Quick Answer

For a U.S. citizen, second citizenship can provide a backup legal home, support an ancestry claim, improve travel options, or help with long-term relocation, but it does not end U.S. tax filing, account reporting, or U.S. passport rules. The main downsides are cost, document burden, real residence requirements, timing risk, and compliance in both countries.

Phase 1: The Strategic Assessment - Defining Your 'Why'#

Pick one primary objective before you compare countries. For most people considering a second citizenship as a U.S. citizen, the first decision is not where to apply, but what that citizenship needs to do for you.

Start with one decision lane. You may care about mobility, family lineage, and relocation at the same time, but only one should drive your first application path.

| Decision lane | Primary objective | Best-fit pathway | Main tradeoff | What you must verify first |

|---|---|---|---|---|

| Backup option | Add a second legal home as a hedge against single-country risk | Citizenship by investment | High upfront cost, due diligence, and no guaranteed timing | Whether the country permits dual nationality in your case, and whether filing must go through an authorized agent |

| Family claim | Secure citizenship you may already qualify for through ancestry | Citizenship by descent | Lineage rules can be narrow, with high document burden | Your exact qualifying line and who is included or excluded in family eligibility |

| Move and settle | Build a long-term base abroad, often tied to residency and tax planning | Naturalization after legal residence | Slow timeline and real physical-presence requirements | The country's residence and presence tests, not just passport eligibility |

| Easier travel | Improve practical travel access on routes you actually use | Investment or descent, based on eligibility | Benefit can be narrower than expected once cost and timing are included | Whether access gains are meaningful for your travel pattern and family plan |

