Quick Answer

Start with residency under Article 3(1a) of the PIT Act, using either the centre-of-vital-interests test or presence in Poland for more than 183 days in the tax year. Next, classify income by source before any PIT calculations, confirm who actually remitted monthly amounts, and keep dated support records across travel, contracts, invoices, and payments. If two countries can treat you as resident, apply treaty conflict rules before filing and record the basis for your position.

Start with residency, not rates#

Start with your likely Polish tax residency status, because many later tax decisions depend on it. In practice, tax in Poland for foreigners is often less about memorizing rates and more about getting status, income scope, and documentation in the right order.

For freelancers and consultants working across countries, the practical sequence is simple: classify residency first, map income second, then handle filing. Under Article 3(1a) of the PIT Act, residency is based on at least one condition, not both. The test looks at your centre of personal or economic interests in Poland, or your presence in Poland for more than 183 days during a tax year. If you treat both tests as mandatory, you can misclassify your status from the start.

After the domestic check, add the treaty layer. Poland's residency provision is applied with regard to double taxation agreements to which Poland is a party, so domestic wording alone is not always the final answer. That treaty layer is the same issue covered in How to Legally Avoid Double Taxation: A Freelancer's Guide to Tax Treaties.

This guide stays practical. It gives you a decision sequence under Polish income tax law and shows where to pause for professional advice. If your facts point in different directions, treat that as a sign to document your position carefully and get written advice before you file. Poland's official guidance on tax residency and scope of tax liability for natural persons, issued on April 29, 2021, is a useful checkpoint for testing your assumptions.

Learn the two terms that control your tax outcome#

Your tax outcome starts with status, not rates, because status determines the scope of income Poland can tax and the return logic you should use.

| Term | What it means in practice |

|---|---|

| Polish tax resident status | Unlimited tax liability in Poland, with potential worldwide income taxation. |

| Non-resident tax status | Limited tax liability, generally focused on income earned in Poland. |

This is the gatekeeping step under Article 3(1a) of the Personal Income Tax Act. If you classify status incorrectly, your PIT return logic can be wrong from the start. Misclassification can also lead to amended returns, foreign income disclosures, and double taxation when two countries both treat you as resident or treaty rules are misapplied.

Use this sequence: lock status first, then calculate tax, then assemble documents. Write down the status you are claiming, why you are claiming it, and the date it applies. If your status changed during the year, document when that change happened. That timing point often drives the rest of the file.

Keep a practical minimum evidence pack with:

- a dated note of your resident or non-resident position

- the effective date of any status change

- the income categories you believe are in scope in Poland

- the facts you rely on, kept consistent across your records and your return

If your facts point in different directions, pause before filing and get written advice. Fixing status after filing can be harder than getting it right upfront.

Are you a Polish tax resident this year#

Start with this rule: under Polish income tax law, meeting either residency test can put you in resident status. If either test is likely met and your facts are mixed, treat the case as higher risk before you file.

Resident status means potential unlimited tax liability and declaring worldwide income in Poland. Non-resident status means limited tax liability and generally declaring only income from sources situated in Poland.

Use this yes or no sequence#

- Centre of vital interests

Is your centre of personal or economic interests in Poland? If yes, or likely yes, you are in resident territory under the domestic rule.

- More than 183 days in Poland in a fiscal year

If not, check physical presence. Spending more than 183 days in Poland in the fiscal year is a separate residency trigger.

- If two countries both treat you as resident, stop and resolve it

Use the relevant double taxation agreement conflict rules before finalizing your filing position.

Pre-filing decision table#

| Trigger | Documentation to support your position | Potential pitfall | Practical filing confidence (editorial) |

|---|---|---|---|

| Centre of vital interests in Poland | A consistent fact pattern showing your personal or economic life is centered in Poland | Treating one fact as decisive and ignoring the full pattern | Higher when most facts point one way, lower when ties are split |

| More than 183 days in Poland in a fiscal year | A documented day count for the fiscal year | Using rough estimates or the wrong period | Higher when records clearly exceed 183 days, lower when the count is close or incomplete |

| Two countries claim residency | Domestic analysis plus treaty conflict review | Assuming one domestic rule ends the analysis | Low until treaty review is completed |

That confidence column is filing discipline, not a legal threshold.

