Quick Answer

Use a written five-step payment sequence for fintech for offshore companies: collect, receive, convert, payout, and reconcile. Add a checkpoint at each step, including payer legal-name verification, held-or-credited status logging, conversion approval, and final reference matching. Set collection terms by client risk instead of convenience, and keep one client evidence pack with invoice records, payment references, and status history. If funds may be held between receipt and payout, confirm whether your setup behaves under EMI-like or PSP-like scope before setting timing expectations.

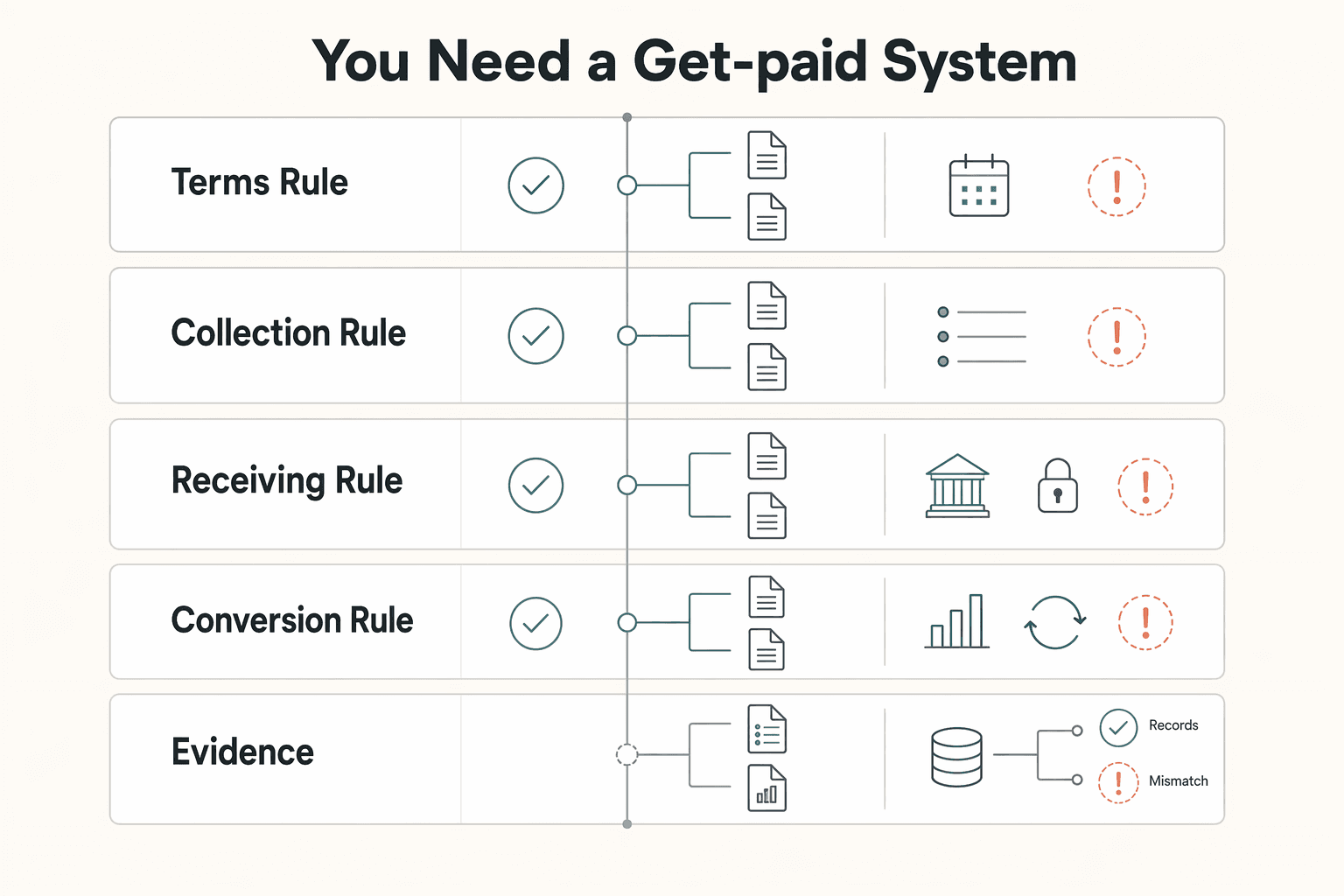

You Need a Get-Paid System, Not More FinTech Noise#

If cashflow is unpredictable, one common issue is payment setup, not just a missing tool. Late payments, surprise holds, avoidable fees, and weak terms can pile up fast and force reactive decisions.

