Quick Answer

Yes. A regtech competitive advantage exists only when your team can trace one case end to end and export defensible records without manual reconstruction. The article’s proof standard is a live walk from intake to decision to export, plus exception-aging and approval-history checks. Tax handling is a useful stress test: if Form 8938 logic is unclear or treated as a substitute for FinCEN Form 114 (FBAR), the tool adds risk instead of durable capacity.

What makes RegTech defensible in compliance#

RegTech becomes a moat only when it makes compliance decisions easier to execute and defend. The buying decision comes down to one question: does this investment create durable capacity, or does it add overhead your team must carry?

Modern RegTech emerged in its current form after the 2008 global financial crisis. Regulatory alert volume rose from about 8,700 in 2008 to more than 64,000 in 2021. Interest is rising because compliance pressure is real, not because the category is new.

Adoption still depends on coordinated execution. Industry coverage points to clear value in financial-services use and to implementation challenges that can persist after procurement. Tools matter, but evidence discipline and operating consistency matter just as much.

For freelancers, small teams, and lean finance groups, the tradeoff is practical. A fast rollout with unresolved exceptions is weaker than a slower rollout your team can run consistently and explain under review.

By the end of this guide, you will have:

- A decision test to separate real capacity gains from surface automation.

- A red-flag checklist for claims that fail live verification.

- A phased rollout sequence that fits limited time and staffing.

Before you build a long shortlist, run this checkpoint. Ask each vendor to walk through a real case from intake to final decision and show what evidence remains if the original reviewer is unavailable. If that trace is slow, incomplete, or person-dependent, treat it as overhead risk.

Annual lists, including those covering 100 RegTech companies, can help with initial research, but they often sit alongside superficial or self-serving commentary. Use a stricter standard: controls that hold under pressure, evidence you can retrieve quickly, and a rollout your current team can sustain.

Define RegTech and the compliance moat in plain terms#

The moat is not the software license. It is reliable execution you can prove under review.

Threshold-based reporting shows why:

| Filer context | Threshold detail | Note |

|---|---|---|

| Certain taxpayers | IRS materials cite a $50,000 baseline. | The threshold is not one universal number for every filer type. |

| Certain specified domestic entities | $50,000 at year end or $75,000 at any time. | Certain domestic entities were included for tax years beginning after December 31, 2015. |

| Joint filers | Higher thresholds can apply. | The threshold is not one universal number for every filer type. |

| Taxpayers residing abroad | Higher thresholds can apply. | The threshold is not one universal number for every filer type. |

Use these working definitions when you compare options:

- RegTech: technology that applies compliance rules, records why decisions were made, and lets you reproduce those decisions later.

- Compliance as a Service: outsourced compliance execution when your team cannot run recurring controls and reporting duties consistently in house.

- Compliance moat: repeatable ability to pass checks quickly while keeping records clear enough for audit and partner review.

A grounded example is FATCA-related reporting through Form 8938:

- Form 8938 is used to report specified foreign financial assets when the applicable threshold is exceeded.

- The threshold is not one universal number for every filer type.

- IRS materials cite a $50,000 baseline for certain taxpayers.

- The instructions also cite $50,000 at year end or $75,000 at any time for certain specified domestic entities.

- Higher thresholds can apply for joint filers or taxpayers residing abroad.

Threshold logic can break in automation workflows. If a platform cannot show which threshold rule it applied to a specific filer and tax year, you still carry manual recheck risk.

Form 8938 reporting applies to tax years starting after March 18, 2010. Most individuals started filing with 2011 returns, and certain domestic entities were included for tax years beginning after December 31, 2015.

If you use a service model, require full traceability: intake facts, filer classification, threshold test, filing outcome, and approver. Confirm one boundary condition directly: filing Form 8938 does not remove FBAR obligations. Buying RegTech is a purchase decision. Building a compliance moat is an execution decision.

Why compliance pressure changed buyer economics#

Compliance now behaves more like a continuous requirement than a periodic project. Buyers judge value differently: a tool earns its place only if it cuts repeat work while keeping decisions defensible under review.

The pressure is structural. Oversight is becoming more data-driven, with more detailed and frequent regulator requests. Regulatory alert volume rose from 8,700 in 2008 to more than 64,000 in 2021. As volume rises, compliance management becomes more challenging and expensive.

The economics changed with it. Continuous pressure rewards platforms that produce clear, repeatable records on demand. Fragmented processes create handoffs, duplicate checks, and context loss. That increases rework and delays decisions.