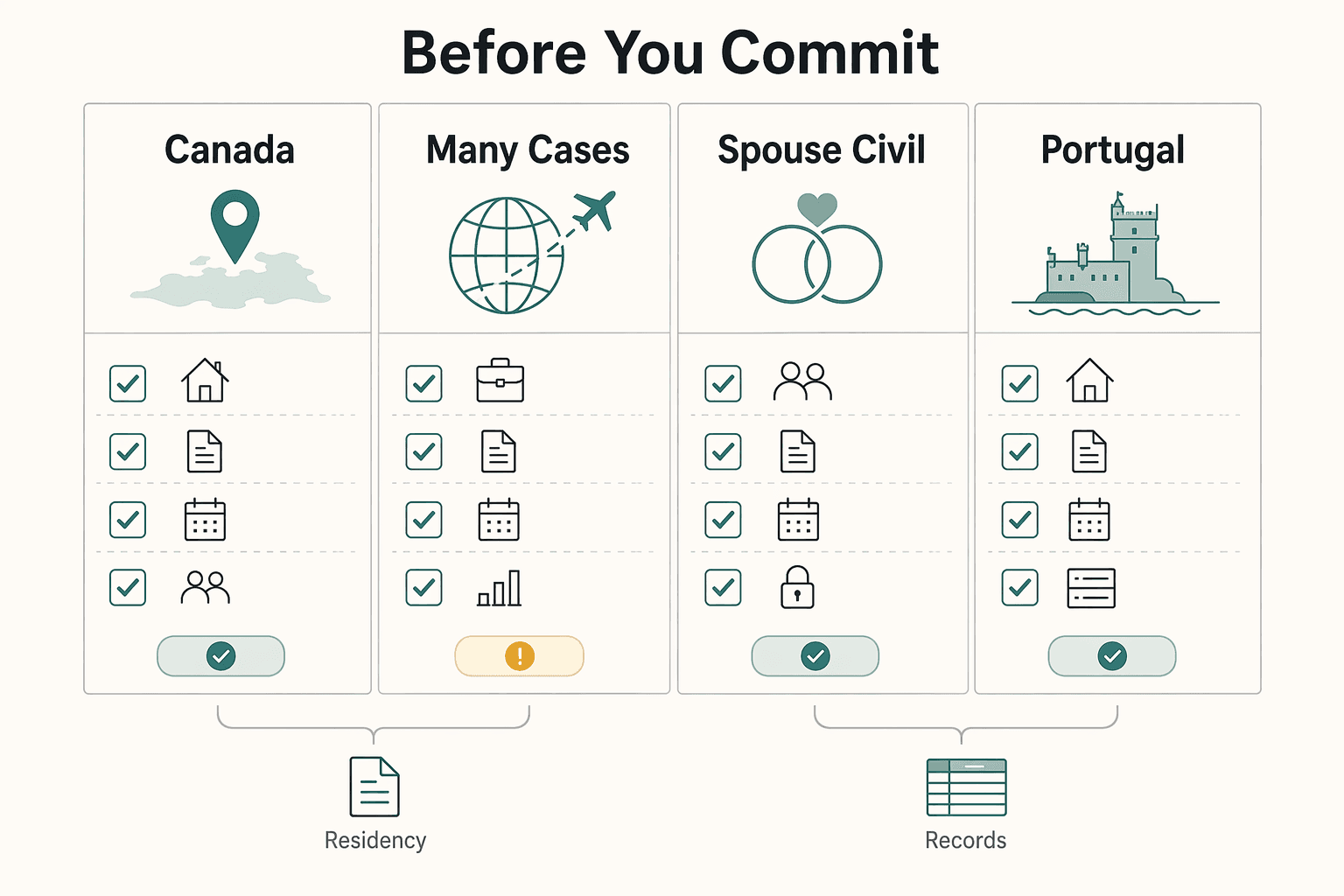

Before you commit#

Once you choose a lane, the verification work becomes more specific. Use the checklist that matches your main objective.

| Country/path | Residence benchmark | Note |

|---|---|---|

| Canada | 1,095 days in 5 years | Example of grounded residence benchmarks |

| UK (many cases) | 5 years | Applies in many cases |

| UK spouse or civil-partner routes | 3 years | Spouse or civil-partner routes |

| Portugal | 5 years legal residence | Another benchmark to check |

Backup option checklist

- Confirm dual-nationality eligibility with that country's embassy or consulate.

- Confirm filing mechanics early. Some programs require authorized agents and due diligence.

- Pressure-test timeline risk. Outcomes are not guaranteed.

- Confirm whether spouse and children can be included.

- Plan for U.S. compliance to continue after approval.

Dominica's program, for example, lists qualifying investments starting at US$200,000 for a single applicant. It also says applicants are generally expected to wait at least three months after submission for approval in principle.

Family claim checklist

- Prove the lineage path with the exact civil records required.

- Budget for apostilles and translations where required.

- Verify family inclusion rules. Eligibility may not extend to all relatives.

- Check timeline risk for document retrieval and consular processing.

- Keep U.S. tax and reporting obligations in scope from day one.

Move and settle checklist

- Verify legal-residence and physical-presence thresholds before planning anything else.

- Confirm you can sustain years of presence and local administration.

- Check family inclusion and dependency rules on the residence-to-citizenship route.

- Build a realistic timeline around residence first, citizenship second.

- Assume U.S. obligations continue while abroad.

Examples like Canada: 1,095 days in 5 years, the UK: 5 years in many cases, 3 years for UK spouse or civil-partner routes, and Portugal: 5 years legal residence show why you should verify the residence test first.

Easier travel checklist

- Name the exact travel friction you want to remove.

- Compare your real routes against expected access gains.

- Verify total cost and timing against those gains.

- Confirm whether your family can be processed with you.

- Keep the U.S. passport rule in view: U.S. citizens must enter and leave the United States on a U.S. passport.

Across all lanes, keep one constant in view: you can end up with legal obligations in both countries, and U.S. worldwide-income taxation still applies. FBAR can be triggered when foreign financial accounts exceed $10,000 in aggregate during the year. Form 8938 may also apply starting at $50,000 in specified foreign financial assets for some filers.

Use this tie-breaker when goals conflict: choose the lane that changes your actions now. Once your "why" is fixed, move to Phase 2, because your U.S. obligations continue even after you add another citizenship. Related: 183-Day Rule Explained: Stop the Tax Myths Before They Cost You.

Phase 2: The Compliance Gauntlet - Managing Lifelong U.S. Obligations#

A second citizenship does not remove your U.S. filing obligations. From day one, treat tax filing, account reporting, and travel-document checks as recurring tasks.

The baseline is simple: if you are a U.S. citizen living abroad, you are still taxed on worldwide income. The goal is not to eliminate compliance, but to keep it clean and predictable. Additional account-reporting obligations may apply, so verify current requirements for each filing track.