| Rule | What to define |

|---|---|

| Terms rule | Define deposit and milestone triggers before work starts |

| Collection rule | Set accepted payment methods by client risk level |

| Receiving rule | Choose accounts by currency route and payout reliability |

| Conversion rule | Define when funds are converted and who approves exceptions |

| Evidence rule | Store a minimum dispute pack for every client |

The practical fix is a reusable financial architecture for digital payments that every client follows from proposal to final payout. Build a first version in a focused working session, then tighten it as real transactions reveal gaps. Day-one consistency matters more than day-one perfection.

This article is for freelancers, creators, and small offshore teams that need reliable money movement. It is not about choosing offshore software vendors. Most outsourcing content focuses on hiring capacity, cost, and delivery speed, which is a different problem from invoice-to-withdraw timing.

You will also see a lot of fintech content centered on market growth. Useful background, but not enough when a payout is stuck or a transfer does not match an invoice.

One distinction that directly affects execution is license scope. An EMI model can include issuing e-money, operating wallets, and holding client balances. A PSP model focuses on payment processing and may not allow extended holding. If cash sits between receipt and payout, that difference can change timing, hold exposure, and buffer planning.

Start with these non-negotiable decisions:

- Terms rule: define deposit and milestone triggers before work starts.

- Collection rule: set accepted payment methods by client risk level.

- Receiving rule: choose accounts by currency route and payout reliability.

- Conversion rule: define when funds are converted and who approves exceptions.

- Evidence rule: store a minimum dispute pack for every client.

Before you lock tools or policies, run one practical check. Ask whether a teammate could execute your payment sequence from written instructions if you were unavailable for a day. If the answer is no, the setup is still too dependent on memory and too fragile under pressure.

Keep one filter through the whole article: if a choice changes invoice-to-withdraw timing, it belongs in your fintech stack. If it only changes staffing capacity, treat it as a separate offshoring decision.

Offshore FinTech and Offshoring Are Not the Same Decision#

Treat these as separate tracks. Fintech decisions govern money movement workflows. Offshoring decisions govern how work is delivered through third parties. If you mix them, you may improve delivery capacity without clearly improving how reliably cash settles.

| Quick filter | Treat it as |

|---|---|

| Changes invoice-to-withdraw timing | Fintech decision |

| Changes hiring capacity, location, or delivery bandwidth | Offshoring decision |

| Cannot map to a payment state | Likely noise for this article |

Staffing guidance is useful when comparing nearshoring, offshoring, and onshoring. It is not a payment-controls playbook for states like received, held, returned, and completed.

Sources in this space often split along that line. Some focus on outsourcing adoption and delivery structure, while others focus on digital-payments growth. That context can help with planning, but it does not answer invoice-to-withdraw execution questions.

A practical way to avoid drift is to tag every decision during planning meetings. If the decision maps to a payment state, keep it in your money-movement plan. If it maps to hiring capacity, handoff structure, or staffing location, keep it in your delivery plan. Mixing those decision types adds noise and can slow execution. Use this quick filter before acting on any recommendation:

- If it changes invoice-to-withdraw timing, treat it as a fintech decision.

- If it changes hiring capacity, location, or delivery bandwidth, treat it as an offshoring decision.

- If you cannot map it to a payment state, it is likely noise for this article.

If you want a quick next step for "fintech for offshore companies," Try the free invoice generator and apply one decision rule to your next live invoice.

