Quick Answer

Yes - uneven freelance payments can support a Portugal D8 filing when the last three months are clearly traceable across contracts, service records, invoices, and bank statements. The core standard here is readability for review: show ongoing paid work, connect outlier months to evidence, and keep your narrative consistent with the documents. Because intake channels can differ on checklist wording, confirm your own consular or VFS requirements before you finalize assumptions.

What your D8 file needs to show when freelance payments are lumpy#

Lumpy freelance payments can still work for a Portugal remote-work filing (often called D8) if your documents clearly show stable, regular income over time. You are not trying to prove identical monthly pay. You are trying to show credible means of subsistence in a way a reviewer can verify quickly.

Portuguese rules frame this directly. Meios de subsistência means stable and regular resources sufficient for essential living needs. For remote-work visa processing, that standard is applied through document checks, including proof of average monthly income for the last three months at a floor tied to four monthly minimum guaranteed remunerations.

So in most portugal d8 visa lumpy income cases, the practical question is simple. Can you prove that your income pattern is real, ongoing, and traceable across the last three months? If you are paid by milestones, retainers, or project completion, focus on making that payment rhythm easy to follow.

That is why execution matters more than headline numbers from search results. Public guidance conflicts on exact monthly amounts, and checklist wording can vary by filing route and by consular or VFS channel. A useful legal anchor for 2026 is the 920,00 € minimum wage, effective 1 de janeiro de 2026. Still, you should verify the exact checklist used in your legal area of residence before setting your target.

Document quality is where many files weaken. General D-visa packs call for full three-month bank statements, and digital-nomad checklists also reference service contracts plus documents attesting services provided. In practice, your file is strongest when each payment has a clear chain:

- contract or engagement record

- service-attestation record

- matching bank credit

Plan for review behavior, not just eligibility. Applications are submitted in person to the consular service for your area. The post may request additional documents, and incomplete files can be refused. If a third party cannot understand your income pattern from your file, tighten it before you apply.

By the end of this guide, you should have a clear sequence for:

- what to gather first, including bank statements, contracts, service records, and your personal statement

- what to explain when spikes or dips reflect normal project timing

- what to verify in your exact filing channel before consular review

The goal is not to make uneven payments look monthly. It is to prove, with consistent documentation, that they still represent stable work and sufficient means of subsistence for Portugal.

Define stable and regular income in practical terms#

For portugal d8 visa lumpy income cases, treat this as a documentation test, not a math puzzle. The available evidence does not establish a single official D8 averaging formula, so focus on showing a pattern a reviewer can follow rather than trying to guess hidden math.

What stable usually needs to look like#

Treat "stable" as continuity, not perfectly even cash flow. If you are earning through active remote client work, that is D8 territory, while D7 is framed around passive income. Build your file to show ongoing work over time, not just a one-off balance snapshot.

What regular should mean for uneven payments#

Treat "regular" as an explainable rhythm over time, not one strong month. Milestone-based payments may still work when your records show repeat activity and a clear sequence of work and payment.

If one month is unusually high, do not let that month carry the case. Anchor your explanation in continuity across the period you are presenting. Avoid importing D7 assumptions, especially passive-income and savings framing, into a D8 file. Keep your explanation tied to active income and the records you can actually show.

Reconcile conflicting D8 income claims before you plan#

If your filing depends on one specific D8 interpretation, verify it in writing before you plan around it. The grounded pattern is narrower than the public chatter. Official checklist excerpts point to a last three months average and a 4x minimum-wage threshold, but tax basis and exact euro wording vary by channel.

