Quick Answer

For most bootstrapped SaaS businesses, Mercury is the better default when runway control, predictable cash flow, and clean banking separation matter most. It works more like a banking core with cash-led spending and simpler records. Brex fits better if you need built-in spend controls, reimbursements, approvals, and broader integrations, and you can handle tighter eligibility rules and repayment discipline.

Mercury vs. Brex: Are You Building a Financial Fortress or a Growth Cockpit?#

For a bootstrapped SaaS operator focused on runway control, predictable cash flow, and clean separation between personal and business finances, this is mostly a model choice once eligibility is confirmed. Mercury is closer to a banking core, while Brex is closer to a corporate card plus expense-control stack.

In plain terms, a banking core is your base account layer: checking, savings, cards, and payments. A corporate card program centers on business credit spend with built-in controls. Expense management is where spend parameters and policy controls get applied. Cash-management features may include treasury-style options, which are not the same thing as insured bank deposits.

| Platform | Account model | Spend model | Control model | Typical operational tradeoff |

|---|---|---|---|---|

| Mercury | Business banking base with checking, savings, cards, and payments | Account-funded spend and payments | Control through account design and API-driven automation | Can improve cash visibility, but may require more internal process design on your side |

| Brex | Cash account + card-led finance stack | Corporate card spend; repayment can be monthly or as short as one business day, depending on account type | Built-in spend controls and budget guardrails at the card layer | Can speed up spend governance, but with tighter dependence on Brex eligibility and card-program terms |

| Both | Product terms and structures can change over time | Business finance workflows | Require current-doc verification before rollout | Re-check eligibility, legal terms, and current feature details before implementation |

Use this three-part lens through the rest of the article: risk tolerance, finance-ops bandwidth, and growth tempo. If you prioritize strict cash discipline and clean records, start with the fortress lens in Pillar 1 and Pillar 2. If your main pain is scaling team spend with tighter controls, start with the cockpit lens in Pillar 2 and Pillar 3. If treasury positioning is part of the decision, use Pillar 3 with extra caution around product terms and risk disclosures.

Before implementation, confirm current eligibility and legal terms. Mercury requires a U.S.-formed entity and says international founders may be accepted subject to partner-bank restrictions. Brex requires a U.S. EIN, valid U.S. incorporation, U.S. operations, and a U.S. physical address. Do not assume advertised yields are guaranteed or risk-free, and do not assume today's limits or terms will stay fixed.

If that is your use case, this may help: How to Use Brex for a Venture-Backed Startup with a Remote Team.

Pillar 1: The Fortress - Protecting Your Personal Assets#

If your priority is a defensible wall between company money and personal money, start with the setup that is easiest to keep clean every month. Mercury can fit that fortress posture with a cash-led operating model. Brex can still work, but it asks more of your card policy and reconciliation discipline.

What "protecting personal assets" actually means#

Protection has three separate parts. Keep them distinct when you review your setup:

- Legal liability protection: your entity structure is the foundation.

- Banking segregation discipline: keep business and personal accounts separate, and avoid commingling.

- Spending-risk controls: define who can spend, from which account, at what limit, and how repayment is handled.

In practice, neither platform fixes weak habits. Clean legal formation with messy owner transfers is still messy. Deposit-insurance language is not a substitute for clean separation. Mercury notes that pass-through insurance depends on specific conditions.