Build the Financial Architecture in Five Layers#

Build your setup in layers so continuity does not depend on a single component or person. The goal is consistent invoice-to-withdraw execution, with clear handoffs and checks at every stage.

| Layer | Action | Checkpoint |

|---|---|---|

| Collect | Issue the invoice and confirm terms before work advances | Verify payer legal name, payment method, due date, and acceptance condition |

| Receive and hold | Confirm incoming-fund status on the receiving flow | Log credited, pending, or held status with timestamp and account reference |

| Convert | Decide whether to convert now, later, or in tranches | Record quote window, approver, and reason for timing |

| Payout | Release funds with controlled beneficiary checks | Confirm beneficiary details match the latest approved record, then log payout reference at release |

| Reconcile | Tie invoice, receipt, FX action, and payout into one ledger trail | Export and archive one evidence pack with invoice copy, payment references, and status history |

A practical sequence is: invoice sent -> payment confirmation -> funds credited or held -> FX decision -> payout request -> reconciliation export. If one step is unresolved, pause there instead of forcing the next action.

- Collect: Issue the invoice and confirm terms before work advances.

Checkpoint: verify payer legal name, payment method, due date, and acceptance condition.

- Receive and hold: Confirm incoming-fund status on the receiving flow.

Checkpoint: log credited, pending, or held status with timestamp and account reference.

- Convert: Decide whether to convert now, later, or in tranches.

Checkpoint: record quote window, approver, and reason for timing.

- Payout: Release funds with controlled beneficiary checks.

Checkpoint: confirm beneficiary details match the latest approved record, then log payout reference at release.

- Reconcile: Tie invoice, receipt, FX action, and payout into one ledger trail.

Checkpoint: export and archive one evidence pack with invoice copy, payment references, and status history.

Where possible, treat each layer as an independent service boundary with its own access, encryption, and compliance scope. This makes it easier to scale payment-heavy steps during peak demand without scaling the full workflow.

Setups that depend on one component are more fragile; fault isolation is what keeps one failure from stopping the full cycle.

This tradeoff is real: modular design improves control and extensibility, but early coordination can be heavier and ROI may take time. If you use this five-layer model, start with all five layers, then optimize the layer creating measurable delay.

A useful way to keep this practical is to assign one owner per layer and one backup owner for escalations. Record handoff timestamps between layers so you can spot whether delays come from provider status, internal approvals, or reconciliation lag. Without that separation, teams can over-correct the wrong layer.

Choose Your Collection Setup by Client Risk, Not Brand Preference#

Choose collection by risk profile and evidence quality first, then by convenience. This is where fee exposure and enforcement clarity are set before money moves. Use this comparison before each invoice:

| Collection option | Fee signals you can verify now | Risk-policy fit | Evidence quality standard |

|---|---|---|---|

| Stripe card link | Stripe pricing lists 2.9% + 30¢ for successful domestic card payments, with possible add-ons like +1.5% international cards, +1% currency conversion, and +0.5% manual entry | Useful when card convenience matters, especially for new payers | Keep payment IDs, timestamps, status changes, and acceptance records together |

| Bank-transfer-first where supported | Example from Stripe pricing: ACH Direct Debit 0.8% with a $5.00 cap | Useful for lower-risk repeat clients with reliable remittance references | Reconciliation quality depends on consistent payer references and fast matching |

| Hybrid default | Keep transfer-first with a card fallback | Useful when you want continuity without giving every client identical terms | Assign one route per invoice and archive one acceptance trail per invoice |

Do not lock policy to one public price table. Stripe notes costs are subject to change, and pricing or method availability can vary by country, volume, and account setup. In Connect, fee exposure also depends on pricing model: "Stripe handles pricing" states no additional account or per-payout fees for the platform, while "You handle pricing" includes $2 per monthly active account and 0.25% + 25¢ per payout sent.

For client-risk rules such as deposits, milestone billing, and net terms, set explicit internal policy and apply it consistently.

Set these contract controls before invoicing:

- Milestone schedule tied to specific deliverables, with invoice release linked to documented acceptance.

- Late-fee clause with a defined start date and calculation method.

- Revision caps that define included rounds and paid overage.

- Acceptance window with a fixed business-day count and written issue logging.

Verification checkpoint before each invoice: confirm signed contract version, milestone ID, acceptance proof, due date, and chosen collection route. Then archive these with invoice and payment records as one evidence pack.

When you are deciding between two collection routes that both look acceptable, test against friction and record quality at the same time. A route that closes fast but leaves weak acceptance records can create extra follow-up later. A route with cleaner records but too much checkout friction can slow payment completion. The target is practical balance, not one perfect method.