Two consultant scenarios#

A consultant with strong personal or economic ties in Poland may still have their centre of interests in Poland even with frequent travel. In that case, the domestic residency case can be strong without relying on day count.

A consultant with weaker long-term ties in Poland may still become resident if they spend more than 183 days there in the fiscal year. If they stay below that threshold and their centre of interests is clearly elsewhere, the domestic case for non-resident status is stronger.

Verification checkpoint before filing#

Before you lock status, make sure one status story holds across your records. If your records point in opposite directions, escalate before filing.

If you need formal confirmation of Polish tax residence, the revenue office can issue a tax residence certificate on CFR-1. It can support your documentation, but it does not replace treaty analysis when dual residency applies.

Map your income sources before you calculate any tax#

Once residency is set, classify income in buckets before you touch rates. Separate what is Polish-sourced, what is foreign-source, and what needs treaty review before it goes into your Polish Personal Income Tax (PIT) work.

Do not classify income by client location alone. Official guidance points to work and residence facts, with treaty conditions where relevant, so payer location by itself is not enough.

Status changes the map#

Your residency status sets the scope of review. If you are a Polish tax resident, you generally declare all income in Poland under unlimited tax liability. If you are non-resident, you generally declare only income from sources situated in Poland under limited tax liability.

Use this order every time: confirm status first, then classify each income line. If you reverse that order, the same item can be misclassified. Quick check: can you explain each income item in one sentence without relying only on the client address? If not, the map is not ready.

Common income types for first pass PIT review#

| Income type | What to ask first | First-pass PIT classification note |

|---|---|---|

| Economic activity or freelance service income | Where was the work performed, and what is your residency status? | Do not classify by client country alone. Work and residence facts come first. |

| Employment income | Where was the work performed? | Official examples anchor this: work performed in Poland for a Polish employer is declared in Poland; work performed in your country of residence for a Polish employer may be declared abroad, depending on facts and treaty conditions. |

| Rental income | Is this rental revenue rather than service or salary income? | Keep it as a separate bucket in PIT review. Rental is listed among revenues that may be subject to lump-sum taxation. |

| Sale of securities or shares | Is this disposal income rather than operating income? | Treat it as a distinct category, not business revenue. |

| Sale of real estate | Is this disposal income rather than operating income? | Review it separately from service and salary income. |

This table is a first-pass map, not a legal conclusion. Cross-border items still require checking the relevant double taxation agreement against your facts.

Freeze the map before you calculate#

Write your source map before using software or sending numbers to an advisor. A short memo is enough: income item, period, where the work or asset facts point, your source conclusion, and whether treaty review is required.

An upstream failure mode is mixing client-location signals with work-location and residence facts, which can distort what you include in Poland and what you analyze under treaty rules.

Before any PIT calculation, verify the map against your records. Contracts, invoices, payment trail, and work-location notes should tell one consistent story. If they conflict, resolve that first.

Decide who remits tax each month and where freelancers slip#

After you freeze your source map, decide who actually remits money each month. Treat remittance responsibility as a verification step: confirm from your documents whether a payer withheld anything or whether you need to remit yourself.

| Status | When to use | Evidence cue |

|---|---|---|

| Payer-withheld | Set remittance status as payer-withheld based on evidence | Any statement showing withholding |

| Self-remitted | Set remittance status as self-remitted based on evidence | Reconcile what was actually paid before you close the month |

| Unverified | Use when payer handling is not established from documents | No withholding note, no contribution breakdown, and no payer statement |

Use this order every month:

- Classify each payment line as payroll-style or freelancer/B2B.

- For payroll lines, verify that social security was withheld and remitted to ZUS.

- For freelancer/B2B lines, set remittance status as payer-withheld, self-remitted, or unverified based on evidence.

- Reconcile what was actually withheld or paid before you close the month.

If you skip this check and assume the payer handled it, you can create a year-end gap with the Polish tax office.

