Quick Answer

Yes, a razorpay moneylender review should be handled as a risk-screening exercise, not a final verdict. The article does not confirm a clearly documented standalone product for that label, so the practical approach is to verify naming and scope in your own account records, run small live invoice tests, and track support-response timestamps before scaling. Keep early exposure capped and maintain a fallback route until reliability is repeatable.

Who Razorpay MoneySaver Is Best For#

This review is a cashflow decision, not a popularity contest. Treat every claim as provisional, and verify it with live transactions and support records before you route meaningful invoice volume.

Start with naming clarity. Razorpay does publish educational material explaining lending, lenders, and commercial lending, including repayment with interest and creditworthiness checks. That helps with terminology, but it does not prove how any specific payment setup will perform.

Label confusion is part of the risk. In this evidence set, Razorpay MoneySaver appears as an article title on a Razorpay tag page that shows three Razorpay-tagged posts. In practice, start by testing observable product behavior. Raise confidence only when scope is explicit in your account documents and dashboard behavior.

Freshness matters. Related pages in this search space include dates as far apart as Jan 09, 2020 and Sep 26, 2025, so keep a dated evidence log and re-check assumptions before each decision to scale. The date spread alone does not prove anything is wrong, but it does show how old assumptions can outlive their shelf life.

Use this method throughout:

- Treat third-party review platforms as separate signal pools.

- Log each note as

claimandcashflow risk if wrong. - Add one verification checkpoint per claim, such as a live transaction test or support-response timestamp.

- Define one failure mode per checkpoint, such as unresolved ticket loops or unexpected behavior after onboarding changes.

Keep your log simple enough to maintain under pressure. If evidence is too hard to record during a real incident, it will be missing when you need it most. A short, repeatable log beats a perfect template that never gets filled.

If the name stays fuzzy, skip the branding debate. Run a small pilot, cap early exposure, and decide from evidence you can reproduce.

What the keyword means and what is still unknown#

The evidence here does not establish a clearly documented, standalone product tied to this exact keyword. What it does show is broader digital-lending risk, so treat the label as unverified until identity and scope are explicit in your own records.

The strongest concrete signal is a reported case in an article dated MAY 30, 2023. It describes a one-click loan with a 60-day repayment window, a requested 15,000 rupees, and a 9,000-rupee disbursal after a stated 6,000-rupee processing fee. The same account describes repayment pressure starting on day six. Use this as a risk pattern to watch, not as proof about any specific provider.

A second anchor is the January 2024 listing titled Digital Lending in India: The Loan Trap (DOI 10.2139/ssrn.4681458). This shows at least one research listing on the topic, but it does not by itself answer product-level questions. One provided PDF source was blocked at access time, so this evidence set is incomplete.

Terms like Payment Gateway, Chargeback, and KYC are not defined in this evidence set. Do not treat any claim as decision-grade until you can pin each term to provider documentation or a written support response.

Use this checkpoint sequence before trusting the keyword:

- Confirm identity: record the exact product name shown in dashboard, onboarding emails, and terms pages on the same date.

- Confirm scope: separate lending-related claims from payment-collection claims.

- Confirm evidence quality: label each note as anecdote, listing, or direct product documentation.

- Confirm uncertainty: where evidence is missing or blocked, mark it and limit exposure until verified.

A practical rule: if two documents use different names for what appears to be the same feature, treat the difference as unresolved until support clarifies it in writing. If support cannot clarify, keep that feature out of your scale decision and evaluate only what your live tests prove.

How to read conflicting reviews without getting misled#

Conflicting public reviews are screening input, not proof. If labels are mixed, a blended score can hide real risk signals.

| Field | What to record |

|---|---|

| claimed strength | Exact wording, with date and platform |

| observed failure mode | What would block collections if the claim fails |

| verification checkpoint | One live test tied to an invoice ID or support ticket ID |

| evidence pack | Screenshot reference, first-contact timestamp, last-reply timestamp, and final status |

The context here is broad, not platform-specific: BFSI is described as increasingly complex as technology, regulation, and customer expectations keep shifting. In that environment, review narratives can disagree without giving you a decision-grade answer on their own.

Keep each review platform as a separate evidence stream and avoid collapsing them into one score. For claims about customer service, holds, or transaction reliability, log the four fields shown above.