Pick Receiving Accounts That Match Corridors and Cash Timing#

Pick receiving accounts for dependable cash access in your main corridors first, then optimize FX. This layer should prioritize clean inbound handling, method-level fees, and how quickly funds become usable. Use this template before routing live client payments:

| Option | Corridor coverage check | Inbound fee structure check | Withdrawal constraint check |

|---|---|---|---|

| Wise Business | Wise says receiving details are available in 24 currencies | Wise receive pricing shows that some Swift or wire receipts have fixed fees, including 6.11 USD for USD wire and Swift, 2.16 GBP for GBP Swift, and 2.39 EUR for EUR Swift | Wise card terms include 2 free ATM withdrawals each month up to 100 USD, then 1.5 USD per withdrawal |

| Revolut Business | Confirm which local account details are available for your payer countries before onboarding | Verify per-method inbound charges and any fixed wire fees in your region and plan | Verify cash-out limits, per-withdrawal charges, and hold conditions in your plan |

| Secondary multi-currency account | Confirm overlap with top invoice corridors so one account issue does not stop receipts | Confirm domestic versus Swift handling and any method-level fixed charges | Confirm withdrawal timing, limits, and returned-credit handling |

Use one rule consistently: if most revenue lands in one currency, optimize for fastest access in that corridor before chasing small FX gains. Also treat Wise numbers above as U.S.-resident page data and validate regional terms before setting policy in other markets.

Set failure handling in advance with a named owner and escalation clock for each case:

- Unmatched deposit: finance operations owns matching and escalation.

- Returned credit: accounts receivable owns correction and payout pause decisions.

- Delayed status update: account admin owns provider escalation and client update timing.

- Incident evidence pack: invoice ID, payer legal name, expected amount, receiving rail, account reference, status timeline, and communication log.

Keep a backup rail active, not just documented. If the primary account has unresolved matching or status issues, route new invoices to the secondary rail until normal operation returns.

During the first few live cycles after changing receiving rails, increase review frequency on inbound status changes and unmatched credits. Issues can surface early when payer references are inconsistent or internal mapping fields are not standardized. Catching those gaps early can reduce manual clean-up in reconciliation.

Convert Currency With Rules You Can Defend Later#

Set your FX rule before funds arrive and apply it consistently. Predictable policy is easier to run under pressure and easier to justify when exceptions appear.

| FX policy | When it fits | Main benefit | Main risk |

|---|---|---|---|

| Immediate conversion | Most costs are due soon in one operating currency | Reduces exposure after funds land | You may overpay if rates improve later |

| Threshold-based conversion | You can tolerate some movement and want tighter execution control | Avoids converting every small receipt | Requires closer monitoring and faster approvals |

| Split by expense horizon | You have near-term bills plus later obligations in another currency | Balances short-term liquidity and longer-horizon exposure | Adds coordination and reconciliation work |

Write the tradeoff into policy: tighter rate control usually adds operational effort, while simpler rules can increase FX drift. If approvals tend to lag market moves, define in advance when to escalate or defer a conversion decision.

If you use corporate crypto rails where your jurisdictions and providers permit them, include compliance context in the conversion decision. Discussion around offshore financial centers has highlighted rising inter-jurisdictional AML risk and the need to balance market integrity, rule clarity, and innovation. In the U.S., payment stablecoins now sit under a federal framework through the GENIUS Act, signed July 18, 2025. Use that as U.S. context, not global permission.

Before any conversion, confirm three basics: payable amounts by currency for the next cycle, current approval authority, and which policy mode applies. If one is missing, pause.

Keep auditable evidence for each conversion so the decision can be reconstructed later:

- Policy mode used and why it was chosen.

- Approval and execution timing.

- Amounts and currencies involved, plus any exception or compliance note.

Add one post-cycle review to conversion operations. Check whether exceptions came from market movement, delayed approvals, or missing balance forecasts. Then adjust approval coverage or trigger rules in policy language, not only in team chat. This keeps your decision trail clear when someone asks why a conversion was handled differently.

