Quick Answer

Yes. Offshore company banking difficulties are common for Cayman and BVI entities, and the practical fix is operational: submit one coherent file before outreach. Match directors, shareholders, and beneficial owners across formation records, contracts, and invoices; run OFAC and counterparty screening with dated notes; and include a one-page payment narrative covering corridors and client types. Banks treat legality and risk acceptance as separate tests, so inconsistencies can trigger holds, returns, or de-risking. If one blocked payout cycle would strain payroll or rent, keep a tested backup receiving path.

Start Here With the Banking Reality for Cayman and BVI Companies#

Treat this as a banking reliability problem first. The goal is stable banking access, not secrecy. A Cayman or BVI company can be lawful for international business, but banking access can become fragile when ownership, activity, and fund flows are not documented in one consistent record.

Start with a few working terms:

- offshore company: a company formed under the corporate laws of jurisdictions such as Cayman or BVI for international business.

- offshore bank account: in this section, shorthand for banking access outside your primary operating jurisdiction.

- de-banking risk: the risk of losing banking access or having payments blocked when economic substance, KYC, or reporting are weak.

For BVI entities, transparency and compliance expectations are explicit. Economic substance rules are described as mandatory from 2019, and CRS information exchange is described as covering over 100 countries. One cited disclosure threshold is beneficial ownership of 10% or more, with non-compliance penalties described as up to $200,000 and possible strike-off. These are BVI-specific points, but the broader signal is the same: weak economic substance, weak KYC, or weak reporting increase de-banking and payment-blocking risk.

Before any bank outreach, prepare a one-page evidence map that aligns legal name, directors, shareholders, beneficial ownership, contracts, invoices, and reporting records. If those records do not match, fix that first. Small inconsistencies can raise KYC concerns and lead to blocked payments.

Before submission, run one internal clarity check. Ask a teammate who did not build the file to explain ownership, activity, and expected payment flows using only the pack you assembled. If they cannot do that quickly, tighten the file before submission.

From here, focus on practical decisions: bank and jurisdiction choices, a document checklist, and contingency steps for payment disruptions. You are not aiming for a perfect approval story. You are aiming for a setup that stays usable when reviews tighten.

Why Cayman and BVI Companies Face Extra Banking Friction#

Banks often apply stricter transparency and risk review to Cayman and BVI files, even when the company is legal and properly formed.

That scrutiny reflects the broader risk context, not just your intent. A European policy study described offshore centres as linked to secrecy, said they historically played a role in hiding illegal activity and criminal ownership, and noted that money laundering and tax evasion often appear together in offshore-leak findings. That does not make every offshore company suspicious, but it helps explain why AML teams may ask for clearer evidence trails.

A common pressure point is control clarity. The same study emphasizes transparency in bank registers and beneficial ownership, so incomplete or inconsistent ownership records can trigger additional review.

Legality and bank risk posture are separate tests. A structure can be lawful and still receive stricter review when transparency expectations are higher. Country-risk controls reinforce this. OCC guidance says the country-risk framework applies to banks with country-risk exposure, and banks with substantial international activity should receive country-risk management examinations.

For freelancers and small teams, timing is often the real problem. Extra review can slow decisions right when you need the account working.

Use this checkpoint before you submit an application pack:

- Confirm beneficial ownership records match across formation documents, shareholder records, and signed contracts.

- Prepare a one-page payment narrative that covers expected payer countries, typical invoice patterns, and service categories.

- Reconcile public signals with filed records, including website claims, invoice descriptions, and account-purpose wording.

- Set an escalation rule: if the same ownership question returns twice, pause new corridors and fix the mismatch before resubmitting.

More prep up front means more admin, but it can reduce avoidable back-and-forth later.

The Legal Baseline You Need Before Applying#

Set your baseline before bank outreach: transparent ownership, clear business activity, and controls that can stand up to sanctions and AML review.

