Quick Answer

Freelancers in India can use Section 44ADA when their work is eligible professional service activity, gross receipts fit the stated limits, and their records support the section choice. In the cited guidance, 50 percent of gross receipts is treated as income, but you should first classify income under PGBP, compare 44ADA with actual-profit filing, reconcile invoices to bank credits, and handle advance tax and TDS cleanly.

Build a defensible Section 44ADA filing path#

For a globally mobile freelancer, a safer tax move is the one you can defend six months later, not the one that feels fastest this week. Start with classification under PGBP, test whether Section 44ADA actually fits your facts, then file with records that support every major number you report.

Section 44ADA can reduce bookkeeping effort because a fixed share of receipts is treated as income. In the guidance used here, that share is 50 percent of gross receipts for eligible professionals. That simplification helps when eligibility and receipt totals are documented clearly.

Thresholds are condition-based. The material here cites Rs. 50 lakhs for 44ADA and Rs. 75 lakhs linked to fully digital sales conditions. Treat those as gates you must prove, not headline numbers you can assume.

Before filing pressure builds, lock three calls in writing:

- Confirm whether 44ADA is genuinely available for your activity and receipt pattern.

- Reconcile gross receipts to invoices and bank credits before you run final tax math.

- Escalate early if section choice or income classification is not clear in one paragraph.

That sequence keeps you from doing clean math on a weak legal position. It also reduces late-stage edits when return numbers and supporting papers do not line up.

A failure pattern to avoid looks like this: the section is chosen first for convenience, then receipts are adjusted to fit the choice, then evidence is gathered late. Reverse that pattern. If classification and reconciliation come first, computation and filing become far less stressful.

Start with the terms that decide your filing path#

Many filing errors start before calculation. They begin with terms chosen loosely, then spread into wrong method, wrong evidence, and avoidable rework.

| Term | Meaning |

|---|---|

| Presumptive Taxation Scheme | Income is computed on a deemed percentage of turnover or receipts instead of a full expense-led profit build. |

| Section 44ADA | A presumptive option for eligible professionals where 50 percent of gross receipts is treated as profit in the cited guidance. |

| Section 44AD | Another presumptive lane, but not a casual substitute for 44ADA when income is professional in nature. |

| Actual profit method (ITR-3) | An alternative where you show real income after subtracting actual expenses. |

| PGBP and Return of Income | Freelance earnings are treated under Profits and Gains from Business or Profession, and filing discipline still applies even when computation is simplified. |

Use a tight baseline vocabulary:

- Presumptive Taxation Scheme: Income is computed on a deemed percentage of turnover or receipts instead of a full expense-led profit build.

- Section 44ADA: A presumptive option for eligible professionals where 50 percent of gross receipts is treated as profit in the cited guidance.

- Section 44AD: Another presumptive lane, but not a casual substitute for 44ADA when income is professional in nature.

- Actual profit method (ITR-3): An alternative where you show real income after subtracting actual expenses.

- PGBP and Return of Income: Freelance earnings are treated under

Profits and Gains from Business or Profession, and filing discipline still applies even when computation is simplified.

Use a fixed order so decisions stay consistent:

- Classify income under

PGBP. - Decide whether presumptive filing (with the relevant section) or the actual-profit method fits that classification.

- Reconcile receipts to source records.

- Run the computation method tied to that classification.

- Prepare the return from reconciled numbers only.

If you reverse that order, you can end up forcing classification to match a number you already prefer, which often weakens the return.

Thresholds also need written context. The same receipt total can lead to different treatment if the condition behind the threshold is not met. Near Rs. 50 lakhs or Rs. 75 lakhs, include a short note on why your condition is met, what records support it, and which receipt figure was used.

Keep one classification note with these fields:

- Income type and why it belongs under business/professional receipts under

PGBP. - Section selected and why other section options were rejected.

- Gross receipts figure used for the decision.

- Threshold condition relied on.

- Link to invoices, bank credits, and return workings.

