Quick Answer

Choose the FEIE test your records can support end to end. For the physical presence test FEIE route, you need a defensible 330 full days in a 12-consecutive-month window, then matching dates in Form 2555 and the rest of your return. If your life was stable in one country for an entire tax year, Bona Fide Residence may fit better. In either case, confirm foreign tax home separately and fix timeline conflicts before filing.

Start Here if You Want a Low-Stress FEIE Decision#

Start with one principle: choose the FEIE path you can prove, then keep every filing detail consistent with that choice. If you are weighing the Physical Presence Test for FEIE, treat it as a documentation job first and an optimization question second.

Your first gate is eligibility, not strategy. The Foreign Earned Income Exclusion applies only if you have foreign earned income, a foreign tax home, and qualification under either the Physical Presence Test or the Bona Fide Residence Test. A strong day count alone is not enough if tax home facts point somewhere else. Excluded income is still reported on your U.S. return.

Use this sequence before drafting Form 2555:

- Confirm base facts: foreign earned income, foreign tax home, and a clear timeline for the year.

- Test Physical Presence first if your year was highly mobile. Can you document 330 full days in foreign country or countries within any 12 consecutive months?

- If facts are stable in one country, test Bona Fide Residence. Can you support an uninterrupted period that includes an entire tax year?

- Choose the test with cleaner evidence, not the one that looks better in a rough estimate.

Lock one date ledger early to avoid rework. Reconcile passport stamps, entry and exit records, flight confirmations, client invoices, and calendar entries before you complete Form 2555. If day logs and income dates do not align, fix them now. Filing-week fixes are where contradictions show up.

Keep the filing checklist tight:

- One finalized travel timeline for the chosen 12 month window or residence period.

- Proof set for tax home position and work location pattern.

- Form 2555 draft that matches the same dates and narrative used in your records.

- A contradiction scan against the rest of your return.

Escalate early when facts are mixed: multiple country moves, partial travel records, or uncertainty about whether a residence period truly covers an entire tax year. The expensive error is not paying for advice. It is filing a story you cannot defend if the IRS asks for support.

For a quick next step, try the FEIE calculator.

Define the Core Terms Before You Choose a Test#

Before you choose a route, lock the definitions. FEIE is the exclusion mechanism, and qualification runs through either the Physical Presence Test or the Bona Fide Residence Test, with tax home as a separate gate.

| Term | Core rule | Key note |

|---|---|---|

| Physical Presence Test | At least 330 full days in foreign country or countries during 12 consecutive months | Days do not need to be consecutive; this test does not depend on the kind of residence you establish |

| Bona Fide Residence Test | An uninterrupted period of bona fide residence that includes an entire tax year | Residence-status route |

| Tax Home Test | Separate gate | A strong day count does not remove the foreign tax home requirement; intent and purpose of your stay can be relevant |

| U.S. tax residency status | Physical Presence language applies to U.S. citizens and U.S. residents | Resident status tied to Internal Revenue Code section 7701(b)(1)(A) |

To claim FEIE-related benefits, your facts must align on three points: foreign earned income, a foreign tax home, and qualifying status under one of those two tests. Choose the test only after those terms are clear.

- Physical Presence Test: day-count route. At least 330 full days in foreign country or countries during 12 consecutive months. Days do not need to be consecutive, and this test does not depend on the kind of residence you establish.

- Bona Fide Residence Test: residence-status route. An uninterrupted period of bona fide residence that includes an entire tax year.

- Tax Home Test: separate gate. A strong day count does not remove the foreign tax home requirement, and intent and purpose of your stay can be relevant to tax home.

- U.S. tax residency status: Physical Presence language applies to U.S. citizens and U.S. residents, with resident status tied to Internal Revenue Code section 7701(b)(1)(A).

Use Publication 54 as your practical anchor when tax home and residency terms feel close but are not the same. Do not treat the IRS LB&I practice unit excerpt as binding authority; it states that it is not an official pronouncement of law.

