Quick Answer

Mercury is the better-documented option for a non-resident LLC in the material reviewed here, while RelayFi may suit operators who want simpler day-to-day budgeting if its current rules are confirmed first. The safer choice depends on address handling, document coherence, payment-rail needs, and whether you keep a backup collection path active in case a review interrupts cashflow.

Why choosing between Mercury and RelayFi is a continuity decision, not a signup-speed contest#

Pick the setup that keeps money moving under pressure, then worry about nicer features.

For a non-resident LLC choosing between Mercury and RelayFi, opening the account is only the first test. The harder question is what happens later, when a review starts, a billing issue appears, or an address field gets challenged and you still need collections and payouts to work.

This comparison starts from that reality. Use it to weigh onboarding friction against day-to-day reliability. It is not legal or tax advice. Use it as a decision tool to spot where risk sits in your setup before you let one provider sit in the middle of all client payments.

Public guidance on non-U.S. resident LLC banking has tightened over the past year, and public claims about the easiest approval path have shifted with it. That is why the right standard here is continuity, not initial approval alone.

| Decision lens | Why it matters | What to verify early |

|---|---|---|

| Approval friction | Unclear eligibility can delay first invoices | Required documents and remote application path |

| Operating fit | The wrong setup can create avoidable payment issues | Whether you need API-oriented processes or clearer multi-account budgeting |

| Disruption resilience | Delays can strain cashflow quickly | A backup collection path instead of a single-account setup |

The practical split between these two options is operating style. Mercury is often positioned as more technology-oriented, including API integration. Relay is often framed around clarity and operational efficiency, including multiple checking accounts in one dashboard. That difference matters, but it should not outrank your ability to keep revenue moving when something goes sideways.

Remote onboarding also needs to be read correctly. Many non-U.S. residents can apply without traveling to the U.S., but remote access does not mean a lighter review. It only means the first step can happen from abroad. A weak file is still a weak file.

So the working rule for the rest of this piece is simple: first choose the option that best fits how you operate, then make sure one provider problem cannot stop collections. If one payout delay would put pressure on payroll, rent, or vendor obligations, do not build your whole setup around a single rail. Open the account that best fits your business, then keep a second collection path active.

That is the thread through the rest of the article: compare what is actually documented, identify the gaps that need written confirmation, and build enough redundancy that one review does not become a cash crisis. You might also find this useful: The Best Bank Accounts for Freelancers in Italy.

Mercury vs RelayFi at a glance#

Start with what is documented, then treat every unclear point as risk until you get it confirmed in writing.

| Criteria | Mercury | RelayFi |

|---|---|---|

| Non-resident onboarding clarity | States support for U.S. companies founded by people outside the U.S.; requires U.S. formation and registration, and lists formation documents, EIN documentation, and government ID. | No verified non-resident eligibility or required-document detail is established here; confirm current policy directly. |

| Address posture | Requires a principal place of business address; says this field cannot be a registered agent, P.O. box, or UPS box. | No verified policy detail here on registered agent address or virtual mail services; request written guidance before applying. |

| Operating model fit | Public terms include a $0/mo baseline and paid tiers ($29.90/mo, $299/mo). | Confirm current tier or feature detail directly with RelayFi. |

| Payments rails to check | Lists ACH, wire, and check. Support docs say no fees for domestic wires, ACH, and checks, and Mercury markets free domestic and international USD wires. | Equivalent current rail and fee detail is not included here; verify ACH and wire scope directly. |

| Stability discipline needed | Identity documentation is required for control person(s) and owners at 25%+; unpaid subscription can lead to a 7-day grace period and then feature loss after unsubscribe. | Review posture and disruption triggers are not documented here; plan for re-verification risk. |

The short version is this: Mercury publishes more of the operating detail that matters for a non-resident file, at least based on what's documented here. Relay may still be the better fit for some operators, but the lack of verified policy detail means you have to do more direct confirmation work before you rely on it.

Known vs unknown: Known: Mercury publishes specific onboarding fields, ownership-threshold language, rails, and plan mechanics. Unknown: an authoritative side-by-side non-resident rulebook for RelayFi is not provided here.

That distinction matters because comparison tables can create a false sense of symmetry. They make both options look equally knowable even when they are not. In practice, one side may be documented and the other may still depend on support replies, product screenshots, or community anecdotes. Those are not the same level of certainty.