Simplified computation does not mean record-free filing. Even where detailed books may be reduced within presumptive limits, your receipt trail still needs to be easy to follow. If facts do not fit presumptive treatment, fuller books and additional compliance requirements may apply.

A practical check before you move to return drafting: ask whether a reviewer who has never seen your records can follow your classification note in one read. If the answer is no, the note is still too vague.

If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

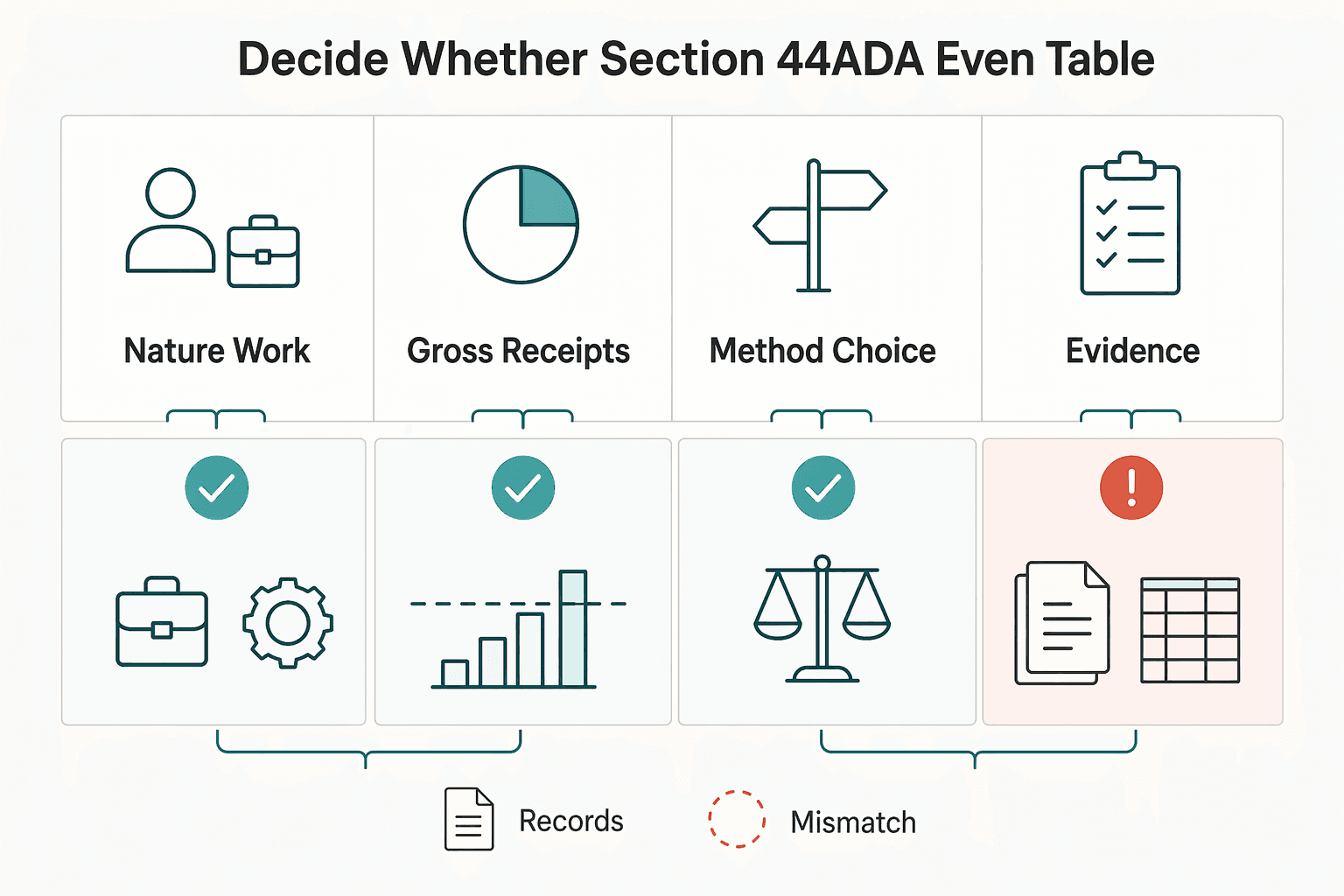

Decide whether Section 44ADA is even on the table#

Treat 44ADA as an eligibility gate, not a convenience option. If fit is uncertain, pause before you compute tax.

