Quick Answer

Run a 30-day pilot first. The philippines freelance market can work for solo operators and small teams, but only if your channel economics and payout path hold up in real deals. Start with one primary channel (for example, Upwork) and one backup (for example, Fiverr), then review close rate, cycle time to cash, revision burden, and payout success. Do not scale until each project has a complete trail from signed scope to invoice, payment reference, and payout receipt.

What Cross-Border Teams Need to Know#

This is a decision memo, not a marketplace pitch. If you are looking at the Philippines freelance market as a freelancer or a small cross-border team, the useful question is not just whether demand exists. It is whether the channel, margin, screening burden, and payment path make sense for the kind of work you actually sell.

There are enough signals to take the opportunity seriously. At least one guide-style source describes freelance work in the Philippines as gaining traction in recent years, with some of that shift tied to the move away from in-person work during the COVID period. At the same time, the evidence is mixed. Some sources are practical explainers or platform roundups, which can still be useful, but they are not the same as a market study with a clear method.

That gap matters because channel choice changes almost everything. Open-bidding platforms are often described as offering broad access to a large talent pool, but that reach comes with more vetting time. Gig-based platforms reduce bidding friction and are often better suited to project work. Direct-hire boards can remove per-transaction fees, but they usually push more of the screening and operating burden onto you. Those are not minor differences. They shape your close rate, your margin, and how exposed you are when a client turns out to be a poor fit.

A good early checkpoint is to test every strong claim against its source type. If you see a growth claim, ask whether it comes from a guide, a promotional article, or something with stated methodology. If you see a pricing or fee example, check whether it is framed as a general rule or just an illustration. One source, for example, uses a $1,000 project and a $200 service-fee deduction to show how platform commission can affect earnings. That is useful as a warning about fee drag, but it is not proof that every freelancer or every platform arrangement works that way.

The main operating risk is not that the market is fake. It is that the market is uneven, and different channels hide different costs. A platform can solve lead generation while adding fee pressure. A direct client can look more profitable until manual screening, vague scope, or payout delays eat the difference. If you do not verify the evidence behind the headline and the mechanics behind the channel, it is easy to confuse visibility with viability.

By the end, you will have a practical go or no-go checklist for three decisions that matter most: which acquisition channel fits your situation, what operating guardrails you need for cross-border work, and how to set up payment operations so invoices, receipts, and payout records are not an afterthought. The point is not to sell you on freelancing in the Philippines as a trend. It is to help you decide, with your eyes open, where the opportunity is real and where the operating risk starts to outweigh it.

Define the Philippines freelance market before you decide#

Start by defining the scope. Here, treat the Philippines freelance market as independent cross-border services, and keep it separate from managed outsourcing labels so you do not compare unlike arrangements.

If Australia is in the client chain, keep these points in view:

| Australia-related point | Detail | Source named |

|---|---|---|

| ABN eligibility | If someone is engaged as an employee, they are not entitled to an ABN for that activity | ABR |

| GST rate | GST applies to sales connected with Australia at 10% | ATO |

| GST registration timing | Once GST registration is required, you must register within 21 days | ATO |

| BAS and GST cycle for non-residents using standard GST registration | BAS lodgment and GST payment are monthly or quarterly | ATO |

| Electronic lodgment outside Australia | You cannot lodge electronically from outside Australia | ATO |

| Tax-agent support | You may need an Australian registered tax agent | ATO |

Compare one operating model at a time before you compare risk or economics:

- Solo freelancer

- Small agency

- Marketplace contractor on Upwork or Fiverr

Keep role and buyer context consistent too. Do not treat all Southeast Asia roles, rates, and expectations as interchangeable when you assess fit.

Set the legal boundary early if Australia is in your client chain. The ABR states that if someone is engaged as an employee, they are not entitled to an ABN for that activity. The ATO states GST applies to sales connected with Australia at 10%, and that once GST registration is required, you must register within 21 days (not every business must register, but penalties can apply if required registration is missed).

For non-residents using standard GST registration, the ATO says BAS lodgment and GST payment are monthly or quarterly, and notes you cannot lodge electronically from outside Australia and may need an Australian registered tax agent.