Verification checkpoint before moving on: write a short eligibility memo with your tax home facts, U.S. status, and test candidate so the rest of the return stays consistent.

Related reading: The Ultimate Digital Nomad Tax Survival Guide for 2025.

Run a Fast Physical Presence Qualification Check#

Treat this as a strict pass/fail screen: if you cannot document 330 full days in foreign country or countries within any 12 consecutive months, stop here and evaluate Bona Fide Residence.

Ask one question first: can you prove the count with records? The Physical Presence Test is time-based, not a residence-style or intent-based test.

Use this triage before drafting Form 2555:

- Build one travel timeline with exact entry and exit dates.

- Count only full foreign days, and mark every U.S. day.

- Confirm the 12-month window is continuous and reaches 330 full days.

- If the threshold is missed, do not force this route.

Do not assume intent or sympathetic facts can fix a shortfall. Missing the full-day requirement fails this test, including when the gap is tied to illness, family problems, vacation, or employer direction.

Then run a record-quality screen for conflicts or weak support. If passport evidence, calendar history, and your broader file do not align, treat the position as high risk.

Before Form 2555, check timeline and tax home together. A clean day count does not satisfy tax home by itself.

Should You Use Physical Presence or Bona Fide Residence This Year#

Use the test you can document most cleanly this year, not the one that seems easier to argue. If your year was highly mobile, start with Physical Presence. If your facts show stable, long-term residence in one country, evaluate Bona Fide Residence first.

| Situation | Suggested path | Grounded note |

|---|---|---|

| Travel spans multiple countries and your day records are complete | Start with Physical Presence | Use when the year was highly mobile |

| Life is concentrated in one country and your residence facts are consistent | Start with Bona Fide Residence | Use when facts show stable, long-term residence in one country |

| Either path depends on reconstructed records or exceptions instead of direct evidence | Escalate early | Pick the path with less interpretation and stronger proof |

Physical Presence is often more mechanical but record-heavy. Bona Fide Residence can fit stable living patterns, but it is more judgment-driven when facts are mixed. In borderline cases, pick the path with less interpretation and stronger proof.

Use this filter:

- Start with Physical Presence when travel spans multiple countries and your day records are complete.

- Start with Bona Fide Residence when life is concentrated in one country and your residence facts are consistent.

- Escalate early when either path depends on reconstructed records or exceptions instead of direct evidence.

IRS rules also recognize two exceptions to minimum time requirements for these tests. One is a waiver for departure caused by war, civil unrest, or similar adverse conditions, and it is country- and date-specific based on Internal Revenue Bulletin listings. To use that waiver, you must be able to show you reasonably could have met the minimum time requirement without the adverse condition, and only actual days in-country count. The other is a legal boundary: time in a country while violating U.S. law does not count toward either test.

Before Form 2555, run one consistency check across your test choice, timeline, and exception status. If that check fails, switch tests early instead of forcing a fragile position.

Build a Day-Count and Evidence Pack You Can Defend#

Your safest move is one defensible record set where your timeline, test choice, and Form 2555 all match.

For a day-count claim, confirm three points first: 330 full days in a 12-consecutive-month period, a foreign tax home position, and Form 2555 dates that align with the same narrative. Lock the test period before drafting, because late changes can break the qualifying-day math. If you qualify for only part of the year, adjust the FEIE maximum by qualifying days.

Use this order of operations:

- Build one master timeline with entry and exit dates by country.

- Reconcile the count against the 330-full-day threshold in your chosen 12-month window.

- Flag and resolve gaps or overlaps before drafting Form 2555.

- Map each claim on the return to records you already have.

- Run a final consistency pass so the dates and narrative stay aligned, while still reporting the income on your U.S. return.

Common failure mode: correct arithmetic, weak traceability. If dates drift across your timeline, draft, and filed return, your position gets harder to defend. Also treat IRS training material carefully: LB&I practice units are not binding legal authority.

