Quick Answer

Choose a convertible note when you need a maturity checkpoint and debt-priority rights in downside scenarios; choose a SAFE when you accept event-based conversion timing without a debt clock. In a safe vs convertible note decision, cap and discount can look similar across drafts, so focus first on the financing trigger, qualified-round conditions, and liquidity or dissolution payout terms. If those clauses are vague, treat the deal as unresolved risk and renegotiate before wiring funds.

The Core Distinction: Why a Loan vs. a Warrant is the Only Thing That Matters#

Start with legal position. That is what determines your control when outcomes get messy. A convertible note gives you a debt-like claim first and may convert into equity later. A SAFE gives you a contractual right to future equity tied to specific events, without a debt claim before those events.

In a safe vs convertible note decision, cap and discount shape upside, but they do not answer the core control questions. Is there a maturity clock? Does value accrue while you wait? Where do you stand if the company fails before conversion?

Debt gives you a clock and a control checkpoint#

A convertible note is debt-like while it is outstanding. It typically includes a maturity date and an interest rate, so there is a defined point when repayment terms come due. Interest also accrues while the note is outstanding.

| Checkpoint | What the paper should show |

|---|---|

| Maturity clause | Whether the note has a defined date when repayment terms come due |

| Repayment mechanics | Whether repayment can be requested and whether majority noteholder action is required |

| Amendment terms | Whether the form includes maturity-extension mechanics |

| Election control at maturity | Who controls any election of stock instead of cash at maturity |

That does not mean every note lets you unilaterally demand cash at maturity. Some forms require majority noteholder action to request repayment. Some allow majority holders to elect stock instead of cash. Some include maturity-extension mechanics. Check four things: the maturity clause, repayment mechanics, amendment terms, and who controls any election at maturity.

A SAFE removes those debt-style mechanics. It has no maturity date, no interest accrual, and no debt repayment requirement. Outcomes are tied to defined events, such as an equity financing, liquidity event, or dissolution event, not a debt due date.

Shared economics, different legal rails#

Both instruments can use the same conversion economics: a valuation cap and a discount. Those terms can improve entry economics for early investors, but they do not erase the legal difference between debt positioning and event-based contract rights.

| Feature | Convertible note | SAFE |

|---|---|---|

| Legal position before conversion | Debt-like claim that may convert later | Contract right to future equity on specified events |

| Maturity | Has a maturity date in the note terms | No maturity date |

| Interest | Accrues while outstanding | No interest accrual |

| Repayment path | May be repayable at maturity, often subject to majority-holder or document-specific mechanics | No debt repayment requirement |

| Priority if the company fails before conversion | Debt positioning matters because creditors come before common stockholders | Not a debt claim |

| Valuation cap | Often sets the maximum valuation used for conversion | Often used in conversion economics |

| Discount | Often reduces the next equity financing price per share | Often reduces the next equity financing price per share |

A common ambiguity point is trigger mechanics, not labels. Notes commonly convert in a next financing, but some only auto-convert if that financing clears a minimum new-cash threshold. SAFEs depend on their listed trigger events, so timing can depend on whether a qualifying event occurs.

Before moving to risk scenarios, verify four items in the actual paper. Check the note maturity and repayment mechanics, any minimum-cash conversion threshold, SAFE trigger-event language, and the exact cap and discount terms. If any of those are unclear, your downside is still unclear. For related context, see What are 'Blue Sky Laws' and How Do They Affect Startups Raising Capital?.

What a Founder's Choice of Instrument Signals#

A founder's choice of instrument is a diligence signal about financing discipline, not just legal paperwork. Your core test is whether they can explain dilution and downside in practical terms, then back it up with a clear cap table view.

A SAFE can work, but it requires clear dilution visibility. Ask for a pro forma cap table that shows total SAFE volume, convertible note principal, accrued interest, and effective ownership after conversion. The common failure mode is that early simplicity turns into late complexity when instruments with different caps and discounts stack up. If they cannot show who absorbs dilution as the stack grows, ask: "Show me ownership after all outstanding instruments convert in the next priced round."

