Quick Answer

Start with a capped weekly admin block, then log each recurring non-billable task with one completion artifact and one deadline anchor. For freelancer administrative burden, the practical shift is to measure repeat rework loops and correct them one at a time. Keep legal-risk items on a separate escalation path, and treat payment tasks as finished only when confirmation, cleared status, and invoice reconciliation all align.

The second job freelancers never planned for#

Freelancer administrative burden is the recurring non-billable work required to stay compliant, get paid, and keep records defensible. For a solopreneur, these admin tasks often look like freelance productivity drag, not visible client delivery. The goal is not perfection. It is a repeatable weekly process with a fixed time budget.

Treat this as process design, not willpower. Define each recurring task with two checks: one artifact that proves it was done, and one date that proves it was done on time. If either is missing, the task is still open.

Much policy guidance is written for employers, so it often centers on recruitment, staff appraisal, task distribution, and discipline. Freelancers still need that context, but the decisions here are different: what to document, what to standardize, and what to escalate first.

A common failure mode is trying to run two jobs with one-job planning habits. One side-hustle analysis ties that mismatch to burnout, weaker performance, and abandoned freelance efforts. It also reports about 10% juggling multiple income streams, average side earnings of $891 per month in 2024, and 43% not reaching meaningful scale. Treat those numbers as directional, not as official national benchmarks.

The risk is simple. Gross income can be consumed by the cost of doing business when admin rework compounds. Tighter controls take time now, but weak controls can erode margin later through missed deadlines, duplicate effort, and payment delays.

This article focuses on operating decisions, time-budget rules, and record-keeping standards, not individualized legal or tax advice. If a case becomes jurisdiction-specific or legally ambiguous, escalate to qualified counsel or a licensed tax professional.

Start week one with this baseline:

- Set a fixed weekly admin budget and track actual time against it.

- Define proof of completion for each recurring task before work starts.

- Record one failure mode per task, such as late payment follow-up or a missing form.

- Review weekly and fix the largest repeat rework loop first.

Set one budget response rule before you begin. If weekly admin time exceeds your cap, do not patch five things at once. Instead, pause, identify the single repeat loop creating most spillover, and correct that loop before adding new process steps. This keeps control steady when client load spikes.

If you want a deeper dive, read Automating Your Freelance Finances: A Guide to Tools and Workflows.

Define what counts as admin work before you try to reduce it#

Do not try to reduce admin until you define it. Put every recurring non-billable task into four buckets, then track proof, deadline, and failure signal for each one. Use one template across all buckets so your week-to-week tracking stays comparable.

| Bucket | What belongs here | Proof artifact | Deadline anchor | Failure signal |

|---|---|---|---|---|

| Compliance | Contractor engagement records, contracts, and related status checks | Signed document or completed checklist with date | The date you set for completion in your process | Missing or outdated records while work is active |

| Tax documentation | Tax forms, payer details, and supporting records | Stored form copy plus dated verification note | The date you set for your reporting process | Mismatched details across records |

| Payment operations | Invoicing, payment confirmation, and reconciliation | Sent invoice, payment confirmation, reconciled ledger entry | Invoice due date plus follow-up interval | Overdue invoice with no logged next action |

| Client coordination | Scope clarifications, approvals, scheduling, and decision follow-ups | Written decision trail in email or project notes | Agreed response window or delivery milestone | Delivery blocked because no decision was captured |

Add a second tag for classification exposure. If a task touches worker classification status, tag it and review it separately from routine process work.

Keep the baseline strict. Only recurring obligations belong in your weekly dataset. Put one-off events in an exception log so they do not distort trend lines.

Use this quality gate for every entry:

- Bucket selected, plus whether a classification tag applies.

- One artifact proving completion.

- One deadline anchor for on-time status.

- One failure mode, such as rework, payment delay, or missing documentation.

Mixed tasks need clear handling rules. If one action crosses two buckets, pick one primary bucket for reporting and add the second as a tag. Close the item only after proof exists for both parts. That prevents hidden work from vanishing into generic notes.