Do not import payroll logic into freelancer invoices#

Payroll and B2B treatment are not interchangeable. In payroll arrangements, social security remittances are monthly, and the employer withholds the employee share and remits to ZUS. Source data also shows payroll contribution splits by contribution type and payer, which is exactly why payroll documents are a useful proof trail.

For freelancer invoicing, do not assume that a Polish payer automatically handled your PIT position. Verify it from documents.

Keep one monthly reconciliation log#

Keep one row per payment, tied to invoices and payment dates, with amounts in Polish zloty (PLN) where applicable.

| Field | What to record |

|---|---|

| Invoice and period | Invoice number and service period |

| Payment facts | Gross amount, currency, and PLN amount used in records where relevant |

| Payer evidence | Any statement showing withholding, plus any payroll or ZUS document if applicable |

| Your conclusion | Payer-withheld, self-remitted, or still unverified |

If money arrived but you have no withholding note, no contribution breakdown, and no payer statement, keep that line as unverified until resolved. This is what prevents filing-time surprises.

Build your filing evidence pack before return season#

Build your filing evidence pack now, not at annual PIT return time. The goal is simple: make your tax residency position, income-source classification, and monthly payment path traceable from dated records before you file with the Polish tax office.

In Poland, one residency condition can be enough. If your closer personal or economic relations are in Poland under the center of vital interests test, or you stay in Poland longer than 183 days in the fiscal year, you can be treated as a Polish tax resident with unlimited tax liability. If not, you may be taxed only on Polish-sourced income. Your documents should support the position you take.

What your working pack can contain#

| Pack item | What to keep current | Why it matters |

|---|---|---|

| Travel-day ledger | Dated entries of days in and out of Poland | Supports your 183-day residency test position |

| Contract set | Counterparties, terms, dates, addresses used | Supports income-source classification and consistency |

| Invoice register | Invoice number, period, amount, currency, payer, payment date | Connects income lines to monthly tax treatment |

| Work-location notes | Where work was performed by engagement or period | Supports source analysis and reduces misclassification |

| Status rationale memo | Short resident or non-resident rationale with dated facts | Anchors filing logic across all records |

For the center of vital interests test, use facts, not broad statements. For the 183-day residency test, make sure your ledger count matches your memo. If your count is close to 183 days, keep the timeline evidence especially tight.

Tie monthly proof to the annual return#

The annual return works much better when monthly proof is already organized. Keep payment confirmations with your invoice register and withholding conclusions so your filing position is supported.

Keep return inputs live through the year: year-to-date totals by income line, payer-withheld versus self-remitted status, and any unverified items. Poland operates a monthly tax payment system, and the annual return is due by 30 April after tax year-end (31 December), so this monthly record is what you rely on at filing time.

Red flags to stop and resolve before filing#

- contradictory addresses across contracts, invoices, banking records, and your residency memo

- missing timeline evidence for travel days, work periods, or payment dates

- resident or non-resident position changes without dated rationale and matching documents

- source treatment in your draft return that conflicts with your work-location notes

- monthly lines marked as handled by payer without withholding or payment proof

If your evidence conflicts, pause filing and resolve the conflict before submitting to the Polish tax office, including professional advice where needed.

Before filing, keep your day-count and tie evidence in one place so your residency position stays consistent across the year: Use the Tax Residency Tracker.

Treat the non-resident 20 percent point as a risk flag not a shortcut#

Treat any mention of a non-resident 20 percent rate as a trigger to verify facts, not as the answer. In non-resident cases, treatment depends on the actual fact pattern and treaty analysis, including residency and income characterization or source.

Flat assumptions fail because they force the rest of the file to fit a guess. Use your evidence pack to keep the analysis anchored in dated records and explicit treaty logic.

Two fact patterns that should not be treated the same#

| Fact pattern | What it signals | Why "20 percent applies" is not enough |

|---|---|---|

| Services clearly delivered in Poland, with timeline, contract, and delivery all aligned | Need for structured review of Polish tax exposure | You still need full status, source, and treaty analysis before final treatment |

| Mixed cross-border delivery, such as remote work, multi-country calls, or unclear place-of-performance language | Source treatment is less obvious and needs closer review | A flat assumption can overstate or misclassify taxable income |

Check treaty interaction after status and source, not before#

Treaty review is a second-layer test after you document residency and map income facts. In U.S.-Poland treaty review materials, the analysis is article-structured, including Article 4 Resident, Article 7 Business Profits, and Article 23 Elimination of Double Taxation. The practical standard is simple: be explicit about which article logic you relied on and why it fits your facts.