Keep one version-controlled timeline as your source of truth. If relevant to your profile, track FBAR/FinCEN/FATCA/Form 8938 items separately rather than mixing them into the FEIE day-count sheet.

If a date is unsupported, do not count it.

Complete Form 2555 Without Creating Contradictions#

Form 2555 should read as one consistent story across your test choice, timeline, and reported income. At this stage, focus on consistency, not new math.

| Check | What to confirm | Grounded note |

|---|---|---|

| Timeline | Match the Form 2555 qualification window to your final timeline | Contradictions usually come from dates and coverage periods that do not match across forms |

| Year limit | Use the correct year limit: $130,000 for 2025 or $132,900 for 2026 | Adjust for qualifying days if qualification is only part-year |

| Tax home explanation | Keep it aligned with the same dates and locations used in your qualification record | Form 2555 should read as one consistent story across your test choice, timeline, and reported income |

| Income and Schedule SE | Compare income amounts and period coverage across FEIE entries and Schedule SE inputs | Schedule SE calculates self-employment tax on net earnings, and the Social Security Administration uses Schedule SE information for benefit calculations |

| IRS instructions | Recheck current IRS instructions before you file | If you switch from the Physical Presence Test to the Bona Fide Residence Test mid-planning, rerun the full review instead of patching one field |

Before filing, tie out Form 2555, your return, and Schedule SE. FEIE applies only if you qualify and have foreign earned income, and that income is still reported on your U.S. return. Contradictions usually come from dates, coverage periods, or amounts that do not match across forms.

Use this pre-file check:

- Match the Form 2555 qualification window to your final timeline.

- Confirm you are using the correct year limit ($130,000 for 2025 or $132,900 for 2026), and adjust for qualifying days if qualification is only part-year.

- Keep your tax home explanation aligned with the same dates and locations used in your qualification record.

- Compare income amounts and period coverage across FEIE entries and Schedule SE inputs.

- Recheck current IRS instructions before you file.

If you switch from the Physical Presence Test to the Bona Fide Residence Test mid-planning, rerun the full review instead of patching one field. A test change can make earlier wording and support notes inconsistent even when totals still look fine.

Schedule SE also needs a direct check: it calculates self-employment tax on net earnings, and the Social Security Administration uses Schedule SE information for benefit calculations. Final red flag: clean spreadsheets with vague explanations. Keep one source timeline and make sure the narrative and numbers agree.

