Quick Answer

Start by treating departure as a compliance sequence, not a travel task list: set tax home and domicile evidence first, choose your legal structure, then lock records and reporting workflows. Use Form 2555 to map your FEIE path, keep a day-count file that can support the 330-day test, and run FBAR and Form 8938 checks separately. Book flights only after visa, transit, insurance, and document-retrieval checks are complete.

Phase 1: Fortify Your Legal & Financial Core (Before You Think About a Plane Ticket)#

Start here, not with flights. Decide your tax home and domicile, choose your legal structure, set up your account-reporting workflow, and check residency risk. If any of those four pieces are unclear, wait to book travel.

Decide your tax home and domicile first#

Action: Map where you expect to live and work for your first 12 months, then test that plan against Form 2555 rules. Outcome: You know whether you may have a viable FEIE path later, instead of assuming travel alone qualifies you. Why this matters: The IRS requires your tax home to be in a foreign country during the qualifying period. FEIE eligibility takes more than being outside the U.S.

| Check | Rule | Note |

|---|---|---|

| Tax home | In a foreign country during the qualifying period | FEIE takes more than being outside the U.S. |

| Physical presence test | 330 full days during any period of 12 consecutive months | Time-based path |

| Bona fide residence path | Uninterrupted period that includes an entire tax year | One year abroad does not automatically qualify |

| State domicile check | New York reminder: you can only have one domicile | State tax rules are not the same as FEIE rules |

For the time-based path, the physical presence test is about time abroad: 330 full days during any period of 12 consecutive months. The bona fide residence path is different. It requires an uninterrupted period that includes an entire tax year, and the IRS says living abroad for one year does not automatically qualify you.

Before you leave, start a day-count file. Keep entry and exit dates, lodging records, and a calendar that ties where you were to where you worked. If you later claim FEIE on Form 2555, that log is far easier to defend than a reconstructed timeline.

Also run a separate domicile check, because state tax rules are not the same as FEIE rules. New York's definition is a useful reminder: you can only have one domicile. Do not assume leaving the U.S. changes state residency by itself. Verify your own state's rules and build evidence before departure.

Choose the simplest legal structure that matches your risk#

Action: Choose your structure before you sign new client work abroad. Outcome: You understand tax treatment, liability exposure, and admin load before you move. Why this matters: Business structure affects taxes, paperwork, financing, and personal liability.

| Structure choice | Best fit | Admin burden | Risk profile | Escalate to a licensed advisor when |

|---|---|---|---|---|

| Sole proprietorship | Solo work, low complexity, fastest start | Low | Highest personal exposure because business and personal liabilities are not separate | You are signing larger contracts, taking debt, or need clearer separation |

| Single-member LLC | Solo work with a formal entity | Moderate | Liability outcomes depend on facts and law; do not assume complete personal-liability protection in every scenario | You are unsure about state formation, multi-state issues, or tax elections |

| Multi-member LLC or LLC with tax election | Partners, alternative federal tax treatment, or higher complexity | Higher | More moving parts; filing risk rises if handled casually | You are adding owners, considering corporate treatment, or operating across jurisdictions |

A common mistake is assuming an LLC creates one fixed federal tax result. IRS treatment depends on member count and elections. If your choice may change who reports income or which returns are due, get licensed advice before departure.

Treat banking convenience and compliance as two different jobs#

Action: Open the accounts you need and build your reporting tracker at the same time. Outcome: You can operate abroad without losing compliance visibility. Why this matters: Useful apps and cross-border accounts do not remove U.S. reporting obligations.

For U.S. persons, FBAR can apply when the aggregate value of foreign financial accounts exceeds $10,000 at any time during the calendar year. FBAR is FinCEN Form 114, filed with FinCEN, not the IRS, due April 15 with an automatic extension to October 15. It can apply even if accounts produced no taxable income.

Do not treat FBAR and Form 8938 as substitutes. They are separate requirements. For specified individuals living outside the U.S., Form 8938 thresholds differ by filing status. The thresholds are $200,000 / $300,000 for unmarried or married filing separately, and $400,000 / $600,000 for married filing jointly. Validate current rules for your filing status and jurisdictions before departure, especially if you use non-U.S. brokerages or hold foreign financial assets beyond checking accounts.