The guardrail to use in practice#

If someone says your non-resident service income is simply flat 20 percent, pause and verify:

- your tax residency position is documented and internally consistent

- work facts are documented by period and deliverable

- contract language is checked against delivery reality

- treaty interaction was checked and the article logic is recorded

Shortcuts are especially risky in a system described as complex and burdensome. Do not assume treaty relief applies automatically because you are taxed elsewhere. If facts are mixed, contract wording is vague, or residency remains arguable, treat the 20 percent point as a risk flag and get written advice before filing with the Polish tax office.

Use treaty relief only after status and source are documented#

Use treaty relief as a claim you prove, not your first guess. A practical default is to lock your domestic facts, then test the double tax agreement result.

Polish guidance sets out domestic starting tests: resident or non-resident status, including the centre of personal or economic interests test or spending more than 183 days in a fiscal year in Poland. Those rules are applied with treaty context in mind, and some advisers analyze DTA provisions early. In either approach, do not backfill facts after picking a treaty outcome.

Lock the domestic position before claiming relief#

Use this sequence as a practical default:

- decide resident versus non-resident status for the year

- map income as Polish-source versus foreign-source

- then test whether the treaty changes taxing rights or gives double-tax relief

If you are resident, the issue is usually worldwide income taxation and how relief is applied. If you are non-resident, the issue is usually whether Poland can tax a specific Polish-linked item, and on what terms.

Record the article logic you actually used#

Your checkpoint is not just "treaty reviewed." Keep a short note of the treaty country pair, the article path you used, and why it matches your facts. If dual residence is possible, record the treaty tie-breaker logic and facts in sequence.

| Note element | What to record | When relevant |

|---|---|---|

| Poland residency conclusion | Your Poland residency conclusion | For worldwide-income relief claims |

| Treaty country pair | The treaty country pair | For the treaty note |

| Article logic | The article logic used for residence, taxing rights, and relief | For the treaty note |

| Tie-breaker logic | Treaty tie-breaker logic and facts in sequence | If dual residence is possible |

| Relief method | Credit or exemption, where the treaty provides it | For worldwide-income relief claims |

| Eligibility evidence | A tax residency certificate | Where relevant |

For worldwide-income relief claims, keep at least:

- your Poland residency conclusion

- the treaty country pair

- the article logic used for residence, taxing rights, and relief

- the relief method used, such as credit or exemption, where the treaty provides it

- eligibility evidence where relevant, such as a tax residency certificate

Treaty treatment is not automatic just because tax was paid elsewhere. Documentation matters, and payors can deny treaty rates when conditions are not met. For U.S. treaty claims, Form 6166 is the IRS certificate used to confirm U.S. tax residency.

Watch country-pair and timing risk#

Treaty outcomes vary by country pair and method, and they can change over time. Do not copy another person's result, or last year's result, without rechecking your facts and current treaty position.

Before filing your annual PIT return in the 15 February to 30 April window, verify current treaty text and status using official national tax authority sources. If facts are mixed, dual residence is plausible, or the relief method is unclear, get the treaty position reviewed before filing.

Align immigration paperwork with tax and social contribution setup#

Run immigration, tax, and social contributions on one timeline, but keep them as separate decisions. Immigration paperwork can affect sequencing, but it does not replace tax-status analysis for Polish Personal Income Tax (PIT). Immigration requirements are jurisdiction-specific, so verify those rules separately instead of treating immigration status as proof that your tax position is complete.

Treat social security as its own lane, including ZUS and cross-border coverage. If your facts include the U.S., the U.S.-Poland social security agreement, effective March 1, 2009, is designed to reduce dual social security taxation on the same earnings. Under that framework, employees working in Poland are normally covered by Poland. For self-employed people residing in the U.S. or Poland, coverage generally follows residence. Temporary assignments of five years or less can follow a different coverage rule.