Before you approve new spend, including Compliance as a Service, run one checkpoint:

- Trace one case from first intake to final decision, including flags, actions, and rationale.

- Confirm the full case record can be produced quickly during a live review.

- Check exception aging across the last two cycles; if unresolved items are growing, process drag is usually growing too.

Speed helps only if documentation quality holds. Fast decisions with weak records create repeat reviews. Fast decisions with clear evidence are more likely to produce consistent outcomes in internal and partner checks. If you cannot produce a complete decision trail quickly, fix evidence continuity before you expand scope.

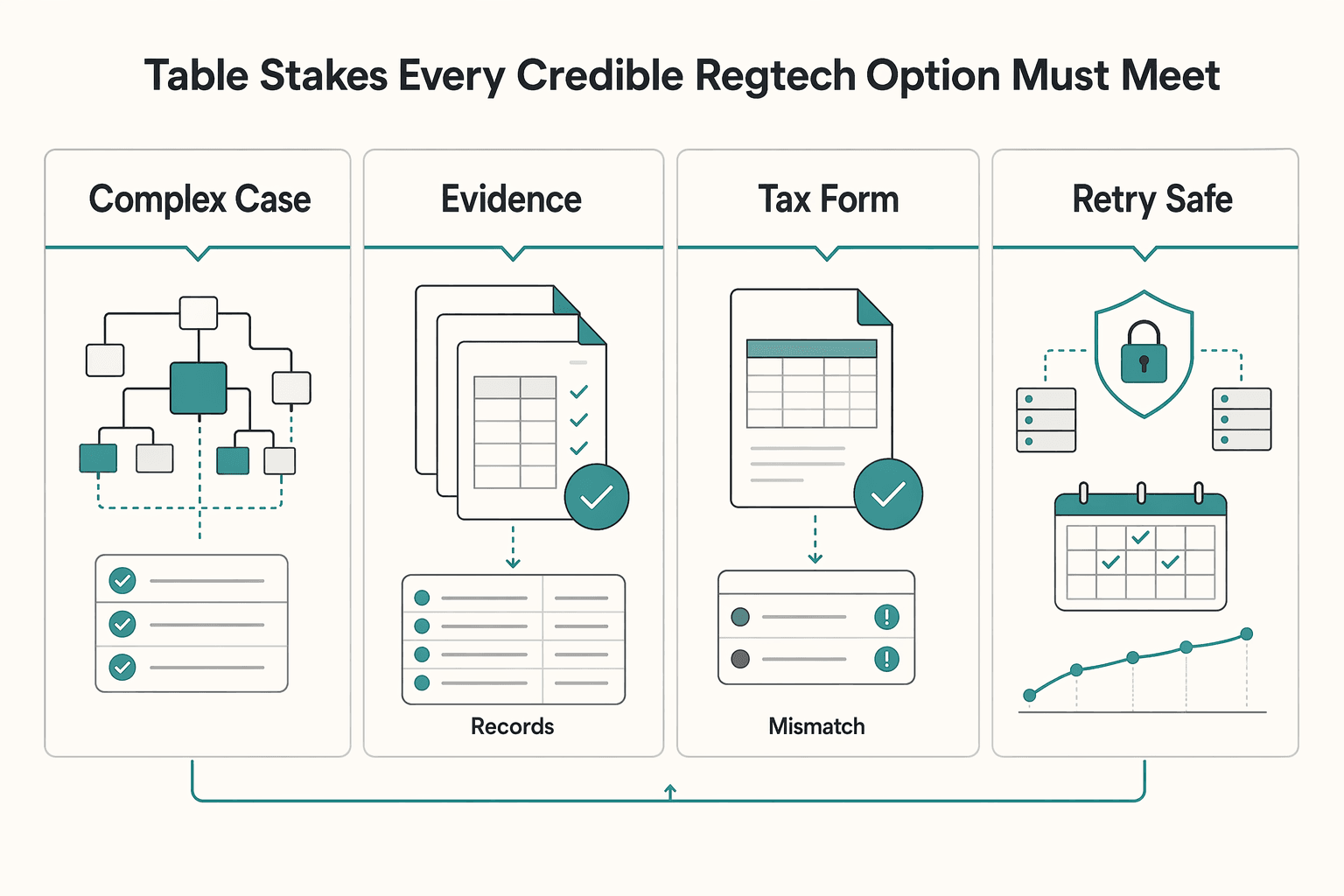

The table stakes every credible RegTech option must meet#

Any credible option should clear four practical checks: control coverage, evidence quality, tax readiness where relevant, and operational reliability. Decisions should stay explainable and repeatable under review pressure, not dependent on personal memory.