What the current evidence says and what it does not#

You can reasonably treat this market as growing, but you cannot treat any single source as a definitive national market-size method.

What is supported:

- A recurring growth narrative: a MicroSourcing article (April 24, 2025) reports "up to 1.5 million" Filipinos on international platforms and a "sixth fastest-growing" gig-market ranking.

- Policy-level attention: an April 2023 policy brief says freelancing is "booming in the Philippines."

- Practical supply visibility on international platforms: useful for channel decisions, but still a visibility signal, not a census.

What is not supported:

- A transparent, auditable method for current national market sizing.

- Independent verification of the headline figure and ranking from primary sources.

The same policy brief that describes growth also states a data gap and a legislation gap. So the direction of travel is more reliable than any precise size claim.

Before you reuse a number, check three things: publication date, counted population, and scope. "Filipinos on international platforms" is not the same as "all freelancers in the Philippines." A March 2024 study scoped to CALABARZON can inform local patterns, not national size. A November 18, 2024 mixed-method paper with 406 respondents adds operating context, including occupational health issues, but it is not a national measurement.

A confidence rubric you can actually use#

| Market assertion | Confidence | Why it sits there |

|---|---|---|

| Freelancing is growing or "booming" in the Philippines | Cross-checked claim | Supported directionally by the April 2023 policy brief and repeated in later market commentary. |

| Up to 1.5 million Filipinos freelance on international platforms | Reported claim | Reported in MicroSourcing, but no transparent sizing method is shown here. |

| The Philippines is the sixth fastest-growing gig market | Reported claim | Reported in MicroSourcing, but no independent method is shown here. |

| Current national market size can be calculated from these sources | Unknown | No auditable market-sizing method is shown here. |

| DP 2022-01 or the BusinessWorld reference settles current size | Unknown | They indicate relevance, but do not show a current sizing method you can inspect. |

Use this as your operating rule: trust cross-checked claims for direction, treat reported claims as prompts to verify, and mark anything without visible scope or method as unknown. The common mistake is turning platform visibility, promotional rankings, or subnational findings into national fact.

With that baseline in place, the next decision is practical: how you will win clients first.

For a step-by-step walkthrough, see How Small Teams Can Outsource to the Philippines Without Losing Control.

Choose your client acquisition channel with clear tradeoffs#

Choose your first channel based on your current bottleneck, not on headline claims. If you need fast lead flow, start with one marketplace; if you already have niche proof, build a direct pipeline to protect margin and fit.

Use this as an operating map, not verified benchmark data. The source base for channel performance here is largely anecdotal, user-generated, or promotional.

| Channel | Control over pricing | Lead quality (when executed well) | Dispute friction | Dependency risk |

|---|---|---|---|---|

| Upwork | Medium | Medium | Medium to high | High |

| Fiverr | Low to medium | Low to medium | Medium to high | High |

| Direct outbound | High | Medium to high | Low to medium | Low to medium |

| Referrals | Medium to high | High | Low at first; rises with unclear scope | Medium |

| Niche communities | Medium | Medium to high | Low to medium | Medium |

Failure modes to plan for early:

- Marketplaces: visibility can shift, so pipeline can swing with platform conditions.

- Direct outreach: pipeline can stay thin if niche, message, or proof is weak.

- Referral-heavy work: scope creep rises fast when boundaries are not explicit.

- Niche communities: trust takes time; hard pitching too early usually underperforms.

Before you write off any channel as "bad," run an internal evidence checkpoint: complete 10-15 real conversations or proposals, then review patterns. Treat that number as a practical decision threshold, not a validated industry rule.

Track each attempt the same way:

- buyer type

- offer sent

- response/no response

- next step reached

- reason lost (if known)

Save proof: proposal links, email threads, call notes, and repeated scope questions. That record helps you see whether the real issue is channel choice or positioning, qualification, and scope control.

Set go or no-go rules for client fit pricing and scope control#

Use a strict go/no-go rule before you sign: if the buyer cannot clearly define success, revision limits, payment timing, and change handling, do not start a full engagement.