Use one integrated checklist with three tracks:

- immigration milestones and document validity

- tax-status and filing-position review

- ZUS or cross-border social-security coverage setup

If a Certificate of Coverage is needed, file early and track it. The certificate is evidence for social-security coverage, not a PIT residency determination. The SSA portal notes that missing required fields block submission, advises waiting 90 business days before follow-up, and says mailing can take up to two weeks if issued.

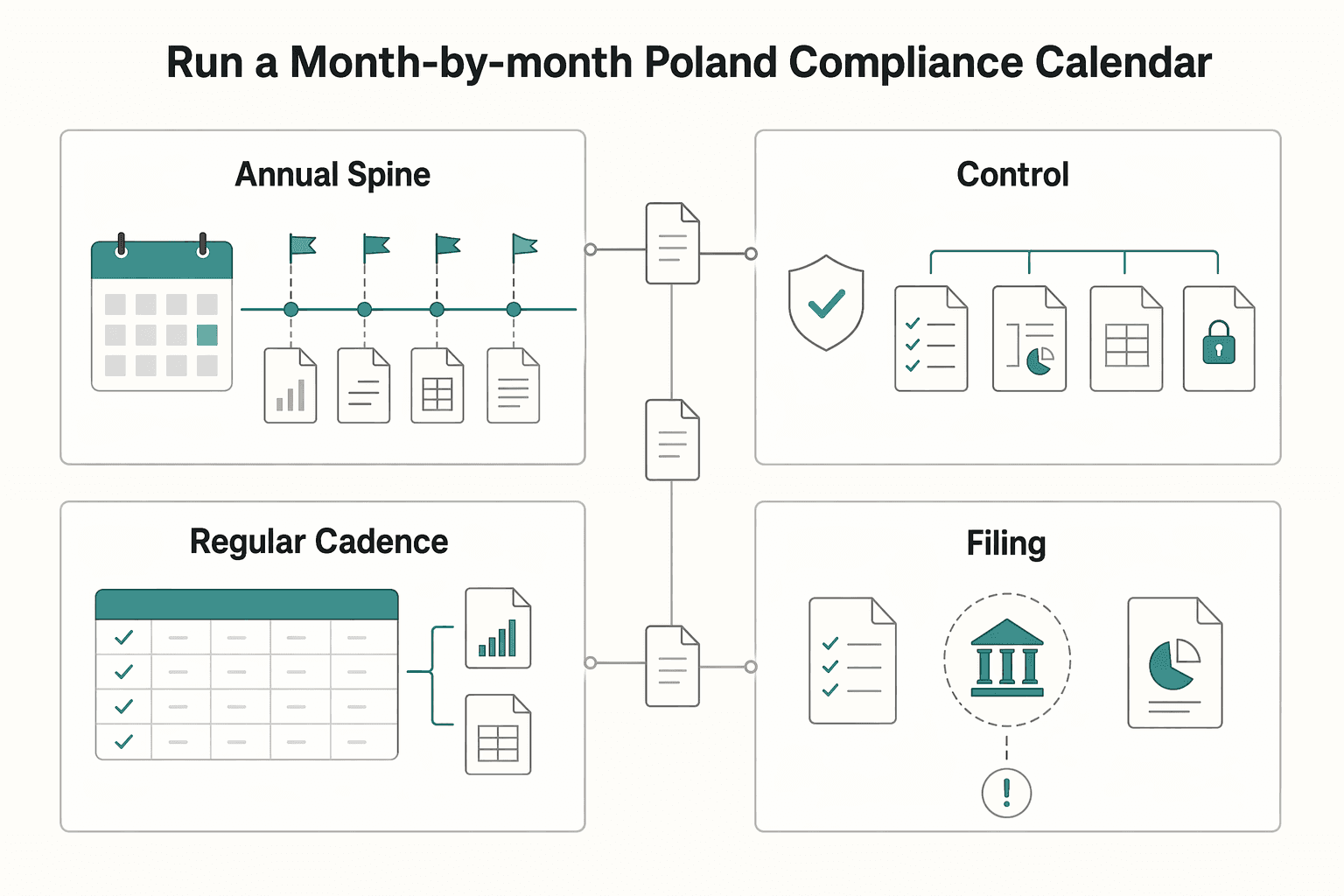

Run a month-by-month Poland compliance calendar#

Use a simple recurring calendar: one annual spine, a short monthly checklist, and a periodic fact check so filing is organized, not rushed.