At your weekly review, pressure-test the categories with three short questions:

- Which bucket created the most preventable follow-up?

- Which bucket had open items with missing proof?

- Which bucket had items marked done but still blocked delivery?

Those checks keep the taxonomy useful, stop passive tracking, and show where updates are overdue.

That gives you a clearer view of where time is leaking and keeps legal-risk work from being treated like a basic productivity issue.

Build a simple admin time ledger that reveals the real cost#

Track admin time with the same discipline you use for client work. Start with a recurring ledger for non-billable tasks. Log each entry with task type, elapsed time, and downstream impact: delay, fee, rework, or risk.

| Ledger field | What to record |

|---|---|

| Task type | Type of non-billable task |

| Elapsed time | Elapsed time |

| Impact type | Delay, fee, rework, or risk |

| Context note | Where the related note lives |

| Next action | Next action if unresolved |

Log entries close to when the work happens, not at week end. If you already bill in quarter-hour segments, use the same interval here so comparisons stay consistent. End-of-week estimates can miss detail and lead to underbilling or overbilling.

Keep each row easy to review by recording one checkpoint: where the related note lives. If key details are missing, keep the item open until they are added.

Keep the row format short and concrete so updates stay quick even on busy days:

Task typeElapsed timeImpact typeContext noteNext actionif unresolved

Run one weekly review and fix the single biggest rework loop first instead of optimizing everything at once. Use this order:

- Sort tasks by total minutes lost to rework.

- Pick one loop to fix for the next seven days.

- Define one change and one check date.

- Re-measure next week before changing a second loop.

Stick to that sequence in your weekly loop. First diagnose where time is lost, then apply one correction, then verify whether the correction worked. Skipping verification can make the ledger less useful and turn it into another unfinished admin task.

If the same issue appears in consecutive weeks, tighten your done condition. For example, do not mark payment follow-up complete when a reminder is sent. Mark it complete when the next decision is captured, dated, and assigned.

Use the data to set pricing and boundaries, but treat public anecdotes as cautionary examples, not benchmarks. The practical signal is simple: accurate, current records matter more than tool choice.

Separate legal exposure from routine friction so you escalate correctly#

Use your ledger to sort risk, not just time. Treat classification ambiguity as high severity. If a working relationship starts to look inconsistent with an independent contractor setup, flag misclassification risk and route a review instead of routine cleanup.

For U.S.-linked work, record jurisdiction anchors early so routing stays clear. Note whether the issue may involve tax or labor authority exposure, and do not guess jurisdiction-specific tests from memory.

Apply one triage rule consistently. If a task could create penalties, status disputes, or contract-enforceability risk, escalate to qualified counsel. If it is repeatable processing with low legal uncertainty, standardize it.

Make contract quality the first checkpoint. An Independent Contractor Agreement should clearly cover deliverables, invoicing, termination, confidentiality, liability, tax handling, and ownership terms. Recheck these terms before kickoff or renewal, then confirm actual working practices still match the agreement.

When review is needed, use both lenses. Legal review checks exposure and enforceability. Commercial review checks whether scope, payment logic, and delivery terms still work in practice.

Keep a written issue log so legal and operational threads do not blur. Capture:

Date openedand trigger eventCounterpartand roleRisk tag(for example: worker misclassification, payment dispute, contract ambiguity)Jurisdiction anchorwhen relevantNext action, owner, and due dateStatusand closure note with supporting evidence

Once an issue is escalated, prepare a short handoff packet before you send it. Include:

- What changed and when

- Which contract clause or record is affected

- What decision is needed

- What deadline is driving urgency

This handoff can reduce back-and-forth and shorten review time. The reviewer gets facts, not a reconstruction request.

As cross-border work grows, this split matters more. Contractor models can become riskier and less efficient over time, and local scrutiny can increase around tax presence, labor practices, and employment contracts. The operating rule stays simple: escalate legal uncertainty early, standardize repeatable admin work, and document every handoff.