Travel documents#

Pick one travel process and stick to it. Border and airline issues usually start when names, passport numbers, or visa records do not match across systems.

- U.S.-linked travel (departure/arrival tied to the U.S.): confirm current carrier and government document requirements in advance, then keep booking and check-in details consistent.

- Third-country travel: use the passport that best matches your entry or stay rights in that country.

- Always: keep names, passport numbers, and visa records aligned across both documents before travel day.

FBAR and FATCA#

| Filing track | What is reported | Who files | Common mistake | Action step |

|---|---|---|---|---|

| FBAR | Items covered by current filing instructions | Filers who meet current criteria | Assuming last year's rules still apply | Verify the current form, threshold rules, and account scope before filing season |

| FATCA | Items covered by current IRS filing instructions | Filers who meet current criteria | Treating it as interchangeable with other reporting requirements | Verify the current IRS form/instructions and thresholds for your filing status |

| Both | Requirements can be separate and case-specific | Some people file one; others may file more than one | Reconstructing balances and ownership at year-end | Maintain a live account/asset tracker with ownership and highest annual balances |

Worldwide income and the FEIE vs. FTC decision#

If you use relief tools, you still file a U.S. return and report the income. That is true even for income excluded under FEIE.

| Item | Key rule | Note |

|---|---|---|

| FEIE | 2026 maximum: $132,900 per person | You still file a U.S. return and report the income |

| Physical presence test | 330 full days in a 12-consecutive-month period | A qualifying day is a full 24-hour period, midnight to midnight |

| Form 1116 | Prepared separately by income category | Each form uses only one category checkbox |

| Foreign housing exclusion | Calculate it first if also using it | It can reduce FEIE available |

FEIE can be relevant when your income is foreign-earned compensation, such as wages, salaries, or professional fees, and you meet eligibility rules. For 2026, the maximum FEIE is $132,900 per person.

For the physical presence route, you need 330 full days in a 12-consecutive-month period. Those days do not need to be consecutive, but each qualifying day is a full 24-hour period (midnight to midnight). If you do not hit 330 full days, you do not meet this test. Waivers may apply in specific adverse conditions, so verify current rules before filing.

If you are evaluating FTC, note that filing is category-based. Form 1116 is prepared separately by income category, and each form uses only one category checkbox. If you are also using a foreign housing exclusion, calculate that first because it can reduce FEIE available.

Risk planning#

Do this before you need it: verify which in-country emergency support channels are actually available to you, and plan around local processes first.

Keep a short emergency sheet with local numbers, legal contacts, and your key local obligations tied to residence or citizenship status. This keeps routine disruptions from turning into avoidable compliance or legal problems.

If you want a deeper dive, read The 2025 Global Digital Nomad Visa Index: 50+ Countries Compared.

Before you lock your citizenship path, track your travel days and residency evidence in one place so your tax position stays defensible: Tax Residency Tracker.

Phase 3: The Integration Plan - Your First Year as a Dual Citizen#

Your first year is an onboarding year, not a paperwork scramble. The practical goal is to make your identity, banking, residency evidence, and tax records tell one consistent story from the start.

| Month range | Focus | Key details |

|---|---|---|

| Months 1 to 2 | Identity baseline | Use one legal-name format, one address format, and one consistent passport-data format; if your home mailing address changed, notify the IRS with Form 8822 |

| Months 2 to 4 | Banking onboarding | Ask how the institution will classify your profile for onboarding; request the exact onboarding list; provide the correct TIN details if requested |

| Months 3 to 8 | Residency evidence | Track physical presence, home base, economic ties, and family/social ties; 330 full days in a 12-month period is the benchmark if you use the physical presence route in U.S. rules |

| Months 6 to 9 | Institution updates | Update banks and payment providers, then brokers and custodians, then tax advisor, then estate counsel in each jurisdiction |

| Months 10 to 12 | Compliance dashboard | Track the FBAR trigger over $10,000 and review Form 8938 if specified foreign financial assets exceed the applicable threshold |

Months 1 to 2#

Set your identity baseline first, before you open new accounts or update advisors. Use one legal-name format, one address format, and one consistent passport-data format across travel, banking, and tax records.