Design Payouts and Withdrawals to Survive Compliance Friction#

Payout controls work best when release decisions are evidence-based, not urgency-based. Treat payout states as internal control labels and require a complete record before any state change.

| Payout state | Internal meaning | Record required before next step |

|---|---|---|

| Requested | Payment instruction is created | Request ID, initiator, beneficiary ID, amount |

| Queued | Passed initial checks, waiting release | Approval timestamp, policy or program tag |

| Processing | Sent to provider rail | Provider submission reference and status timestamp |

| Held | Blocked by mismatch, review flag, or missing data | Hold reason, owner, next review time |

| Returned | Transfer bounced or rejected | Return reference, failure reason, remediation owner |

| Completed | Provider marks success and funds are treated as final | Provider reference captured, ledger state updated, recipient confirmation logged |

Prioritize three controls: account validation, name-match consistency, and policy-gated withdrawal timing. Reviews often assess data flows, access controls, and whether each transaction is traceable end to end, not only whether funds eventually arrive.

If beneficiary data changed recently, use a verification checkpoint before release. Define "high value" in policy, then keep this checkpoint short and mandatory:

- Re-verify identity, bank ownership, and beneficiary details.

- Confirm legal name matches the approved beneficiary record.

- Confirm approval authority is valid for this payout type.

- Confirm there is no unresolved hold or recent return on that beneficiary.

- Confirm trace fields are complete before release.

Poorly designed payout integrations can lead to transaction drops, duplicate payments, delayed settlements, and audit red flags. For each incident, keep one evidence pack with request details, approvals, provider references, state transitions, and communication notes so retries do not create a second failure.

Define completion as a binary control. Sent is not done. Done means provider reference captured, ledger updated, and recipient confirmation logged. If one item is missing, keep the payout open.

End-of-week release volume can create urgency. Treat unresolved verification fields as a red flag, not routine urgency. If checks are incomplete, hold and communicate clearly.

Build a Failure Response Checklist Before You Need It#

Build this checklist before incidents happen. When a payment stalls, use a consistent first-response sequence with full traceability. The goal is controlled speed while reducing duplicate retries and audit gaps.

Failure patterns often repeat. Weak bank API integrations can lead to transaction drops, duplicate payments, delayed settlements, and audit red flags. Recurring payment flows also need clear handling for failures, reversals, and retries. If status is still unclear at the next check window, consider pausing related actions and opening a trace before retrying.

First response sequence#

Use an internal sequence like this, then adapt it to your provider workflow:

- Isolate affected invoices and pause linked automations so no reminder, retry, or payout runs on stale status.

- Notify the client with verified facts only: invoice IDs, amount affected, current state, and next update time.

- Open a provider trace with payment reference, submission timestamp, beneficiary details, and current state.

- Set the next status update time and owner before closing first response.

Failure checks by incident type#

| Failure mode | First verification checkpoint | Immediate risk if skipped |

|---|---|---|

| Payment hold | Recheck account validation details: identity, bank ownership, and beneficiary details | Review delays or failed transfers from mismatched records |

| Chargeback or reversal | Gather invoice acceptance proof and communication history used in your response process | Slower response with weaker traceability |

| Payout failure | Compare internal ledger status to provider status before any retry | Duplicate payment from blind resubmission |

| Compliance-triggered delay | Confirm access-control history and state-change history are complete | Incomplete trace during later review |

Evidence bundle and closure rule#

For internal controls, keep one evidence bundle per incident so the timeline is easy to audit:

- Invoice and acceptance proof

- Communication log with timestamps

- Payment reference and provider trace details

- Timeline of actions, owners, and status changes

Close a case only after reconciliation matches internal ledger entries to bank or provider records. Then send a final status update to the client and assign dated follow-up for any unresolved exceptions.

Communication discipline matters as much as technical checks. Keep the first client message factual and brief, and avoid guessing causes before verification. Promise only the next update time you can meet. This helps reduce follow-up confusion while the trace is still open.

Keep Audit and Tax Records Ready Without Slowing Operations#

Keep one minimum evidence pack per client and update it as payments move. Then review it on a fixed monthly close cycle. This keeps operations moving while reducing last-minute document hunts during disputes, audits, or tax reviews.

As volume grows, recordkeeping risk grows too. One scaling-focused source notes that adding employees, transactions, and jurisdictions increases audit and reporting risk, and controls that worked at 50 employees often fail by 500. Treat documentation and data controls as core operations, not end-of-quarter cleanup.