Start with sanctions risk because it can halt activity quickly. OFAC administers and enforces U.S. economic and trade sanctions, and some OFAC programs require blocking property and interests in property of specified persons or entities. A file can look complete and still face restrictions if an owner, counterparty, or related payment involves a restricted party.

Treat AML and related onboarding checks as entry conditions, not optional admin. OCC guidance states regulated institutions must implement effective anti-money laundering programs that include terrorist-financing controls. When records conflict, review cycles can expand into repeat follow-ups. Before you apply, run this baseline checklist:

- Align formation records, beneficial ownership records, invoices, and contracts so the same story appears everywhere.

- Prepare a short business narrative: what you sell, who pays you, and expected payment patterns.

- Screen owners and major counterparties for sanctions risk, then keep a dated record of what you checked.

- Verify legal text from official legal sources before citing it. Informational XML pages are not legal notice.

Order matters here. Resolve ownership consistency first, complete sanctions checks next, and only then finalize the narrative you submit to the bank. That sequence reduces avoidable contradictions inside your own file. Keep one non-negotiable rule: if the structure depends on hiding beneficial ownership, stop and fix that before contacting any bank.

How Banks Actually Assess an Offshore Company#

Banks assess offshore files through a risk-and-transparency lens, so a clear, consistent business story often matters more than extra paperwork. In practice, the difficulty usually comes from assessment friction, not just one missing document.

A practical test is coherence. Business purpose, payment flows, client geography, and sector profile should all point to the same reality. When those elements conflict, banks may raise additional risk questions because the file is harder to validate.

Internal review paths differ by institution, and offshore files may go through multiple internal checks before a decision. If key details are incomplete or hard to verify, deeper review and repeat follow-ups are more likely.

That caution is tied to enforcement context. A U.S. Senate investigation described hidden offshore accounts in connection with unpaid taxes on a billion scale, listed findings on bank practices that facilitated U.S. tax evasion and inadequate bank response, and called for greater transparency from tax haven banks. Against that backdrop, banks may favor files that are straightforward to verify.

For cross-border business, payment-flow clarity is often the hinge. If the narrative is vague, expect more follow-ups. If it is specific and backed by documents, you may see fewer loops. Keep one evidence pack that aligns your core documents and expected payment routes so each reviewer sees the same story.

When follow-ups arrive, answer with the same source documents and language you already submitted unless a real change occurred. Frequent rewording can look like factual change, even when you are only trying to be more helpful.

Thresholds and escalation triggers can vary by bank and jurisdiction, so public guidance is directional. Confirm each institution's requirements directly and document what they ask for in writing. If you need a practical next step while tightening your paperwork, try the free invoice generator.

The Document Pack That Reduces KYC Back-and-Forth#

Files move faster when each document supports one clear business story. Build one pack that helps reviewers verify identity, activity, compliance posture, and transaction intent with fewer follow-ups.

| Pack area | Include | Supports |

|---|---|---|

| Core identity records | Formation and control documents, clear beneficial ownership evidence, and current versions with consistent legal name, registration details, directors, shareholders, and ownership details | Identity |

| Business and compliance proof | Signed client contracts, invoice samples, a short service description, applicable tax records, plus FinCEN documentation when U.S. obligations apply | Activity and compliance posture |

| Transaction evidence | A one-page transaction profile covering expected cross-border corridors, counterparties, and average use cases | Transaction intent |

Core identity records#

Start with formation and control documents for your company, plus clear beneficial ownership evidence. Keep current versions and make sure the legal name, registration details, directors, shareholders, and ownership details are consistent across every file.

When beneficial ownership is unclear, you are more likely to get extra scrutiny. Keep basic file hygiene tight. Use one naming pattern, keep issue dates visible, and archive superseded versions so only current documents enter an onboarding packet. Simple file discipline helps prevent accidental mismatches that can restart review.

Business and compliance proof that matches declared activity#

Add business records, such as signed client contracts, invoice samples, and a short service description, that match what you declared in onboarding. Include applicable tax records, plus FinCEN documentation when U.S. obligations apply.