Install a minimum tax and document stack you can maintain#

If you cannot retrieve a complete client record quickly, your stack is too fragile. Use retrieval speed as the test so admin stays routine instead of turning into a filing-season scramble.

For each client and payment flow, keep one consistent packet. It should let you trace the numbers both ways:

- Tax documents and signed records used for that client relationship

- A running payment log tied to your ledger

- The working inputs you rely on for tax prep

- Supporting evidence for each payment: request, proof, and matching ledger record

For cross-border exposure, add a separate monitoring layer. When applicable, Form 8938 is used to report specified foreign financial assets and must be attached to your tax return. It falls under FATCA, and it does not replace FBAR obligations. A person may need both Form 8938 and FinCEN Form 114.

Do not hardcode one threshold for everyone. Higher Form 8938 thresholds can apply in some cases, including joint filers and taxpayers residing abroad, and some tests use year-end versus any-time asset values. Also, if you are not required to file an income tax return, Form 8938 is not required.

The failure mode to avoid is filing on time but being unable to verify numbers quickly. Run a short recurring check that records return-filing status, possible Form 8938 trigger, and possible FBAR trigger. Escalate unclear items to a tax professional before deadlines compress your options.

Run a retrieval drill during your monthly close. Pick one client at random and confirm you can pull the full packet without hunting across tools. If the packet is incomplete or slow to assemble, log the missing piece and fix that storage gap before the next cycle.

Use one naming and dating convention across tax files, payment evidence, and reconciliation notes. Consistent naming does not change legal obligations, but it reduces avoidable errors when you need to defend a number under time pressure.

Fix payment operations that quietly create rework every month#

Recurring payment rework can drop when you run one standard invoice path from issue to settlement and assign a clear owner to every exception state. Without explicit ownership, follow-ups get orphaned and the same problems return next cycle.

| Invoice step | Required action |

|---|---|

| Issue invoice | Issue the invoice with due date and payment method confirmed |

| Capture acknowledgment | Capture client acknowledgment in writing |

| Log initiation | Log payment initiation and reference ID |

| Mark cleared | Mark funds as received and cleared |

| Reconcile ledger | Complete the ledger update with invoice reconciliation |

| Close record | Close the record only after supporting proof is attached |

Run that same sequence every time:

- Issue the invoice only after the due date and payment method are confirmed.

- Capture client acknowledgment in writing.

- Log payment initiation with the reference ID.

- Mark funds as received only after they are cleared.

- Complete the ledger update with invoice reconciliation.

- Close the record only after supporting proof is attached.

Treat paid as complete only when confirmation, cleared status, and reconciliation align. That keeps drift visible before month-end and helps prevent avoidable rework from broken handoffs. If you need a tighter payout-check sequence, use Decoding International Wire Transfers as a practical companion checklist.

The risk is operational, not theoretical. One source notes that a single missed handoff can delay five deliverables, and another describes how waiting 60 days to get paid hurts loyalty. A separate payout analysis describes older batch processing that often took 3 to 5 days to settle, which shows how unresolved exceptions can compound delay.

An end-to-end audit trail helps keep disputes factual. Store timestamped status changes, payout references, and reconciliation notes in one place so you can resolve questions from records instead of memory. Real-time tracking is associated with lower finance and operations overhead, and early-access payout options can improve contractor experience without changing pay terms.

For compliance gates, keep rules conditional and explicit. If a market or payout program has required verification checks, place that gate before payout-related actions and record pass or fail status with date and reviewer. If status is unresolved, hold release and escalate rather than proceed on verbal confirmation.

Keep a visible exception queue with clear states. This keeps items from disappearing between reminders:

- Sent and awaiting acknowledgment

- Acknowledged and awaiting initiation

- Initiated and awaiting clearance

- Failed or returned payment

- Cleared and awaiting reconciliation proof

Attach an owner and next action date to every exception state. If the date passes without progress, escalate immediately instead of creating another reminder loop.