Known vs unknown#

Use this split to separate filing-language facts from online noise.

| Topic | Known from the excerpts | Still unknown or contested | What to do with it |

|---|---|---|---|

| Four-times-minimum-wage rule | Multiple VFS D8 checklists require proof of average monthly income for the last three months tied to 4x the Portuguese monthly minimum wage. | Which exact euro amount your channel applies if minimum wage changed after an older checklist version. | Use 4 x current Portuguese minimum wage as your internal planning benchmark, then confirm your channel’s current checklist before filing. |

| Gross-before-tax standard | The excerpts do not establish one universal gross-before-tax rule. | Whether your intake channel treats the threshold as gross, net, or with channel-specific wording. | Do not assume gross unless your filing channel confirms it in writing. |

| Net-income wording | One UK VFS one-pager states €3280, net of any tax and social contributions. | Whether that wording applies outside that specific channel or version. | Treat it as evidence of channel variance, not as a universal D8 rule. |

| Reddit/Facebook claims | Community claims are not filing authority, and public guides show conflicting figures such as €3,680 vs €3,480. | Whether any community claim matches your exact consulate’s current standard. | Use community posts to generate questions, not filing decisions. |

That is the practical divide between common digital-nomad visa talk and what the excerpts actually support. Three-month averaging + 4x minimum wage are repeatedly cited. One universal tax basis and one fixed euro figure are not.

The benchmark that keeps planning stable#

Pick one internal benchmark and keep it until your channel says otherwise. For 2026 planning, 4 x €920 = €3,680 is a reasonable working number because the government announced the minimum-wage increase from €870 to €920 in 2026. Treat this as a planning anchor, not proof that every filing channel will display or assess the threshold the same way.

Then set one external checkpoint before filing. Check your exact VFS or consulate page, save the checklist PDF version you relied on, and ask a written question if wording is unclear. Keep the question specific. For example, ask whether Article 61-B remote-work residence visa applications in your filing channel are assessed on a gross or net basis, and whether applicants should use the current 4x minimum-wage figure or the numeric amount printed on that checklist.

This checkpoint matters because checklist language can differ materially. One UK page uses €3280 net wording. Another says employment income can be considered and separately requires an available bank balance of at least €920. The same checklist set also states that consulates may request additional documentation and that submission does not guarantee approval. If your case only works under a contested reading, delay filing until you have written confirmation from your exact intake channel.

Decide if your income profile is filing-ready now#

Do not ask whether your income looks neat. Ask whether it is readable. Your file is closer to filing-ready when a third party can follow your income pattern from documents alone. The provided excerpts do not establish a Portugal D8 definition of filing readiness, and the non-SEC excerpts are not official D8 standards, so treat this as a self-check.

Name the pattern from records, not memory#

Start by classifying your recent period from your invoices and bank statements, not from memory. These are practical labels for organizing records, not official D8 categories:

- Seasonal: income clusters in predictable periods.

- Project-based: quiet stretches followed by larger milestone payments.

- Client-concentrated: most income comes from one payer.

If the pattern becomes clear when you line up invoice date, payer, amount, and deposit date, the volatility is at least explainable. If it still looks random, the problem is documentation clarity, not just uneven cash flow.

Judge traceability before totals#

For proof of income, start with traceability. Can you match meaningful credits to named clients and dated invoices without guessing? Use this stress test: Would a third party understand this pattern from my financial documents alone? If not, the file likely needs more work before you rely on it.

Apply a practical go/no-go rule#

Use a simple decision rule for your internal readiness. If income is uneven but explainable, strengthen the evidence narrative with clean reconciliation, consistent naming, and clear explanations for spikes and gaps tied to documents. If income is uneven and thinly documented, wait and build a cleaner record. This does not establish how a consulate will decide a D8 case.

A useful red flag is this: if you cannot explain a large deposit or a quiet period in one sentence and point to a supporting document immediately, treat the profile as not ready yet.

Keep non-cash noise separate. Do not let formal-looking statements replace cash traceability. In the provided excerpts, the only clearly formal filing artifact is an SEC Form 6-K from March 2015. It explicitly notes that reported results can look more volatile when valuation movements are recognized. Different context, same practical lesson: keep your readiness call anchored to document-level income traceability, not presentation-quality reporting.

Build the evidence pack that survives document scrutiny#

Build this part of your file so a reviewer can verify income quickly, not interpret it. For uneven freelance income, each meaningful payment should be traceable from service evidence to billing records to bank credit. This matters especially across the last 3 months, which is the window explicitly referenced in one VFS temporary-stay checklist version for average monthly income proof.

That same checklist also states that missing required documents may lead to rejection, and consular authorities can request supplementary documents. So the goal is a complete, cross-checkable first submission.