Keep account-opening confirmations, monthly statements, and a running balance log from day one. FBAR records generally need to be kept for five years from the due date.

Check residency risk before you book a base#

Action: Test each likely destination against its own residency rules before committing to long stays. Outcome: You reduce the chance of accidental tax residency. Why this matters: There is no single universal 183-day rule.

Some countries use a day threshold as part of their test. Spain cites habitual residence when someone remains there for more than 183 days during the calendar year. Australia also uses a 183-day test, but the ATO states it is only one of the tests used. In dual-resident cases, treaties may apply sequential tie-breaker tests.

So do not rely on visa status or forum shortcuts. Before you stack stays or extensions, review the destination's residency rules and relevant treaty notes for your case. For a deeper reset on this topic, read 183-Day Rule Explained: Stop the Tax Myths Before They Cost You.

This is where tax and legal planning starts to affect daily operations. The next phase is about making your business hold up under real travel conditions.

Use this compact compliance tracker:

| Item | Trigger/check | Due date window | Keep on file |

|---|---|---|---|

| U.S. income tax return | U.S. filing obligation applies | April 15 regular due date; eligible taxpayers abroad may get automatic extension to June 15 | Return workpapers and supporting records |

| Form 2555 | Claiming FEIE or housing benefits | With your U.S. return | Day-count log, travel calendar, support for tax home and qualifying period |

| FBAR (FinCEN Form 114) | Foreign accounts exceed $10,000 aggregate at any time in the year | April 15; automatic extension to October 15 | Account statements and balance evidence, generally 5 years from FBAR due date |

| Form 8938 | Threshold met for your filing status and residency category | With your U.S. return | Asset and account records supporting the threshold test |

| State return or exit filing | State-specific rule | Add after verification | State residency and domicile evidence file |

| Destination-country filing/registration | Country-specific residency and filing rules | Add after verification | Local test notes, deadlines, required documents |

You might also find this useful: The 'Digital Nomad's' Annual Financial Review Checklist.

Before you book flights, pressure-test your move plan against tax-residency exposure. That keeps your timeline and compliance steps aligned: Use the tax residency tracker.

Phase 2: Engineer Your 'Business-of-One' Operational Stack#

Build this before you leave. Your work continuity depends on a setup you can run under pressure. Visas, taxes, and documentation are part of operations now, so do not let your tools turn into a random pile of apps.

Build in order, then test weak points#

A durable setup starts with the work you must do reliably, not the software you happen to like. Build from the core tasks outward, then test the handoffs before you depend on them from abroad. Weak controls can fail before strategy has a chance to work.

- Choose tools by requirement. Start with what you must do reliably: invoice, collect, sign, store, and control access.

- Configure handoffs. Make sure signed scope flows into invoicing, payment proof, and records without guesswork.

- Test failure points. Run a test contract and invoice, confirm exports, and test account recovery while assuming you are abroad.

- Document ownership. Keep a control sheet with tool name, purpose, owner, recovery method, and retention setting.