If FBAR applies, keep your filing copy and calculation notes together:

- Use U.S. dollar amounts rounded up to the next whole dollar, for example

$15,265.25becomes$15,266. - If a computed value is negative, enter

0. - Periodic account statements may be used when they fairly reflect the year's maximum.

- If no Treasury rate is available, use another verifiable exchange rate and record the source.

Keep a dated deadline note on file:

- For all other individuals with an FBAR filing obligation, the due date remains April 15, 2026.

- For certain U.S. individuals with signature authority only and no financial interest, FinCEN extended filing to April 15, 2027.

Transaction evidence AML/KYB teams can test#

Add a one-page transaction profile covering expected cross-border corridors, counterparties, and average use cases so intent is easier to validate.

Before submission, run a four-point check:

- Identity match: ownership and control records are consistent.

- Activity match: contracts, invoices, and service description align.

- Compliance match: tax and FinCEN records are complete and dated.

- Transaction match: declared counterparties and corridors fit expected account use.

If your real payment pattern has changed since the first draft, update the profile and supporting documents together before you send anything. A partial update can trigger another review cycle.

If FinCEN terms are still unclear, review a plain-language FinCEN explainer before sending your file. Related: What is FinCEN? A Guide for Freelancers and FinTech Users.

Red Flags That Trigger De-Risking or Account Denial#

Incorporation is only part of a bank's risk view. The bigger question is whether your file is clear enough to assess. These signals can increase scrutiny, but they do not create an automatic denial threshold on their own. Banks act as gatekeepers against money laundering and terrorist financing, and increased supervisory pressure and public expectations can push reviewers toward caution when information is incomplete or inconsistent.

Financial institutions remain vulnerable to misuse, and regulated institutions are expected to run AML programs that cover both money laundering and terrorist financing. The FATF Recommendations are recognized as the global AML/CFT standard. When your file is hard to verify, risk assessment quality can weaken and controls may tighten.

Inconsistent story risk#

Inconsistency across your website, onboarding answers, contracts, invoices, and transaction profile can raise review friction. Even if each document is legitimate on its own, mismatches can make the overall profile look less reliable.

Before submission, confirm:

- Service description and client type match across website and onboarding.

- Invoice line items match signed contract language.

- Declared operating footprint matches actual counterparty geography.

- Expected payment corridors fit declared business activity.

Ownership opacity and intent risk#

Unclear ownership information can create friction because insufficient information weakens risk assessment. Unresolved conflicts in ownership, control rights, or signatory authority can lead to additional review before a decision.

How you describe your activity also matters. If key details are vague or inconsistent, reviewers may ask for more information. If privacy is your concern, state the lawful reason clearly and still provide full disclosure.

Flow risk and de-risking outcomes#

Activity that does not align with your declared business profile can prompt tighter controls, deeper review, or de-risking measures.

If your operating model changes, tell the bank early and provide refreshed supporting documents. More clarity up front can reduce avoidable review disruption.

Choosing Between One Primary Bank and a Backup Setup#

Choose based on continuity risk. If one failed payout cycle would seriously affect your payroll or rent, consider using a primary account plus a backup receiving path in another jurisdiction. If that risk is low, one well-run offshore bank account may be enough.

The tradeoff is straightforward. A single account is simpler. A primary-plus-backup setup can reduce single-point exposure during de-risking events, but it adds ongoing admin and KYB/KYC upkeep. Offshore account onboarding is often similar to home-country onboarding, and institutions commonly ask for proof of identity, address, and income.

| Setup | What you gain | What you carry |

|---|---|---|

| One primary bank | Simpler operations and fewer recurring reviews | Higher dependency if access is restricted |

| Primary plus backup | Resilience if one provider tightens risk controls | More document upkeep and coordination across institutions |

Ownership transparency is often where friction starts. Banks often apply a 25% UBO checkpoint, and in heightened-risk EU contexts some reviews may move closer to 10%. Keep ownership, control, and signatory records aligned across both banks so either provider can verify who in the end controls the company.

Use a light governance cadence so your risk picture does not drift:

- Assign monthly ownership and signatory checks across both institutions.