| Checkpoint | What the article says |

|---|---|

| Nature of work | Service-based professional activity, such as writing, design, consultancy, or similar services. |

| Gross receipts | Within the stated Rs. 50 lakh gross receipt limit. |

| Method choice | You are intentionally choosing the 50 percent presumptive method and can explain why. |

| Record trail | Receipts can be reconciled to your records, such as invoices and bank entries. |

In the cited material, 44ADA is presented as a simplified route for service-based professional work, with a Rs. 50 lakh gross receipt limit and deemed income at 50 percent. That means the first job is proving fit, not jumping to the 50 percent number.

Use this as a pre-check, not a definitive legal eligibility test:

- Your work is service-based professional activity, such as writing, design, consultancy, or similar services.

- Gross receipts used for the year are within the stated limit.

- You are intentionally choosing the 50 percent presumptive method and can explain why.

- Receipts can be reconciled to your records, such as invoices and bank entries.

If any item above is unclear, do not force a yes. Move to an advice step and get a written view.

A practical way to reduce mistakes is a one-page 44ADA memo:

- Nature of services and client mix.

- Gross receipts figure and reconciliation reference.

- Section selected and reason for selection.

- Known edge points you want documented.

- Signature and date for your own audit trail.

That memo does not replace legal advice. It does something equally useful for daily execution: it keeps your filing logic stable when you revisit the return later.

Use these red flags as practical escalation triggers:

- Receipts include both professional services and a different business stream.

- The reconciled receipt total changes late in the process.

- Bank credits do not map cleanly to invoices.

- You cannot explain section choice in plain language without caveats.

44ADA can reduce detailed books and tax-audit burden when facts fit. It does not reduce your burden to explain why the facts fit.

If you are unsure what "clear fit" looks like, use a short script: "My income type is X, my gross receipts are Y, my records are in Z folder, and this is why 44ADA applies." If any part of that script feels forced, pause and verify before filing.

Choose between Section 44ADA and Section 44AD without guessing#

Section choice should follow income character, not convenience. Eligibility can be unclear, so if classification is weak, the filing method is weak even if the math looks clean.

| Decision point | Section 44ADA as described in excerpts | Section 44AD as described in excerpts |

|---|---|---|

| Who it is for | Presented as a presumptive route for certain professionals | Described as a different presumptive lane where professional or freelancing activity was previously outside scope |

| Income characterization | Tied to professional receipts, with stated conditions such as gross receipts up to Rs. 50 lakhs and at least 50 percent declared profit | Not presented here as a direct substitute for professional-service classification |

| If you choose wrong | Classification may be questioned and the filing basis may need to be reworked | Similar rework may follow if mixed receipts were self-classified without support |

Hard stop rule: if your facts are partly professional and partly business, do not self-select between 44ADA and 44AD for speed. Treat that as a professional review point.

Use this pre-choice sequence:

- Label each revenue line as professional, business, or unclear.

- Tie each labeled line to an invoice and matching bank entry.

- Isolate unclear lines in a separate list instead of forcing them into one section bucket.

- Write a short section-choice note that can stand on its own.

- Seek written advice if any line remains unclear.

A short decision note can prevent drift when filing gets rushed. It should state what you chose, why it was chosen, and what evidence supports the choice. If those three points are not clear, the return may not be ready.

Tradeoff is straightforward: even if a deemed method looks simpler, weak section choice can still lead to later corrections, explanations, and disputed positions.