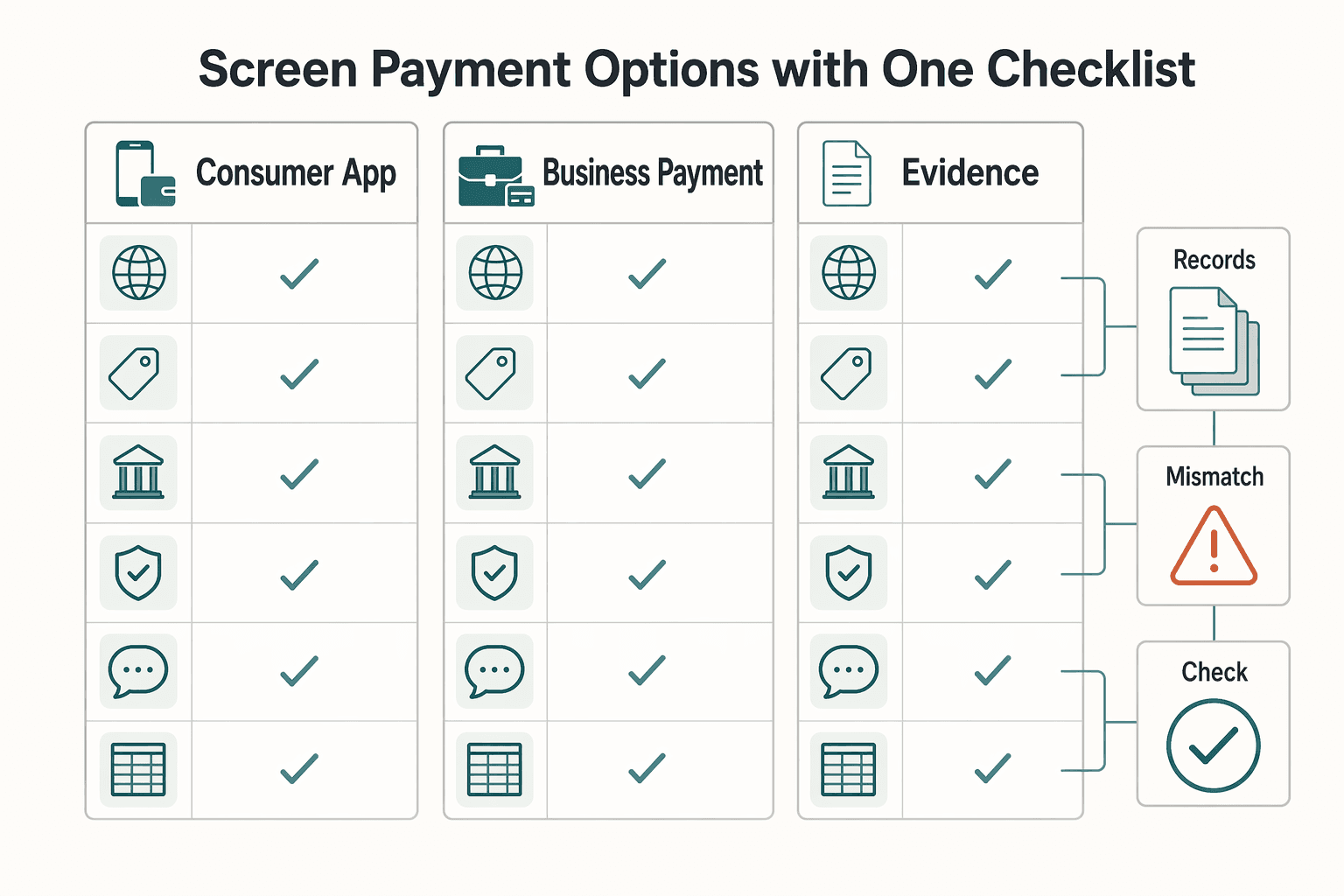

Screen payment options with one checklist#

Run the same checks on every option: supported currencies, fee transparency, tax-handling scope, payout reliability, dispute workflow, and accounting export compatibility. If those answers are unclear in provider documentation, treat that as operational risk.

| Platform type | Best fit | Verify before committing | Main tradeoff |

|---|---|---|---|

| Consumer app | Potential fit for low-volume, occasional collections | Business-use terms, invoice quality, currency support, fee visibility, dispute path, export options | Often faster setup, but lighter business controls |

| Business payment stack | Potential fit for ongoing B2B invoicing and repeat work | Currency coverage, payout consistency, reconciliation and export workflow, access controls | More setup, with potentially stronger operational control |

| Merchant-of-record model | Potential fit when you want a provider to run more of the billing layer | Contract scope, payout flow, customer experience, retrievable records | Less direct control over parts of billing |

Make contracts a repeatable workflow#

Ad hoc contract handling can break down quickly once you are moving. Use one contract path so scope, signatures, and invoicing stay tied together.

| Control | Requirement |

|---|---|

| Master template | Keep one master template and controlled edit access |

| Version history | Track version history so the current document is obvious |

| Signature rules | Check current signature acceptance requirements for your common jurisdictions, then log exceptions for review |

| Signed-record package | Store the signed file, signature audit trail, version, send and sign dates, and referenced scope or pricing attachment |

| Invoice source | Generate invoices from the signed scope, not memory |

Operate a real records system and basic incident response#

If you cannot find a document quickly, you do not really have a records system. Use a fixed folder structure, close records monthly, and keep your security steps simple enough that you will actually follow them.