Where exposure actually appears#

The important difference is not simply debit versus card. It is where problems show up when cash gets tight or records are reviewed.

| Exposure point | Mercury | Brex | Why it matters |

|---|---|---|---|

| Core spend rail | Cash-led debit spend from a selected checking account with set limits; also offers an IO card path for eligible organizations. | Card-led spend with limits set via cash-based and/or revenue-based underwriting. | Cash-led spend is usually simpler to map to available funds; card-led adds another monitoring layer. |

| Personal guarantee dependency | Debit spend pulls from company cash rather than creating a separate card balance. If using Mercury IO, verify current terms before rollout. | Brex states business underwriting and says applying does not affect personal credit score; confirm live agreement terms before implementation. | This is the row to verify carefully if founder-level exposure is your main concern. |

| Cash and repayment mechanics | Debit draws directly from company cash. Mercury IO materials describe daily repayment and lower limits initially, with higher limits and monthly repayment at a $15K balance threshold. | Brex says the card is not secured and does not require collateral/security deposit; cleared transactions are auto-paid daily or monthly by account type. | Auto-repayment cadence can become the stress point during thin cash periods. |

| Statement complexity | Often cleaner because outflows are direct cash movements. | More moving parts: card activity plus automatic statement payments. | Cleaner records are easier to defend during bookkeeping, tax, diligence, or lending review. |

| Failure mode under cash pressure | Cash pressure tends to show up immediately because spend pulls from company cash. | With automatic daily or monthly repayment, pressure can surface around repayment timing. | One mode creates immediate friction; the other can concentrate pressure around repayment timing. |

For some bootstrapped SaaS teams, that last row is the practical tie-breaker.

The separation checklist that actually holds up#

The best protection here is boring, repeatable discipline, so run this monthly:

| Monthly control | What to verify | Article detail |

|---|---|---|

| Account structure hygiene | Business and personal activity stay separate | Business revenue lands in business accounts only; no personal bills from business funds. If using Mercury cards, confirm each card's source checking account and spend limits still match role and purpose. |

| Transaction labeling standards | Labels are explicit | Avoid vague labels like "transfer" or "misc." Use labels such as payroll, owner draw, capital contribution, or expense reimbursement so records clearly show income and expenses. |

| Reimbursement boundaries | Mixed-use items are split correctly | Personal, living, and family expenses are generally not deductible. For mixed-use expenses, split business and personal portions when recording the transaction. |

| Documentation habits | Core records are organized | Keep formation documents, EIN materials, key invoices, receipts, and written context for unusual owner transfers in one organized place. |

| Address compliance | Legal address is valid | Mercury requires a valid legal address, does not accept P.O. boxes or virtual offices/workspaces as legal address, and notes account access can be temporarily restricted if a valid legal address is missing. |

Run that table monthly. It is less glamorous than product features, but it is what keeps separation clean when cash is tight or records are reviewed later.

Personal underwriting readiness#

Do not assume either platform improves personal loan, lease, or mortgage outcomes. What you can control is record clarity: traceable business income, consistent owner pay or draw patterns, and clearly explained business-to-personal transfers. That often matters more than whether spend happened on debit or a corporate card.

Non-resident and compliance caveats#

Treat eligibility and onboarding as policy-dependent, not static. Mercury says applicants need a U.S.-formed or registered entity (including U.S. territories), says international founders may be accepted subject to partner restrictions, and says decisions are usually in 1-2 business days but may require additional documents. Because Mercury support content can vary by product and account type, re-check current entity requirements before relying on any fixed summary.

| Requirement | Mercury | Brex |

|---|---|---|

| Entity status | Applicants need a U.S.-formed or registered entity, including U.S. territories. | Only U.S.-organized or registered companies may apply. |

| Address or presence | Requires a valid legal address and does not accept P.O. boxes or virtual offices/workspaces as legal address. | All applicants need a U.S. physical address, and virtual-address applicants must have a beneficial owner or control officer with verifiable U.S. physical presence. |

| Review timing | Decisions are usually in 1-2 business days. | Review is expected in 1-3 business days. |

| Possible extra checks | International founders may be accepted subject to partner restrictions, and additional documents may be required. | May request SSN for KYC while stating it is not used for underwriting or a credit check. |

If you are a non-U.S. founder using a U.S. entity, verify the address and presence requirements before you spend time on feature comparisons.

In this pillar, choose the model you can keep clean under pressure, then enforce disciplined separation every month.