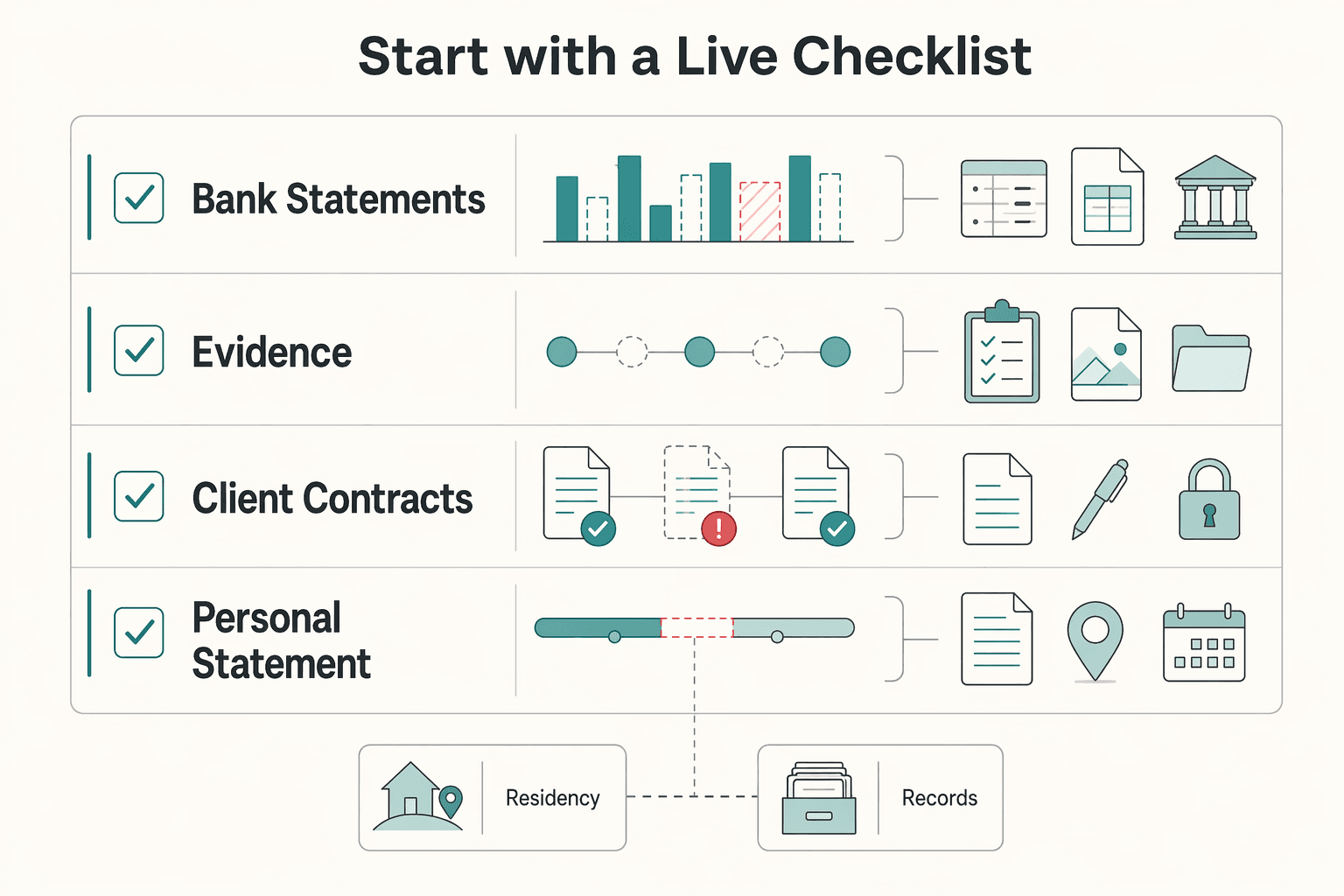

Start with a live checklist#

| Artifact | What it should show | Owner or source | Status | Missing evidence fallback |

|---|---|---|---|---|

| Bank statements | Incoming credits, dates, amounts, and account ownership details that can be matched to your work records | Your bank | Ready / partial / missing | Request full reissued statements; add account ownership proof; add supporting remittance or payment records when payer names are unclear |