- Track KYC and KYB refresh reminders before each bank's expected review window.

- Review jurisdiction fit regularly so the backup path still matches your client corridors and operating pattern.

A backup path works best if you keep it current. Keep the same ownership narrative and business description synchronized across both institutions, then update both records whenever your operating pattern changes.

Offshore banking can be legal, but it does not remove disclosure or reporting duties by default. Treat a backup setup as continuity planning, not secrecy planning.

Building a Cashflow-First Receiving and Payout Structure#

For Cayman or BVI setups, tie money movement to a clear business-entity record rather than ad hoc personal handling.

BVI and Cayman are commonly used by start-ups. Forming an entity is framed as a legitimacy and professionalism step while also separating founders from personal liability for business debts. Structure receiving and payout activity so each transaction stays traceable to that entity boundary and can be reviewed consistently.

Prioritize traceability over speed claims. Keep a direct chain between contract terms, invoice language, account purpose, and transfer references. This can help an internal check or bank review follow the same story end to end. If one link changes, update the related records at the same time.

Before you open a new corridor or payment path, use a simple decision rule. If you cannot describe expected counterparties, expected purpose, and expected volume pattern in language that matches your existing file, pause and update documentation first. Expansion without documentation can create avoidable review friction later.

There is no universal payout sequence here. Detailed process design is provider-specific and jurisdiction-specific, so avoid speed choices that weaken record quality.

Related: The Psychology of Client Retention: Building Long-Term Freelance Relationships.

What to Do When Funds Are Held Returned or Delayed#

When funds are held, returned, or delayed, first determine status, then escalate.

Start with status triage#

Classify the transfer before contacting anyone, and keep one shared incident note.

| Status | Meaning | First step |

|---|---|---|

| Credited | Settlement appears complete | Confirm beneficiary receipt before retrying anything |

| Held | Status is still unresolved | Avoid re-sending while the case is active |

| Returned | Transfer appears reversed | Confirm the return reference and destination before issuing a new payout |

Capture the same details each time: provider reference, your payout ID, submitted account details, amount and currency, status timestamp, and any error text. Keep communication tight while the case is open. Multiple parallel tickets with different summaries can create confusion and may slow resolution.

Investigate the delay signal before assuming failure#

In one reported forum case, a user said their business account was closed without warning and that the provider reported due diligence checks were still in progress. In that same thread, a commenter said holds may run for 30 or 60 days if a dispute is requested, and that refunds are sent to the bank account the user provides. Treat those points as scenario-specific reports, not universal policy.

Escalate in a fixed order#

Use a fixed sequence to reduce loops:

- Internal evidence check.

- Provider ticket with full references and timeline.

- Beneficiary-side confirmation to close the loop.

If a hold exceeds your operating tolerance, route new critical payouts through your backup path and keep a full audit record of both paths and decisions.

Decision Rules for Freelancers and Small Teams#

Use a strict go/no-go filter. Open or keep Cayman Islands or British Virgin Islands banking only when your cross-border complexity is real and your team can sustain ongoing compliance.

Apply the go-no-go filter before opening or keeping accounts#

A go decision needs both real international operating needs and strong record discipline.

| Rule | Fast test | If the answer is no |

|---|---|---|

| Go or no-go | Do you have genuine cross-border complexity that your current setup cannot handle cleanly? | Keep the structure domestic and simplify. |

| Risk | Can you keep beneficial ownership records and related tax records accurate year-round? | Do not proceed with offshore banking. |

| Cashflow | Would one failed payout cycle create immediate operating pressure? | Build redundancy before optimizing for fees. |

| Governance | Can you review de-risking exposure quarterly with documented outcomes? | Treat the setup as unstable and reduce dependency. |

If the decision is close, score each rule as pass or fail and keep that note with your compliance records. The value is not the label. The value is a written rationale you can revisit when conditions change.