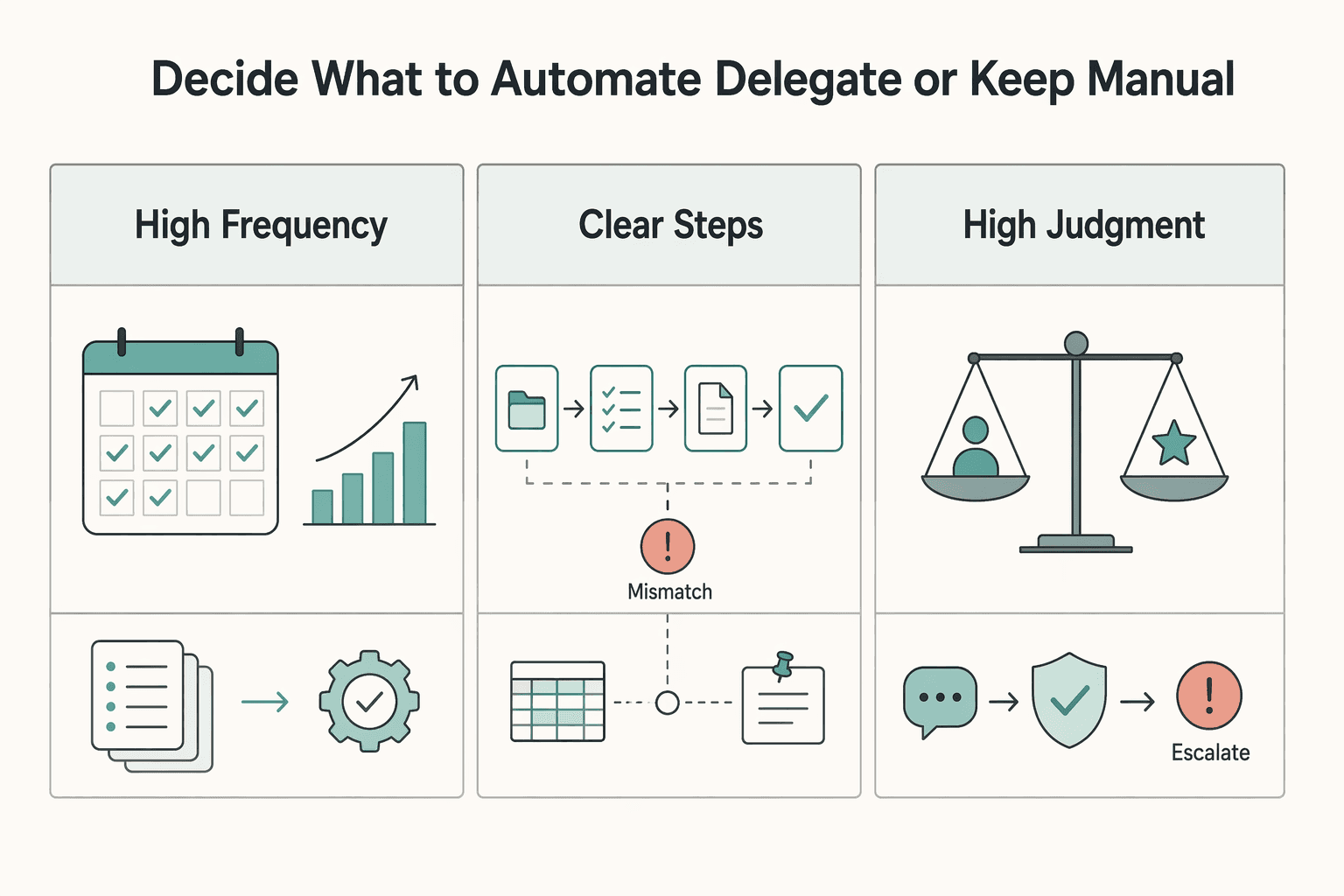

Decide what to automate, delegate, or keep manual#

Route each admin task with one rule: score the downside if it goes wrong, how often it repeats, and how much context it needs, then choose automate, delegate, or keep manual.