Use the same three filters through the rest of the article: approval friction, control model, and disruption resilience. If a provider does not answer one of those cleanly, that gap belongs on your risk list.

Mercury also states that it is a fintech company, and says banking services are provided through partner banks that are FDIC members. Its FAQ also references up to $5M in FDIC insurance. Those details are useful, but they do not replace the need to confirm current terms, plan mechanics, and rail scope before you route critical payments through the account.

A practical reading rule for this table is simple. Unknown does not mean acceptable. Unknown means follow-up required. If a missing detail could affect approval, account use, or access during a review, get the answer before you submit. That is especially true for address handling, remote onboarding, and what happens if your operating pattern changes after approval.

That takes us to the real approval question. Most files do not fail because one document is missing. They fail because the whole story does not hang together cleanly.

What non-resident approval actually checks#

Approval usually turns on coherence more than any single document.

A verified Mercury or RelayFi approval checklist is not established here, so the most useful pre-check is whether your business story, documents, and expected account activity all line up on first read. Reviewers are not just looking for paperwork. They are looking for a file that makes sense without extra interpretation.

Signals on ease are mixed. Some sources describe remote onboarding as straightforward, while others describe non-resident business accounts as difficult or sometimes not possible. Read that as uncertainty, not as a promise either way. A remote application path only helps if the file itself is clean.

Before you apply to either provider, run this pre-check:

- Entity and tax consistency: Keep formation records ready, and make sure the legal name matches everywhere.

- Business profile clarity: Prepare a short plain-language summary of what you sell, who pays you, and expected transaction patterns.

- Application coherence: Keep ownership and business details consistent across the materials you submit.

- Provider structure and custody model: Confirm whether you are onboarding with a fintech provider and how partner-bank custody works.

- Protection language: Confirm the exact FDIC wording you are relying on and how it applies to your account setup.

- Remote onboarding scope: Confirm current remote onboarding availability for your situation in writing.

It works because it mirrors how a reviewer will likely read the file. First the entity. Then the people behind it. Then the activity. Then the practical details, including where the business operates and how the account will be used. If those pieces conflict, the reviewer has to guess. Once a reviewer starts guessing, your timeline gets worse.

One useful checkpoint before submission is to ask a teammate or advisor to read your package as a stranger. If they cannot quickly explain what your company does, who owns it, and how money flows in and out, a reviewer may struggle too. Fix that before you apply.

Another useful test is sequencing. Read the file in the order a reviewer may see it: entity first, people second, activity third, address support last. If that sequence creates obvious unanswered questions, your application is not ready. You want the reader to move from one item to the next without having to wonder why a company formed in one place operates from another, why one person controls the account while another owns it, or why expected payment patterns do not match the business description.

In practice, many avoidable delays start here. Operators focus on collecting documents, not on whether those documents tell one consistent story. A complete file can still be a weak file if it creates friction at every handoff.

That same logic carries into address handling. You can have a clear business description and still slow the review down if the address fields do not match the story.

Address rules that cause the most mistakes#

Address mistakes are one of the fastest ways to turn a straightforward file into a messy one.

The common failure mode is not one fake or obviously wrong document. It is blended address roles. Legal, operating, and owner identity addresses get mixed together, and the file starts to look inconsistent even when each underlying document is real.

In practice, keep the address roles separate. Treat legal formation, trading or operating, and beneficial-owner identity addresses as distinct fields whenever forms ask for them. Reusing one address in every box may feel tidy, but it often creates extra review when records no longer match the business story.

Community reports from late 2024 to early 2025 suggest this pattern, but they are not official Mercury or Relay policy. One Relay-related post claimed a physical U.S. address requirement. One Wise case described a personal residence ID being rejected for trading-address verification in favor of business-name documents. Treat those as risk signals, not universal rules.

The practical lesson is that trading-address checks can be sensitive to both name and recency. In one reported flow, documents issued within the last 3 months to the business name were requested. Whether that happens in your case or not, the safer move is the same: prepare the cleanest address pack you can before you submit.

Fix these red flags first:

- Trading address in the form does not match business documents or profile data.

- A legal or registered address appears in fields meant for actual operating activity without explanation.

- Owner ID proves only a personal address, while business documents do not support the submitted trading address.