A convertible note can signal contingency planning if the founder addresses maturity outcomes directly. You want a specific plan for what happens if no priced round occurs before maturity, including extension, renegotiation, or repayment risk. Ask: "If financing does not happen before maturity, what is the plan, who can approve changes, and which terms are most likely to be reopened?"

| Founder choice | Likely founder intent | Investor risk implication | Your next diligence action |

|---|---|---|---|

| SAFE | Prioritize early-stage simplicity | Dilution visibility can be delayed until conversion math is consolidated | Review one pro forma model showing total SAFE volume and effective ownership after conversion |

| Convertible note | Work with a financing clock and discuss downside terms upfront | Maturity can trigger extension talks, renegotiation, or repayment pressure | Read the maturity language and request the no-priced-round contingency plan |

| Mixed instruments with different caps/discounts | Raise opportunistically across checks | Cap-table congestion and more Series A negotiation friction | Reconcile every instrument into one conversion model |

| Either instrument explained as "standard" | Template-driven reasoning | Weak command of financing mechanics | Ask why this instrument fits this round specifically |

The real red flag is not simplicity, but unexamined simplicity. When a founder can connect instrument choice to dilution, cap-table clarity, Series A negotiation, and investor perception, that is signal. When the answer is only "this is the standard form," treat it as noise and keep testing. That matters because the paper only shows its teeth when the company leaves the happy path. Related: How to Price AI-Assisted Freelance Services.

The Operator's Risk Matrix: How SAFEs and Notes Perform Under Pressure#

When outcomes get messy, your control often comes from a note, not a SAFE. The split is simple: a note has a maturity clock, and a SAFE does not.

Big priced round#

If the company closes a strong priced round, both instruments can land in a similar place for you: conversion into preferred equity. Notes are commonly drafted to convert in the next financing, and SAFEs convert at an Equity Financing.

Do not confuse similar upside with similar protection. Before conversion, a note still carries debt features like maturity and usually interest accrual. A SAFE is designed to stay outstanding until a defined termination event. Also check the note's qualified financing definition. Automatic conversion may not trigger unless the raise clears the stated minimum threshold.

Stagnation without new funding#

If the company stalls, your practical leverage is usually stronger with a note. Maturity can create a decision point: repayment, extension, amendment, or negotiated conversion.

| Point to verify | What to check |

|---|---|

| Note maturity date | Confirm the date that creates the maturity decision point |

| Maturity remedy | Check whether the outcome is repayment, extension, amendment, or negotiated conversion |

| Interest | Verify whether interest accrues and how it is calculated |

| Qualified financing trigger | Confirm the trigger language for conversion |

| Minimum new-money threshold | Check any minimum amount required for automatic conversion |

| SAFE termination events | Read the exact termination events in the form being used |

With a SAFE, there is no maturity trigger, so you may have no built-in clock to force that conversation. If no priced round or exit happens, your capital can remain outstanding for an open-ended period.

Before you wire money, verify the note maturity date and exact maturity remedy. Check whether interest accrues and how it is calculated, plus the qualified financing trigger and any minimum new-money threshold. For a SAFE, read the exact termination events in the form you are using.

Small exit before a priced round#

In an early sale, payout order and trigger language usually matter more than cap or discount. A note is debt, so your position is typically stronger than shareholders in downside claim order, but transaction documents and instrument drafting still control the actual payout.

For a SAFE, focus on the Liquidity Event clause. Payment timing is typically tied to closing, but cash-out formulas differ across SAFE forms, so you cannot assume one universal treatment. Verify the exact SAFE template and version, then record the real outcome in your deal memo.

| Scenario | Likely outcome for you | Investor leverage | Key clause to inspect | Immediate diligence action |

|---|---|---|---|---|

| Big priced round | Both often convert into equity | Moderate; mostly economic terms | Equity Financing / Qualified Financing trigger | Confirm conversion mechanics and any minimum raise threshold |

| Stagnation | Note can trigger a maturity conversation; SAFE can remain outstanding | Usually higher with note | Maturity remedy, interest, SAFE termination events | Ask what happens if no priced round occurs before maturity or for an extended period |

| Small exit | Note often has stronger downside position; SAFE outcome is form-dependent | Clause-driven in both | Change-of-control / Liquidity Event treatment | Write exact cash-out or conversion treatment into the memo after document check |

If you are underwriting downside instead of only upside, prefer the instrument that gives you a clock and a clear negotiation point. In many deals, that is the note. Once you understand how the paper behaves under stress, test whether the team understands those same pressure points. If you want a deeper dive on SAFE mechanics, read What is a SAFE (Simple Agreement for Future Equity) in Startup Fundraising?.