This evidence set does not provide verified ratings, complaint counts, or service benchmarks for Trustpilot, Capterra, G2, or Software Advice. Treat platform mentions as hypotheses, then confirm or reject them in your own pilot.

When signals conflict, prioritize downside risk over convenience. Easy onboarding should not outweigh payout blockers that you verify in your own tests.

You can make this practical by assigning each claim a single decision tag: test now, watch, or ignore. Claims tied to payout timing are test now. Claims tied to convenience can wait until reliability risk is cleared. This keeps your test queue focused when time is limited. If you want a quick next step, Try the free invoice generator.

Table-stakes checks any credible payment setup must pass#

Use this as a go/no-go baseline: do not scale invoice volume until you have verified coverage, onboarding, live payment flow, and dispute handling in your own records. Public reviews can suggest what to test, but this evidence set is broad BFSI context, not provider-level operating proof.

Two grounded signals support a stricter baseline. A November 2025 BFSI reference describes a sector reshaped by technology, regulation, and changing customer expectations. A separate January 2024 listing, Digital Lending in India: The Loan Trap (DOI 10.2139/ssrn.4681458), indicates recent digital-lending analysis in this environment. Treat checks as date-stamped and repeatable, not one-time screenshots.

| Check area | What to verify in writing | Live checkpoint | Failure mode to log |

|---|---|---|---|

| Collection coverage | Payment methods relevant to current clients | Test each needed method with a real invoice reference | Client cannot pay through an expected method |

| Onboarding readiness | Onboarding requirements, blockers, and next steps | Track submission-to-activation timeline | Activation pauses without a clear next step |

| Core collections path | Core payment flow tied to invoice references | Run an end-to-end live path and record status events | Payment completes but status trail is incomplete |

| Dispute handling | Dispute process, required inputs, and update path | Submit a controlled support query and track response path | Dispute handling remains unclear when time-sensitive |

Use the table as a sequence, not a menu. Coverage first, onboarding second, collections path third, and dispute handling fourth. If you skip that order, you can pass a later check while still failing a basic earlier one.

For each row, define who confirms the check and where evidence is stored. Ownership matters because vague responsibility is how test results fail to inform scale decisions. A check is only complete when the evidence is recorded, reviewed, and accepted against a pass condition.

If any block remains unverified, keep volume capped and run another test cycle. Convenience claims can wait; verified behavior on your invoices is the signal to expand.

Build your go no-go scorecard before you move volume#

Use a weighted scorecard before scaling. Table-stakes checks tell you a provider can run, but they do not tell you how much cashflow risk you are routing through it.

Keep the scoring date-bound. A September 2021 EY snapshot described India payments as still being disrupted, with continued fundraising and revenue growth at that time, so older impressions should not be treated as permanent truth. Re-score on a recurring cycle using the same tests and evidence format.

| Risk area | Weight | What earns a pass | What fails the gate |

|---|---|---|---|

| Payment success consistency | 30 | Stable completion across your required payment paths | Repeated drop-offs or unexplained status gaps |

| Hold probability | 25 | No surprise holds at pilot volume, or clear release logic in writing | Unexpected holds without clear release criteria |

| Support responsiveness | 20 | Time-stamped replies and a clear closure path on test tickets | Long silence, circular responses, unresolved ownership |

| Dispute recovery | 15 | Clear accepted evidence list and predictable status updates | Ambiguous evidence requirements or stalled dispute status |

| Onboarding friction | 10 | KYC and activation steps complete without repeated rework | Repeated document loops that delay go-live |

If you reference Trustpilot, G2, Capterra, or Software Advice, use them to shape tests, not to replace tests. For each risk area, log one checkpoint and one failure mode. Then attach the matching evidence trail: invoice ID, payment method, first and final status timestamps, ticket ID, response timing, closure note, and required dispute documents.

Make the scorecard hard to game. Do not count a check as pass if the issue closed without a clear reason, or if status changed without confirming the underlying problem is gone. A closure note that cannot be validated in a follow-up transaction should be treated as pending, not resolved.

A tie-break rule also helps when scores are close. If two options are similar on top-line score, choose the one with cleaner evidence quality and fewer unresolved exceptions. Cleaner evidence reduces decision risk when conditions change and you need to re-evaluate quickly.