- Two trading addresses appear across countries without stating which one governs the account.

- Address documents are old or issued to a person instead of the business.

If any of those show up, stop and reconcile them before you apply. It is much easier to submit one clean address narrative than to unwind a mixed file after review starts.

One simple control helps here. Keep a one-page address map in your folder that lists each address, the field where it belongs, and the supporting document tied to that field. That page can prevent a surprising number of copy-paste mistakes, especially if you revise the application later or apply to more than one provider.

File organization matters too. Arrange support files by address role before submission. Put legal-address records together, business-operating records together, and owner-identity records together instead of dumping everything into one unsorted folder. If a provider later asks which document supports a specific field, you can answer directly instead of resending the whole pack and hoping the reviewer makes the connection.

If a label on the application is ambiguous, do not improvise. Ask Mercury or Relay to clarify the field in writing. Address review is rarely helped by assumptions.

Once the address story is under control, the next question is practical fit. A provider can be approvable and still be the wrong tool for how you actually run the business.

Feature fit for freelancers and small teams#

For most freelancers and small teams, the right account makes routine money handling boring and predictable.

So the first decision rule is simple: prioritize clear day-to-day cash control, then pay for deeper automation only when your volume and process complexity justify it.

| Usage lens | Mercury (documented) | RelayFi (confirm directly) |

|---|---|---|

| Daily money control | Approval rules for large purchases and auto-transfer rules between accounts. | Whether account structure and permissions give the same clarity for routine budgeting and spend control. |

| Automation depth | Paid plans are positioned for more control, customization, and automation; Plus includes Invoicing API capacity of 500 invoices/month. | Whether API scope, limits, and permissions match your tools and approval flow. |

| Payment execution | Scheduled and recurring payments via ACH, wire, and check; domestic ACH, domestic wires, and checks are listed with no fees. | Whether ACH and wire behavior, limits, and international wire scope fit your payout patterns. |

| Advanced products | Treasury is unlocked with a $250K Mercury balance; FAQ also references treasury management and venture debt options. | Whether equivalent advanced options exist and what eligibility thresholds apply. |

| Plan economics | Baseline is $0/mo, with paid tiers at $29.90/mo and $299/mo. | Current tier pricing and which features are gated by plan. |

The tradeoff is simple. If your main problem is reserve discipline, mixed funds, or poor payout visibility, account structure matters most. If your main problem is repetitive finance work across invoices, approvals, and reporting, then API depth and automation start to matter more.

A quick fit check keeps this grounded:

- Stay on the baseline plan if volume is modest and the core tools already cover your process.

- Upgrade only when added controls or automation replace recurring manual work.

- If international wires are critical, confirm currency and corridor scope in writing before routing key payments.

- If treasury access is part of your plan, verify you can maintain the

$250Kbalance threshold.

That last point is easy to miss. A feature that looks attractive during comparison is not really part of your operating setup if you cannot meet the balance or plan conditions that unlock it. In practice, many people compare the top of the feature ladder without checking whether they will actually live there.

Mercury's billing mechanics also matter as more than pricing if your processes depend on paid features. Before committing, verify plan details in Settings > Plan & Billing > View all Plans. Billing renews on the first of the month, and a failed subscription payment can enter a 7-day grace period before paid features are removed. If a workflow depends on those features, a missed billing event becomes an operations risk, not just an admin annoyance.

The cleanest way to compare fit is to run a week of mock operations on paper before you commit. Write down how you would collect invoices, approve spend, and run payouts using your current workload. Then check whether the provider supports that pattern with minimal patching. That exercise usually tells you more than a feature page.

Go one step further and mark where failure would hurt most. For one business, that may be delayed invoices. For another, it may be confusion about which sub-account holds tax money or contractor payments. The better fit is usually the one that makes your highest-stress routine simple and repeatable, not the one with the longest marketing page.

Once you frame the choice that way, pricing becomes easier to read too. The real cost problem is rarely the headline fee. It is what happens when friction interrupts normal operations.

Hidden costs and constraints people miss#

The biggest cost here is usually not the monthly fee. It is interruption.

If review drags, access changes, or a document issue freezes action, invoices, payroll, or contractor payouts do not wait for the provider to catch up. That is why continuity risk usually matters more than small pricing differences.