Use this folder structure, then close records monthly by archiving finals, reconciling missing items, exporting key files, and noting any unresolved rules as items that must be verified from the relevant official source, provider, policy, or adviser record before use.

- 01 Clients & Contracts

- 02 Invoices & Payment Confirmations

- 03 Expenses & Receipts

- 04 Travel and Proof of Location

- 05 Tax and Compliance

- 06 Security, Access, and Incident Notes

For security, keep controls simple and consistent: enable 2FA on critical accounts, use a password manager, encrypt devices, and maintain an encrypted backup. If an account or device is compromised, revoke sessions, rotate credentials, preserve logs, and follow any notice steps only after you verify current requirements.

For a step-by-step walkthrough, see The Pre-Launch Checklist for a Digital Product.

Phase 3: Execute the Logistical Wind-Down (The 'Easy' Part)#

This phase is your final execution gate. Move here only after Phases 1 and 2 are stable, because logistics should confirm readiness, not patch legal, tax, or records gaps.

Buy medical coverage that matches the trip you are actually taking#

Treat policy selection as a fit check, not a checkbox. U.S. Medicare and Medicaid do not pay for care outside the United States. Travelers are usually responsible for paying medical costs out of pocket at most destinations, so confirm exactly how claims are handled before departure.

Medical evacuation is a major cost risk: it can exceed $100,000. Also verify insurance rules on the official destination authority page, since visa standards differ by country and program.

| Policy type | Coverage scope | Common exclusions or limits | Claims workflow | Visa compatibility | Portability |

|---|---|---|---|---|---|

| Travel health insurance | Trip-based medical care while abroad | Coverage details vary by policy; verify exclusions and limits from the policy, and confirm any visa-specific insurance requirement from the official destination source before purchase. | Prefer policies that can pay hospitals directly, not reimbursement only | May work for short stays; do not assume long-stay visa compliance | Typically tied to a defined trip |

| Global health policy | Longer-term medical coverage (scope varies by policy and region) | Terms vary by plan and country; verify limits, carve-outs, and covered regions from the policy before relying on it. | Verify direct billing and claims steps before departure | Can still fail visa rules unless verified country by country | Portability depends on covered regions and policy terms |

| Medical evacuation coverage | Emergency transport to a higher-capability hospital | Primarily transport coverage; confirm treatment boundaries and authorization limits in the policy before relying on it. | Confirm trigger rules and authorization steps | Do not assume this alone satisfies visa insurance requirements | Useful add-on when transport to a higher-quality hospital may be needed |

Turn document prep into a recovery plan#

Your goal is recovery under stress, not just scanned files. Prepare password-protected digital copies of documents that would halt travel, work, or identity verification if lost, and keep redundant copies in separate locations.

Include at least: passport, visa approval, insurance policy or card, and your core tax, banking, and business records. Keep one secure copy accessible to you, one password-protected backup, one physical copy set separate from originals, and one copy set with a trusted person.

Run a retrieval test before departure:

- Open key files on your phone and a second device with your primary laptop unavailable.

- Confirm your trusted contact can find the right folder quickly.

- Confirm passport validity lead time early. Some countries require at least 6 months beyond travel dates.

- If timing is tight, remember that urgent passport appointments are handled within stated windows: 14 days, or 28 days when a foreign visa is needed. Appointments are not guaranteed.