In the Philippines, full-time freelancers are commonly treated here as self-employed independent contractors. That gives flexibility, but it does not remove dispute risk. Vague commissions or deliverables can still turn into payment, content, or brand-use conflicts.

Use a five-point acceptance check#

Before you send a contract, run a short clarity test. If any item stays unclear after a serious conversation, treat that as commercial risk.

| Checkpoint | What a good answer looks like | Red flag |

|---|---|---|

| Buyer clarity | Named decision-maker, billing entity, and one approver | Multiple stakeholders with no final approver |

| Deliverable definition | Specific outputs, format, quantity, and due dates | "Help us improve this" or "we'll know it when we see it" |

| Revision limits | Number of review rounds and what counts as a revision | "Unlimited revisions until we're happy" |

| Payment trigger | Deposit, milestone, or final payment tied to clear acceptance | Payment only after broad business results |

| Escalation path | Named contact and written method for disputes or delays | No contact beyond chat messages |

Confirm these points in writing before kickoff. A short recap email, signed proposal, or redlined statement of work is enough. If the buyer avoids written confirmation or rewrites terms loosely, treat that as a no-go signal.

Put the contract primitives in plain language#

You do not need a long contract, but you do need the right building blocks every time.

| Contract element | What it should cover |

|---|---|

| Statement of work | Exact outputs, exclusions, timeline, and client dependencies |

| Acceptance criteria | What "done" means for each deliverable |

| Change-order language | Extra requests change timeline and price |

| Termination clause | Notice, payment for work completed, and handoff terms |

| Governing-jurisdiction assumptions | Expected law, forum, and notice method |

Value-based pricing can be flexible, but scope should not be. If price is tied to expected impact, still anchor it to concrete deliverables and a finite review window.

Keep a simple evidence pack for each engagement: signed SOW, proposal version, approval emails, invoice trail, and written scope-change approvals. When disputes happen, records usually matter more than memory.

Downgrade risky deals instead of arguing#

If a buyer asks for unlimited revisions, vague deliverables, or open-ended "strategic support," do not force a full project. Shift to a paid diagnostic, audit, or discovery sprint with one output and one decision point.

This matters more in cross-border work. If you are in the Philippines and the client is in another jurisdiction such as Queensland, unstated assumptions can diverge on notices, disputes, approval authority, or termination. Make those assumptions explicit before work starts.

A practical no-go rule: if the client refuses a written SOW, rejects revision limits, or will not name who can accept the work, walk away or offer only a small paid diagnostic.

Need the full breakdown? Read A Deep Dive into the 'Assignment' Clause in a Freelance Contract.

Build a compliance and documentation baseline for cross-border work#

Your baseline should do one job well: keep documents consistent enough to survive payer checks, tax prep, and disputes as your cross-border work grows. Treat it as a system, then add a mandatory "confirm with payer and local advisor" checkpoint before recurring volume.

Use a simple document matrix by counterparty so requirements are tracked instead of guessed.

| Counterparty | Verification and compliance track | Tax-document readiness track | Evidence pack to retain |

|---|---|---|---|

| Individual client | Track KYC expectations from the payer, platform, bank, or payment rail | Confirm whether the payer requests a W-8 or W-9 and whether Form 1099 handling is relevant | Signed agreement, invoices, payout receipts, tax form copy/version, approval messages |

| Registered business client | Track KYB/AML expectations where the relationship or payment flow requires it | Confirm required tax documents before first recurring payment | MSA/SOW, invoices, remittance records, billing-entity details, tax form copy/version |

| Platform or intermediary | Follow platform-led onboarding and verification requirements | Keep profile and tax forms current in-platform and save what was submitted | Platform terms, onboarding confirmations, payout statements, verification notices |

Keep one consistency rule across all rows: names and entities should match across contract, invoice, payout account, and tax documents. When those records drift, payments and verification often slow down.

For U.S.-tax planning, keep FEIE and related flags in scope but separate from legal advice. U.S. citizens and resident aliens living abroad are taxed on worldwide income, even when some foreign earnings may be excludable, and excluded income is still reported on a return. The physical presence test is 330 full days in a 12-month period (days do not need to be consecutive), your tax home must be in a foreign country, and the 2026 FEIE maximum is $132,900 per qualifying person.