Eligibility ambiguity is the first hidden cost. Public claims conflict on remote access. Some say non-U.S. founders can open from abroad, while others say remote acceptance tightened in 2024 to 2025. Treat eligibility as case-specific and get written confirmation for your ownership profile, country exposure, and signing method before you submit. Otherwise you can lose time building around an account path that was never cleanly available to you.

Review overhead is the second hidden cost. Compliance paths can include Customer Due Diligence, Enhanced Due Diligence for higher-risk exposure, and ongoing suspicious activity monitoring. One non-resident account narrative describes review stretching from two weeks to three weeks to one month, with business activity effectively stalled. Even if your case is simpler, the lesson holds: the operational cost of waiting is often larger than the visible account fee.

Document logistics are the third hidden cost. A reported checklist includes an executed Operating Agreement and, when a U.S. representative opens the account, written LLC authorization. Some cases may also require notarized signatures at a U.S. embassy or consulate. None of that is complicated in theory, but it becomes painful when you are gathering it after a review request lands.

Do not assume: anecdotes or rankings can predict your approval outcome. Treat them as directional, not definitive.

Support expectations matter here too. If your team assumes fast answers but your case enters extended review, internal stress rises quickly. Decide in advance who handles document replies, who updates clients, and who controls payout priorities while access is uncertain. That feels administrative until the first review notice arrives. Then it is suddenly operational.

Another hidden cost is rework. When the first application folder is sloppy, every later request takes longer because you are renaming files, checking mismatched addresses, and rewriting the same business description in different words. Clean preparation reduces not only review friction but also the labor cost of every follow-up after submission.

If one delayed payout would hurt rent, payroll, or vendor commitments, set up a backup collection rail before relying on a single provider. Even modest transfer-fee differences can cost less than a frozen week. Cash shortfalls are a common reason businesses fail, which is why continuity should outrank minor price gaps.

That makes the next step fairly obvious. Before you click submit anywhere, build one file that is strong enough to survive both onboarding and follow-up questions.

Pre-application checklist before you submit anywhere#

Do not submit until the file can be reviewed cleanly without extra explanation.

The best way to get there is to build one reusable application folder, then tailor it only after each provider confirms current requirements. That approach keeps you from rebuilding the same packet under time pressure and makes it easier to respond consistently if questions come later.

At minimum, that folder should cover four things:

- Entity foundation: your state-choice rationale (investor expectations, fees, franchise tax, and where business is conducted), plus LLC formation filing (Articles of Organization or Certificate of Formation).

- Registered agent details: registered agent name and required physical U.S. address for service of process in the formation state.

- Ownership and tax records: tax identity records you already have (such as an EIN letter, if issued), plus a clear ownership and control summary.

- Business profile: short plain-language description of what you sell, who pays you, and typical transaction patterns.

The discipline here is consistency, not volume. Before submitting, run a strict line-by-line check across documents and form drafts. Legal entity name, state, registered agent details, and address fields should match exactly. If they do not, fix the source issue rather than explaining around it later.

Also check whether your operating footprint could create nexus in another state, since that can trigger extra filings or taxes. That may feel outside the banking question, but it affects whether your overall story holds together.

Use a hard go or no-go gate:

- No-go if identity or address fields conflict across records and forms.

- No-go if registered agent information is incomplete or used inconsistently.

- No-go if ownership or control details are unclear.

- No-go if business activity description is too vague to review cleanly.

- No-go if possible nexus-related filing issues are unresolved.

A good working habit is version control for the whole application pack. Date each revision, keep one current copy, and archive replaced files. When a provider asks for clarification, you want one source of truth, not three nearly identical folders with small differences.

It also helps to keep a short internal cover note, even if you never send it. In a few lines, state the legal entity name, who owns and controls it, what it sells, where it operates, which address belongs in which field, and which documents support those points. That note gives you a stable script for emails, forms, and support tickets, so your responses do not drift under pressure.

Final step: provider-specific onboarding requirements are not confirmed here, so verify current requirements with each provider right before submission and validate your folder against that list. This will not guarantee approval, but it will reduce preventable friction.

Before you apply, standardize your client billing records so your business profile stays consistent. Keep a clean invoice trail, and use the Free Invoice Generator if needed.

Good preparation should also survive the period after approval. That is where the first 90 days matter.

First 90 days controls to reduce freeze risk#

The first 90 days are about record discipline, not clever tactics.