For that angle, see Mercury vs. RelayFi: Which is the Best US Bank Account for a Non-Resident LLC?.

Pillar 2: The Cockpit - Mastering Daily Financial Control#

Once the legal and cash-separation basics are set, the next question is operational control. Daily financial control means running money operations without month-end surprises. For a bootstrapped SaaS team, that usually comes down to four things: transaction visibility, approval discipline, reconciliation speed, and exception handling when receipts or syncs fail.

Mercury and Brex solve that in different ways. Mercury can offer more control over how workflows are built and owned. Brex offers a more prebuilt operating layer across spend, receipts, and accounting connections.

| Control area | Mercury | Brex | What it means in practice |

|---|---|---|---|

| Transaction visibility | Transactions can be reviewed with graphs, filters, and table tools in real time. | Brex emphasizes connected spend and accounting workflows through integrations. | Mercury fits teams that want bank-led monitoring; Brex fits teams that want controls centered around spend workflows. |

| Approval discipline and policy enforcement | Supports amount-based approval thresholds and separation of duties so initiators cannot approve their own payments. Roles determine what each user can and cannot do. | Spend limits include policy controls and amount limits for employee spend. | Both support discipline, but through different levers: payment-approval design versus spend-policy controls. |

| Accounting sync depth | Native integrations include QuickBooks Online, Xero, and NetSuite. Bank-feed syncing is automatic multiple times a day, with connector-specific setup steps and limitations. | Broad integrations across ERP, HRIS, messaging, and other systems. QuickBooks exports can match bank-feed entries for reconciliation; some accounting features are plan-dependent. | Mercury covers core accounting paths; Brex can connect across a wider stack, but plan and connector details need verification. |

| Receipt workflow quality | Grounding supports integrations and CSV fallback, but not a comparable built-in receipt-validation workflow claim. | Receipt flow includes validation and review flags; some auto-generated receipts can arrive 1-3 days later. | If receipt exception handling is a daily pain point, Brex has the clearer built-in process. |

| Automation setup burden and ownership | API supports programmatic access to accounts, transaction history, and payments for custom internal workflows. | Brex highlights broad integrations, while deeper ERP setups can still be multi-step, for example NetSuite setup and mapping. | Mercury can require more in-house ownership; Brex can reduce initial build work for standard stacks. |

| Manual fallback path | CSV export is available for manual import to your accounting system. | CSV export is also available for manual import. | Both provide a fallback when direct sync is constrained. |

Where Mercury helps, and where it can bite you#

Mercury is strongest when your workflow is specific and someone on your team can own it. The upside is control. You can shape automation around your process instead of forcing your process into a fixed connector.

The risk is governance drift. You need clear owners for automations, role permissions, and exception checks, plus active monitoring for failures. If an automation breaks quietly, payment approvals may still run while downstream reporting or internal controls fall behind.

Where Brex helps, and where lock-in shows up#

Brex can be strongest when finance ops bandwidth is limited and you want standardized controls working quickly. The tradeoff is dependency. When policy, receipts, categorization, and exports all sit in one system, later tool changes can mean process and mapping rework.

Before committing, run this reliability check:

| Reliability check | What to confirm | Article detail |

|---|---|---|

| Plan access | Needed accounting integration is on the current plan | Confirm the exact accounting integration you need is available on your current plan. |

| Receipt exceptions | Real transactions are tested end to end | Test real transactions end to end, including failed receipt validation and delayed receipt arrival windows. |

| QuickBooks aging | Process for older transactions is defined | For QuickBooks, verify how you will handle transactions older than 90 days. |

| NetSuite setup | Admin access and ERP limit work for the team | For NetSuite, confirm admin-access availability and whether the one-active-ERP limit is acceptable. |

The rule here is simple. Choose customization when your workflows are unique and manageable in-house. Choose integration when you need standardized controls with less internal build overhead.