Until support quality is proven in your own account, cap early volume and keep a backup payment gateway live. Do not approve full rollout until your minimum score is cleared repeatedly with consistent evidence. Related: A Guide to Tax Residency in Australia for Digital Nomads.

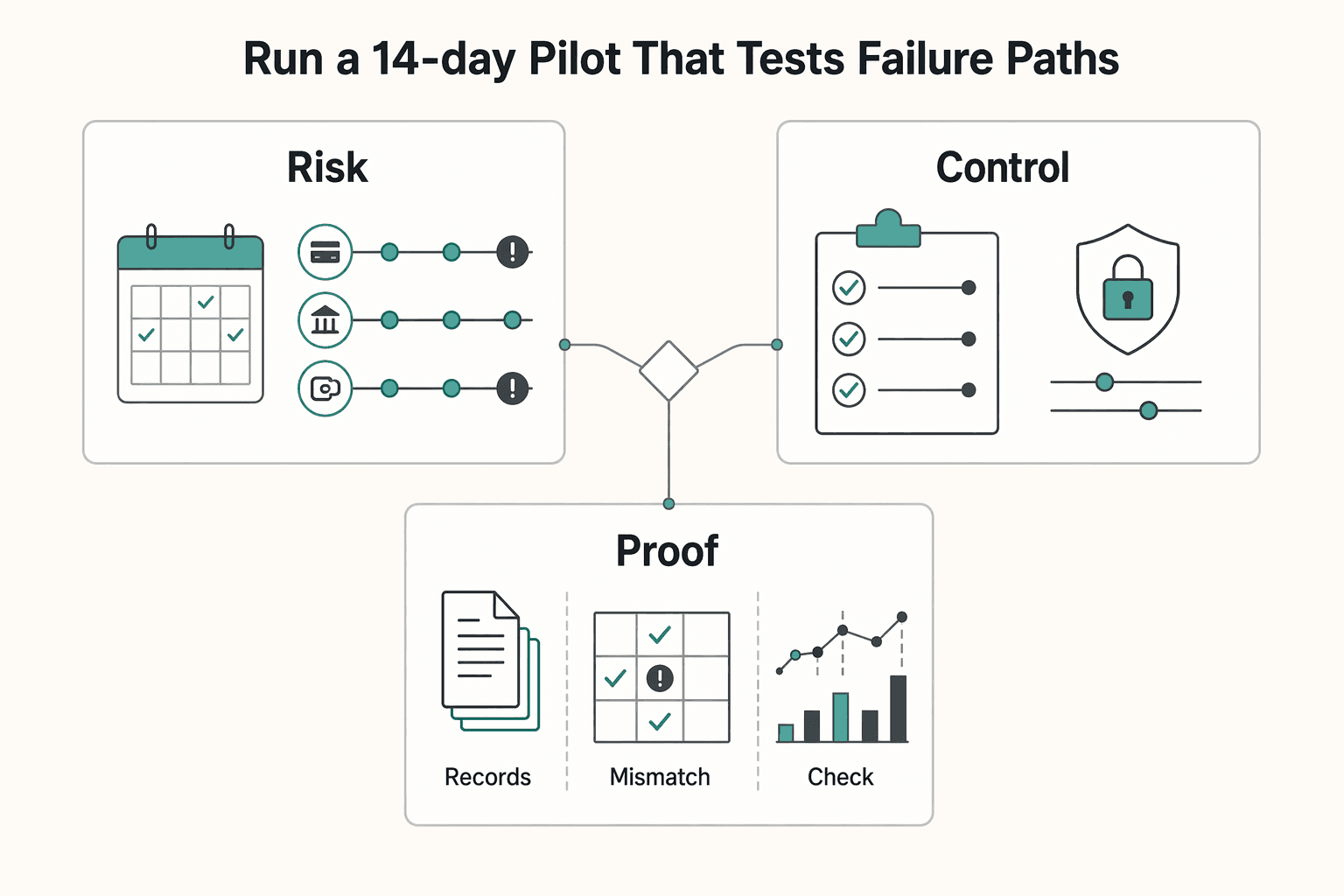

Run a 14-day pilot that tests failure paths, not just happy paths#

Treat the pilot as a stress test for payout reliability, not a demo of successful checkout. These materials do not validate one fixed pilot length, so set a short time box that fits your risk and volume. The decision at the end is simple: scale, keep volume limited, or pause.

