Quick Answer

Yes. IT consultants usually need professional indemnity insurance when their work involves advice, implementation decisions, or software outcomes that could be linked to client loss. The practical move is to confirm your services match the policy definition, test limits and excess against your strictest client contract, and verify exclusions in writing before you bind. Keep records of scope, approvals, and acceptance evidence so you can respond quickly if a dispute turns into a claim.

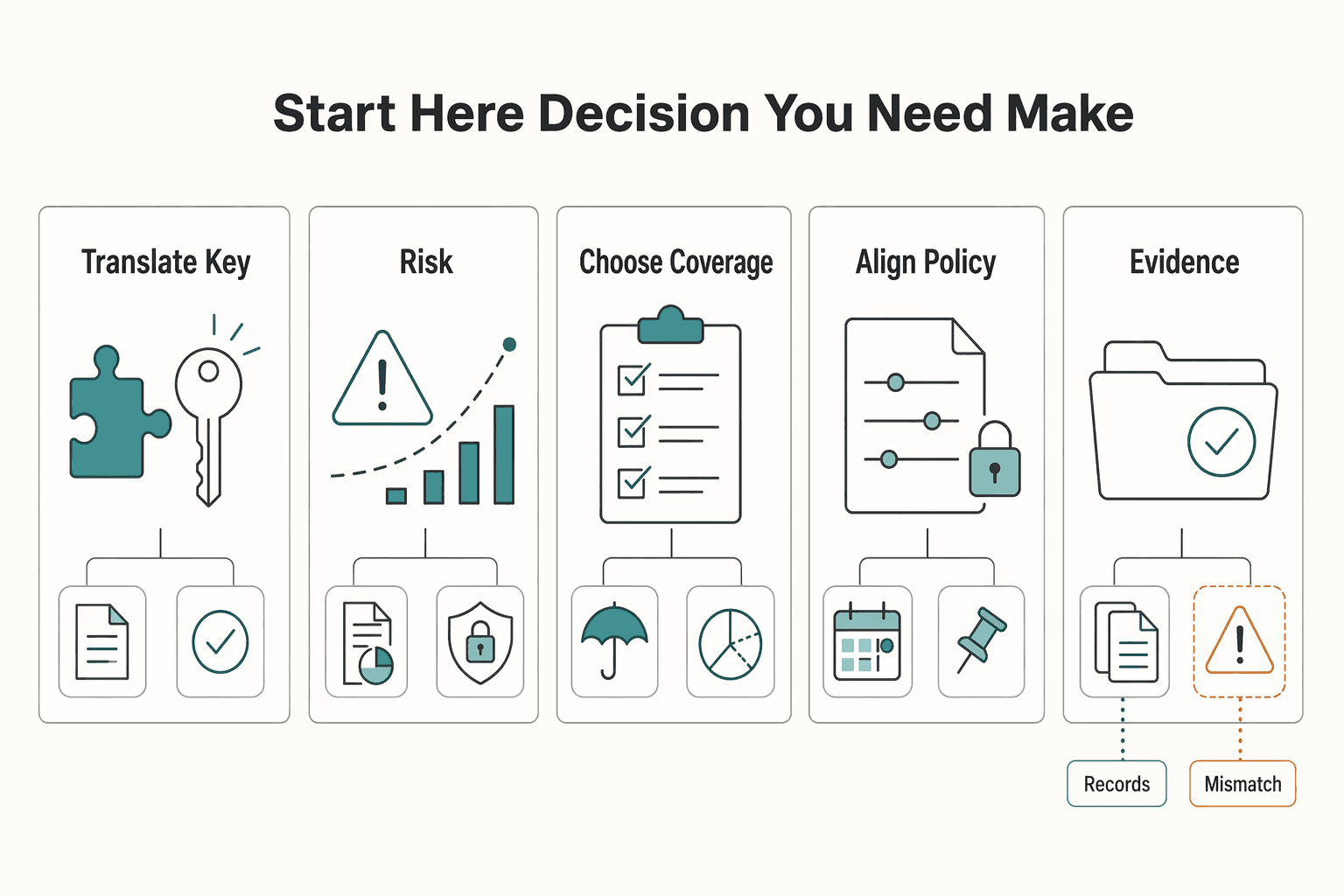

Start here with the decision you need to make#

If your brief is professional indemnity insurance it consultant, make the first call practical: choose cover that matches the services you deliver, the contracts you sign, and the cash risk you can carry. Claim reality matters more than label language because allegations about negligence, mistakes, or misinformation can trigger defense costs and damages under policy terms, including disputed claims.