This pressure is not hypothetical. Regulation is becoming more stringent and affecting more participants, with examples including Consumer Duty, EMIR Refit, DORA, and T+1 Settlement. Businesses of all sizes still face an ongoing challenge in predicting, preparing for, and implementing regulatory change.

Cost pressure raises the bar further. One cited estimate puts U.S. compliance cost at about $70 billion annually, while market messaging can still be superficial or self-serving. Use demos to screen, then require proof in live scenarios.

| Capability to test on your shortlist | Why it matters now | What to verify live |

|---|---|---|

| Identity and AML workflow coverage relevant to your obligations (for example, KYC/KYB steps, screening, holds, and CDD trails) | Transparency and identity or AML control demands are rising | Trace one case from intake to final decision, including holds, releases, rationale, and approver history |

| Case-level evidence you can export (for example, timestamped events and decision rationale) | Reviews depend on complete evidence, not summaries | Export one full case record for internal audit and, where relevant, regulatory requests without manual stitching |

| Tax-form and jurisdiction handling where relevant (for example, W-8, W-9, Form 1099, or VAT) | Tax and compliance work often spans mixed obligations | Confirm what is native versus custom and test missing or expired document handling with a clear audit trail |

| Retry-safe processing and status tracking | Failures and retries happen in live operations | Re-run a failed step and confirm no duplicate outcome while preserving full history |

One common risk is a fragmented stack: one tool for KYC/KYB, another for AML actions, and rationale stored elsewhere. Teams then spend review time rebuilding a decision path instead of producing it on demand.

Reject early if you hear broad claims without a live case walkthrough and export. Do the same if onboarding is fast but decision rationale or approval history cannot be shown clearly. Reject early if in-scope tax-form coverage breaks on missing or expired documents.

The Compliance Moat test for small teams and finance operators#

Once table stakes are met, the moat is evidence continuity. You should be able to explain a payout decision directly from records, without rebuilding context from chat, memory, or side files.

Run a recurring live-case check. Pick one completed payout and trace the path end to end: identity and compliance checks, decision notes, approval history, and an exportable case record. If the path depends on spreadsheet handoffs, treat it as a gap in process integrity and audit readiness.

| Buyer axis | What to verify live | Risk signal |

|---|---|---|

| Control depth | Trace one case from intake to payout with checks, rationale, and approver history tied to the same record | Decision rationale lives outside the case record or cannot be reproduced end to end |

| Integration effort | Confirm status, decision, and payout metadata stay aligned without manual copy steps | Teams repeatedly reconcile key fields by hand across tools |

| Team workload | Review how exceptions are tracked, resolved, and reopened in real queues | Automation looks strong on the happy path, but exceptions require heavy manual cleanup |

| Audit and export quality | Export a complete case packet for tax-related review scenarios | Dashboard views look clean, but export history is incomplete or exception context is missing |

For U.S. tax-reporting readiness, verify how the tool handles Form 8938. Form 8938 applies when specified foreign financial assets exceed the applicable reporting threshold, and thresholds vary by filer type. For some taxpayers, that includes a $50,000 trigger. Specified domestic entities may also have filing obligations (for tax years beginning after December 31, 2015), including a $75,000 at-any-time test.

Confirm the record shows which threshold category was applied. Confirm it supports attaching Form 8938 to the tax return. Keep this separate from FBAR obligations, since Form 8938 does not replace FinCEN Form 114.

If your stack fails this test, fix evidence lineage and exception handling before adding tools. For small teams, defensibility usually comes from cleaner decision records, not a larger vendor stack. If you want a deeper tax context, read Taxes in Germany for Freelancers and Expats.

Compare build, bolt-on, and unified platform choices#

Prioritize connected compliance and payout records, and move to custom build only when documented edge-case needs exceed platform limits.