If your home mailing address changed, notify the IRS with Form 8822. Do not assume later filings will fully fix this.

Build your archive now and keep it current: passports, citizenship or residency approvals, account-opening forms, tax forms, and records supporting income and deductions. IRS recordkeeping is evidence-based. The general assessment period is 3 years, and it can extend to 6 years in some underreporting cases.

Months 2 to 4#

Banking setup is institution-specific. Some institutions have separate resident and non-resident onboarding paths, so your route depends on what you can document now and what that institution allows. Use this checklist before you submit applications:

- Confirm your route first: ask how the institution will classify your profile for onboarding (for example, resident or non-resident, where applicable).

- Request the exact onboarding list from that institution: identity verification requirements are institution-specific, and brokers run formal identification programs.

- Expect citizenship and tax-status questions: foreign financial institutions may ask about your citizenship when you open an account.

- Prepare U.S. taxpayer details: if requested for information reporting, provide the correct TIN details (often via Form W-9 workflow).

- Save proof on day one: keep signed tax forms, onboarding confirmations, account owner details, institution, jurisdiction, and open date.

Be consistent about your U.S. status during onboarding to avoid correction work later. Also track all foreign accounts as one set. FBAR uses an aggregate test, and filing can be required once the combined value exceeds $10,000 at any point in the year.

Months 3 to 8#

If tax outcomes matter to you, build evidence continuously instead of relying on intent. Your file should support where your tax home is and, where relevant, where your personal and economic relations are closest.

Track four evidence buckets throughout the year, but add country-specific tests only after you verify current local rules:

- Physical presence: maintain a live day-count log tied to travel records. If you use the physical presence route in U.S. rules, the benchmark is 330 full days in a 12-month period.

- Home base: keep lease or housing records and proof of regular use.

- Economic ties: track local work or business activity, account relationships, and professional engagements.

- Family/social ties: where applicable, document where close personal life is actually centered.

Months 6 to 9#

Update institutions in sequence, not ad hoc. A controlled sequence can help reduce conflicting addresses and identity data across filings. Use this order: banks and payment providers, then brokers and custodians, then tax advisor, then estate counsel in each jurisdiction.

When you brief your tax advisor, send a full packet: identity data, move timeline, account inventory, day-count log, and available foreign tax documents. For estate planning, coordinate both jurisdictions from one shared asset and family fact set so documents do not conflict. Brokers may require refreshed identification documents under customer identification controls.

Months 10 to 12#

By year-end, turn the process into a reusable compliance dashboard. A simple version looks like this:

| Category | Owner | Trigger | Output |

|---|---|---|---|

| Residency tracking | You | Monthly close and each border-crossing update | Updated day-count log plus evidence under physical presence, home base, economic ties, and family/social ties |

| Tax filing position | You + tax advisor | Q4 review and pre-filing planning | Written filing plan, including tax-home and residency-position support |

| Account reporting | You | Aggregate foreign account value exceeds $10,000 at any point in the calendar year | FBAR package for FinCEN Form 114 (due April 15, automatic extension to October 15, no separate extension request) |

| Asset reporting | You + tax advisor | Specified foreign financial assets exceed your applicable Form 8938 threshold (base threshold language starts at at least $50,000, with higher thresholds in some cases) | Form 8938 review file aligned to your U.S. return |

| Document archive | You | Monthly close and pre-filing checks | Complete support file for income, account onboarding, tax forms, and advisor communications |

One final timing check matters here. If you qualify for the automatic abroad filing extension, your return timeline may shift from April 15 to June 15. Interest can still accrue from the regular April due date on unpaid tax, so run this review before filing season pressure starts.

For a step-by-step walkthrough, see How to Prepare for the US Citizenship Test (Naturalization Test).

Conclusion: Second Citizenship as the Ultimate Act of Self-Reliance#

Treat this as a strategic project, not a yes-or-no decision. For a U.S. citizen seeking a second citizenship, the real question is whether your route fits your objective, whether you have handled U.S. compliance deliberately, and whether your first-year setup is realistic.

The "Business-of-One" frame is only useful if it stays practical. Your plan works only if your eligibility evidence, timing, and execution steps hold up under review.