Close your domestic footprint in blocks#

Do not shut down your U.S. life one loose task at a time. Work in blocks, assign an owner, and only mark a block complete when the proof is in hand. Use one tracker with Owner / Action / Status, and only mark green when each block is fully verified.

| Block | Owner | Action | Status |

|---|---|---|---|

| Housing and assets | You | Close lease or handoff, document condition, sell or store major items, save proof | Green when keys are returned and related autopays are off |

| Financial accounts and subscriptions | You | Cancel location-bound services, download final statements, confirm which accounts stay active | Green after one clean billing cycle with no unexpected charges |

| Communications continuity | You | Confirm your working contact channel and account-recovery path, then enroll in STEP for embassy or consulate alerts and emergency contact support | Green after a successful test call or security-code test |

| Mail and compliance handling | You + trusted contact | If moving abroad, submit USPS change-of-address in person at a Post Office, file Form 8822 for IRS mailing-address changes, and set an FBAR reminder if you are required to file | Green after a scanned test letter is received and reviewed |

Use bookings as the final go or no-go gate#

Bookings should confirm that your plan is ready, not force it forward too early. Book your first flight and first month of accommodation only after the control checks are done. Use this go or no-go check. If any answer is no, delay booking and close the gap first.

- Insurance matches your stay type and is verified against official destination rules.

- Passport validity and entry window are confirmed, including Schengen's 90 days in any 180-day period, if relevant.

- Critical documents are retrievable without your primary device.

- Mail, communication, and account-recovery tests passed.

- Domestic closures are complete enough that you are not exporting unresolved problems.

If you want a deeper dive, read The 2025 Global Digital Nomad Visa Index: 50+ Countries Compared.

Your Pre-Departure Checklist is a Launchpad, Not a To-Do List#

Your checklist is complete only when it proves you can operate legally and financially after departure, not just reach the airport. The point is to build control across tax setup, business operations, and exit logistics so avoidable gaps do not turn into expensive problems once you are abroad.

Phase 1 sets the legal and tax foundation. Before you leave, confirm whether your tax home can be in a foreign country during the qualifying period. Also confirm which FEIE path you are actually planning around: the physical presence test, 330 full days in 12 consecutive months, or a bona fide residence timeline that includes an uninterrupted period covering a full tax year.

Phase 2 makes the business runnable from anywhere. If you are self-employed, you need quarterly estimated-tax operations and records that clearly show income and expenses. You also need a defined foreign-account review process for FBAR when aggregate foreign account value exceeds $10,000. Your process should reflect that FBAR is filed separately from your tax return and electronically through FinCEN.

Phase 3 is the final execution check. Confirm destination visa and entry requirements, review local laws for transit stops, and verify passport timing with mailing lag included, not just processing windows. If health coverage is part of your plan, check for coverage gaps and schedule pre-travel health planning at least 4-6 weeks before departure.

| Phase | What you set up | Risk it controls | What to confirm before departure |

|---|---|---|---|

| Legal and tax setup | Tax-home position, FEIE path, filing workflow | Weak tax position and timing errors | Which qualifying path you are relying on and how you will meet its timeline |

| Systems | Quarterly tax operations, recordkeeping, FBAR review process | Reporting gaps, weak records, and avoidable compliance misses | Records clearly show income and expenses; FBAR trigger and filing path are documented |

| Logistical exit | Visa and entry checks, transit-law checks, passport timeline, health prep | Entry friction, document delays, and insurance surprises | Destination and transit requirements are verified and passport timing still works |

You are ready to launch if...#

- You can state the exact basis of your tax plan and show how you are tracking the required timeline.

- You have a working system for quarterly estimated taxes and organized records that clearly show income and expenses.

- You have reviewed FBAR exposure against the $10,000 aggregate trigger and documented the electronic filing path through FinCEN.

- You have written and verified jurisdiction-specific items, including your destination visa basis, local-law requirements, entry requirements for each transit stop, and passport validity rule, using official sources or adviser records before departure.

When these checks are verified, you are not just ready to depart. You are ready to keep operating once travel becomes day-to-day life. Related: The Ultimate Pre-Travel Checklist for Digital Nomads.