Independent consultants usually juggle three pressures at once: proving coverage when a client asks, controlling premium spend, and keeping delivery on track. A useful rule is to insure your current scope first, then adjust when services, client profile, or contract terms change.

Start by mapping your risk lane before you compare quotes. Common IT exposures include negligence allegations, disputed outcomes from advice, and incidents tied to data handling. Professional liability insurance, often described as errors and omissions (E&O), is built for service-related allegations and can sit inside a broader coverage stack.

Before kickoff, confirm you can produce current proof of coverage that matches contract requirements. Then compare quotes with care. Published guidance notes that pricing varies by coverage mix, business size, and work type, so a lower number can reflect narrower protection rather than better value.

Use the rest of this guide in this order:

- Translate key terms so policy names do not hide practical differences.

- Build a risk model around your actual services and client types.

- Choose coverage layers without paying for overlap.

- Align policy wording with contract obligations before work starts.

- Keep disciplined project records to support dispute response.

- Recheck limits and fit during annual reviews.

If you want one immediate action, start a simple decision file now. Put three items in it: your side-by-side quote comparison, your contract alignment check, and your evidence pack checklist. Keeping those together turns renewal from a rushed purchase into a controlled decision. By the end, you should have a clearer setup, stronger client conversations, and fewer surprises when pressure is highest.

Define the key insurance terms before you compare quotes#

Compare policy wording before you compare labels. For IT consulting, names like professional indemnity, professional liability, and E&O often refer to the same practical coverage family, but wording still decides what is actually covered.

At a working level, this cover responds to client allegations tied to errors or omissions in professional services or advice. Policies are commonly described as paying legal defense costs and, where terms allow, settlements and judgments.

The term map helps with buying conversations, but it is not a legal shortcut. Treat naming as orientation and policy text as authority. If two insurers use similar naming but different definitions of professional services, those quotes are not equivalent.

Before you compare price, check each quote against your work and client contract:

- Confirm your services fit the policy definition of professional services.

- Check how legal defense costs, settlements, and judgments are treated.

- Review exclusions, especially intentional fraud and physical injury.

- Confirm the named insured matches the contracting party.

Capture this review in one page you can reuse. Record the exact wording points that matter, the unclear clauses you need clarified, and the final written responses. That one page is often the difference between a clean buying decision and a last-minute guess. The objective is straightforward: match policy language to your delivery model and contract obligations, not just to a familiar product name.

Understand where IT consultant claims usually come from#

A claim can center on an allegation that your work caused client loss. That can happen even when you believe delivery was reasonable.

In IT-focused wording, allegation patterns include professional negligence, negligent misstatement or misrepresentation, and software not being fit for purpose. These are claim types worth planning for, not assumptions to treat as universal across every policy.

Separate delivery disagreement from legal exposure. A scope dispute can escalate into a legal-cost issue. Some policy wordings state that costs and expenses are paid in addition to the indemnity limit, but confirm how your own quote handles this before you rely on it. Use a simple trigger test:

- If your role includes recommendations, check how misstatement allegations are handled.

- If your role includes implementation decisions, assume negligence allegations are possible.

- If your role includes software outcomes, verify treatment of fit-for-purpose allegations.

Scenario contrast helps here. A short advisory engagement can still produce a claim if a client alleges your recommendation caused loss. Ongoing support can produce a similar claim when delivery outcomes are disputed. Different service models, similar practical legal risk if client loss is alleged.

Project advisory and ongoing support can fail in different ways, but both can still produce negligence-based claims. The practical move is consistent documentation of scope, assumptions, and acceptance so your records match how work was delivered.

Before you send a proposal, ask two checks: what allegation could follow from this service, and what document would prove what was agreed. Those two checks push clearer scope and better record discipline before work starts.

Know what professional indemnity usually covers and what it does not#

Treat professional indemnity as two linked protections: defense against service-related allegations and payment of established legal liability for client financial loss, up to the indemnity limit. That is the baseline, and policy wording decides the final boundary.

You will also see this sold as professional liability insurance or errors and omissions insurance. Use those labels as orientation only, and check the policy wording for the actual scope. One explainer groups cover this way:

- Defense costs: legal costs to respond to allegations tied to negligence, error, or omission in professional services.