Your Due Diligence Checklist: 5 Questions to Ask Before You Invest#

After you map deal risk, test the operators behind the paper. At pre-seed, you often do not have customers to call, revenue history to audit, or much historical data, so people diligence and corporate hygiene carry more weight. Use these five asks live, then score the responses before you wire.

Use one scale across all five:

- Green flag: Specific answer, consistent with documents.

- Caution: Plausible answer, but documents or assumptions are incomplete.

- Escalate: Stop and verify. Do not rely on verbal summaries.

| Ask | Why it matters | What to inspect | Green flag | Caution | Escalate |

|---|---|---|---|---|---|

| 1. Who founded and currently manages the company, and are any previous founders no longer actively involved? | Pre-seed diligence is heavily people-focused. | Current founder/management roster, role history | Team gives a clear, consistent account of who is active now and who is not. | Role changes are mentioned but timelines or responsibilities are unclear. | Conflicting answers about who is still involved. |

| 2. Show me the current cap table and where cleanup work may still be needed. | The cap table is a core ownership checkpoint, and unresolved departures can leave outsized early ownership. | Current cap table, ownership notes tied to founder departures | Table is current, and any cleanup work is explicitly identified. | Table exists, but assumptions or ownership notes are stale. | No reliable table, or unresolved departure ownership with no cleanup path. |

| 3. Would any current key team member refuse a background check if requested? | Early disclosure of this risk is better than finding out later. | Direct yes/no from the team and any documented exceptions | Direct answer with no refusal. | Hesitation or conditional answers without clarity. | Refusal, evasive answers, or issue disclosed only late. |

| 4. Which answers today are evidence-backed, and which are still assumptions? | Pre-seed diligence is hard and iterative; separating facts from assumptions reduces surprises. | Diligence notes showing confirmed items vs open items | Unknowns are explicitly labeled and tracked. | Some unknowns are acknowledged, but tracking is incomplete. | Assumptions are presented as settled facts. |

| 5. If new information changes risk, how will diligence be updated before wire? | A repeatable process keeps core questions consistent across investments as your approach evolves. | Update owner, decision memo, and timing before close | Clear owner and update path before funds move. | Update path is informal or partially defined. | No owner, no process, or no timing for updates. |

When any answer lands in Caution or Escalate, go back to the records. Verify who is actively involved, what the cap table currently shows, whether founder-departure ownership is resolved, and whether any background-check issues were disclosed early. If the story and records diverge, treat the gap as unresolved risk until clarified.

Pre-wire verification#

Before sending funds, turn this checklist into a go or no-go memo so you can compare answers against current records:

| Record | What to confirm |

|---|---|

| Current management roster | Current roster pending source-record verification |

| Previous founders no longer active | Current status pending source-record verification |

| Current cap table version/date | Current cap-table version/date pending source-record verification |

| Ownership cleanup needed | Current status pending source-record verification |

| Background-check exceptions disclosed | Disclosure status pending source-record verification |

| Open diligence unknowns | Current open items pending source-record verification with owner and date |

- Collect the latest founder/management roster, current cap table, and notes on any founder departures.

- Fill it from records, not memory:

Current management roster: Current roster pending source-record verification. Previous founders no longer active: Current status pending source-record verification. Current cap table version/date: Current cap-table version/date pending source-record verification. Ownership cleanup needed: Current status pending source-record verification. Background-check exceptions disclosed: Disclosure status pending source-record verification. Open diligence unknowns (owner + date): Current open items pending source-record verification with owner and date.

- Reconcile the memo against founder answers. If a material blank remains or a conflict is unresolved, pause the wire.

For a step-by-step walkthrough, see How to Create a Financial Forecast for a Funding Round.

After you pressure-test people and cap-table risk, map how funds will actually move and be controlled in operations with the Gruv docs.