| Timing | What to do | Note |

|---|---|---|

| Annual spine | Block tax year close, recurring control-review dates, and a pre-filing work window | Run the pre-filing window as a 60-day sprint |

| Monthly controls | Reconcile invoices issued against money received; verify what was actually remitted; update your residency-day count | Log major travel or location changes |

| Regular cadence (for example, quarterly) | Re-check tax residency assumptions when travel, home base, or contract mix changes materially | This is a practical control, not a legal quarterly filing rule |

| Before filing | Do one internal sign-off on your status memo, source map, and evidence completeness | Pause and resolve the mismatch if those records conflict |

Set the annual spine#

Block three anchors now: tax year close, your recurring control-review dates, and a pre-filing work window for your annual filing package. Run that pre-filing window as a 60-day sprint, not a last-week scramble.

Keep a hard boundary between personal and company obligations. CIT-8 timing and CRBR updates within 14 days are stated for KRS-registered companies. Do not add them to a solo PIT calendar unless they actually apply to your structure, and confirm any freelancer PIT deadlines separately.

Keep the monthly controls boring#

Use the same checks every month:

- reconcile invoices issued against money received, by date and amount

- verify what was actually remitted under your current setup

- update your residency-day count and log major travel or location changes

If you work across countries, note where work was physically performed while the month is still fresh.

Re-test facts before filing#

Re-check your tax residency assumptions on a regular cadence, for example quarterly, when travel, home base, or contract mix changes materially. This is a practical control, not a legal quarterly filing rule.

Before anything goes to the Polish tax office, do one internal sign-off on your status memo, source map, and evidence completeness. If those records conflict, pause and resolve the mismatch before filing.

Use Gruv records to reduce filing stress and evidence gaps#

Use one traceable record trail for operations and filing prep. Treat Gruv records as your working source of truth, then map that evidence to your filing categories with advisor review.

Start from the ledger, not from memory#

Begin with a ledger export, then classify each line in your working tax view. If you classify first and reconstruct records later, mismatch risk can increase.

Keep each income item traceable across the same core points every month: invoice, payer, payout status, and your classification note. For cross-border work, add a short note on why you mapped the item the way you did.

Run a simple monthly reconciliation before updating any tax worksheet: invoices issued, payouts received, payouts pending, and items flagged for review. If those views conflict, resolve the record mismatch first.

Preserve the references that disappear first#

Keep provider references, payout status history, and dated ledger-linked exports from the start. These items can be hard to rebuild later.

Useful habits include:

- save ledger-linked exports in dated monthly folders

- keep invoice files and payout confirmations tied to the same reference

- retain payout status history, including pending, failed, reversed, or retried states

- add short notes when classification decisions are not obvious

Build an evidence pack before you need one#

Create a monthly evidence pack and keep it immutable: export, invoice set, payout confirmations, and mapping notes together. If you reclassify later, add a dated adjustment note instead of silently replacing prior records.

A practical control is bidirectional traceability: invoice to payout, and payout back to invoice and ledger line. If that chain breaks, rebuild from the ledger export before moving forward.

Know what Gruv can and cannot do#

Where enabled, Gruv compliance and tax-document workflows can help organize records, preserve transaction history, and reduce evidence gaps. They do not replace legal interpretation of applicable tax rules.

Use Gruv to keep records clean and auditable, then have an advisor validate the filing position. If your legal view and your records conflict, treat that as a stop signal and resolve it before filing.

Conclusion#

Use this order to keep compliance low-stress: decide tax residency first, map income source second, run monthly controls third, and file once your position is documented.

That sequence changes outcomes. If you are a Polish tax resident, you are exposed to tax on worldwide income. If you are a non-resident, you generally declare only Poland-source income and are subject to limited tax liability.

Start with the residency call and make it consistent with facts you can support. Poland uses two alternative triggers: your centre of personal or economic interests, or spending more than 183 days in the fiscal year. If those signals point in different directions, treat that as a review point before filing.