- Legal liability: payable amounts when liability is established, up to the indemnity limit.

Contractual promises are one place to check closely. If a contract promise is broader than what the policy wording treats as covered professional services, a coverage gap can follow. You need policy language and contract language to point in the same direction.

Do not assume one policy covers every risk. Exclusions and conditions vary, and common examples include dishonest or fraudulent acts and contractual liability.

Use one buying rule across every quote. If wording is unclear for a scenario you are likely to face, treat it as not covered until you receive written confirmation.

Build a complete insurance stack without paying for overlap#

Build your stack by risk type, not by product name. Each major risk should have one primary policy home. If two policies appear to cover the same event, verify how each policy responds in the wording. If neither clearly responds, you may have a gap. Set boundaries this way:

| Exposure | Primary policy or action |

|---|---|

| Negligent advice, design mistakes, or project-management errors tied to financial loss | Professional liability insurance (professional indemnity) |

| Third-party bodily injury and property damage from day-to-day operations | General liability insurance |

| Other material exposures | Run a risk assessment first and decide whether they are insurable before assigning a policy |

Professional liability insurance(professional indemnity) for service-related allegations such as negligent advice, design mistakes, or project-management errors tied to financial loss.General liability insurancefor third-party bodily injury and property damage from day-to-day operations.- In contractor contexts, keep both general and professional liability active where relevant. Standard CGL forms commonly exclude professional services, so one does not replace the other.

- For other material exposures, run a risk assessment first and decide whether they are insurable before assigning a policy.

Do not stop at labels when you do overlap checks. Combined products and endorsements can look complete in summaries but still leave gray areas once wording is read line by line.

Before binding, run one mapping checkpoint and document it:

- List your top risks in plain language.

- Map each risk to one primary policy and note why.

- Flag any secondary policy that might also respond, then verify boundaries in endorsements.

- Add one non-insurance control per risk, such as tighter scope language or a clearer contract clause.

- Save the map with definitions, exclusions, and endorsements for renewal review.

This wording-level overlap check is where duplicate spend and silent gaps can appear. If a risk cannot be mapped cleanly, treat that as an unresolved issue and get written clarification before purchase.

Choose limits and excess with clear decision rules#

Set limits and excess from your highest-risk accepted work, not your average project. Start with the strictest client contract you are willing to sign, then record a repeatable rule so decisions stay consistent at each renewal.

Review contract insurance clauses before comparing quotes. Pull required limits, trigger language, and claims-handling conditions. Your minimum viable limit should satisfy your highest-stakes engagement. If one contract requirement is materially higher, treat that requirement as your floor unless you decline the work.

For claims-made cover, timing matters. The policy in force when the claim is made is typically the one that responds. Lowering limits at renewal can reduce what is available for later claims tied to earlier work. One published example shows a reduction from £10,000,000 to £3,000,000. In that case, a later £7,000,000 claim had only £3,000,000 plus costs available.

Choose excess based on cash resilience. If one defended claim could disrupt operations, set an excess you can absorb and confirm how legal-defense costs are treated. Defense costs can consume meaningful limit before trial, so stress-test your numbers against that failure mode.

Use a tiered rule by service profile:

- Lower-exposure, narrow-scope work can sit at the lower end of your range.

- Higher-exposure or contract-heavy work should push limits higher.

- Where potential settlements and dispute costs rise, limits should rise with that exposure.

Keep a one-page limits rationale and refresh it before binding and renewal:

- Highest client contract requirement and the clause that sets your minimum.

- Current limit and excess, with one sentence on fit for your cash position.

- Service tiers and which tier drives peak exposure.

- Worst credible settlements scenario and how much insurance should absorb.

- Defense-cost treatment in wording, plus unresolved clarifications in writing.

Add one more checkpoint to keep decisions stable: note which engagements you will accept at current limits and which you will decline. That turns limits into an active risk boundary, not a number chosen once and forgotten.

Review this page at least annually, and sooner when services, clients, or scope change. If you lower limits, record which work you will no longer accept.

Check policy wording before you buy#

Limits and excess are only useful when wording matches your actual work. Verify before purchase, not after a claim. Read the full policy pack as one contract: wording, statement of fact, schedule, and endorsements.

Start with definitions and scope. If the policy is split into sections, confirm where your services sit (for example, Professional Indemnity versus Public Liability) and flag ambiguity before binding.