This section does not include a provider-specific trigger list, so there is little value in guessing what Mercury or RelayFi may flag. The better approach is to keep your own records clean enough that any later question is easy to answer.

A simple monthly routine is usually enough:

- Check that entity and owner details stay current across records and account profile.

- Reconcile incoming and outgoing transfers to invoices, contracts, or delivery proof.

- Scan for abrupt pattern changes in volume, ticket size, counterparties, or timing, then document context early.

- Keep a lightweight evidence pack organized by month so review questions are faster to answer.

The point is not to create paperwork for its own sake. It is to make future questions answerable in one pass. If a payment looks unusual later, you should be able to pull the supporting invoice, contract, or short explanation without reconstructing the whole month from memory.

If activity is about to change, prepare the explanation and supporting records before the change lands. This does not guarantee a specific outcome, but it puts you in a much better position if a review starts. The difference between a manageable review and a disruptive one is often whether the context already exists when the question arrives.

Turn this into calendar discipline. Pick one recurring day each month, run the same checks in the same order, and log what changed. That keeps compliance work small and predictable instead of letting it pile up into a cleanup project.

A lean evidence pack is usually enough if it is organized. Match incoming payments to invoices, match outgoing payments to vendors or operating needs, and keep short notes for anything that would look unusual without context. Short and orderly beats exhaustive and chaotic.

If a review does happen, this routine pays off immediately. You are no longer scrambling to prove what happened. You are simply packaging records you already maintain.

What to do if an account review happens#

If your account goes under review, move on two tracks at the same time: send one complete response quickly, and protect incoming cashflow through a backup collection rail.

Doing only one of those is how a small issue turns into a business interruption. A clean response helps the review. A live backup rail protects the business while the review runs.

Work from a timeline you control. Acknowledge the request, confirm exactly what is needed, submit a complete package, and track every follow-up in one place. Reviews can run longer than expected. One published non-resident case describes waits of two weeks, then three weeks, then one month before another document request.

A practical response sequence looks like this:

- Acknowledge promptly and confirm required items in writing.

- Submit one complete package instead of drip-feeding files across threads.

- Index files clearly and map each requested item to the matching document.

- Keep one follow-up log with dates, requests, submissions, and next actions.

- Follow up on a consistent cadence tied to unresolved items.

The quality of the response pack matters more than the volume of material. Prepare a template before problems appear. Include core entity records, beneficial ownership verification records, and business-activity evidence. If a transfer may look unusual, add a short written explanation so the reviewer does not have to infer the story from raw documents alone.

When you reply, stay narrow. Answer the exact question, map the answer to the attached file, and avoid mixing unrelated issues into the same message unless the provider asked for them together. A tidy response gives the reviewer a cleaner path to move the case forward and reduces the chance of getting the same question back in a different form.

At the same time, protect cashflow. One account is a single point of failure, while multiple banking partners reduce disruption if one account is frozen or inaccessible. Keep a secondary collection rail active without assuming that any one backup guarantees uninterrupted service.

While review is open, stage payouts by priority. Cover essential outflows first, delay non-critical spend, and make sure clients know which rail to use now. Treat review as a contained incident with clear communication, complete evidence, and active backup collections.

If your team has more than one person, assign roles before review happens. One person owns provider communication. One prepares documents. One updates clients and internal cash forecasts. Clear ownership reduces delays and mixed messages when timing is tight.

This is also where your provider choice gets easier to judge. The right option is not just the one that looks good in normal weeks. It is the one that you can explain, document, and back up when a review lands at the wrong time.