Use a four-axis scorecard rather than a feature checklist: control depth, integration effort, team workload, and audit and export quality. That matches multi-factor RegTech evaluation used in market screens such as REGTECH100, rather than relying on one headline capability.

| Option | Best fit | Main tradeoff | What to verify live |

|---|---|---|---|

| Build-heavy | Teams with strong engineering depth and in-house compliance specialists | High control, but rule and policy updates can compete with product work | Review a recent rule-change path from request to production, then test one updated compliance rule in a sandbox case |

| Bolt-on stack | Teams that need quick initial coverage with existing tools | Fast start, but reconciliation gaps can appear between compliance decisions and payout states | Run one exception case end to end and count manual handoffs across tools |

| Unified platform | Teams prioritizing connected evidence and fewer handoffs | Less custom behavior at first, with potential limits on edge cases | Trace one case from screening through payout and export, including any tax artifacts enabled for your market and program |

Synchronization quality is a practical checkpoint. If records are disconnected or delayed across tools, risk response can slow and exception handling can get harder. Ask vendors to show how status changes propagate across compliance checks and payment states, then inspect timestamps for drift or missing updates.

Build-heavy can still make sense when off-the-shelf options cannot represent your policy logic cleanly. Choose it only when both conditions are true: platform limits are clearly documented, and your team can ship compliance-rule updates predictably. If either condition is weak, tighten integration quality first to protect evidence continuity.

Where RegTech projects fail in the first 90 days#

Most early failures come from weak foundations, not weak features. In the first 90 days, teams that launch on assumptions instead of evidence and clear ownership usually create avoidable rework.

Split ownership is the first failure mode. When no single decision owner is accountable for closure, critical workflows can stall. Before you launch, define one owner per workflow, one escalation path, and one closure rule.

An unclear problem statement is the second failure mode. If the team cannot answer what specific workflow is being improved and for whom, handoffs and priorities drift. Use a hard gate: trace one representative case end to end and confirm each handoff and decision point is explicit.

Skipping operational-readiness checks is the third failure mode. Teams may collect information, but without clear prelaunch requirements, later review can expose gaps. Set a prelaunch checklist with required evidence, decision rationale, and a timestamped record.

| 90-day stage | What to lock down | What breaks if skipped |

|---|---|---|

| Days 1-30 | Foundation and market discovery: a clear problem statement, ownership, and evidence-backed assumptions | Scope debates and unresolved decisions |

| Days 31-60 | Workflow validation and decision rules across the process | Avoidable rework and prolonged firefighting |

| Days 61-90 | Operational readiness and organizational clarity before scaling | Execution pressure exposes foundational gaps |

If ownership is unclear, the workflow definition is vague, or assumptions are untested, pause expansion and fix those gaps first. The first 90 days are about operational readiness and organizational clarity under pressure.

What to verify before you trust a vendor claim#

Treat every claim as unproven until a live proof test shows a complete case trail and clear scope limits.

Start with one transaction and trace it from intake to decision to export in a single session. Require the reviewer to show the case record, CDD notes, AML actions, approver history, status changes, timestamps, and final export output. If any part depends on side notes or manual reconstruction, the claim is not validated. Next, force boundary clarity before you discuss fit.

| Claim area | What to verify live | Red flag |

|---|---|---|

| End-to-end trace | One case from intake to export with CDD, AML actions, approvals, and timestamps | Full chain cannot be produced from the case record |

| Jurisdiction handling | Clear split of what is native, configured, or manual across the jurisdictions and programs you operate | Universal coverage is claimed without documented limits |

| FEIE handling (where supported) | Qualification checks are explicit, excluded income is still reported on the return, and current-year limits are handled (for 2026: $132,900 per person) | FEIE is treated as automatic with no qualification gates |

| FBAR value handling (where supported) | Maximum account value method, Treasury rate conversion for foreign currency, and rounding up to whole U.S. dollars | Conversion or rounding method is unclear or inconsistent |

| Tax-document handling (where enabled) | How FEIE/FBAR-related tasks, exceptions, and reviewer notes are tracked | Coverage is promised but exception and review states are not visible |

Use one edge-case drill, not just the happy path. For FEIE, test a case where minimum time requirements may be waived because someone had to leave a foreign country due to war, civil unrest, or similar adverse conditions.

Close with a written boundary list: what changes by market or program, and what still requires custom policy or manual review. If a vendor cannot pass the live trace and an edge-case tax drill, do not treat the claim as validated.

Compliance artifacts your team should export on demand#

Export readiness means you can pull four complete bundles from one case record on demand, without manual reconstruction. If any bundle still depends on chat notes, spreadsheets, or side files, that is an execution gap.

Keep one consistent record trail across all bundles, including timestamps, reviewer identity, and status history, so legal, finance, and compliance can review quickly.