Add one more safeguard when facts change mid-year: revisit the note instead of patching numbers in isolation. If activity mix changes but section logic is not rechecked, mismatches can show up late during return review.

Calculate presumptive income and test it against real expenses#

Run both paths before final filing. Presumptive filing can be simpler when you are within limits, but it is not always the lower-tax outcome.

Under 44ADA, deemed profit is 50 percent of gross receipts. Under actual-profit computation, freelance earnings are treated under PGBP, and taxable income reflects actual expenses such as software, internet, home office, and travel.

| Scenario | What usually happens | Filing direction to test |

|---|---|---|

| Low-expense consultant | Actual profit can sit above the 44ADA deemed amount | 44ADA may reduce taxable income, so test it carefully |

| High-expense freelancer | Actual profit can fall below the 44ADA deemed amount | Actual-expense computation may be cheaper, so run it fully |

Use the same gross-receipts figure for both methods so the comparison stays meaningful.

A practical comparison sheet should include:

- Gross receipts used for both methods.

- Deemed profit amount under 44ADA.

- Actual expense total used for non-presumptive computation.

- Resulting taxable income under both paths.

- Final method selected and reason.

Common failure modes to avoid:

- Comparing methods with different gross-receipts figures.

- Leaving out expenses when testing actual-profit treatment.

- Choosing presumptive only because it is faster to draft.

If expenses materially change the result, that is your signal to fully evaluate both methods before locking the return. If actual-profit treatment is better on supported numbers, use it instead of defaulting to presumptive.

Keep the choice note simple: method tested, result, and reason. Short and clear is better than long and vague.

Also keep assumptions identical across both methods. If assumptions change between versions, the comparison becomes less useful.

Handle advance tax without penalty surprises#

Computation may be simplified, but payment timing is not. Even under presumptive schemes, advance-tax discipline still matters for clean filing.

Most avoidable trouble comes from timing assumptions:

- Treating presumptive filing as a single year-end task.

- Skipping estimate updates when income moves.

- Paying without preserving challan evidence.

- Filing before payment records are reconciled.

Those gaps can create interest exposure and penalty risk if not managed correctly.

Use this execution sequence:

- Estimate liability from your current profit view.

- Set reminders before planned payment points.

- Make payment and save challan proof immediately.

- Map each challan to your computation sheet.

- Recheck cumulative paid amount before return finalization.

When income shifts late, update the estimate early instead of waiting for filing week. The earlier you top up, the easier it is to control shortfall risk.

If timing is uncertain, choose the more conservative payment approach and document why. Over-documenting payment logic is usually cheaper than explaining gaps later.

Keep one payment log with:

- Date of payment.

- Amount paid.

- Challan reference.

- Period covered.

- Link to working paper.

That log turns year-end filing into a verification exercise instead of a reconstruction exercise.

A useful rhythm is a brief review after each payment: confirm posting, confirm record link, confirm updated estimate. Small checks done on time prevent large corrections close to filing.

You might also find this useful: Tax Residency in Greece: A Deep Dive into the Non-Dom Regime.

Claim deductions correctly without double counting#

Protect your return by separating income computation from deduction claims. Keep two distinct buckets and do not mix them.

Bucket 1 is income under Profits and Gains from Business or Profession. Bucket 2 is personal claims under Chapter VI-A.

For cross-border activity, set the income base first. Foreign client income is treated like business income, tax is computed in INR, and payment route does not change taxability. Residential status then determines scope: ROR is taxed on global income, while RNOR is taxed on income earned or received in India and certain India-controlled business income. If this base is wrong, deduction claims become harder to defend later.

A common failure pattern is category drift:

- Expense-side items get pushed into deduction-side claims.

- Section codes are assigned from memory instead of proof.

- One item is counted in more than one place.

- Return totals do not match supporting sheets.

Use this checkpoint:

- Keep one sheet for income-side computation.

- Keep a separate sheet for

Chapter VI-Aclaims. - Label each deduction by exact section code.

- Store proof by section code folder.