Risk shows error cost. Frequency shows where repeated effort creates drag. Context shows how much live judgment is needed for client-specific situations. Using the same criteria each month keeps routing decisions consistent.

| Task profile | Best mode | Control to keep |

|---|---|---|

| High frequency, low judgment | Automate | Keep a simple approval checkpoint for sensitive actions |

| Clear steps, moderate judgment | Delegate | Hand off with a documented checklist and named owner |

| High judgment or high downside | Keep manual | Require direct review before completion |

Automate repetitive, rules-based tasks first. That can reduce admin load while keeping the work consistent. However, keep approval checkpoints for sensitive actions so mistakes do not scale.

Delegate only after the process is written step by step. A documented checklist makes ownership clear and helps reduce rework on sensitive administrative tasks.

If you use a platform, prioritize features that centralize project data, automate administrative tasks, and secure important information.

Add a monthly routing review so task placement stays accurate. Work that starts as manual may become safe to delegate after repeated clean cycles. Work that was automated may need to move back to manual when exceptions rise. The goal is not permanent labels. The goal is matching control level to current risk.

When you delegate, define return conditions. If a delegated task hits ambiguity, missing records, or legal uncertainty, it should come back to the owner with a clear note and attached evidence. That keeps it from stalling in a queue.

Handle cross-border complexity with explicit country and program checks#

Cross-border work needs a hard gate. Do not send the first invoice until your country-and-program matrix is complete and verified. Use it to confirm payment method, documentation, tax steps, and exception handling before launch.

Keep the matrix as a working document, not a one-time checklist. Use one row per country and mark each rule as global default or country/program-specific so assumptions do not spread into the wrong market.

| Control area | What to capture | Verification before go-live |

|---|---|---|

| Payment method | Agreed payment rail and fallback path | Confirm payout path with current provider rules and document the fallback |

| Documentation | Required contract and tax documents | Confirm all required files are collected and retrievable |

| Tax steps | Tax documentation status, IRS documentation needs for U.S.-linked work, treaty relevance | Mark each item as verified, pending review, or not applicable |

| Classification | Local worker status treatment for the engagement | Confirm whether U.S. 1099 contractor treatment applies (U.S. context only) or not |

| Exception handling | Named owner and escalation contact | Confirm who handles failed payments or missing documents |

Keep classification language precise. U.S. freelancers are commonly treated as 1099 independent contractors, but that does not transfer automatically to other jurisdictions. If status is unclear, pause onboarding and escalate before work starts.

Add a payment-data checkpoint. One study summary reports 14% of global payments fail, with an average $12 fee for rejected or repaired payments. It also notes many teams still manually check beneficiary details. Treat those figures as a warning, not a universal constant, and verify beneficiary name and address details before release.

For treaty handling, document a simple yes or no decision on whether treaty relevance exists for this engagement. If U.S.-Canada work is in scope, include a specific U.S.-Canada Tax Treaty relevance line and route unresolved points to qualified tax review.

Use a strict go or no-go rule:

- No first invoice until required documents are complete and retrievable.

- No payout release until primary and fallback payment paths are confirmed.

- No launch if required tax documentation, treaty relevance, or IRS documentation status is unknown where applicable.

- No start if exception ownership is undefined.

Before go-live, run a short scenario check with the responsible owner: one successful payment path and one failed payment path. Confirm who acts first, where evidence is stored, and what escalates. This is not extra bureaucracy. It prevents slow decision-making when the first real exception appears.

If any item is still pending, delay launch. A delayed invoice can be less costly than repeated cross-border failures after delivery begins. Related: A Freelancer's Guide to the US-Canada Tax Treaty.

Run weekly and monthly control points so admin stays bounded#

A fixed weekly and monthly cadence helps keep admin from drifting into billable time. The goal is to catch exceptions early, decide quickly, and prevent repeats.