In the first phase, run low-risk invoices across more than one payment method on different days. Record each status transition from initiation to final state so you can see where timing or state changes break.

In the second phase, test support under pressure with controlled cases and edge-case transaction queries. Ask for the owner, next action, and closure condition so you can assess whether issue handling is clear or circular.

Keep one compact evidence pack for each test:

- Invoice ID

- Payment method

- First status timestamp and final status timestamp

- Support ticket ID and handoff notes

- Final resolution note

Add a brief review at the end of each phase. Compare what you expected with what actually happened, then decide what must be retested next. This helps you avoid a common failure mode where teams finish a pilot with raw logs but no clear interpretation.

Use a clear internal expansion gate defined before the pilot starts. If unresolved reliability issues persist, keep new routing limited and continue with your fallback path until closure is documented and subsequent transactions look stable.

Spot red flags early before they become cashflow damage#

Use this step to turn pilot data into routing decisions. A red flag is not commentary. It is any issue that can affect payout access, timing, or reconciliation.

Public reviews can still help, but only as hypotheses. In a BFSI environment where technology, regulation, and customer expectations keep shifting, signal quality matters more than headline sentiment.

Run one weekly screening pass and store findings in the same evidence pack format used in your pilot:

- Cross-source repeat: the same issue theme appears in more than one review source.

- Concrete event: the report names a specific failure point, not a generic complaint.

- Time anchor: the issue is recent enough to influence current routing.

- Internal match: you can map the claim to your own invoice IDs, ticket IDs, timestamps, or closure notes.

Keep compliance requests in a separate risk lane so friction is visible early. Track request date, submitted document, current status, and owner for each step. If an open compliance item starts affecting expected payout timing in your cash calendar, pause expansion and route fresh invoices through your fallback path until closure is documented.

Compare marketing claims against pilot outcomes each week. If support is described as responsive but your own tickets show unclear ownership or unresolved closure notes, treat that gap as a risk signal until your evidence improves.

Set one hard threshold in writing. If unresolved operational incidents cross that threshold in a month, freeze new routing on that rail. Keep fallback routing live until the next month closes without carryover issues.

Do not wait for a dramatic failure before acting. Small repeats often signal larger reliability problems. A delayed closure note, a ticket handoff with no owner, and a status reversal in the same week may look minor in isolation, but together they can justify keeping volume split until consistency returns.

Handle holds disputes and payout delays with a fixed escalation sequence#

Contain holds and payout delays with one internal escalation sequence and one accountable owner. This helps keep a single issue from becoming a broader cashflow problem.

Treat this as your internal escalation method, not a provider policy. In this source set, available material is either access-gated, blocked by security checks, or non-procedural conference content, so provider-specific dispute rules are not validated here.

- Confirm transaction status first: log invoice ID, payment ID, current status, first timestamp, latest timestamp, and payout state in the dashboard.

- Collect invoice proof second: keep the issued invoice, payment confirmation, and relevant status screenshots from the same time window.

- Compile a communication timeline third: record ticket IDs, response times, handoffs, and promised next steps in order.

- Escalate once with one evidence bundle: request a named owner, the current blocker, and the exact closure condition.

For chargeback or reversal cases, keep an internal dispute pack ready. Required evidence varies by provider, and this source set does not validate provider requirements:

- Contract scope tied to the billed milestone

- Delivery proof with date and version marker

- Invoice terms covering payment and acceptance conditions

- Client acceptance or approval messages

Keep the escalation language direct and testable. Ask what is blocked, what action is needed, who owns that action, and how closure will be confirmed. Vague responses are not enough when payout timing is at risk.

If a case is still unresolved by your next planned payout date, document the risk, confirm current options with the provider, and make any routing changes only under your internal approvals.

Cross-border reality for Indian freelancers and small teams#

For cross-border invoices, prioritize operational reliability first: predictable settlement, clean reconciliation, and complete records. Checkout acceptance alone may not be enough to choose your primary rail.