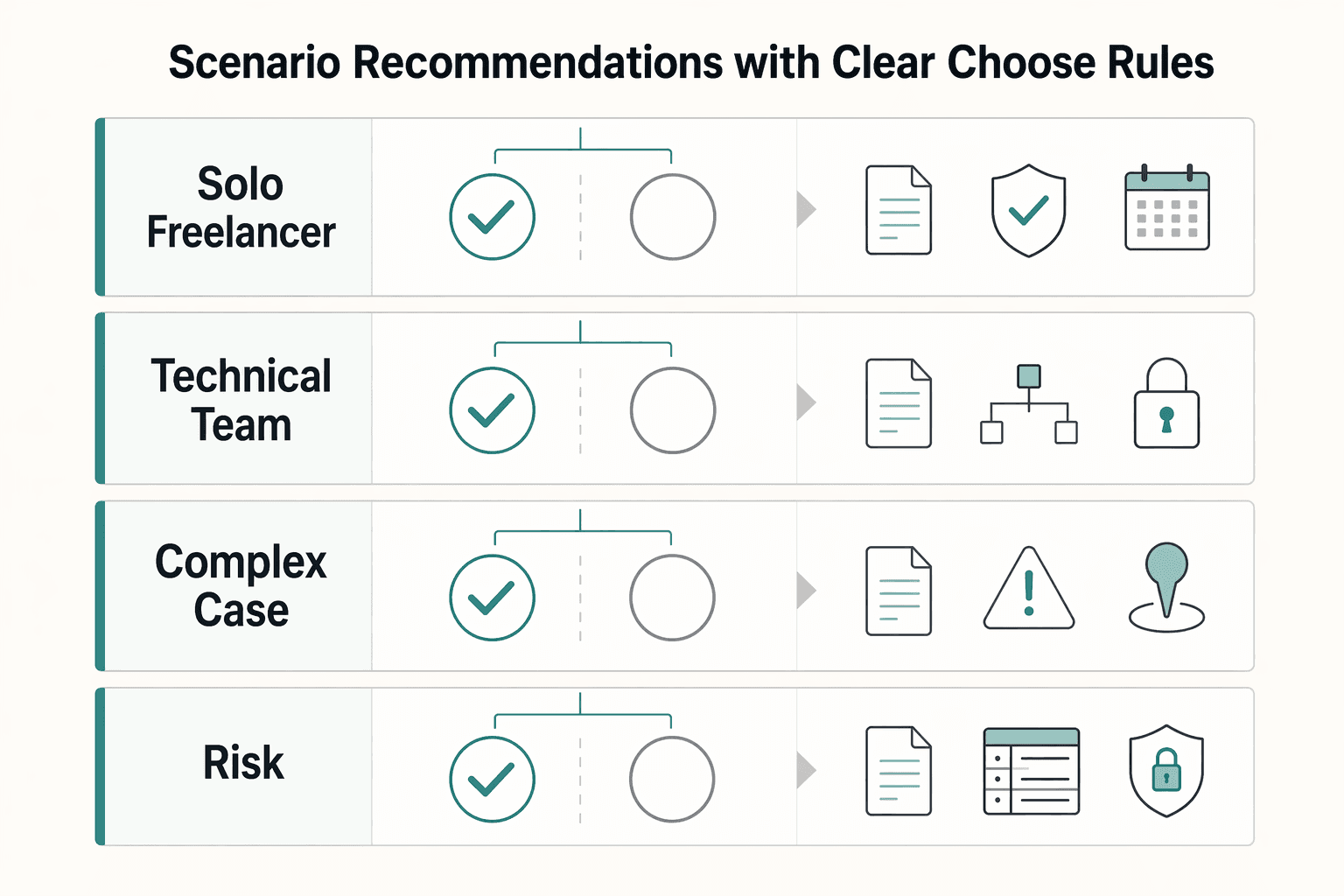

Scenario recommendations with clear choose rules#

Choose by failure mode first.

Pick the option that best protects cash flow in your operating scenario, then verify unresolved policy details in writing before routing core revenue through it. That keeps the decision grounded in what can go wrong, not just what looks attractive during setup.

| Scenario | Better first fit | Why this is safer | What to verify before committing |

|---|---|---|---|

| Solo freelancer, variable invoices, light tooling | Relay-leaning | Relay is described as stronger for day-to-day budgeting, including cash flow account separation with multiple checking accounts in one dashboard. | Current tiers, limits, and how account structure maps to your invoicing pattern. |

| Technical team with automation needs | Mercury-leaning | Mercury is described as more technology-oriented, with API capabilities and integrations (QuickBooks, Xero, Stripe, PayPal). | API scope, permissions, limits, and controls for your expected process. |

| Address complexity is your top risk | Whichever gives clearer written guidance now | Confirm address edge-case rules with Mercury or RelayFi directly. | Exact handling of registered agent address details and required supporting records for your entity profile. |

| Downtime risk is unacceptable | Multi-rail setup regardless of primary choice | Single-account dependence can create a single point of failure during review or access disruption. | Backup collection readiness, tested payout fallback, and client communication steps. |

The table gives you a first direction, not a final answer. The practical choice still depends on how much confidence you can get around the unresolved items.