- Reconcile deduction totals to return entries before submission.

If you cannot explain a line item in one sentence as income-side or deduction-side, stop and reclassify it.

A clean split does two things at once: it improves filing accuracy now and makes any later review easier because each number has one clear home.

Before final submission, run one last duplicate check across both sheets. Even a single repeated amount can distort tax outcome and create avoidable follow-up.

Build the minimum evidence pack even when books are simplified#

Even if your filing approach is simplified, keep traceable evidence for every major return figure.

| Evidence item | What it should show |

|---|---|

| Invoice register | Date, client, amount, currency, INR value used, and receipt status. |

| Contracts, SOWs, or engagement emails | Service scope and billing terms. |

| Payment proofs mapped to invoices | Bank credits or remittance records. |

| Expense proofs | Used during method comparison before final selection. |

| Method-choice memo | Why the filing approach was selected, or why it changed. |

| Return-mapping sheet | Major return fields linked to exact files. |

India-specific recordkeeping rules are not established here, so treat this as an internal evidence standard for defensibility.

Use one controlled evidence pack:

- Invoice register with date, client, amount, currency, INR value used, and receipt status.

- Contracts, SOWs, or engagement emails showing service scope and billing terms.

- Payment proofs mapped to invoices, including bank credits or remittance records.

- Expense proofs used during method comparison before final selection.

- Method-choice memo explaining why the filing approach was selected, or why it changed.

- Return-mapping sheet that links major return fields to exact files.

Keep file names consistent so retrieval stays fast. The goal is simple: a reviewer should be able to move from a return number to its source document in one pass.

Run a readiness check before filing:

- Pick any major number from the return.

- Trace it to the working paper.

- Trace working paper lines to source documents.

- Confirm labels and totals match.

- Document any unresolved item before submission.

Treat formal review as a contingency, not a surprise. If classification is unclear, records are incomplete, or reconciliations fail, escalate before filing rather than trying to patch support after submission.

If you revise any working paper late, update the return-mapping sheet on the same day. Keeping mappings current helps prevent mismatches between final numbers and archived support.

Manage TDS credits and client paperwork#

Treat TDS reconciliation as a practical filing check. Claim credits only when they are verified against client payment records.

Tax Deducted at Source affects your final tax position. Under Section 194J, TDS can apply to payments for professional fees or technical services. You still file through ITR-3 or ITR-4 at applicable slab rates.

Before locking return figures, run a strict match:

- Keep client paperwork for each deduction entry.

- Map each TDS entry to specific invoice lines.

- Check payment proof against those invoices.

- Remove orphan entries with no invoice mapping.

- Claim verified totals, not expected totals.

Under Section 44ADA, freelancers may declare 50 percent of total receipts as taxable income. Presumptive treatment simplifies income tax compliance for eligible freelancers.

Keep one reconciliation sheet with:

- Client name.

- Invoice amount.

- Amount received.

- TDS amount claimed.

- Support reference.

If a credit is disputed or unsupported, park it for follow-up instead of forcing it into the current filing cycle. A delayed clean claim is often safer than a quick unsupported claim.

Where timing differences appear, note them clearly and keep the same treatment across return drafts. Clear notes on pending or parked items can reduce confusion when you revisit the file later.

Handle cross-border complexity before it becomes a residency problem#

Cross-border activity needs an early checkpoint. If you are resident in India, overseas client payments are foreign income and can still be taxable in India.

Withholding patterns are a common confusion point. Indian clients paying professional fees may deduct TDS at 10 percent under Section 194J, while foreign clients generally remit without TDS. No TDS on foreign receipts does not make the income tax-exempt in India, and you remain responsible for advance-tax planning.

| Client side | Typical withholding pattern | Filing implication |

|---|---|---|

| India client paying professional fees | TDS may be deducted at 10 percent under Section 194J | Track deducted tax in your India tax computation |

| Foreign client | Payment is generally remitted without TDS | Include income in India tax computation if resident, and plan advance tax |

Cross-border checks still matter. Keep a clear client and payment log tied to your return support so each receipt has clear treatment.