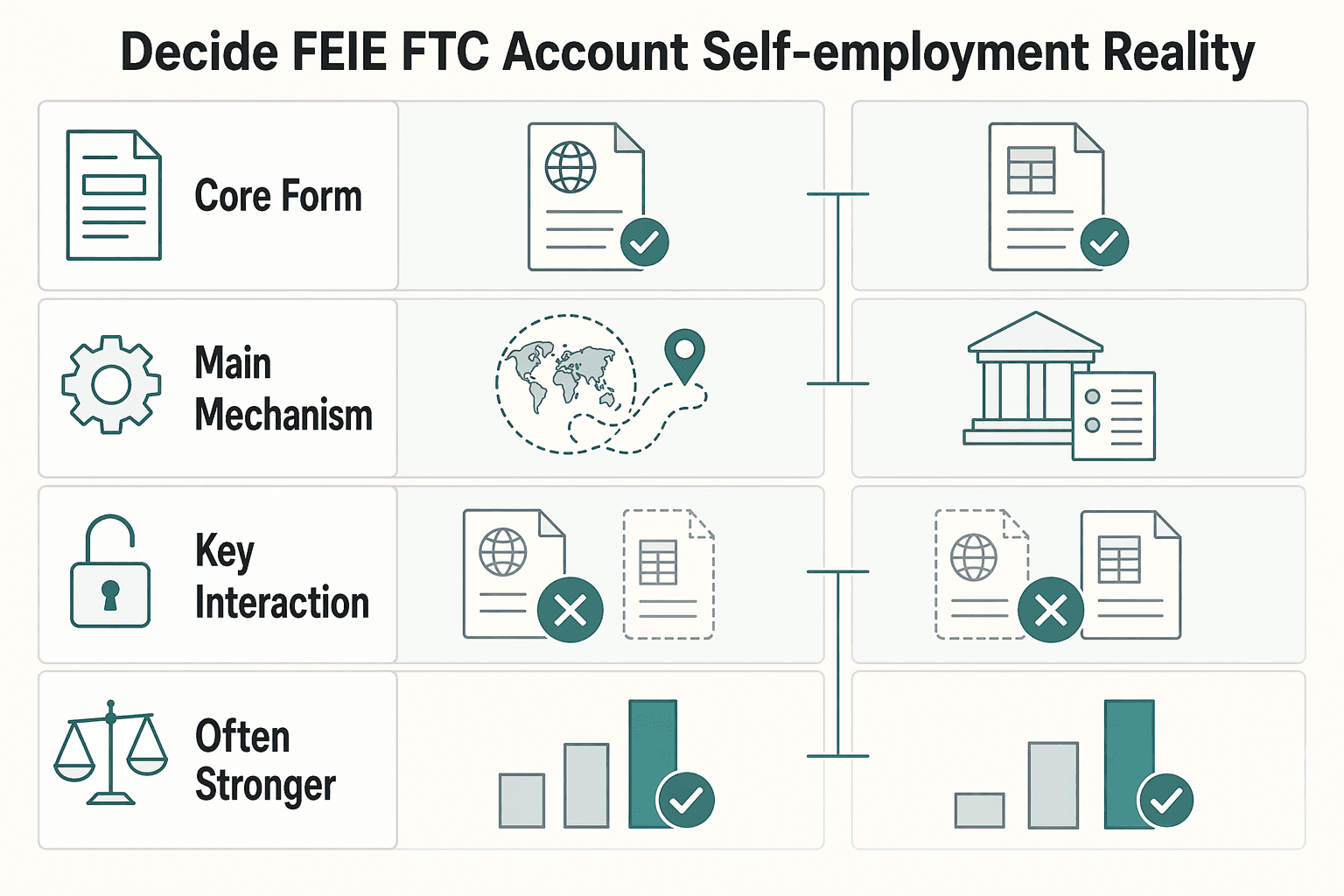

Decide FEIE vs FTC and Account for Self-Employment Reality#

Run FEIE and FTC side by side before filing, and choose the path that creates less overall U.S. tax friction for your actual year. Do not choose by habit.

For 2026, FEIE can exclude up to $132,900 per person, but you still file a U.S. return reporting income. If you exclude income under Form 2555, you cannot also claim FTC on taxes tied to that excluded income.

| Checkpoint | FEIE path | FTC path |

|---|---|---|

| Core form | Form 2555 | Form 1116 |

| Main mechanism | Excludes qualifying foreign earned income up to the annual limit | Claims a credit for qualifying foreign taxes |

| Key interaction rule | Excluded income cannot also be used for FTC | Credit applies to qualifying foreign taxes, but not on excluded income |

| Often stronger when | The exclusion covers most qualifying earned income | Foreign taxes are significant and exclusion still leaves U.S. tax friction |

Before you lock the method, run one clean comparison file:

- Keep the same period assumptions across eligibility, income, and foreign tax entries.

- Model the FEIE path with Form 2555 assumptions.

- Model the FTC path with Form 1116 assumptions.

- Separate tax tied to excluded income, since that portion is not creditable.

- Review self-employment items on the same income set, but treat that analysis as its own check.

If exclusion still leaves material U.S. tax friction, pressure-test the credit path in detail. For deeper scenario modeling, use FEIE vs. FTC: A Strategic Choice for High-Earning US Expats.

Handle Country and Program Differences Without Guessing#

Do not guess across countries or programs. Build one dated, internally consistent file that aligns residency facts, tax home position, and Form 8938 analysis for the same tax year.

Use this confirm-before-filing checklist:

- Confirm your local residency posture for each country tied to the year, including any status-change dates.