Then check claims mechanics. In claims-made-and-notified wording, cover applies to claims first made during the policy period and notified to the insurer. Confirm notification duties and process in writing.

Next, test exclusions and conditions against real scenarios you handle. Do not assume technology disputes are covered by default. Do not assume the split between Section 1 (Professional Indemnity) and Section 2 (Public Liability) resolves gray areas by itself. Use this verification sequence:

- Shortlist suitable options.

- Compare definitions, claims conditions, and exclusions line by line.

- Mark unclear clauses tied to your real delivery work.

- Get written clarifications and keep them in the policy file.

- Treat verbal assurances as non-final.

Two failure points to watch for are relying on wording that is not in bound documents and incomplete disclosure. Changes only take effect when confirmed in writing, and non-compliance with policy obligations can reduce payment or lead to claim refusal.

Control the final handoff before you pay. Confirm the bound schedule and endorsements match the version you reviewed, confirm clarifications are attached in writing, and confirm your internal file has one complete copy. This is basic document hygiene, and it helps prevent post-purchase surprises.

If wording is unclear on a material scenario, pause and resolve it in writing before you buy. Related: A Guide to Securely Wiping Your Devices Before Selling Them.

Align insurance with contracts and scope control#

Before kickoff, align contract promises and scope language with what the policy actually covers. IT consulting firms often work inside clients' critical systems and support systems tied to revenue, compliance, and operations, so unclear scope language can increase dispute risk.

Treat contract and scope documents as risk controls. As a practical approach, define deliverables, limits, client responsibilities, and completion criteria in terms both sides can test. Useful checkpoints in engagement documents can include:

- Acceptance criteria that state how work is evaluated, who signs off, and when.

- Dependency assumptions that state required client inputs or access and what happens if they are delayed.

- Change control terms that state how scope or timeline changes are approved before extra work starts.

Watch for red flags before signature. Outcome promises that are broader than your actual control, vague completion language, and open-ended remedy language can create obligations your policy wording may not fully match.

Run a pre-kickoff reconciliation: compare material promises in contract and scope against policy wording, conditions, and exclusions. If a promise is broader than your cover, address it in writing before work starts.

Keep one internal rule: no kickoff until contract terms, scope, and insurance assumptions are reconciled in writing. Once terms are aligned, the next step is proving delivery followed those terms, which is why your evidence pack matters.

Build a claim-ready evidence pack before anything goes wrong#

Build the evidence pack at project start, not after a dispute. Contract and policy alignment only helps if you can show what happened, in sequence, with signed records. Defense costs alone can reach tens of thousands of dollars in some professional liability claims, so missing records can get expensive early.

| Evidence item | What to include |

|---|---|

| Signed scope and contract set | Core terms, addenda, schedules, exhibits, pricing attachments, and the exact scope version used at kickoff |

| Insurance package | Policy wording, statement of fact, schedule, and endorsements, where applicable |

| Approved change records | Date, approver, and updated deliverable or timeline |

| Acceptance records | Test evidence, sign-off emails, and acceptance conditions |

| Key client approvals | Access, architecture choices, and risk decisions |

| Advice trail artifacts | Recommendations, options considered, assumptions, and client responses |

Keep each engagement as one complete record, not scattered files. Store the full signed contract set together, including core terms, addenda, schedules, exhibits, and pricing attachments, plus the exact scope version used at kickoff. Store the insurance package with it: policy wording, statement of fact, schedule, and endorsements, where applicable.

Use one standard evidence pack for every project:

- Signed scope and contract set, including all addenda and attachments.

- Approved change records with date, approver, and updated deliverable or timeline.

- Acceptance records, including test evidence, sign-off emails, and acceptance conditions.

- Key client approvals for access, architecture choices, and risk decisions.

- Advice trail artifacts: recommendations, options considered, assumptions, and client responses.

For contested incidents, preserve chronology. Keep timestamped deployment notes, incident tickets, and remediation logs to support incident narratives. If records are corrected, keep both versions and note why.

If inaccurate advice or misrepresentation is alleged, communication records do heavy lifting. Preserve what you recommended, which alternatives you presented, which assumptions you stated, and what the client approved.

Keep policy-change evidence in the same repository. Most professional liability policies are claims-made, and policy changes in this type of wording only take effect when confirmed by the insurer in writing.

