Form 8938 | Attached to your annual income tax return, due with that return, including extensions | Thresholds vary by filing status and residence. U.S.-resident examples include $50,000 on the last day or $75,000 at any time for unmarried filers, and $100,000/$150,000 for married filing jointly. |

| FBAR (FinCEN Form 114) | Filed with FinCEN, not with the IRS | Foreign financial accounts with an aggregate value over $10,000 at any time during the calendar year. |

Before you conclude anything, check scope. Form 8938 applies to a specified person, which can be a specified individual or a specified domestic entity, and specified domestic entities can include certain domestic corporations, partnerships, and trusts. If no income tax return is required for the year, Form 8938 is not required for that year.

Keep account ownership records and statement archives clean across domestic and foreign accounts so the evaluation work is repeatable. Your review should show who owns each account, who can sign, and which filings were considered. Clean labels and complete files reduce rework when advisors review your position.

Keep a simple evidence pack so filing season stays manageable:

- Account ownership records for each foreign account, including legal owner name, entity type, and signer authority.

- Monthly and year-end statements archived in one place with consistent account labels.

- A filing memo showing which accounts were evaluated for Form 8938 and which were evaluated for FBAR, even when the result is not required.

- A pre-filing check against the latest IRS Form 8938 instructions.

Use one operating rule to avoid rework: if you change owner pay timing, switch account ownership, or add a foreign account holder, pause and re-check reporting impact before the change goes live. Reporting scope depends on filing status, residence, entity type, and current thresholds, so confirm obligations with a qualified tax professional before you change owner pay or account structure. If you want a deeper refresher on owner-pay choices before that discussion, see How to Pay Yourself from an LLC: A Guide for Freelancers.

Keep a 30-day implementation checklist so this sticks#

Treat this as a repeatable reset skill, not a perfect first month. If you miss a week, restart with the smallest unfinished action and move forward.

- Week 1: Set the baseline. Write down your current setup, identify the biggest gap, and complete one simple fix first.

- Week 2: Reduce friction. Move through recurring money flows one by one, note what changed, and keep a pending list for anything not finished.

- Week 3: Define exceptions. Document how non-routine transactions are handled so edge cases are processed the same way each time.

- Week 4: Close and improve. Review the month, clear unresolved items, and tighten the single failure point that repeated most.

At day 30, run one verification pass: review recent transfers, map each one to a documented purpose where possible, and note anything that still needs cleanup. Keep the notes brief so month two is easier than month one.

| Day-30 check | Pass threshold | Fix if missed |

|---|---|---|

| Unclassified transactions | 0 items older than 7 days | Resolve and document the oldest exception first |

| Owner-transfer documentation | 100% tagged as salary, draw, or reimbursement | Backfill labels and note approval context in the same close cycle |

| Receipt coverage for business charges | 95%+ with receipt and purpose note | Move missing-support items to exception queue until complete |

If progress stalls, do not restart from zero. Pick one unresolved item from your exception list, close it fully, and continue from there. Momentum can return when the first blocked item is cleared with complete documentation.

The main takeaway#

Separation is a day-to-day discipline, not a one-time setup task. Treat the business as its own entity in every transaction.

Keep one clear rule in place: business money and personal money do not mix. Dedicated business accounts make that boundary visible and support cleaner bookkeeping, clearer tax compliance work, and more usable numbers.

Risk builds when mixing becomes routine. Personal spending through business accounts or undocumented owner transfers can create accounting errors, cash flow confusion, and weaker separation in a legal dispute.

Use one formal owner-pay process and document it every time. If you pay yourself, use a defined method such as salary or owner's draw and keep a record of each payment. If personal and business spending gets mixed, treat it as an exception and document the correction clearly.

Use a simple monthly check:

- Business income and expenses run through business accounts.

- Owner transfers are documented consistently.

- Mixed transactions are corrected quickly with a clear note.

Run the checklist at the same point each month, then carry forward only documented exceptions. That cadence turns separation from a reminder into an operating habit you can prove.

This guidance is educational, not individualized legal or tax advice. It will not remove every risk, but clear separation and complete records can reduce avoidable problems as the business grows.

If you want your invoicing, records, and payouts to stay organized as you grow, explore Gruv for freelancers.

Frequently Asked Questions

Do I need separate accounts if I already formed an LLC?

Yes. Forming an LLC is not enough if day-to-day operations still mix personal and business money. Use a dedicated business account and pay business expenses from it to keep the business clearly separate. The practical test is simple: can you show, from your records, which charges belong to the business and which belong to you personally? If not, separation is not yet working.

What exactly counts as commingling of funds?

Commingling means mixing personal and business funds in ways that blur ownership. Common examples include paying personal groceries from a business account or buying business inventory on a personal debit card. If money moves between you and the business, document it. A useful rule is to classify money movement by purpose at the time it happens. If purpose is unclear, treat it as an exception until support is complete.

Can I ever use my personal card for a business expense?

It can happen, but it should stay an exception. When it does, record the transfer clearly as a reimbursement, loan, or owner’s draw so the paper trail stays intact. Repeated personal-card use without records weakens separation and can create tax problems, including deduction issues. Keep the receipt and note attached to the related entries.

Should I pay myself with an owner's draw or a salary?

Both are used in practice, and no single method is universally correct in every setup. Choose a formal process, run it on a regular cadence, and keep records for each payment. If you change methods later, document when the change starts and how each payment type is categorized so records remain clear.

What is the minimum setup I can finish this week?

Start with one business checking account and a business debit card. Then set one rule: business expenses are paid by the business, and owner transfers are documented. That gives you a clean baseline you can tighten over time.

Which records matter most if I am audited or legally challenged?

Keep clean, separate records that show what belongs to the business and what belongs to you personally. Prioritize account statements and written records for owner transfers, including draws, reimbursements, and loans. This paper trail supports expense treatment and helps show the business was operated as its own entity. When records conflict, resolve the mismatch and keep a short note explaining what changed.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- ask.fdic.gov/fdicinformationandsupportcenter/s/article/Q-...trusted

- irs.gov/businesses/corporations/do-i-need-to-file-fo...trusted

- irs.gov/businesses/small-businesses-self-employed/pa...trusted

- mn.gov/deed/assets/a-guide-to-starting-a-business-i...trusted

- sba.gov/blog/5-ways-separate-your-personal-business-...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Sole Proprietorship vs LLC for Global Freelancers in 2026

For most freelancers in 2026, the practical default is still simple: use the simplest structure you can run cleanly, then formalize when risk actually rises. If your work is still in validation mode and the downside is contained, a sole proprietorship is often the practical starting point. When contract exposure, delivery stakes, or dispute risk starts climbing, forming an LLC deserves earlier attention.

How to Pay Yourself From an LLC as a Freelancer

Your pay method should follow tax treatment, not the fact that you formed an LLC. IRS guidance ties owner compensation to elected business structure, so classification comes before any transfer.

The Best Business Bank Accounts for Freelancers

APY can break a tie. It should not drive your shortlist. If you are comparing the best business bank accounts for freelancers, start with the setup that keeps money moving, records clean, and month-end work manageable.