- Reconcile that timeline with your Tax Home Test position and the narrative already used on Form 2555 and the return.

- Identify whether you hold specified foreign financial assets, then test total value against the applicable Form 8938 threshold for your filer category.

- Treat the common $50,000 figure as a starting point, not a universal threshold.

- If you are filing as a specified domestic entity, apply the instructions test: over $50,000 at year end or over $75,000 at any time during the year.

- Confirm filing dependency: if no income tax return is required, Form 8938 is not required for that year.

- Keep FBAR on a separate verification track so assumptions do not get mixed.

Red flag: assuming trust-reporting relief automatically eliminates Form 8938 exposure. Trust relief does not remove section 6038D reporting obligations, so Form 8938 still needs its own test.

Escalate before filing if facts are mixed: multiple moves, unclear residency classification, partial account records, or a late switch between tests. The goal is one coherent story across residency, tax home, and asset reporting.

If you want a deeper dive, read Common and Costly Mistakes to Avoid When Claiming the FEIE.

Make the Test Choice You Can Prove#

Choose the FEIE path you can document cleanly, then keep that same position consistent in Form 2555 and the rest of your return. The goal is a filing you can defend with records, not a theory you have to explain later.

If you use the Physical Presence Test, treat it as a strict day-count rule:

- You need 330 full days in foreign countries within any 12 consecutive months.

- The 330 days do not have to be consecutive.

- If you miss 330 days, you fail this test, even for illness, family issues, vacation, or employer orders.

Use a conservative sequence:

- Confirm which test your records actually support.

- Verify your tax home position as a separate gate.

- Reconcile Form 2555 and related filing narrative so dates and status claims align.

- Submit only after a final contradiction check.

Use IRS sources as your baseline, and treat IRS training materials as context only, not controlling law. If your facts are borderline, unclear, or hard to document, escalate early to protect downside and keep the filing defensible.

To confirm what is supported for your specific country or program, Talk to Gruv.

Frequently Asked Questions

What is the physical presence test feie in plain English?

It is one path to qualify for the Foreign Earned Income Exclusion through a day-count rule abroad. The IRS standard is at least 330 full days in foreign countries during any 12 consecutive months. You still file a U.S. return and report income when claiming the exclusion.

How is the Physical Presence Test different from the Bona Fide Residence Test?

Physical Presence is mainly a time-and-location calculation. Bona Fide Residence depends on whether you were a bona fide resident of a foreign country for an uninterrupted period that includes an entire tax year.

Can I qualify for FEIE if my foreign days are not consecutive?

The 330-day threshold is measured within a 12 consecutive month period. Verify the current IRS filing guidance before you file.

What usually disqualifies someone even when they lived abroad most of the year?

A common break is missing a core eligibility condition. FEIE requires foreign earned income, a foreign tax home, and a qualifying test path.

Do I still need to think about Tax Home Test if my day count is strong?

Yes. Day count alone does not establish FEIE eligibility. Tax home is a separate requirement and must align with your filing narrative.

How do FBAR, FinCEN, FATCA, and Form 8938 relate to this decision?

Verify FBAR, FinCEN, FATCA, and Form 8938 thresholds, deadlines, and filing rules separately.

When should I choose FTC instead of FEIE?

FTC may be an option for qualifying foreign taxes paid or accrued. FTC is claimed on Form 1116, and it cannot be claimed on income excluded under FEIE. Taking FTC on excluded income can create FEIE election-revocation risk.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

FEIE vs Foreign Tax Credit for High-Earning US Expats

Start with compliance, then optimize tax. If you are a globally mobile freelancer or consultant filing `Form 1040`, first confirm what you can actually claim and support, then compare the tax result.

Common FEIE Mistakes That Break Form 2555 Claims

Treat FEIE as a compliance decision, not a shortcut. It can reduce U.S. federal income tax only when you qualify and file correctly, and the bigger mistakes usually start when someone jumps straight to the tax savings before confirming the facts that make the claim possible.

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.