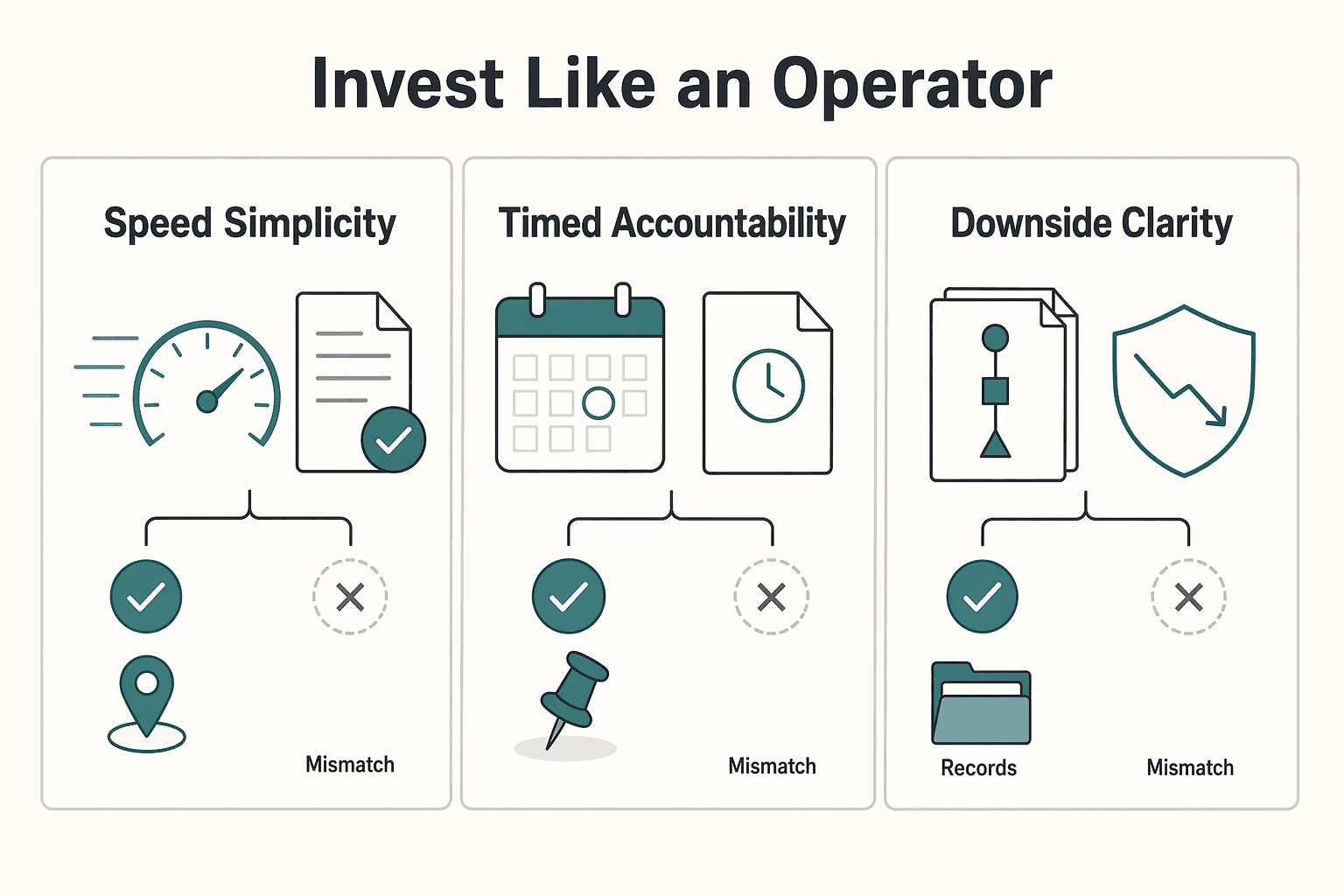

The Final Verdict: Invest Like an Operator, Not a Speculator#

In a safe vs convertible note decision, use a conditional rule. Choose the instrument only if the signed draft matches your risk tolerance on timing, payout clarity, and downside outcomes.

| Your priority | Better fit only if the draft clearly includes | What to confirm before signing |

|---|---|---|

| Speed and simplicity | Terms you can explain line by line, regardless of instrument | Conversion trigger, payout language on liquidity or dissolution, amendment mechanics |

| Timed accountability | A clear process for how the instrument resolves if no priced round happens | Any maturity timeline (if present), what happens at that point, and whether repayment or conversion terms are explicit |

| Downside clarity | Explicit language on priority and payout in a bad outcome | Waterfall order, subordination language, and economic terms tied to downside outcomes |

Before you sign, verify four items in the executed document, not a summary. Check the conversion trigger, any maturity clause (or explicit absence of one), the repayment or payout language, and the priority stack in a sale, shutdown, or similar downside case. If any of these are vague, you are accepting uncertainty on when, or whether, your capital is resolved.