Weekly control point#

Review three items together each week: admin hours by category, overdue items, and unresolved payment or compliance exceptions. If a category rises, tie it to one process step, one client or country row, and one failure point so the fix stays specific.

Keep a short exception log with an owner, current age, next action date, and blocking dependency. Treat any exception missing those fields as untriaged and assign ownership before new work starts.

Set intervention thresholds in advance, such as repeated missed deadlines or recurring exceptions in the same process step. When a threshold is crossed, make one concrete process change that week and track whether it reduced the next review's exception load.

Close each weekly review with two decisions: what to stop doing this week and what to tighten this week. That helps keep your list from growing without limit and keeps attention on changes that reduce repeat failure.

Monthly control point#

At month-end, reconcile records from invoice through settlement, then verify the cross-border reporting inputs you rely on. For cross-border exposure, review FBAR and Form 8938 trackers only where relevant.

Keep Form 8938 checks precise: it is attached to the tax return, and if no income tax return is required, Form 8938 is not required. Some financial accounts are excluded from Form 8938 reporting, so apply the current instructions when determining what to include. Keep FBAR as a separate track, since filing Form 8938 does not remove a possible FinCEN Form 114 filing obligation. Because Form 8938 materials are updated as needed, confirm you are using current instructions before closing the month.

End each month with a short retrospective note: what increased burden, what reduced it, which decision fixed a recurring issue, and what you will stop doing next month.

Add one continuity check at month-end: Can another trusted person follow your records and understand current status without asking you for context? If the answer is no, your documentation may not yet be defensible enough for disruption or audit pressure.

Watch for red flags that mean stop and escalate#

Use clear stop rules. If an exception could create filing errors or unrecoverable rework, pause and escalate instead of treating it like routine cleanup.

Red flags that require an immediate pause#

| Red flag | Pause trigger |

|---|---|

| Form-attachment risk | Form 8938 may be required but is not ready to attach to the tax return |

| Record-integrity risk | Account records are missing, inconsistent, or cannot support reported values |

| Cross-border reporting uncertainty | You cannot clearly determine whether FATCA-related reporting, FBAR (FinCEN Form 114), or Form 8938 applies for the year |

| Calculation-trail gap | You cannot show how non-U.S. account values were converted to U.S. dollars, rounded up to whole dollars, and sourced |

- Form-attachment risk: Do not file if Form 8938 may be required but is not ready to attach to the tax return.

- Record-integrity risk: Hold filing changes if account records are missing, inconsistent, or cannot support reported values.

- Cross-border reporting uncertainty: If you cannot clearly determine whether FATCA-related reporting, FBAR (FinCEN Form 114), or Form 8938 applies for the year, escalate before filing pressure forces assumptions.

- Calculation-trail gap: If you cannot show how non-U.S. account values were converted to U.S. dollars, rounded up to whole dollars, and sourced, stop at the break point and assign one owner to rebuild evidence.

Pausing should be explicit, not informal. Freeze the affected task, log the reason, assign an escalation owner, and define what evidence is required to restart. Without that restart condition, pauses drift into silent backlog.

Tax checks to verify quickly#

For Form 8938, confirm in writing whether filing is in scope. For certain U.S. taxpayers, one stated trigger is aggregate specified foreign financial assets exceeding $50,000, and if Form 8938 is required, it is attached to the tax return.

Keep FBAR as a separate decision track. Filing Form 8938 does not remove a separate FinCEN Form 114 filing requirement when FBAR is otherwise required.

When FBAR values involve non-U.S. currency accounts, keep the method consistent and documented: convert to U.S. dollars, round up to the next whole dollar, and record the exchange-rate source if you use a verifiable fallback rate. If a computed account value is negative, enter zero for that field.

Set these thresholds in advance so escalation is automatic, not delayed. If a red flag crosses your threshold, pause execution, escalate to qualified support, and log the decision before restarting.

The point is control not perfection#

Control is the goal, not flawless admin. Measurable process rules protect billable capacity better than vague productivity advice by surfacing risk early and making decisions repeatable.