Fragmentation is a failure mode. Assign one repository of record and run a monthly completeness check. If you cannot quickly produce signed scope, current change approvals, acceptance proof, and current endorsements, treat the project as not claim-ready and close gaps immediately.

A practical monthly test keeps this manageable. Can you retrieve the signed scope and latest approved change set within minutes? Can you show acceptance evidence tied to the same deliverable version? Can you show the current endorsement set without hunting through old threads? Can another team member find the same documents without your help? If any answer is no, the pack is incomplete and should be fixed before the next client milestone.

Handle United Kingdom and United States differences without guessing#

Do not treat UK and US insurance language as interchangeable. Translate terms, then verify contract wording and policy wording separately before you sign.

UK materials may use professional indemnity insurance. US materials may use professional liability insurance or errors and omissions (E&O) insurance for overlapping service-risk categories. E&O language is tied to claims about mistakes, oversights, or failures in service delivery, but naming similarity does not prove identical cover.

A useful reminder from the legal sector is that, in SRA-regulated legal practice, rules require cover that is adequate and appropriate, with profession-specific minimums for law firms (for example, compulsory primary cover can be £2m or £3m under SRA minimum terms). That shows how jurisdiction and sector can change expectations. It is not a direct benchmark for IT consulting.

For cross-border work, confirm terms in writing instead of relying on labels. Use this pre-signing checklist:

- Obtain broker or legal review of how policy terms interact with contract terms in each jurisdiction.

- Obtain written insurer confirmation for territorial scope, jurisdiction assumptions, and notification expectations.

- Align contract language to confirmed policy terms.

- Store confirmations, endorsements, and the signed contract set in your evidence repository.

It also helps to keep a short internal glossary in your contract file. Map each term used by the client contract to the equivalent wording in your policy documents. That reduces misunderstanding when multiple parties review the same engagement across jurisdictions.

Run an annual review that keeps coverage current#

Treat renewal as a risk decision, not admin. Professional indemnity insurance is typically renewed annually, and because it is usually claims-made, the policy in force when a claim is notified is the one that responds.

Use trigger events to set review depth, for example new services, larger clients, higher-risk sectors, and material operating changes. When those change, avoid auto-renew by default. Keep one renewal checklist and update it line by line:

- Risk changes since last renewal, tied to real engagements.

- Contract changes, especially liability wording and proof-of-cover clauses.

- Policy wording changes, including notification conditions and exclusions.

- Retained-risk changes, including any self-insured retention.

- Unresolved exclusions or ambiguous clauses that need escalation before binding.

- Whether your wider insurance stack still fits exposure, and which non-PI risks are handled separately where relevant.

Review wording carefully because scope can differ across insurers. Start with what professional indemnity is intended to cover, then confirm where boundaries sit so out-of-scope risks are handled separately or accepted knowingly.

Test claims-readiness during renewal: can you produce a complete evidence pack and current proof of coverage quickly for contract review? Retrieval speed matters because clients may ask for proof before they commit.

Use claims-made timing as a practical check: a claim notified in 2020 for work done in 2015 is handled under the 2020 policy. Maintain coverage through the liability period, and close or explicitly accept checklist gaps in writing before binding.

Finish each renewal with a short decision note. Record what changed, what remained unresolved, and what you will verify next cycle. That simple note builds continuity and prevents repeating the same review questions every year.

Make your next insurance decision with confidence#

Choose for claim reality, not label language. The right decision comes from what allegations are covered, what costs are paid, and what reporting duties apply.

A dispute can become expensive before any final ruling. Covered policies can include legal defense costs, settlements, and judgments, and uninsured costs can exceed $100,000 even when a case does not go to trial. In technology consulting, claims can follow alleged service interruption or data loss linked to your recommendations.

Before your next renewal or proposal, use one side-by-side comparison sheet with only decision-critical fields:

| Decision field | What to capture | Red flag |

|---|---|---|

| Policy form | Whether wording is claims-made and the reporting and notification timing requirements | Late notice is treated as harmless |

| Scope definition | How the policy defines your professional services versus what you actually deliver | A core service is missing or vague |

| Limit baseline | Compare quotes on a common baseline, for example $1M per claim / $2M per policy term where available | Limits are copied without checking fit |

| Quote assumptions | Revenue, location, and service profile used for each quote | Prices are compared across different assumptions |

| Operational factors | Bundled coverage, COI speed, and purchase path | Buying speed outweighs wording quality |

Treat headline pricing as orientation, not a final answer. One published comparison shows a $21.00 starting monthly figure and normalizes quotes to a common limit baseline where possible. The same comparison also notes that pricing changes with profile details like location and annual revenue.