Once your pre-departure checklist is locked, you can set up a cleaner way to invoice clients and manage cross-border payouts while you are abroad. You can Explore Gruv for freelancers.

Frequently Asked Questions

How can I keep a usable US business address while living abroad?

Address handling requirements vary by provider and institution, and this grounding pack does not establish one universal setup. Before you leave, confirm accepted mail types, scan and forward timing, and run one live test with real mail. Do not assume one provider will satisfy every bank or client without verification.

What’s the difference between a traveler’s checklist and a business pre-departure checklist?

A traveler checklist is mostly about personal convenience and entry readiness, while a business checklist is about continuity and document readiness. If a destination asks for proof of onward travel, missing it can create entry friction, and skipping your first week or two of accommodation can add avoidable arrival stress. If your business records and notice handling are weak, the fallout usually lasts longer than a rough arrival day. | Decision area | Traveler checklist intent | Business checklist intent | | --- | --- | --- | | Personal convenience vs continuity risk | Prioritize flights, bags, SIM, and short-stay setup | Prioritize notice handling, record access, and organized files | | Operational continuity | Get settled quickly | Keep client work, invoicing, and response workflows running | | Documentation readiness | Travel documents and onward-travel proof if requested | Retrievable business records, payment evidence, and identity backups | | If missed | Delays and rebooking stress | Missed notices, payment friction, and weaker continuity |

What’s the best way to track my days for tax residency and Schengen limits?

Confirm country-specific day-count thresholds with the relevant authority. Use a consistent log of your travel dates and keep supporting records in one folder (for example, boarding passes, stamp photos, booking confirmations, and accommodation invoices). Review regularly against current local rules, and escalate to a qualified cross-border advisor when your plans or stay length changes. For common misconceptions, see 183-Day Rule Explained: Stop the Tax Myths Before They Cost You.

Do Wise or Revolut accounts belong in my foreign account reporting review?

Treat these accounts as review items, verify reporting requirements for your jurisdictions, and keep monthly statements plus balance records from day one.

What is the cleanest way to receive larger client payments internationally?

There is no single cleanest setup supported here. If you are choosing between a Merchant of Record and direct invoicing, verify legal and tax implications for your jurisdictions before deciding. Do not switch providers right before departure without testing settlement timing, payout access, and client-facing receipts.

What are the first steps to reduce the risk of becoming a tax resident somewhere by accident?

Start before arrival: map your dates and commitments country by country, then verify current rules for each jurisdiction in your plan. Review your employment contract and rental agreement early, because even a natural lease end may still require written notice. Examples like two to four weeks’ job notice are only starting points, not universal rules. Escalate quickly if plans shift, lease-break costs appear, or time-zone pressure from client work extends your stay beyond what you intended.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- irs.gov/businesses/small-businesses-self-employed/re...trusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- pmc.ncbi.nlm.nih.gov/articles/PMC12212517trusted

- sba.gov/business-guide/launch-your-business/choose-b...trusted

- tax.ny.gov/pit/file/pit_definitions.htmtrusted

- travel.state.gov/en/international-travel/planning/checklist.htmltrusted

- travel.state.gov/en/international-travel/planning/guidance/in...trusted

- wwwnc.cdc.gov/travel/page/insurancetrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The 2026 Global Digital Nomad Visa Index for 50+ Countries

Start with legal fit, not lifestyle filters. The practical order is simple: choose a route you can actually document, then decide where you want to live. That single change cuts a lot of wasted comparison work and stops you from falling in love with places that were never a real filing option.

Digital Nomad Pre-Travel Checklist for Long-Stay Moves

Set your departure dates first. Long-term travel planning breaks down when timing stays vague. Vague timing usually turns into rushed paperwork, rushed bookings, or unresolved home obligations.

183-Day Rule Tax Myths That Trigger Residency Filing Mistakes

If you are a mobile freelancer or consultant, start here: the "183 day rule tax" idea is not a single universal test. It is a shortcut phrase people use for different residency rules that do not ask the same question. If you mix federal and non-federal residency logic, you can create filing risk even when your travel calendar looks clean.