| Service and billing records | Evidence of services provided and related amounts/periods (for example, invoices) | You or your business | Ready / partial / missing | Reissue or supplement records so names and dates can be matched to payment records |

| Client contracts | Scope, parties, and billing terms | You and client | Ready / partial / missing | Use a service contract, proposal of service contract, or document attesting services provided |

| Personal Statement | Signed statement specifying reason for settling in Portugal, intended area of residency, and type of accommodations | You (applicant) | Ready / partial / missing | Update and sign the statement so it aligns with the rest of your file |

| Supporting financial documents | Bridge records that connect service/billing records to deposit identity | Payment intermediaries, bookkeeping records, or client confirmations | Ready / partial / missing | Add intermediary statements or client confirmations that link deposits back to your service/billing records |

Treat “partial” as a real gap, not a placeholder.

Match each payment stream three ways#

For each major client or payment stream, build one documentary chain:

- engagement evidence, such as a contract, proposal, or similar service evidence

- service/billing record tied to that work

- matching bank credit trail

This is what makes lumpy income easier to read as consistent underlying work. As one Portugal immigration lawyer frames it, reviewers assess income consistency, source of income, contractual documentation, and bank statements.

Add a short cover note that explains the pattern#

If your records need context, add a short note that explains the billing pattern in plain language and points directly to the evidence. Keep it consistent with your Personal Statement and include only what helps verification:

- period covered, aligned with your submitted records

- billing model, for example milestone or retainer cycles

- why highs and lows occur, tied to attached documents

- where each explanation is evidenced in the file

A practical line you can adapt is this: income is uneven month to month, but work is continuous and documented through service evidence, billing records, and bank records. Practitioner guidance is aligned on this point: “The most important thing is to demonstrate consistency and regularity of income.”

Before submission, do one final pass. Every statement in your note should map to a document, and every weak item should already have its fallback attached.

For a step-by-step walkthrough, see How to Use a Wise US Business Account to Satisfy 'Proof of Income' for Spain's Digital Nomad Visa.

If your documentation is still scattered, use this visa checklist to verify what to assemble before filing: Visa Cheatsheet for Digital Nomads.

Convert lumpy cashflow into a clear reviewer narrative#

This is where many workable cases become convincing or confusing. Your goal is not to make irregular payments look monthly. Your goal is to make the last three months easy to verify across work evidence, income documents, and payment records.

Organize around the three-month evidence window#

Use the same window and document types shown in checklist language: average income over the last three months, plus bank statements and invoices or payslips for that period, with wording varying by filing post.

A practical way to present each payment trail is to keep the same sequence:

- Client contract or other service evidence

- Invoice or payslip tied to that work

- Bank statement entry showing the matching credit

This keeps self-employment evidence readable because income records and work-relationship documents are both part of the review.

Explain spikes and gaps with document-backed context#

Uneven income is workable when it is clearly explained and tied to records. If a spike or gap appears, state it in one short line and point to the matching service evidence, invoice dates, and bank credit dates. Keep explanations factual and brief. Think of this as indexing evidence, not telling a story.

If one client dominates, strengthen continuity before filing. A single large client is not automatically disqualifying, and the checklist language provided does not explicitly require multiple clients. Practitioner guidance treats consistency and client diversification as credibility positives.

Keep wording consistent across documents#

Use the same names, service descriptions, and period labels across your personal statement, service documents, invoices or payslips, and bank records. Final check: every claim should map to a document, and all documents should tell the same story.

Sequence your timeline from first prep to filing day#

The cleanest timeline is simple: lock your filing channel, collect raw documents, reconcile them, then build summary pages. That order helps protect your income narrative and keeps you from polishing a file that still has gaps.

Start by confirming the exact requirements for your filing channel before final assembly. Checklist details can vary, and at least one VFS D8 residence checklist requires documents in the exact listed order. Build your plan around that reality, plus possible supplementary-document requests.