Separate acceptance from settlement in your evaluation. A payment can be accepted while payout clarity or verification steps are still unclear, so score each lane on settlement predictability and documentation effort before scaling.

Do not generalize from one successful invoice. Verify each lane with current evidence inside your own account before treating it as repeatable.

Use this distinction: acceptance answers whether a client can pay now, while settlement and reconciliation answer whether you can trust that rail for ongoing billing. Treat settlement and reconciliation as a separate risk check.

Confirm safely before scaling#

- Written support confirmation for your exact scenario, saved with ticket context.

- Current dashboard behavior captured in the same session, including statuses, payout views, and verification prompts.

- One low-value live test logged end to end with timestamps, status movement, credited amount, and reconciliation notes.

If support guidance and live behavior conflict, pause that lane and keep routing through your backup path until the conflict is resolved in writing. Before naming a primary rail, compare expected net receipts against rework effort using your own baseline.

Contract and invoice terms that lower payment risk before checkout#

Contract and invoice clarity can reduce avoidable confusion before a payment request is sent. Payment friction often shows up when scope language and invoice language are not aligned.

Your payment review should include this layer because process reliability alone will not fix unclear terms once a dispute begins. Recovery is usually easier when the record clearly shows what was agreed and what was billed.

A simple test before sending each invoice: could a neutral reviewer read your contract, invoice, and approval trail and reach the same interpretation of what is due? If not, tighten the wording first and send later.

Define terms that can be audited#

Use plain language for the core terms in each statement of work. Keep terms specific enough that a neutral reviewer can match the contract and invoice record without guesswork.

Before you send a payment request, confirm the record for that milestone is complete:

- Written scope reference for the billed milestone

- Invoice details for that milestone

- Dated client confirmation

- Payment request date and amount

- Delivery record with version/date details

Structure invoices for recoverability, not convenience. Breaking work into clearly defined milestones can make later review easier than one large end-of-project bill, and documented checkpoints between stages can reduce confusion.

When terms drift, risk usually increases. If scope changes are not reflected in the written record, routine delays can become disputes about what was authorized. Keep changes and approvals aligned before the next bill goes out.

If a client asks for terms you cannot support, reduce exposure before sending the payment request. Adjust the commercial structure where possible. If alignment is still not possible, narrow scope or decline the engagement.

Your 30-day rollout checklist for a reliable get-paid system#

Use a staged 30-day rollout with fixed internal gates. Scale only when your own records show stable operations, and pause when evidence quality or issue handling slips.

Before Week 1, define pass/fail criteria in writing so decisions stay evidence-based under pressure. Keep the criteria visible to everyone involved in billing, support follow-up, and reconciliation so judgment does not shift between teams.

Week-by-week execution#

- Week 1 setup: Complete required account setup tasks, map the transfer methods you need now (for example UPI/IMPS where applicable), and set primary plus backup processing paths.

- Week 2 controls: Set an incident log template, assign escalation owners, and standardize one evidence pack format for issue review.

- Week 3 validation: Run controlled pilot volume, then compare ticket closure behavior and unresolved issues against your go/no-go scorecard.

- Week 4 scale decision: Expand only if your operational metrics pass the scorecard; if not, keep volume split, remediate, and re-test.

Keep lending claims separate from payment-flow validation. Figures such as ₹1,000-₹50,000 amounts, 7-30 day tenures, or instant-to-15-minute approvals are payday/salary-advance lending terms and should not be used as payment-system reliability benchmarks.

Close the 30-day cycle with a written decision note. Record what passed, what failed, and what must be retested before the next scale step. This creates continuity, especially when responsibilities shift or when you need to explain why volume stayed capped.

Conclusion#

Use mixed ratings as a prompt to investigate, not as a decision rule. Protect cashflow with repeatable checks tied to your own logs, and scale only when those checks keep passing under real invoice volume.

When product labeling around lending remains unclear, do not assume scope. Lending has specific mechanics: money is provided with expected repayment plus interest, and approval typically includes a creditworthiness check. If a flow does not clearly show borrower assessment criteria, identity detail capture, or lending terms, treat lending claims as unverified and evaluate the payment behavior you can confirm.

Keep expansion decisions on a short scorecard. Use these checkpoints:

- Verification checkpoint: for lending-style flows, confirm whether the application requests core identity details and whether AML screening against sanctions, watchlists, or PEP lists is part of review.