If your route depends on adoption-based eligibility, verify every threshold before you spend money. In the cited IR2 path, the child must be unmarried, under age 21, adopted before age 16, and have jointly resided with the adopting parent or parents for at least two years. The same guidance also notes a real failure mode in some fact patterns: not eligible for any immigrant or NIV classification.

Use primary sources, and treat summaries as starting points only. The cited 9 FAM excerpt shows a 06-18-2025 header. Parts are marked unavailable, and non-government commentary can be current but still non-authoritative.

| Your objective area | First check | Tradeoff to watch |

|---|---|---|

| Family/adoption-based path | Confirm IR2/IR3/IR4 eligibility details in current primary guidance | Missing one requirement can make the case ineligible |

| Any route decision based on secondary summaries | Re-verify against primary government sources before filing | Outdated or incomplete summaries can mislead planning |

Before you proceed, close these four items:

- Confirm your primary objective in one sentence.

- Validate route requirements against current primary sources.

- Align any U.S. compliance workflow with qualified advice.

- Set a first-year relocation execution plan with documents, deadlines, and setup tasks.

You might also find this useful: The Best Citizenship by Investment Programs in the Caribbean.

If your move will change how you collect, hold, convert, or pay funds across borders, review implementation options in the Gruv docs.

Frequently Asked Questions

Can a U.S. citizen legally have dual citizenship?

This article does not determine whether a dual-citizenship case is valid. Before paying for filings, translations, or document retrieval, confirm eligibility and pathway rules with the relevant government authorities or qualified counsel.

Do U.S. citizens with dual citizenship still have to file U.S. taxes?

Often yes. The article says U.S. citizens living abroad are still taxed on worldwide income, and filing may still be required even when FEIE or FTC reduces tax due. FEIE is not automatic, and the physical presence test requires at least 330 full days in a 12-month period. If you plan to claim FTC, review Form 1116 by income category and by country.

What is the fastest way for a U.S. citizen to get a second citizenship?

There is no single fastest route stated here. Timing depends on the country, the pathway, and how complete your documentation is. Confirm current requirements and processing expectations with the issuing authority or qualified counsel before spending money.

Which passport should a U.S. dual citizen use to enter the U.S.?

Use your U.S. passport to enter and leave the United States. For third-country travel, use the passport that best matches your entry or stay rights there. Confirm current carrier and government document requirements before travel.

What are the main disadvantages of dual citizenship for a U.S. citizen?

The main disadvantage described here is ongoing compliance complexity, not the initial application. A dual citizen may need to manage U.S. worldwide-income taxation, account reporting, travel-document consistency, and legal obligations in both countries.

Can I lose my U.S. citizenship if I get a second one?

This tax-focused guidance does not determine citizenship-status outcomes. If a status change is part of your plan, consult qualified nationality counsel early before doing anything irreversible.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- fam.state.gov/fam/09FAM/09FAM050203.htmltrusted

- irs.gov/individuals/international-taxpayers/us-citiz...trusted

- irs.gov/individuals/international-taxpayers/us-citiz...trusted

- travel.state.gov/en/international-travel/planning/personal-ne...trusted

- travel.state.gov/content/travel/en/legal/travel-legal-conside...trusted

- usa.gov/dual-citizenshiptrusted

- gov.uk/apply-citizenship-indefinite-leave-to-remainexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

The 2026 Global Digital Nomad Visa Index for 50+ Countries

Start with legal fit, not lifestyle filters. The practical order is simple: choose a route you can actually document, then decide where you want to live. That single change cuts a lot of wasted comparison work and stops you from falling in love with places that were never a real filing option.

183-Day Rule Tax Myths That Trigger Residency Filing Mistakes

If you are a mobile freelancer or consultant, start here: the "183 day rule tax" idea is not a single universal test. It is a shortcut phrase people use for different residency rules that do not ask the same question. If you mix federal and non-federal residency logic, you can create filing risk even when your travel calendar looks clean.

Renounce US Citizenship With a Clear CLN and Tax Closure Plan

If you plan to **renounce US citizenship**, treat it as a sequence, not a single embassy appointment. In practice, you are managing three checkpoints: the consular renunciation act abroad, State Department approval reflected in a Certificate of Loss of Nationality (CLN), and tax-compliance follow-through with the IRS.