Minimum export set#

| Bundle | What to export |

|---|---|

| Case file bundle | Core case intake and review records, plus decision times, reason codes, status changes, and overrides. Include intermediate holds, reopens, and handoffs, not only the final decision. |

| Regulatory bundle | Program-specific reporting outputs required by your policy, including reporting period, legal entity, submission status, and traceable case references. |

| Tax bundle | FBAR and FEIE tracking artifacts when enabled. For FEIE, keep qualification path and qualifying-day count; FEIE applies only to qualifying individuals with foreign earned income, and the annual cap must be adjusted for partial-year qualification (for example, 2026: $132,900 per person). For FBAR, keep each account maximum separately, apply Treasury year-end conversion for non-USD accounts, round up to whole U.S. dollars, and record 0 if a computed maximum is negative. |

| Incident bundle | Exception history for delayed or blocked workflows, including detection time, remediation actions, owner changes, customer communications, and final disposition. |

Verification checkpoint that catches weak tools#

Run a recurring spot check on closed and blocked cases. Generate all four bundles and confirm that timestamps, reviewer actions, and status transitions reconcile across outputs.

When FEIE waiver handling appears, verify that the record captures the adverse-conditions basis and the IRS annual bulletin period used for the decision. When FBAR values appear, verify separate per-account valuation and year-end conversion handling.

Teams often fail here by exporting summaries without method fields. That may satisfy routine reporting but break under audit follow-up. If full bundles cannot be produced in one pull, fix exports before scaling. Related: How to Automate Your Freelance Tax Preparation.

Rollout sequence that reduces risk without slowing growth#

Use a three-phase rollout with fixed checkpoints. Stabilize core controls first, add tax and reporting depth second, and optimize speed only after evidence quality is consistently reliable.

| Phase | What to do | Checkpoint |

|---|---|---|

| Phase 1, control stability | Define escalation owners and reason codes for include, hold, and exclude outcomes on foreign-asset reporting cases. | Do not expand automation until exception aging is stable across weekly reviews. |

| Phase 2, tax and reporting depth | Add tax and reporting layers only after Phase 1 is predictable. | For U.S. foreign-asset reporting, use Form 8938 as a checkpoint: reporting is threshold-based, it must be attached to the tax return, and there is no universal threshold. |

| Phase 3, throughput and experience | Improve handoff speed and user experience only after traceability is stable. | Preserve decision history, status changes, and reviewer attribution. |

In Phase 2, remember that thresholds vary by filer context, with higher thresholds for joint filers and taxpayers residing abroad.

Form 8938 details are practical rollout guardrails. The often-cited $50,000 figure is only an example for certain taxpayers, not a universal rule.

Form 8938 reporting applies to tax years starting after March 18, 2010. Most individuals began filing with the 2011 return cycle, and certain specified domestic entities entered scope for tax years beginning after December 31, 2015. Filing Form 8938 also does not remove separate FinCEN Form 114 (FBAR) obligations when they otherwise apply.

- Weekly exception aging review: Track unresolved Form 8938 determination cases by age and cause. If backlog growth persists, pause new automation and clear decision debt first.

- Monthly evidence-sample audit: Sample filed and held cases and confirm threshold rationale, filer context, and return-attachment status. Separately verify whether FinCEN Form 114 (FBAR) is still required in those cases.

- Quarterly scope review: Reconfirm which filer contexts and tax years are in scope, and adjust for continuous-use Form 8938 and instructions updates before scaling further.

Country and program variation checks you must confirm#

Before launch, confirm country, entity, and program variation. If it is not explicit, do not roll out.

Oversight is increasingly data-driven, with more detailed and frequent requests, and regulatory alert volume grew from about 8,700 in 2008 to more than 64,000 in 2021. That is why copied configurations can break down: they can create repeat exceptions across onboarding, monitoring, and reporting.

Pre-launch variation map#

Build one map per new route or entity, and treat missing evidence as a launch blocker.

| Check area | What to confirm before launch | Red flag |

|---|---|---|

| Rule applicability by route and entity | Do not assume uniform applicability. Record, by route and entity, which obligations are in scope and who approves them | One global rule sheet reused without route or entity signoff |

| Product-enabled vs policy-enabled controls | Separate product capability from policy dependency and assign an owner for each dependency | A product toggle is treated as full compliance coverage |

| Segment-specific tax and reporting scope | Keep separate rows for each audience segment and tax/reporting workflow in scope, with status per row | One template reused across segments without review |

| Data-request readiness | Define required fields and extraction cadence for recurring regulator or partner requests | Responses depend on ad hoc cleanup |

Tool coverage varies by design focus, and adoption still requires coordinated action across teams. Use the map to force aligned signoff before launch, not after exceptions start.