Use the speed-versus-velocity lens when you prioritize. Speed is raw output, while velocity is progress toward your business goal. Fast starts are real in some cases because freelancers can begin immediately. Traditional senior hiring can exceed 60 days. That advantage can fade when follow-up, missing records, and rework consume the saved time.

A major preventable risk is single-person dependency (a bus factor of 1). If status, handoffs, and proof of completion live only in your head, one disruption can stall delivery. Control means a trusted helper can open your records and see current status, next action, and completion evidence without guesswork.

Run a 4-week admin ledger, then keep only what proves useful:

- Track each non-billable task with

task type,elapsed time, anddownstream impact. - Add one evidence checkpoint per task, such as confirmed payment status or matched notes.

- Choose one high-rework process and define its start trigger, handoff point, and done condition end to end.

- Set one stop rule before week one, such as repeated failures triggering a pause and redesign.

After week four, review two outputs: total non-billable hours and repeat-failure count. If hours drop but repeat failures rise, you traded control for speed. If hours stay flat but repeat failures fall, continue one more cycle before expanding changes. Then calibrate your pricing guardrails with How to Calculate Freelance Rate so reduced admin spillover turns into measurable margin.

Use the next cycle to harden what worked. Keep the checks that reduced exceptions. Remove steps that added admin time without improving proof quality or on-time completion.

Keep scope realistic across programs and jurisdictions. Rules and process requirements vary, so disciplined records and clear decision checkpoints help prevent avoidable surprises.

Frequently Asked Questions

What is freelancer administrative burden in practical terms?

It is recurring non-billable work that keeps projects and records in order. In practice, that can include tracking jobs, monitoring progress, and following payment status alongside delivery work. Tasks tied to payment tracking and core recordkeeping are typically part of this admin load.

Why does admin work feel like a second job even when client work is stable?

These tasks recur alongside delivery work. One published example describes compliance, payroll, and HR work as a major drain on time and resources. Because this work sits outside billable delivery but still has to be done, it can feel like a second role.

Which tasks usually consume the most non-billable time each week?

A common recommendation is to focus on status tracking and payment follow-up. One practical option is a single spreadsheet that tracks each job, hours spent, source, stage, and payment status. If you are unsure where time is going, start by reviewing repeated follow-up loops.

How can I reduce admin load without increasing compliance or tax risk?

Start with one clear tracking method before adding new tools. Keep job and payment status current in one place, then review on a fixed weekly cadence. This can improve visibility, but it does not replace country-specific tax or legal guidance.

What should I track weekly to keep admin from spilling into billable time?

One recommended weekly tracker includes jobs, hours spent, source, stage, and payment status. Those fields help you see what is in progress, what is complete, and what still needs follow-up.

What parts of freelancer admin advice are still uncertain or country-specific?

Platform rules are platform-specific, not universal. For example, one marketplace states that users with incomplete profiles cannot bid, but that applies to that platform only. Legal and tax obligations can vary by country and engagement details, so broad advice is only a starting point.

When should I escalate to a tax professional or lawyer instead of troubleshooting alone?

Escalate when a decision could change legal exposure, filing position, or contract terms and the answer is still unclear. Escalate when records conflict and you cannot verify the correct version before a deadline. If two interpretations could lead to different consequences, hand it off early enough for a qualified reviewer to influence the outcome.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

Automating Freelance Finances Without Losing Cashflow Control

You can [automate freelance finances](https://solofinancehub.com/blog/how-to-automate-freelance-finances) and still keep control over key cash decisions. The practical target is simple: automate repetitive admin, then keep human approval for higher-risk exceptions.

U.S.-Canada Tax Treaty Filing Workflow for Freelancers

If you are working through the us-canada tax treaty freelancer question, lock down the facts before you choose forms. That is a practical way to reduce double-tax risk. Confirm residency and work location first, then test what the treaty can and cannot coordinate. The treaty can help reduce double taxation, but it does not erase domestic filing duties.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.