If you are non-technical and mostly need cleaner budgeting, prioritize account separation and day-to-day control. If finance operations depend on integrations, prioritize API depth and confirm current eligibility for advanced features. One source mentions a historical $250,000 threshold for upgraded Mercury services, so confirm current requirements directly.

Also verify live pricing before deciding. The material reviewed here includes a conflict: one source cites a Relay Pro tier at $30 monthly, while another says both platforms have no monthly fees. Do not let stale price snapshots decide the issue for you.

When two options both look workable, break the tie with downside risk. Ask which choice is easier to explain during review, easier to back up with a second rail, and easier for clients to follow during a payment change. Those questions usually lead to a better decision than comparing screens or small fee differences.

Operational effort is another good tie-breaker. If one option requires more manual work to keep invoices, approvals, and account structure aligned with how you already operate, that extra admin load becomes part of the real price. The safer choice is often the one your team can run cleanly even during a busy month.

From there, the next move is practical. Whatever primary option you choose, build the failover path before you need it.

Build a two-rail get-paid setup so one provider issue does not stop revenue#

Whatever primary account you choose, this is the step that makes the whole setup sturdier.

A two-rail arrangement will not remove review or access risk, but it does lower the chance that one provider issue stops collections or urgent payouts. For most non-resident operators, that matters more than squeezing the last bit of efficiency out of a single account.

Use this structure:

- Rail A: day-to-day account (for example,

Mercury) for normal invoicing and payouts. - Rail B: separate backup collection rail with current beneficiary details and tested payout access.

- Switch instructions: one-page procedure with owners, failover triggers, client communication text, and recovery steps.

Minimum switch checkpoints:

- Define failover triggers, such as transfer disruption, access issues, or loss of a required paid-plan feature.

- Send updated payment instructions to active clients and confirm receipt for priority invoices.

- Route new collections to Rail B first, then prioritize outgoing payments.

- Move traffic back to Rail A in phases after stability returns.

The key idea is that backup only counts if it is usable right now. A second account with stale beneficiary details, untested payout access, or old invoice instructions is not really a second rail. It is just a nice intention.

Before urgent payout windows, run operational checks and verify beneficiary details before release. Test ACH payments, and test international USD wires if you rely on them. A backup rail that has never been tested is only half a backup.

For Mercury specifically, treat billing status as an operations control. Support describes a 7-day grace period after failed subscription payment. After that, paid features may be lost, and recurring invoices can be canceled after unsubscription. Re-check recurring and scheduled payment behavior after any plan or billing change so you do not discover a gap during a busy week.

A simple resilience drill for freelancers and small teams looks like this:

- Run one small ACH test on each rail and confirm posting.

- Verify beneficiary details for at least one critical payout path.

- Simulate failover by routing new collections through Rail B for a short window.

- Reconcile drill activity and keep a record.

Keep the switch procedure visible, not buried in an old folder. If only one person knows how to fail over, the setup is still fragile. Even for a solo operator, the instructions should be clear enough that you can follow them under pressure without trying to remember which client got which payment details or which scheduled payout needs to be paused first.

A final checkpoint before each drill is easy to overlook: make sure client-facing invoice templates for both rails are current. Outdated payment instructions can cause the backup path to fail at exactly the wrong moment.

As you scale, keep collection, conversion, and payout controls modular where supported so you can change rails without rebuilding your payment operations from scratch. The goal is not complexity. The goal is recoverability.

Conclusion#

Choose the setup that protects continuity, not the one that only looks easiest to open.

If one account becomes frozen or inaccessible, a single-rail model can disrupt collections and payouts at the moment you need them most. That is the real decision frame here.

Mercury is described as more technology-oriented, including an API-first integration posture. Relay is described as more operations-focused, including multiple checking accounts in one dashboard. Use that fit to choose your primary rail, but keep resilience as the first filter.

Policy signals can change, and third-party updates may conflict over time. Use current written guidance from each provider as your final checkpoint, especially on address handling, onboarding scope, and rail availability.

- Run the pre-application checklist and reconcile all document and address fields.

- Choose by scenario fit: account separation for budgeting clarity, or integration depth for automation-heavy operations.