Minimum evidence pack per client#

Use one standard pack for every client cycle. Keep it lean, but make each artifact independently useful.

| Record | Minimum fields | Monthly check |

|---|---|---|

| Signed terms | Executed version, acceptance date, billing terms | Latest version linked to active invoices |

| Invoice history | Issued invoices, revisions, credits, status timeline | No missing status steps |

| Payout records | Payment reference, payout state, return or hold notes | References match provider exports |

| Reconciliation exports | Internal ledger export and bank or provider export | Variances assigned to an owner |

| Control artifacts | Masked records, export logs, traceable transaction references | Masking and trace fields present |

Include program-sensitive checks as explicit fields, not informal notes: compliance gate status, validation status, and tax-document readiness where relevant. Coverage varies by market and provider program, so track owner and next review date for pending items.

Deloitte describes potential value across more than 100 RegTech solutions in reporting, risk, identity and control, compliance, and transaction monitoring. Use that as a category map, then verify that each chosen control produces usable logs and exports for your evidence pack.

Monthly close checklist#

- Confirm signed terms, invoice history, and payout records exist for every active client.

- Reconcile ledger totals to bank or provider exports, then assign each variance to a named owner.

- Review program-specific compliance and tax-document status fields, and escalate pending items with dates.

- Sample masked records, export logs, and transaction references for review readiness.

- Run a short internal audit pass, update policies where gaps appeared, and assign follow-up training.

This does add monthly admin time, but it can reduce emergency effort when filings or disputes appear. If reconciliation exports or transaction references are missing, do not mark close complete.

You can reduce close friction further by standardizing file naming and retention conventions. Keep invoice IDs, payout references, and period tags aligned across exports to limit manual relabeling during audits. Small consistency choices can save time once transaction volume increases.

Automate Repetitive Steps but Keep Human Approval Gates#

Automate routine notifications and data sync first, and keep payout-release decisions with a person while controls are still being validated. That keeps speed in repetitive tasks and judgment where mistakes are costly.

Stripe pricing helps frame the tradeoffs. Domestic cards are listed at 2.9% + 30 cents per successful transaction, with possible add-ons such as 1.5% for international cards, 1% for currency conversion, and 0.5% for manually entered cards. In Connect, one model lists $2 per monthly active account and 0.25% + 25 cents per payout, while another lists no platform fees. Stripe also notes that pricing can change, so fee capture and reconciliation can help you spot margin drift.

Start with repeatable handoffs#

Use automation for steps that do not require judgment, and keep each handoff traceable.

- Invoice status updates after payment confirmation.

- Payment confirmations that use verified status fields.

- Reminder cadence updates for overdue invoices based on current status.

- Reconciliation handoffs that move payment records into monthly close.

Keep approval gates human#

| Control point | What to enforce | Evidence to keep |

|---|---|---|

| Failure handling | Route failed automations to a named owner | Exception record, owner, resolution timestamp |

| Data minimization | Pass only required fields for each step | Field map and masked payload logs |

| Payout release | Require human approval before funds are released | Approval record, reviewer, decision timestamp |

Use Automating Your Freelance Finances: A Zapier Workflow for Connecting Stripe as a starting pattern. Then review exceptions monthly and run short post-mortems using How to Conduct a Client Post-Mortem and Gather Feedback.

As automation volume grows, track exception themes instead of only exception counts. If the same failure repeats, fix the data handoff or validation check at the source. Repeated manual intervention is a signal that the handoff logic needs refinement, not just better monitoring.

If you want a deeper dive, read Automating Your Freelance Finances: A Zapier Workflow for Connecting Stripe.

Put This Into Practice With One Client This Week#

Run the five-layer architecture through one real client invoice cycle this week so terms, rails, and fallback actions are decided before money moves.

Create a one-page execution sheet before the next invoice goes out. Use five rows: collect, receive and hold, convert, payout, and reconcile. For each row, record owner, verification checkpoint, evidence to store, and first fallback action.

- Collect: confirm signed terms, trigger conditions, and invoice release date; store signed agreement and invoice ID.

- Receive and hold: pre-check sender and expected amount; if funds arrive unmatched, pause release, open a trace, and set the next client update time.