Build backward from submission day#

Pick a target submission date and work backward.

| Stage | What you do | What you verify | Common failure mode |

|---|---|---|---|

| Raw collection | Gather income evidence, work evidence, passport copy, and police-certificate inputs as required by your checklist | You have the last three months for income evidence | Building summaries from partial records |

| Reconciliation | Match work evidence, invoice or payslip, and bank credit | Names, dates, and amounts align across documents | Deposits that cannot be tied clearly to underlying work |

| Readability layer | Create your cover note, payment index, and final ordering | Every summary statement maps to a document | Summary claims that the file cannot support |

| Submission readiness | Run checklist-order and completeness checks | File is complete, current, and arranged as required | Last-minute substitutions that weaken consistency |

Put two checkpoints on the calendar#

Do not wait until the end to test the file. Use a mid-process quality check after collection and reconciliation, before formatting. Confirm three things:

- Every claimed payment has a document chain.

- Names and labels stay consistent across statements, invoices or payslips, and your note.

- No critical document will age out before filing.

Then run a final pre-file audit against checklist wording: proof of average monthly income earned in the last three months, with a minimum equivalent to four times the Portuguese monthly minimum wage. Also audit for completeness, since missing required documents can lead to rejection, and consular authorities may still ask for supplementary documents.

Schedule fragile documents early#

Time-sensitive items should go near the front of your plan. In the US channel checklist, police clearance must be issued less than 90 days before submission and include the Hague Apostille. Applicants with over one year of US residence may need an FBI-issued certificate. One checklist also requires a passport valid for at least 3 months beyond the intended stay. If either item is tight, fix it early.

Use a real go/no-go rule#

Make go or no-go about evidence quality, not urgency. If you still have unexplained gaps, unmatched deposits, inconsistent names, or expiring documents, pause and fix the file first.

Treat processing timelines as estimates, not guarantees. One checklist cites 60 calendar days, while another says 1 to 2 months. This is a visa for residence permit, described as valid for two entries and four months. A complete, ordered file is a stronger baseline than rushing a weak one.

Related reading: Golden Visa vs. Digital Nomad Visa: Which Path to Residency is Right for You?.

Catch red flags that commonly weaken D8 applications#

The provided excerpts do not establish official D8 rejection criteria. Treat this as a self-audit for internal consistency, not as an official checklist. If your file has unclear links between claims and documents, tighten it before filing.

As a practical self-check, try to make each income claim traceable from your summary note to supporting records without guesswork. Check for:

- mismatched names or labels across contracts, invoices, bank statements, and tax records

- payments that are hard to reconcile to billed work because timing or amounts are unclear

- narrative statements that do not match totals, labels, or dates in the underlying documents

When you find a gap, explain it directly in your file and attach the document that resolves it. Keep the narrative aligned to the records, not the other way around.

Do not treat weak online excerpts as documentary authority for D8 standards. In this research set, one source is a U.S. House proceedings record dated June 29, 1966, and another is a Science.gov page that includes a conference note about 127 delegates from 15 countries. Those materials are not Portugal D8 adjudication guidance, so they should not drive your filing logic.

Choose D8 or D7 when your income mix is changing#

When your income mix changes, use this as a practical framing, not an automatic rule: is your case centered on active remote work or on living from individual revenues? If active remote work is dominant, use the digital-nomad remote-work logic often called D8 in common guidance, then confirm the official category name with your filing post. If passive income is dominant, pressure-test D7 before you file.

D7 materials are framed around residence for retirement, religious purposes, or living from individual revenues. The remote-work route is framed as residence for professional activity done remotely. That framing changes what counts as convincing proof of income.

| Checkpoint | Remote-work route | D7 route |

|---|---|---|

| Best fit | Main story is paid work done remotely | Main story is living from individual revenues |

| Core evidence | Employment contract or employer declaration; for self-employment, service contract, articles of association, or proof of services provided | Explanation of income sources, plus documents showing revenue from property or intellectual or financial assets where relevant |

| Income review angle | Active professional activity plus proof of financial resources, including income history for the last three months | Source and nature of the income stream, supported by source documents |

Final check before you assemble documents: confirm naming in your consular channel. In some official materials, remote-work digital nomad is labeled D9 while D8 is used for accompanying family members, even though private guides often call the digital nomad route D8.