Before binding, document the assumptions behind each quote and get written clarification whenever terms or reporting duties are unclear.

If you want a practical final sequence, do it in this order: finish the comparison sheet, confirm claims-made reporting requirements, and verify that each quote uses comparable assumptions. That keeps your insurance decision tied to real delivery risk, not a headline quote.

Frequently Asked Questions

Is professional indemnity insurance the same as E&O for IT consultants?

Usually yes in day-to-day usage. Professional liability insurance is commonly described as errors and omissions insurance, and both refer to cover for mistakes in professional services. The exact trigger and scope still depend on the wording and form of the policy you buy. Treat naming as shorthand, because differences in definitions, conditions, or exclusions can still change practical protection.

Do IT consultants need professional indemnity if they already have a signed client contract?

A signed contract does not replace insurance. Contracts define responsibilities, but they do not pay legal costs if a claim is filed. This cover is not universally required by law, but client requirements often drive the need to carry it. In practice, clients may still ask for current proof of coverage before work starts.

What does professional indemnity for IT consultants usually cover?

It generally responds to allegations tied to professional services and can help with legal costs if you are sued. Common allegation themes include negligence, misrepresentation, inaccurate advice, and failure to protect personally identifiable information. Final scope depends on your specific terms, limits, and conditions. When you compare options, check both defense-cost treatment and legal-liability wording because those details shape real claim response.

What is usually not covered under professional indemnity policies?

Do not assume one policy covers every business risk. Professional indemnity does not automatically include cyber liability, public liability, or general liability. This source set also does not provide a complete exclusions list, so policy wording needs a direct review. The safest approach is to test likely scenarios against your actual wording and get written clarification where language is unclear.

Do IT consultants also need public or general liability and cyber liability insurance?

Often they need to be considered separately because these policies address different risk types. Professional indemnity focuses on service-related allegations and does not automatically include those other covers. The right stack is usually shaped by contract requirements and your operating risk profile. Map each major risk to one primary policy so you can see overlap and gaps before you bind.

How should a solo IT consultant choose policy limits and excess?

Use contract requirements as a starting point, then test whether those numbers match your delivery risk. Choose an excess you can absorb without disrupting operations if a claim arrives. Recheck both at renewal as your services and client profile change. Keep a one-page rationale so your limit and excess decisions stay tied to service type, contract pressure, and cash resilience.

How much does IT consultant professional indemnity insurance cost, and what is still unknown from public quote pages?

Public quote pages are useful for rough orientation, not final pricing. You may see examples like $21 per month, $229 / year, a comparator such as $87 a month, and sample limit structures like $1M / $2M. What is often unclear from those summaries is policy form and full coverage boundaries, so headline price should be treated as a first signal only. Compare quotes only after you confirm like-for-like assumptions and policy wording, then verify terms before you rely on the price.

Try a related tool

A former tech COO turned 'Business-of-One' consultant, Marcus is obsessed with efficiency. He writes about optimizing workflows, leveraging technology, and building resilient systems for solo entrepreneurs.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- acus.gov/sites/default/files/documents/1993-03%20Peer...trusted

- ecfr.gov/current/title-2/subtitle-A/chapter-II/part-200trusted

- michigan.gov/dtmb/-/media/Project/Websites/dtmb/Procureme...trusted

- rules.house.gov/bill/119/hr-3838trusted

- johnheath.com/professional-indemnity-insurance/it-consulta...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Canada Digital Nomad Visa Planning for Visitor Status and Work Permits

The phrase `canada digital nomad visa` is useful for search, but misleading if you treat it like a legal category. In this draft, it is shorthand for existing Canadian status options, mainly visitor status and work permit rules, not a standalone visa stream with its own fixed process. That difference is not just technical. It changes how you should plan the trip, describe your purpose at entry, and organize your records before you leave.

Securely Wipe Devices Before Selling Them With Clear Risk Checks

Make one call before you touch the device: choose a wipe level that matches the risk, then document each step you complete. That keeps your decisions consistent when you are under pressure from a buyer, a trade-in deadline, or a handoff date.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.