Use BOI scope and timing as a compliance stress test#

If your entity is foreign and registered to do business in the U.S., FinCEN says an interim final rule published on March 26, 2025 revised who is a reporting company. FinCEN also says entities created in the U.S. are exempt from BOI reporting. For qualifying foreign reporting companies, FinCEN says the filing timeline was April 25, 2025 for entities registered before March 26, 2025, or 30 calendar days from registration for entities registered on or after that date. FinCEN also says reporting companies do not need to report BOI of U.S. persons. Keep a dated BOI scope memo and update it whenever ownership, registration status, or U.S. nexus changes.

Do not rely on stale wording. FinCEN notes some older page guidance is not fully updated for the interim rule. FederalRegister.gov also states its web version is not the official legal edition. Verify legal research against an official edition of the Federal Register. If you need a plain-language refresher before escalating, review the FinCEN BOI fact sheet first.

Cashflow and governance rules that reduce avoidable shocks#

If client concentration is high, prioritize continuity over marginal fee savings. Maintain a primary route and a backup route, and test both before critical payout windows.

Run a quarterly review with written decisions on:

- Jurisdiction exposure.

- Counterparty mix.

- Bank communication quality.

- Record freshness for beneficial ownership and related tax records.

When one item remains unresolved across reviews, treat it as an active risk until a documented fix is complete. Closing the loop matters more than adding new review notes. If risk signals stay unresolved across reviews, reduce dependency instead of waiting for a forced de-risking event. If you want a deeper dive, read Automating Your Freelance Finances: A Zapier Workflow for Connecting Stripe.