Store each client or platform evidence pack in one controlled location, mask unnecessary PII in working copies, and set written retention rules. Add a final onboarding checkpoint to confirm country-specific compliance and tax obligations with a qualified local advisor before you scale.

Once you have the documents under control, the next weak point is usually the payment path itself. Related: How to Build a 'Glocal' Marketing Strategy for Your SaaS Product.

Design a payment operations stack that survives delays and disputes#

Your payment stack should make ownership and status explicit from invoice to payout, not hide money movement in disconnected tools. That matters even more if you enter this market through the independent contractor model: it is often a lean starting point, but it puts more compliance and payment operations on you.

Map the payment sequence before you add tools#

Set one order of operations and use it every time:

| Step | What to confirm |

|---|---|

| Issue the invoice | Use a unique ID and a usable payer reference |

| Confirm receipt details | Payer name, amount, currency, and arrival date |

| Apply hold logic | Apply any hold logic, for example dispute or compliance review, before release |

| Decide conversion timing | Log the quote timestamp you used |

| Release payout | Release payout only after beneficiary details and account status are confirmed |

Do not release funds on assumptions when references do not match. Resolve the mismatch against contract, invoice, and remittance records first.

Choose the stack shape that fits your volume#

Start with the model you can operate consistently, then reduce handoffs as volume grows.

| Path | What you manage directly | Main risk |

|---|---|---|

| Separate invoicing, bank/wallet, FX, bookkeeping tools | Every handoff and status sync | More manual matching and more places for records to drift |

| Integrated rails such as Gruv Virtual Accounts + Payouts (where supported) | Provider setup plus your internal controls | Better visibility can still fail if statuses and exports are not clearly defined |

| Integrated rails plus Merchant of Record workflow (where supported) | Less direct collection admin, more provider-term dependence | Confusion over who owns charge handling, tax handling, and dispute records if roles are not documented |

Add controls that reduce rework#

If your stack exposes an API, use idempotent retries for payment and payout requests so retried calls do not create duplicates. If it supports webhooks, treat them as event notifications and reconcile final state from a single ledger source.

Plan for predictable failure modes up front:

- Stale FX quotes at conversion time.

- Unmatched deposits when payer references are incomplete.

- Failed beneficiary details from name or account mismatches.

- Compliance holds that pause withdrawals after funds arrive.

Keep the hold notice, submitted verification, and release confirmation with the payment record so you can resolve disputes without rebuilding the timeline.

Related reading: A deep dive into the 'severability' clause in freelance contracts.