- Activate a backup rail before high-stakes client payments.

- Confirm current provider requirements directly, then run your own first-90-days control routine.

Resilience first, fit second, convenience third. If one provider issue does not stop revenue movement, your setup is doing its job. Next step: pick your primary rail this week, schedule your first resilience drill, and confirm provider requirements in writing before your next major payout cycle.

If you want a second collection rail to reduce the chance that one provider issue blocks incoming payments, review Gruv Virtual Accounts where enabled.

Frequently Asked Questions

Can a non-resident LLC use a registered agent address for Mercury or RelayFi?

For Mercury, no. Mercury says the principal place of business cannot be a registered agent address, P.O. box, or UPS box, though it may be a U.S. or international address, including residential. RelayFi's current address rule is not verified in this material, so get written confirmation before applying.

Is a virtual mailbox likely to increase account freeze or review risk?

There is no verified direct freeze or review link for virtual mailbox use at Mercury or RelayFi. What is explicit is Mercury's restriction on using a registered agent, P.O. box, or UPS box as the principal address. If your setup depends on mailbox-style addressing, confirm accepted address types in writing before you apply.

Which is better for non-technical freelancers, Mercury or RelayFi?

There is not enough verified RelayFi detail here to name a definitive winner for non-technical freelancers. Choose the provider that gives clearer onboarding steps and simpler day-to-day handling for your case, after confirming address rules, required documents, and available payment rails in writing. If your work is simple and repetitive, clarity usually matters more than feature depth.

Does initial approval mean your account is safe from future account review?

No. Initial approval does not guarantee long-term continuity. For Mercury paid plans, a failed subscription payment can trigger a 7-day grace period, and plan unsubscription can remove paid features and cancel recurring invoices. Good records, stable profile data, and a backup rail still matter after approval.

What documents should I keep ready after onboarding to avoid payment disruption?

Keep formation documents, your IRS-issued EIN document, government ID records, and identity documentation for at least one person with operating control and any owner with at least 25% ownership. Also keep business-activity support such as invoices, contracts, or similar records that explain incoming and outgoing transfers. Organized records will not prevent review, but they can make your response faster and cleaner.

Are public approval-rate claims for Mercury and Relay reliable enough to decide on their own?

No. This comparison does not include verified side-by-side approval-rate benchmarks for Mercury and RelayFi. Use documented policy details, your risk tolerance, and direct written confirmations instead of treating public approval stories as decision-grade evidence.

Should I keep Wise or another backup rail even after one account is approved?

Yes, if downtime would disrupt payroll, rent, or supplier payments. The article says Wise uses a pay-as-you-go model with no subscription plans, but fees vary by route and method. Keep any backup rail usable by maintaining current beneficiary details, testing the path, and keeping client payment instructions ready.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 5 external sources outside the trusted-domain allowlist.

- businessanywhere.io/5-best-neobanks-or-fintech-platforms-for-sma...external

- foundeck.com/blog/llc-business-bank-accounts-for-non-us-r...external

- llcuniversity.com/foreigners/open-us-bank-account-llc-non-resi...external

- offshorecorptalk.com/threads/are-there-any-real-alternatives-to-m...external

- xpezia.com.pk/blog/the-hidden-risks-of-cheap-us-llc-format...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Does My Freelance Website Need a Cookie Banner?

Treat this like any risk-sensitive web deliverable: make one clear decision, wire the site to that decision, and keep proof it works. If your site uses nonessential tracking for analytics, advertising, or personalization, ask first and track second. If it uses only strictly necessary functionality, a short notice and a clear privacy policy may be enough, but only after you verify what actually loads in a clean session.

How to Stay Motivated When You Work for Yourself

**Step 1. Reframe the problem as business continuity.** If you work for yourself, the goal is not to feel inspired every morning. The goal is to keep delivery quality steady when your energy, focus, or mood drops. For a freelancer or solopreneur, that means protecting core business outcomes: output consistent enough to ship, clear commitments you can meet, and client confidence that your work habits are dependable.

The Best Bank Accounts for Freelancers in Italy

Choose for payout reliability and predictable operating cost first. Base fees matter, but they do not help if onboarding or transfer routes fail when invoices are due. In one sitting, narrow to two candidates, score them with the same gates, and validate both with live transactions in your first month.