Do not mix category logic in one file. If your evidence is mostly freelance contracts and proof of services, keep the case built around active work. If passive income now carries the case, rebuild around that stream and its source documents. Related: Portugal Digital Nomad (D8) Visa: A Complete Guide.

Run a final pre-submission quality check#

Before you submit, run one last audit: every factual claim in your summary should map to a document already in your file.

Trace each claim to one hard document#

Do not leave any claim unsupported. If you state income was earned in the last three months, make sure your file includes income evidence for that period. If you state remote work is active, tie it to a client or service contract, a proposal of service contract, or a document attesting services provided.

A practical pass is to label each summary claim with its matching evidence. If a claim has no clear document anchor, remove it or rewrite it as context rather than fact.

Reconcile names, dates, and payer identity#

Inconsistency can weaken your file. Check names, dates, and payer/account details across your financial documents.

If bank payer names differ from invoice client names, for example because of a parent entity or payment processor, explain that difference directly. Also verify that your pack supports the checklist wording around average monthly income in the last three months and the benchmark expressed as four times the Portuguese monthly minimum wage.

Record unknowns as unknowns. If something is unclear, state it plainly and verify it with your consular channel before filing. Do not guess a fixed euro threshold when public guides conflict, and do not present pending items, such as a tax residence certificate, as complete. Incomplete files can be rejected, and requests for supplementary documents can pause examination until the missing items are submitted.

Next steps for a confident D8 filing with uneven income#

File only when your evidence tells one consistent story. For a D8 application, a smaller, reconciled file is usually stronger than a large bundle with duplicates, mismatched dates, or unexplained payments.

Build one reviewer-readable file#

Your target is to show stable and regular income that is sufficient for your needs. In checklist terms, at least one D8 remote-work checklist asks for evidence of average monthly income for the last three months at a minimum equivalent to four monthly minimum guaranty remuneration, plus proof of professional activity and fiscal residence.

Make the file easy to follow from work performed to payment received. For each payment stream, match:

- service contract, or a document attesting services provided to one or more entities

- invoice or equivalent billing record, if you use one

- bank or credit statements in your name for the relevant period

- tax residence document

- an optional summary sheet that aligns dates, payer names, and amounts

The key checkpoint is traceability. If a contract says Client A paid for January work, the billing record and bank credit should align without interpretation. Large deposits without service documentation, or inconsistent client naming across documents, create avoidable risk.

Verify the exact filing route before you finalize anything#

Use the exact visa-type page for your jurisdiction, then confirm intake details with the competent consular post before submitting. This step matters because requirements can vary by filing channel. One post-specific checklist asks for bank or credit card statements in your name from the previous 3 months. Another states the embassy may request additional documents or an interview. If your case depends on assumptions, such as whether a payment-platform statement is acceptable, confirm that with your actual filing channel before you submit.

Prioritize consistency over volume#

Your proof of income is strongest when every summary point maps to a specific document. If you include a cover note, keep it short and factual. Explain spikes or dips by linking them to project timing, milestone billing, or renewals, then point to the exact supporting records.

Do not upload everything by default. Extra volume can introduce contradictions. If a summary says three clients but the file supports only two, fix the gap first. If statements include transfers between your own accounts, label them clearly so they are not read as client payments.

Use a real go/no-go rule. Before submission, run one final check: could a third party understand your last three months from the file alone, without your explanation? If not, the file is not ready.

Use a strict go rule:

- your benchmark matches your post’s current checklist

- each claimed income item has a document trail

- contracts, statements, and tax-residence evidence are internally consistent

Even a complete submission with paid fees does not guarantee approval, which is why the final pass should be evidence-first, not urgency-first.

If you need cleaner, timestamped records to support your income narrative, generate standardized invoices before your next billing cycle: Free Invoice Generator.

Related Guides and Official References#

- Use this related guide to align your scope and pricing assumptions before execution.

- Cross-check execution steps with Value-Based Pricing for Freelancers and tighten approval checkpoints.

- Review a contingency pattern in this backup playbook before rollout.

- Benchmark assumptions against this supporting article to avoid planning drift.

- Track legal/compliance edge cases in this linked explainer if your setup is cross-border.