Also verify legal wording in official source text when accuracy matters. FederalRegister.gov says its prototype edition is unofficial and that legal research should be checked against an official edition, including the official PDF on govinfo.gov.

Given the limited excerpts available here, avoid absolute rules about either instrument.

Next step: compare term sheets side by side, pressure-test downside clauses, and pick the instrument that matches your actual risk tolerance, not the fastest narrative. We covered this in detail in A Guide to 409A Valuations for Startups.

When you are ready to turn your seed-round plan into an auditable collect-to-payout workflow, review Merchant of Record for business.

Frequently Asked Questions

What is the biggest practical difference?

You are choosing between two legal positions. A SAFE gives you a right to future equity, while a convertible note is a loan that converts under defined conditions. If the company stalls, debt status plus maturity often matters more than shared terms like cap and discount.

What should you check first if you are buying a note?

Start with the maturity date, the qualified financing definition, and the repayment language if conversion has not happened by maturity. If the next round may miss the minimum-cash trigger, you are underwriting a maturity negotiation, not just conversion math.

How should you read the valuation cap?

Treat the cap as a pricing term for conversion, not a general signal that the deal is investor-friendly. Check how conversion price is calculated, whether a discount also applies, and whether that cap actually applies to the trigger you expect. A strong cap can still disappoint if conversion does not happen cleanly or recovery is constrained by priority in a downside outcome.

What does qualified financing actually mean?

For notes, it usually does not mean any future round. Automatic conversion is commonly tied to a minimum amount of new cash, and that threshold varies by document. If you cannot point to the exact trigger amount in the note, treat verbal summaries as incomplete.

What is the difference between a pre-money and post-money SAFE?

With a pre-money SAFE, SAFE investors in the round dilute each other. With a post-money SAFE, ownership is measured after all SAFE money is counted and fixed relative to other SAFEs before new priced-round money. Ask which version you are signing before comparing caps, because dilution outcomes can diverge fast when multiple SAFEs stack.

What happens on a sale, change of control, or shutdown?

Read the exact liquidity, change-of-control, and dissolution clauses before you assume how you get paid. In some SAFE forms, a liquidity event before termination entitles the holder to the greater of the purchase amount or the as-converted amount, but that cash-out is junior to outstanding indebtedness and creditor claims, including convertible promissory notes. Also confirm how change of control is defined and where dissolution proceeds place you in the waterfall.

Does a SAFE have no downside rights at all?

No. A SAFE can include automatic payout rights in liquidity or dissolution events, but those rights are not the same as holding debt. Read payout mechanics and priority language together, because that combination controls real recovery.

When is each usually a fit?

In practice, SAFEs are widely used in early rounds. Carta reports SAFEs were 90% of earliest pre-seed deals on its platform in Q1 2025 and 64% of seed rounds, compared with 10% for convertible notes. If your priority is maturity discipline and debt mechanics when conversion does not occur, a note may be the better fit when you negotiate trigger and maturity terms up front.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 5 external sources outside the trusted-domain allowlist.

- investor.gov/introduction-investing/general-resources/new...trusted

- investor.gov/introduction-investing/investing-basics/inve...trusted

- carta.com/learn/startups/fundraising/convertible-secur...external

- cooleygo.com/convertible-debtexternal

- crv.com/content/safe-vs-convertible-noteexternal

- moonshotnx.com/capital/safe-vs-convertible-noteexternal

- ycombinator.com/documentsexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

What is a SAFE (Simple Agreement for Future Equity) in Startup Fundraising?

A SAFE, short for Simple Agreement for Future Equity, is a contract where an investor gives you money now in exchange for a future ownership interest if a trigger event happens, often a later equity financing or an acquisition of the company. It usually fits an early raise when you need speed, simpler documents, and the ability to close investors one by one. It is a weaker fit when investors want negotiated control rights now, or when you need exact dilution certainty before taking money.

How to Price AI-Assisted Freelance Services

Protect cashflow first, then optimize upside. Late-payment risk rises when scope is unclear, approval ownership is loose, and payment terms are left until late in the process.

How Blue Sky Laws Affect Startups Raising Capital

If you are raising money, state securities law matters from the start. For most startups, **the [blue sky laws](https://www.investor.gov/introduction-investing/investing-basics/glossary/blue-sky-laws) that matter are the state securities rules that sit alongside federal securities law**. Even if your round fits a federal exemption, states may still require notice filings, fees, and compliance with anti-fraud rules as money comes in.