- Convert: choose one conversion rule in advance and log approver plus timestamp for each decision.

- Payout: recheck beneficiary details before release and hold payout until that check is complete.

- Reconcile: close only when provider reference, ledger entry, and recipient confirmation align; keep an exception log for open items.

As you evaluate options, separate promotion from evidence. For example, the Bain and JJC announcement is explicitly labeled as a paid press release, so treat it as context rather than proof. Use discovery lists, including items like REGTECH100, as a starting point, not as a current ranking. Then verify current documentation and controls against your actual payment path, including client lifecycle handling plus KYC and AML checks where required.

Finish the week with a short decision memo: what stays, what changes, and what still needs proof. If needed, book one focused demo and keep questions on corridor coverage and compliance fit for your markets.

If you want this to stick, set a short review after the cycle closes. Check where timing slipped, where approvals slowed release, and where evidence was missing. Update your written steps immediately while details are fresh. Small edits each cycle create a payment process that gets more predictable instead of more complicated.

Frequently Asked Questions

What is fintech for offshore companies in practical terms for freelancers and small teams?

In practice, it usually means the payment stack between invoice and usable cash. It covers how you collect funds, where they arrive, when you convert, and how you withdraw. If a choice changes payout timing or fee drag, it belongs in this stack.

How can an offshore freelancer reduce payment delays without hurting close rates?

Keep the client payment path simple, then add stricter checks after payment is confirmed. For higher-risk engagements, use deposits and milestone invoices before extending longer terms. This protects cashflow without adding avoidable checkout friction.

What are the biggest payment risks for offshore service businesses, and what is the first mitigation for each?

A common risk is disruption between payment confirmation and usable cash, including transfer and payout exceptions that slow release. A practical first response is triage: pause the affected release, open a provider trace, and send a clear client update with the next status time. Keep one complete case record per disputed payment so resolution is faster and decisions stay consistent.

What should be in a minimum fintech stack for an offshore company handling cross-border clients?

A minimum stack can be one collection rail, one multi-currency receiving layer, one payout rail, and one reconciliation export into your ledger. Add a backup receive or payout path so a single account issue does not block obligations. Keep a final beneficiary-check step before higher-value releases.

How do you choose between **Wise Business**, **Revolut Business**, and other multi-currency account options?

Start with your main payment corridors and test inbound reliability and withdrawal timing before optimizing for small FX differences. Wise states pay-for-use pricing with no subscription plans, says sending fees vary by currency from 0.57%, applies discounts after 25,000 USD in monthly transfers, and lists fixed receiving fees such as 6.11 USD for USD wire and Swift payments. For Revolut, confirm business-plan terms for your country and account type separately, since the excerpt available here is a Personal Fees (Standard Plan) page rather than a Revolut Business fee schedule.

What is the difference between offshore fintech decisions and offshoring models like **staff augmentation** or **Build-Operate-Transfer (BOT)**?

They are separate decisions. Fintech choices usually determine settlement timing, fee exposure, and when cash is available. Staffing models should be evaluated on their own and should not be used as a substitute for payment choices.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- home.treasury.gov/sites/default/files/2018-08/A-Financial-Syst...trusted

- home.treasury.gov/system/files/261/FSOC2025AnnualReport.pdftrusted

- sec.gov/Archives/edgar/data/2003292/0001628280250128...trusted

- sec.gov/Archives/edgar/data/1761055/0001193125242376...trusted

- stripe.com/pricingtrusted

- wise.com/us/pricing/receivetrusted

- fintech.global/regtech100/wp-content/uploads/2021/12/RegTec...external

- globalfintechseries.com/finance/tax-ibn-technologiespreparation-and-...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Automating Your Freelance Finances: A Zapier Workflow for Connecting Stripe, QuickBooks, and Wise

Cleaner books and fewer month-end fire drills come from sequence, not software. Run this in the right order: structure, compliance, accounting architecture, then automation.

How to Conduct a Client Post-Mortem and Gather Feedback

A client post-mortem turns finished work into better future delivery. It is not admin for the sake of admin. It is the step that helps you keep what worked, fix what failed, and reduce repeat friction before the next engagement starts.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.