- Reliability checkpoint: for collections, log invoice ID, payment method, settlement timestamp, ticket ID, and closure note so you can reconstruct exceptions.

- Failure trigger: if unresolved support cases or reconciliation gaps repeat during the pilot, pause new routing on that rail and move fresh volume to a backup.

- Scale gate: increase volume only after prewritten pass criteria hold across repeated review cycles.

Weight evidence quality before you trust external narratives. A user-uploaded, AI-labeled document is weak support compared with documented product behavior and your own records. Missing critical API capabilities can reduce completion before an application is submitted, so conversion risk can appear before credit risk.

The practical win is disciplined execution: run a controlled pilot, keep a live fallback rail, and treat ambiguous product labels as a risk signal until documentation and live results align. If you only keep one habit from this review, keep a dated evidence log and require written closure before each expansion step.

Frequently Asked Questions

Is Razorpay good or bad for freelancers in 2026?

This evidence set does not support a universal good-or-bad verdict for freelancers in 2026. Treat it as a fit decision based on your own pilot records, and scale only when your internal results are stable under real usage. A practical interpretation is to avoid binary labels and rely on repeatable internal evidence. If your results stay consistent, continue testing in stages; if they drift, limit exposure until stability returns.

Why do Razorpay review scores differ so much across Trustpilot, Capterra, G2, and Software Advice?

This grounding pack does not include verified cross-platform score comparisons, so it cannot explain those differences with confidence. Use external ratings as directional signals, not final proof, and verify recurring complaints against your own records before changing routing decisions. Without verified comparison data here, treat each platform as a separate hypothesis to test against your own incidents and timestamps.

What are the biggest risks I should test before routing most client invoices?

From this pack, the clearest risk checks are whether your flow can verify identity, fetch credit data quickly, move money securely, and flag fraud. For lending-style decisions, confirm creditworthiness checks are explicit before approval. Razorpay’s lending explainer also points to core screening inputs: credit score, income, and debt-to-income ratio. Keep those lending checks separate from payment-collection performance when deciding how much volume to route.

How do I evaluate a “razorpay moneylender” claim when product-level details are unclear?

Start with definitions: lending is providing money with expected repayment plus interest, and a lender assesses creditworthiness before approval. The same source lists credit score, income, and debt-to-income ratio as assessment inputs. If those mechanics are not clearly documented, treat the claim as unverified until written scope and criteria are provided. Keep naming and behavior checks separate. A label may sound clear while product scope is still vague; until written scope and live behavior line up, keep lending claims outside your rollout decision.

What is the minimum pilot I should run before full rollout?

No source here validates a universal minimum duration or numeric cutoff. Use a staged pilot with pass/fail rules set in writing before launch. Expand only after repeated cycles meet your internal reliability standard. The duration is less important than the quality of evidence you collect during the pilot.

When should I switch or add a backup payment provider?

These excerpts do not provide one validated switch threshold, so set your own triggers in advance. Move new volume to a backup when your internal incident or risk thresholds are exceeded, and return volume only after closure is documented and the next review cycle passes. Document the switch trigger before incidents happen so decisions remain consistent across billing cycles.

Try a related tool

Ethan covers payment processing, merchant accounts, and dispute-proof workflows that protect revenue without creating compliance risk.

Sources

Includes 3 external sources outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

Indian Freelancer Payment Analysis That Protects Net INR

For freelancers in India, the number that protects cash flow is the net INR credited to your bank, not the USD amount on the invoice. Start from that outcome and work backward through every payment decision.

How to Build a Predictable Content Strategy for Your Agency

If your calendar is full but your pipeline signal is weak, you do not have a posting problem. You have a decision problem. Predictable growth comes from a small set of repeatable choices about what to publish, why it matters, who owns it, and how you will judge whether it helped lead qualification.

Australia Tax Residency for Digital Nomads With GST and ABN Checkpoints

The goal is a defensible, low-drama position the Australian Taxation Office (ATO) can follow from your records, not a clever workaround. For a digital nomad, that usually means keeping two tracks straight: residency and GST/ABN admin. Consistency is what holds up over time: use real facts, take steps in a clear order, and keep documents that still match months later.