A practical log can track:

- Client country and legal name.

- Invoice amount and amount received.

- Whether payer was Indian or foreign.

- Whether 194J TDS was deducted.

- Advance-tax action where no TDS was deducted.

- Link to return workings and support files.

Escalate early when travel pattern, client footprint, or banking footprint is complex. Small ambiguities can become costly when residency status and foreign receipts are reviewed late.

A short monthly residency note can help when movement is frequent. Record travel changes, client-location changes, and any uncertainty while details are fresh. Early notes are easier to trust than memory during filing season.

Related: How to Handle Taxes for a Side Hustle.

Use a month-by-month compliance checklist#

Tax compliance is mostly cadence. Reconcile monthly, review quarterly, and lock decisions before filing.

Monthly reconciliation is a control practice, not a statutory filing frequency. When receipts, TDS lines, and support records are matched each month, return preparation becomes confirmation work instead of year-end reconstruction.

Advance tax follows a pay-as-you-earn logic for income without automatic withholding. If estimated annual tax liability exceeds ₹10,000 after TDS credits, advance tax is payable and should be planned during the year. Section 234B can apply at 1% per month when advance tax paid is below 90% of assessed tax, and Section 234C can apply at 1% per month when an instalment deadline is missed.

| Cadence | What to review | Checkpoint before close | Main risk if skipped |

|---|---|---|---|

| Monthly | Income, expenses, GST liability, TDS credits, advance-tax payments, and audit-threshold tracking | Each receipt ties to invoice and bank credit, and each TDS item has support | Missing records force estimates later and weaken return support |

| Quarterly | Updated profit estimate and tax payable after TDS credits | Compare paid advance tax to revised estimate and top up when short | Shortfalls accumulate and increase Section 234B and 234C exposure |

| Pre-filing | Section choice and evidence-pack completeness | Return figures tie back to workings and payment proofs | Unsupported positions or avoidable filing errors |

| Post-filing | Archive and continuity notes | Full file set and decision notes are easy to trace later | Future queries become slow and error-prone |

For FY 2025-26, the final advance-tax instalment due date is March 15, 2026, with an expectation of 100% of estimated annual tax paid by then. For eligible 44ADA filers using the cited timing approach, advance tax can be paid in one lump sum by March 15. If that approach does not apply, keep reviewing through the year so missed instalments do not compound.

A practical monthly close can be done with a short checklist:

- Reconcile invoice total to bank credits.

- Update cumulative TDS verified amount.

- Update cumulative advance-tax paid.

- Recompute current-year taxable estimate.

- Record unresolved items with owner and target date.

A practical quarterly close adds one more decision:

- Confirm whether current section choice still holds based on latest receipts and activity mix.

That single review step catches drift early, before the return is drafted.

One final discipline helps at year end: do not wait for memory to fill gaps. If any line item is uncertain during a monthly or quarterly check, tag it immediately and resolve it in the next cycle.

Conclusion#

44ADA reduces compliance effort only when eligibility, timing, deductions, and records are handled with discipline. Use it as a deliberate choice, not a default setting.

Lock your position early and document why it fits. In the material used here, 44ADA is positioned for specified small professionals, taxable income is deemed at 50 percent of gross receipts, eligibility covers individuals and partnership firms but not LLPs, and the text cites a Rs. 50 lakhs cap with a Rs. 75 lakhs condition when sales are fully digital. If your facts sit near those edges, confirm before you file.

Keep the tradeoff explicit. This route simplifies computation but disallows business-income deductions under sections 28 to 43C. If operating costs are high, do not assume presumptive treatment is better without a direct comparison. The same material states that Chapter VI-A deductions such as 80C, 80D, 80E, and 80G can still be claimed where applicable.

A strong close process is short and practical:

- Track the advance-tax trigger context at

Rs. 10,000. - Match payment timing to due milestones because delays can trigger 234B and 234C.