Use official documentation for policy and filing details, including primary guidance, administrative rules, and reference material.

Quick Comparison Table#

| Proof packet | Minimum evidence | Execution note |

|---|---|---|

| Income continuity | 6-12 months of invoices | Explain client concentration changes |

| Cash buffer | Dedicated reserve account | Map reserve duration vs visa timeline |

| Currency consistency | EUR-normalized summary | Include FX method and date |

Frequently Asked Questions

What income level is most commonly cited for the Portugal D8 Visa, and why do public numbers differ?

The checklist wording most commonly cited is proof of average monthly income from the last three months at four times the Portuguese monthly minimum wage. Public euro figures differ because the minimum-wage baseline changes over time, so older references can show 01/01/2024 (€820) while newer ones can show 01/01/2025 (€870). Use the exact checklist version and filing channel for your application, not a recycled number from general search results.

Is D8 income usually treated as gross income before tax or after tax?

The D8 checklist text does not conclusively set a universal gross-versus-net rule. It states “average monthly income,” but that wording alone does not settle interpretation across filing channels. If your eligibility depends on one interpretation, confirm it directly with your consular or VFS channel before filing.

Can lumpy freelance payments still qualify as stable and regular income?

Potentially. Lumpy freelance payments may still qualify if the three-month average is supportable and the payment trail is clear. The reviewer should be able to follow your work and payments through service-contract evidence and your income proof. A large payment without supporting service documentation can trigger follow-up document requests.

What documents matter most when proving income consistency for a D8 application?

For self-employed applicants, prioritize the checklist items: a service contract or a document attesting services provided to one or more entities, plus the tax residence certificate listed in the D8 checklist. Then organize your income evidence so the reviewer can trace it across documents.

How should I handle a month with unusually low or unusually high income?

Address it directly and anchor it in the last-three-month average test. Then attach objective support that explains the dip or spike through your service documentation and income evidence. Do not leave an outlier month unexplained, especially if it conflicts with your summary of ongoing remote work.

When should I reconsider D8 and evaluate D7 instead?

Reconsider D7 when your case is primarily based on passive income rather than active remote professional work. The D7 checklist language is explicitly framed around living from passive income. If your evidence does not strongly support an active-work narrative, pressure-test D7 before filing.

What details are still unknown from public SERP sources and must be verified directly before filing?

You still need to verify the exact checklist version for your filing post, how that channel applies income interpretation in practice, and whether it requires extra documents beyond the baseline list. Public pages do not provide one universal document list for every filing route, and consular posts can request supplementary documents. Because incomplete files can be rejected, confirm these points directly with the competent consular office before submission.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- congress.gov/89/crecb/1966/06/29/GPO-CRECB-1966-pt11-6-1.pdftrusted

- congress.gov/81/crecb/1950/06/06/GPO-CRECB-1950-pt6-14.pdftrusted

- digital.lib.washington.edu/researchworks/bitstreams/164507e1-15ee-4f8d-...trusted

- govinfo.gov/content/pkg/GPO-CRECB-1972-pt1/pdf/GPO-CRECB...trusted

- science.gov/topicpages/s/senri+osaka+japantrusted

- sec.gov/Archives/edgar/data/1116578/0001193125151171...trusted

- www2.gov.pt/en/migrantes-viver-e-trabalhar-em-portugal/m...trusted

- alibaba.com/product-insights/digital-nomad-visa-vs-touri...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

The 2026 Global Digital Nomad Visa Index for 50+ Countries

Start with legal fit, not lifestyle filters. The practical order is simple: choose a route you can actually document, then decide where you want to live. That single change cuts a lot of wasted comparison work and stops you from falling in love with places that were never a real filing option.

Portugal Digital Nomad Visa Decisions That Prevent D8 Delays

Start with verification, not paperwork. In this research set, some material is useful only as EU VAT context, not as D8 instruction, and mixing those categories is one of the fastest ways to build the wrong plan. We use the same separation rule in [Global Digital Nomad Visa Index](/blog/global-digital-nomad-visa-index) comparisons.

Proving 'Sufficient Funds' for Portugal's D8 Visa with Fluctuating Freelance Income

---