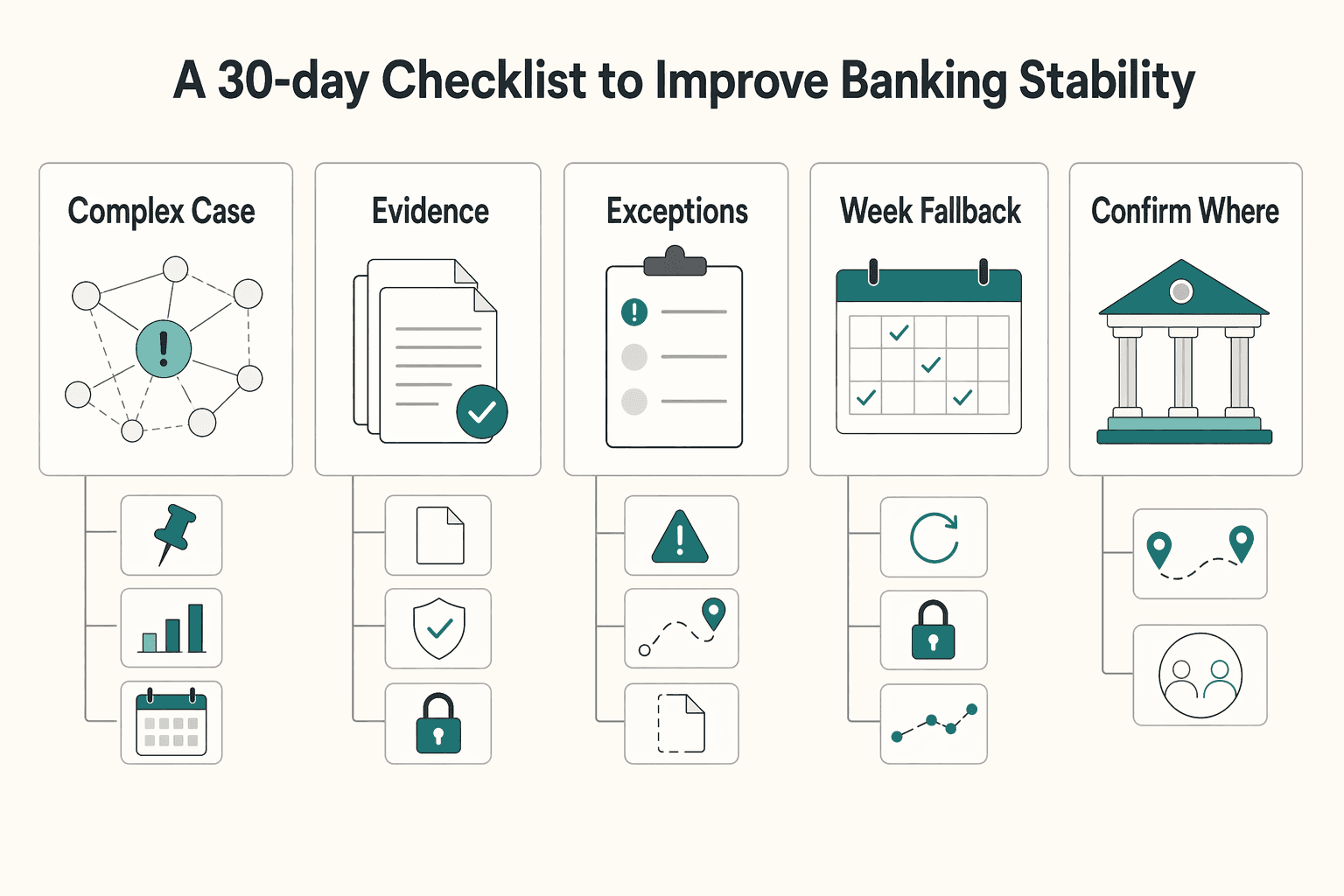

A 30-Day Checklist to Improve Banking Stability#

Use a 30-day operating cadence to make your setup easier to review and more resilient in practice. Treat it as a risk-based approach: focus most attention on the highest-risk gaps, not equal effort across everything. This is an operating timeline, not a universal legal deadline.

| Week | Focus | Action |

|---|---|---|

| Week 1 | Legal and identity baseline | Validate legal and identity records, confirm documentation completeness, and reconcile names, control details, and profile information across your bank profile and operating documents |

| Week 2 | Decision-ready evidence pack | Assemble a clear AML review pack and map expected payment behavior, especially in higher-risk areas |

| Week 3 | Path testing and exception handling | Test receiving and payout paths, including backup routes, and document how your team handles held or returned transactions |

| Week 4 | Fallback ownership and monthly cadence | Document fallback procedures, assign owners, set a monthly compliance refresh calendar, and keep operating notes current so execution stays consistent under pressure |

- Week 1: legal and identity baseline

Validate legal and identity records and confirm documentation completeness. Reconcile core records so names, control details, and profile information are consistent across your bank profile and operating documents.

- Week 2: decision-ready evidence pack

Assemble a clear AML review pack and map expected payment behavior, especially in higher-risk areas. Keep the narrative consistent across what you do, who you transact with, and how funds are expected to move.

- Week 3: path testing and exception handling

Test receiving and payout paths, including backup routes. Document how your team handles held or returned transactions so exceptions are managed with a repeatable sequence.

- Week 4: fallback ownership and monthly cadence

Document fallback procedures, assign owners, and set a monthly compliance refresh calendar. Keep operating notes current so execution stays consistent under pressure.

Ongoing monthly checkpoint before changing rails:

- Confirm where support exists by market, jurisdiction, and program.

- Confirm what is enabled on your account and who can approve changes.

- Confirm where coverage varies before shifting meaningful volume.

- Confirm communication quality by tracking unresolved requests and response speed.

At month end, carry unresolved items into the next cycle with a named owner and a clear target date. That habit helps prevent repeated discussion of the same issue without actual resolution. This checklist stays aligned with risk-based controls and documentation discipline: clear records, clear ownership, and repeatable checks.

What to Do Next for a Reliable Get-Paid System#

Stable cashflow comes from transparent compliance evidence and planned fallback paths, not secrecy tactics. A legal offshore structure can still become fragile if records drift after onboarding, so the next move is disciplined execution.

Execute the next phase in order#

- Freeze your core evidence pack. Keep beneficial ownership records, current business documentation, and source-of-funds explanations consistent with declared business activity and actual transaction activity.