- Tie TDS records to final payable or refund.

- Keep receipts and workings that support each major return figure.

- Preserve a section-choice note and final method comparison note.

If classification is unclear or facts are mixed, escalate early. That is the most reliable way to keep 44ADA simple and avoid expensive cleanup later.

Final execution rule: choose positions you can explain quickly, support each position with records, and resolve uncertainty before submission. That is the difference between a clean filing year and a correction-heavy one.

Frequently Asked Questions

Can a freelancer in India use presumptive taxation under Section 44ADA?

Yes, when the facts fit the section conditions. In the guidance used here, 50 percent of gross receipts is treated as taxable income for eligible professional cases. Confirm eligibility before you compute, especially if service type or receipt classification is unclear. A short written note on why 44ADA applies can reduce rework later.

What is the practical difference between Section 44AD and Section 44ADA for freelancers?

This article supports operational use of 44ADA in professional freelance cases. It does not provide enough detail for a full 44AD comparison in mixed or unclear fact patterns. The practical rule is to classify income first, map receipts to evidence, and avoid switching sections for convenience. If revenue lines do not fit cleanly into one lane, get written advice before filing.

Is taxable income always treated as deemed income under Section 44ADA, or are there exceptions?

Under the referenced presumptive approach, taxable income is treated as 50 percent of gross receipts when 44ADA genuinely applies. The exception is eligibility itself. If your facts do not fit 44ADA conditions, do not assume the deemed 50 percent method applies. Classify income and reconcile receipts before final computation.

Do freelancers under presumptive taxation still need to pay Advance Tax, and when?

Yes. The article cites an advance-tax trigger when annual tax liability exceeds Rs. 10,000 after TDS credits. For eligible 44ADA filers using the cited timing approach, advance tax can be paid in one 100 percent payment by March 15; otherwise the cited instalment milestones are June 15, September 15, December 15, and March 15. Missed timelines can trigger Sections 234B and 234C.

Can I claim Section 80C and other deductions when I file under Section 44ADA?

This article does not provide detailed eligibility limits for 80C, 80D, 80E, or 80G. Treat deductions as a separate validation step, keep income computation and deduction support separate, and claim only amounts supported by documents. If the section code, proof, or categorization is unclear, resolve it before submission.

What records should I keep if detailed Books of Accounts are not required?

This article does not establish definitive books-of-accounts requirements. Practically, keep enough records to support each major return figure without rebuilding the year from scratch. A useful baseline is gross-receipt support, TDS support, advance-tax challans, computation workings, and a clear mapping from return numbers to working papers and source files.

When should I stop self-filing and talk to a professional?

Stop self-filing when your residential status is unclear, because tax scope depends on whether you are ROR, RNOR, or NR for the year. Seek help when your day-count position is close to key residency tests, including the 182-day condition and related multi-year tests. Also escalate when section choice is unclear, receipts are mixed, or your facts are hard to classify before filing.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 4 external sources outside the trusted-domain allowlist.

- irs.gov/publications/p17trusted

- freefincal.com/who-is-eligible-to-pay-tax-only-on-50-of-inc...external

- jiraaf.com/blogs/taxation/freelancer-income-tax-filing-...external

- pnbmetlife.com/articles/taxation/how-section-44ada-simplifi...external

- taxbuddy.com/blog/section-44ad-44ada-how-presumptive-taxa...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

How to Handle Taxes for a Side Hustle

If you want less stress at filing time, use sequence instead of shortcuts. When one year includes payroll income, contractor income, and time in more than one country, the order of operations matters. This guide gives you a defensible path so you can make each decision once, document it, and avoid rebuilding the return later.

When Greece Non-Dom Tax Residency Fits a Solo Consultant

Use this guide as a go-or-no-go compliance filter, not a shortcut. It is for globally mobile freelancers and consultants who want a practical way to decide before committing to a Greece tax-residency path.