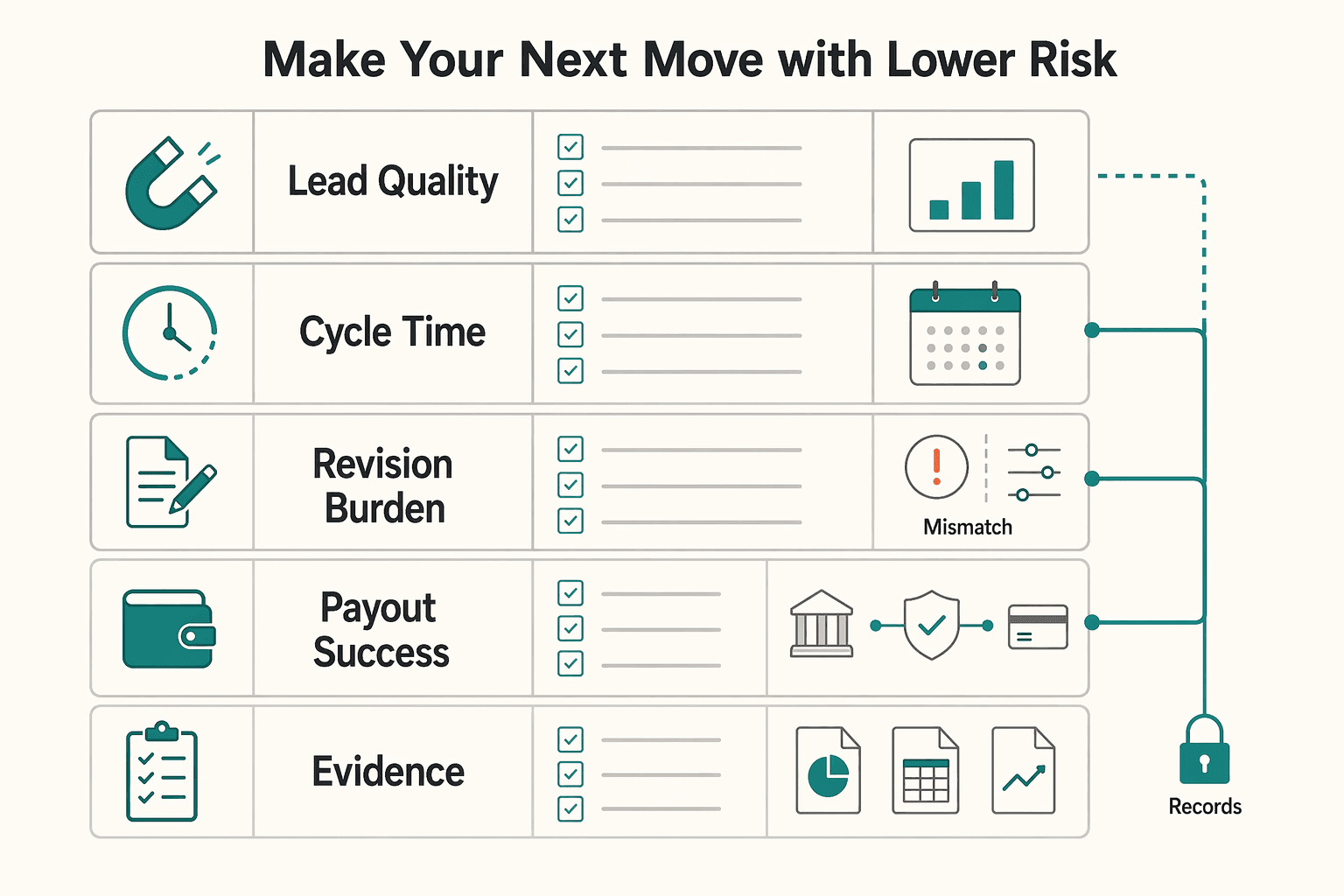

Run a 30 day pilot and score it before scaling#

Run the first 30 days as a controlled pilot, then scale only if the results stay clean. Keep the cohort narrow: one niche service, one primary channel (for example, Upwork), and one backup channel (for example, Fiverr).

A narrow setup makes decisions clearer. If you mix services and channels too early, it becomes hard to tell whether weak outcomes came from offer fit, pricing, or payment friction. Pilot-first measurement is the right standard here, but any benchmark from other contexts is directional, not universal.

Track these five metrics weekly in one sheet tied to your ledger:

- Lead quality

- Close rate

- Average cycle time to cash

- Revision burden

- Payout success rate

Apply stop rules before you add volume:

- Pause if disputes start clustering

- Pause if payment lag worsens

- Pause if documentation gaps appear in KYC/AML or tax records

Use a hard scale gate: increase volume only after two clean payout cycles and complete reconciliation across invoices, payouts, and ledger records. If that evidence trail is incomplete, keep the pilot in place and fix operations first.

Make your next move with lower risk#

Treat this as a real opportunity, but only after a 30-day pilot with explicit go/no-go rules, clean records, and a payment flow you can reconcile end to end.

The outside signals are useful context, not decision-grade proof on their own. The Feb 17, 2023 Colliers piece points to rising freelance activity alongside demand for flexible workspaces, while a 2025 growth headline appears without enough body evidence to validate the claim. Use both as directional inputs, then decide from your own operating data.

During the pilot, track:

- lead quality by channel, including how many conversations become scoping calls

- cycle time to cash, from first message to cleared payment

- revision burden, especially where vague scope creates unpaid extra work

- payout success, including failed details, holds, or unmatched deposits

- document completeness per deal: proposal thread, signed scope, invoice, payment reference, and payout receipt

Judge the pilot on proof, not activity. A first-person story can mention "$3000 a month," but that same account also says starting alone is not easy and client acquisition can take months on Upwork. If your records cannot tie each job to invoice, payment confirmation, and payout outcome, pause and fix the process before scaling.