- Test contingency paths before pressure hits. Run controlled transactions on primary and backup routes where available, then confirm you can track outcomes and reconcile records. A backup reduces single-point-failure risk, but it does not guarantee continuity.

- Operate for ongoing review, not one-time approval. Banks use compliance reviews to maintain acceptable risk with regulators, and intensity changes with risk profile. Even lower-risk clients can face periodic checks, often annually or biannually, so keep records current and communicate material changes early with your relationship manager.

- Confirm jurisdiction-specific obligations before scaling. Rules and enforcement can vary by country, so validate legal and tax requirements with qualified advisors when structure or transaction patterns change. In U.S. context, older GAO testimony described offshore income reporting duties and referenced a $10,000 control threshold; treat that as historical context, not universal current law.

Choose infrastructure by control quality#

When comparing providers, score operational control quality over marketing claims.

| Decision area | What to verify before committing |

|---|---|

| Compliance gates | Clear onboarding and ongoing review requirements, including change-triggered checks |

| Audit trail quality | Traceable history for account changes and compliance review outcomes |

| Reconciliation | Reliable matching between external statements and internal records |

| Status visibility | Clear tracking for review requests, temporary holds, and final outcomes |

If your documentation is not current and consistent, pause expansion and fix it first. Reliability is built through repeatable evidence, tested contingency paths, and fast, accurate responses when review requests arrive.

Frequently Asked Questions

Why is it hard to bank a Cayman or BVI company even when the structure is legal?

A Cayman or BVI structure may be legal and still face stricter review. Some sources note that many traditional banks are more cautious with non-resident structures, so approval depends on risk controls, not legality alone. In practice, banks often ask for deeper identity and source-of-funds verification, which can slow onboarding.

Is offshore company banking legal if I fully disclose income and ownership?

Sources here describe offshore banking as legal in principle. An offshore bank is a bank outside the country where most account holders live, and an offshore bank account is simply an account at that bank. Even with full disclosure, approval is not guaranteed because each institution applies its own compliance and risk standards.

Which behaviors make banks classify an offshore account as high risk?

Banks tend to escalate when customer identity and fund origin are unclear or hard to verify. Inconsistent information across forms, ownership records, and transaction explanations can raise concern. Requests that resemble anonymous or numbered-account behavior are also misaligned with current practice.

What should I prepare before applying so KYC and KYB reviews move faster?

Prepare a complete, consistent file for identity, ownership, and business activity. Make sure names, control persons, and core details match across your documents and account profile. Clear explanations of expected payment flows and fund origin can reduce back-and-forth during review.

How do AML, CRS, and FATCA expectations affect day-to-day banking outcomes?

They generally increase focus on transparency, customer identification, and verification of where funds come from. Programs cited in this context include CRS and FATCA, alongside broader AML-driven controls. Day to day, that means accounts are judged on whether records and activity stay consistent with what was declared.

What can I do if my offshore bank account is delayed, restricted, or closed?

Start by confirming the exact status of the payment or account before taking new action. Then provide a complete, consistent set of identity, ownership, and source-of-funds documents so the bank can reassess quickly. Because reviews can take time, plan for temporary payment disruption while the case is under review.

Watch

Why Cayman and BVI Companies Struggle With Banking

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Automating Your Freelance Finances: A Zapier Workflow for Connecting Stripe, QuickBooks, and Wise

Cleaner books and fewer month-end fire drills come from sequence, not software. Run this in the right order: structure, compliance, accounting architecture, then automation.

What Is FinCEN for Freelancers and FinTech Users

If you are asking **what is fincen**, focus first on the decision in front of you. FinCEN, the Financial Crimes Enforcement Network, is tied to FBAR filing through FinCEN Form 114 when foreign financial accounts create reporting duties. By the end, you should know whether to act now, gather records, or escalate.

Freelance Client Retention: Weekly Systems for Repeat Work and Long-Term Relationships

Keeping good clients is easier when they can predict how you work. Use a weekly checklist to keep communication, scope, and admin clean before small issues turn into bigger ones.