Do not assume list#

Document every dependency marked with uncertain language before rollout.

- Any item marked

where supportedmust include the exact market and entity list. - Any item marked

when enabledmust include feature name, owner, and activation status. - Any control exception path must include an escalation owner.

- Any tax or reporting workflow row must include audience segment and current status.

- Any unresolved interpretation should block rollout until an owner signs off.

Conclusion and next step#

RegTech is defensible only when controls, evidence, and daily execution stay reliable as rules and communication channels change. Buying software is not the moat. Dependable operation under change is.

The pressure is persistent: estimates place 10%-15% of financial-services headcount in compliance and risk, and investment-bank compliance/control spend has reportedly tripled since 2008. Supervision complexity is also rising as communication tools multiply, while many firms still report archiving and recording gaps.

Next step: run the compliance moat test on your current stack and identify the first broken checkpoint. Start with evidence integrity before adding automation. If you cannot trace decisions with complete capture, archiving, retention, supervision, auditing, and e-discovery records, fix that gap first. Keep human review in AML and KYC decisions instead of assuming full automation is safe.

Use this final selection checklist before choosing a vendor:

- Confirm table stakes: core compliance and risk controls are active, with clear ownership and accountability.

- Verify exportable artifacts: required evidence can be produced on demand without manual reconstruction.

- Validate coverage boundaries: each claimed capability has clear scope and approval ownership.

- Check channel coverage: voice and text records are governed consistently for retention, supervision, and audit access.

- Test change resilience: run a rule-change scenario and confirm execution stays stable before scaling.

Frequently Asked Questions

What is RegTech competitive advantage in one sentence?

It is the ability to meet increasingly stringent, data-driven compliance demands with consistent execution and defensible records as complexity grows. In practice, you can produce clear compliance evidence on demand instead of rebuilding it under pressure.

When does RegTech become a moat instead of just another tool?

It becomes a moat when compliance execution stays stable as rules change, instead of turning every update into manual rework. If evidence continuity breaks each time requirements shift, you have software spend, not defensible capacity.

What are the top failure points in RegTech adoption for small teams?

Common risk areas are unclear ownership, weak long-term regulatory planning, poor visibility into system risk, and weak control of third-party dependencies.

What are the true table stakes in a credible RegTech setup?

Table stakes are reliable compliance and risk controls, streamlined reporting, clear accountability, and the ability to answer data requests without ad hoc cleanup. A practical test is whether you can quickly export complete compliance records without manual reconstruction.

Which metrics matter most when ROI benchmarks are inconsistent across vendors?

Use internal metrics you can verify: time to implement regulatory changes, reliability of reporting responses, manual rework volume, and unresolved dependency issues. These measures show whether execution is improving or hidden operational load is growing.

How should buyers compare integration effort versus compliance control depth?

Score both directly for your highest-priority obligations, include system and third-party dependency complexity on the integration side, and choose the option that meets required control depth with the lowest operating drag. Then validate that score in an end-to-end trace from intake through reporting output.

What should I confirm first when rules vary by country or program?

Confirm applicability by country, entity, and program before rollout, and treat unknowns as blockers until clarified. Then verify which requirements are product-enabled versus policy-dependent, with explicit ownership for each dependency.

Try a related tool

Connor writes and edits for extractability—answer-first structure, clean headings, and quote-ready language that performs in both SEO and AEO.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Taxes in Germany for Freelancers and Expats

Low-stress compliance in Germany comes from decision order, not tax tricks. Use this sequence: confirm core facts, apply conservative temporary assumptions, verify the few points that can break invoices or filings, and keep one evidence file that explains each decision.

How to Automate Your Freelance Tax Preparation

**To automate freelance taxes safely, automate the boring mechanics and keep human approval for the decisions that create real compliance risk.** You are the CEO of a business-of-one. Your job is to run a system that stays resilient while your clients, tools, and countries change.

Singapore EntrePass Timeline for Foreign Entrepreneurs

Treat the Singapore EntrePass as a work pass decision first, not a paperwork sprint. It is described as a work visa for foreign entrepreneurs, innovators, and experienced investors who want to start and run a business in Singapore, and foreign professionals need a valid work pass before starting work there.