Then move to source mapping and monthly control. For certain non-resident income, a default 20 percent flat tax on revenue may apply unless a double tax treaty changes the result. Where monthly PIT advances apply, use the 20th day of the following month as the remittance checkpoint and reconcile earnings, payments, and remittances as you go.

File in the annual window of 15 February to 30 April of the following year, and treat filing as confirmation, not reconstruction. If you need formal confirmation of status, the tax residence certificate is issued by the revenue office on the CFR-1 form.

For foreigners dealing with Polish tax, documented assumptions usually beat shortcuts, especially around non-resident status and treaty claims. Complete your residency decision and documentation now, then escalate only genuinely ambiguous points before filing.

Frequently Asked Questions

Who is taxed in Poland on worldwide income, and who is taxed only on Polish-source income?

Polish income-tax residency rules and worldwide-versus-source income treatment require verification. Confirm the applicable rules with current official Poland tax guidance before filing.

What exactly triggers Polish tax residency for foreigners under the center-of-vital-interests and day-count tests?

Applying the center-of-vital-interests or 183-day residency tests to your specific facts requires careful review. Verify current official tax rules with the relevant authority before drawing any conclusions.

Do freelancers in Poland need to make monthly tax advances, and how do they verify payments were made correctly?

Monthly Polish PIT advance obligations are not established in this material. Confirm what applies from current official guidance and your own payment records.

When can non-residents face a 20% tax on services, and what should be checked before relying on that rule?

Whether a specific 20% non-resident services-tax rate applies depends on scope, conditions, and treaty interaction. Verify the rate and its applicability with current tax authorities before relying on it.

What is the practical filing timeline for an Annual PIT return, and what should be prepared before deadline week?

Polish annual PIT filing dates and filing windows should be verified directly from official tax guidance before planning your calendar.

How do double tax agreements change the final tax result for cross-border freelancers?

The U.S.-Poland Totalization Agreement is intended to prevent dual social-security taxation and help address benefit-coverage gaps. Income-tax treaty outcomes for cross-border freelancers should be verified with a qualified adviser.

Do work permit, residence permit, ZUS, and social security setup affect tax compliance sequencing?

This material does not establish how permit status or ZUS setup determines Polish PIT residency. It does confirm social-security rules and process points: employees working in Poland are normally covered there, detached workers sent temporarily for five years or less can stay on home-country coverage, self-employed people are generally covered by their country of residence, and when U.S. coverage applies a Certificate of Coverage request should be complete because missing required fields can delay decisions (with follow-up typically after 90 business days and mailing up to two weeks if issued).

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- 2009-2017.state.gov/e/eb/rls/othr/ics/2013/204716.htmtrusted

- 2009-2017.state.gov/documents/organization/100326.pdftrusted

- congress.gov/119/crec/2025/09/17/171/152/CREC-2025-09-17.pdftrusted

- eg.usembassy.gov/wp-content/uploads/sites/197/2026/02/19EG302...trusted

- federalreserve.gov/publications/files/cbem-7000-202602.pdftrusted

- foreign.senate.gov/download/explanation-poland-06-19-14trusted

- govinfo.gov/content/pkg/CHRG-112shrg79797/html/CHRG-112s...trusted

- govinfo.gov/content/pkg/GPO-CRECB-1934-pt4-v78/pdf/GPO-C...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Is Poland Business Harbour Still Usable for Your 2026 Move?

You are here to make one practical call: is **Poland Business Harbour** usable for your case now, or should you switch routes? Treat this as a go/no-go decision, not a broad research exercise.

Warsaw Digital Nomad Guide for 2026 Long-Stay Moves

If you want this move to hold up under pressure, treat it like an operating decision, not a lifestyle experiment. This piece is for people planning a serious stay in Poland, not a quick city hop. Start with legal clarity, then timeline, then spending. In practice, that order prevents rework.

How Freelancers Can Legally Avoid Double Taxation With Tax Treaties

Classify the tax problem before you touch a return. If your income is mostly personal service fees across borders, this guide fits. If your issue is C corporation profits and shareholder dividends, you are solving a different problem.