Keep the opportunity in view, but let evidence from your own operation drive the next move. If 30 days show clean scope control, acceptable cycle time to cash, and two orderly payout paths, continue. If not, repair the weak point first.

If you need integrated Virtual Accounts, Payouts, and audit-ready records where supported, set that up before you add more volume.

Frequently Asked Questions

Is the Philippines freelance market worth entering in 2026 for solo professionals?

It can be, but this guide does not provide market-size or growth proof, so treat it as self-employment rather than a shortcut to easy income. The supported points are that freelancers are responsible for finding work and negotiating terms, and that getting started and finding clients can be tricky. If you need predictable income immediately, keep this as a controlled pilot until your own close rate, cycle time to cash, and payout flow are clear.

Which is better for starting out, Upwork or Fiverr, and when should you move to direct clients?

There is no supported evidence here that one platform is a proven winner. The better starting choice is the one that best matches how you currently sell and deliver. Start with one primary channel, then judge it after real client conversations and paid work. Move to direct clients once your scope, terms, and payout process are stable and well documented.

What are the biggest legal and compliance risks in cross-border freelance engagements?

A practical risk control is to confirm deliverables, revision limits, acceptance criteria, and payment triggers in writing before work starts. Keep your client details, invoices, and payout records aligned so disputes are easier to resolve if they happen.

How do I validate market claims when sources are promotional or methodologically thin?

Use a simple filter: reported claim, cross-checked claim, or unknown. If a source makes a growth or market-size claim but does not show its method, sample, or date, treat it as context rather than decision-grade evidence. You should also ask what the publisher is selling, because a recruiter, marketplace, or payments company may be useful but not neutral.

What documents should I prepare before taking international clients?

Prepare a practical starter set: a contract or statement of work template, an invoice template, your ID and payout details, and a folder for each deal with scope and payment records. Keep a short service description and pricing note ready too, because freelancers are expected to negotiate terms and compensation themselves. If you work in an area affected by brownouts, prepare a one-paragraph continuity note covering backup internet, backup power, and response expectations.

How should I set up payments so I can track every transaction and avoid payout surprises?

Use one ledger or tracking sheet that ties each job to the client, invoice, payment reference, payout receipt, and final reconciliation entry. Before taking on volume, test the full path with a small transaction and confirm that names, account details, and payout timing match what you expect. Brownouts are part of daily life in the Philippines, so if your payment approvals depend on being online, plan backup power (such as a UPS) instead of assuming continuous access.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- abr.gov.au/business-super-funds-charities/applying-abn/...trusted

- ato.gov.au/businesses-and-organisations/gst-excise-and-...trusted

- ato.gov.au/businesses-and-organisations/international-t...trusted

- bloomfield.edu/wp-content/uploads/2024/04/2021-22.pdftrusted

- community.ato.gov.au/s/question/a0J9s0000001Dmq/p-00029303trusted

- efile.fara.gov/docs/3457-Informational-Materials-20240421-4...trusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- irs.gov/individuals/international-taxpayers/figuring...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Best Digital Nomad Cities in Southeast Asia

Pick the city that can support a normal workweek, not the one that looks best across a dozen tabs. If you want one practical answer from this Southeast Asia shortlist, use these three gates in order and drop any city that fails one.

How to Build a 'Glocal' Marketing Strategy for Your SaaS Product

You're not just localizing pages. You're deciding whether buyers in a target market can discover you, trust you, buy, get onboarded, and renew with minimal friction. If checkout, invoicing, support, or legal review breaks, a launch can stall even when clicks and trials look healthy.

How to Automate Client Onboarding with Notion and Zapier

Automate repeatable steps first, and keep judgment calls manual. If you want to automate client onboarding in Notion, the goal is consistent execution, not full autopilot. Give every new client the same intake, setup, task handoff, and first message, with a named human owner for exceptions.