If that is relevant, see A Freelancer's Guide to the US-UK Tax Treaty.

Pillar 3: The Engine - Fueling Capital-Efficient Growth#

Once daily control is handled, the growth question becomes less about features and more about how you fund motion without exposing the company to avoidable stress. For a bootstrapped SaaS, this pillar is mostly a runway decision. Mercury can favor tighter cash discipline, while Brex can support higher spend velocity if you actively manage liquidity and credit risk.

Keep these three terms in view as you compare the options:

- Idle-cash strategy: where unused cash sits, what it earns, and how quickly it returns to operations.

- Spending leverage: purchasing power created by underwriting-based credit, not just debit spend tied to current cash.

- Global-operating readiness: your ability to collect from customers, pay international vendors, reimburse team members, and control FX costs without fragile workarounds.

| Decision point | Mercury | Brex | What it means in practice |

|---|---|---|---|

| Yield access model | Mercury Treasury markets up to 3.67% with same-day access. Eligibility needs verification because captured pages show both $250K and $500,000 minimum balance thresholds. | Treasury markets up to 3.68% with no minimum deposit; the rates page says yield is variable and effective as of 03/27/26. | Brex is easier to start with at smaller balances. Mercury may become relevant as reserves grow, but confirm current eligibility before planning around it. |

| Liquidity constraints | Treasury emphasizes near-term access, but new sweep allocations can take up to 24 business hours. | Wires can only be sent and received from Checking. If funds are in Treasury or Vault, they must be moved first. | Brex adds a transfer step before some payments, which can become a failure point when timing is tight. |

| Sweep and protection mechanics | Sweep programs spread deposits across FDIC-insured program banks, and pass-through coverage applies only if conditions are met. | Yield applies only to invested Treasury funds, and Brex discloses that money market mutual funds can lose money. | Do not treat treasury balances like plain checking; document what stays liquid versus invested. |

| Card-driven spend flexibility | Cash-funded discipline keeps spend tied to available cash. | Card limits are underwriting-based on cash and/or revenue, not just debit balances. | Mercury can naturally limit overspending. Brex can increase throughput, but also raises the chance that spend outruns collections. |

| Operational complexity | Can be simpler when you want cash controls and payments closer together. | More moving parts across Checking, Treasury, card policy, and cross-border tools. | Brex can support scale, but requires tighter operational controls and plan-level verification. |

The core decision is not a tiny yield spread. The gap between 3.67% and 3.68% is usually less important than runway protection and cost of capital. Cash runway is how long you can operate before reserves run out, and cost of capital is the minimum return required to create value. If revenue timing slips, a small yield difference will not offset transfer delays, payment bottlenecks, or constrained spend.

Debit-funded discipline usually helps when sales cycles are uneven and you want every expense grounded in available cash. Credit-enabled throughput can help when you prepay software, spend before collections settle, or need short-term flexibility for vendor and travel commitments. It hurts when credit is covering a timing gap you have not modeled.

Before deciding, run this global-readiness check:

- Customer collections: confirm the exact inbound rails you need, not only outbound wire capability.

- Vendor payouts: Mercury supports non-USD outbound wires in 40+ currencies with a stated 1% conversion fee; Brex says payments can be made in 30+ local currencies, but verify plan access.

- Team reimbursements: Brex markets reimbursements in 40+ countries; test the real approval and payout workflow.

- FX exposure controls: Brex discloses card FX markup of up to 3% for international use, while Mercury discloses a 1% conversion fee on non-USD wires. Compare by your actual payment mix, since these are different cost mechanisms.

Recommendation: choose Mercury when protecting runway is the primary goal. Choose Brex when higher spending throughput or broader global operations clearly outweigh the added liquidity checks. During evaluation, save current screenshots of eligibility, rates, and wire rules. Those details can change the decision.

For the downside-planning side of this, see How to Create a Disaster Recovery Plan for a SaaS Business.

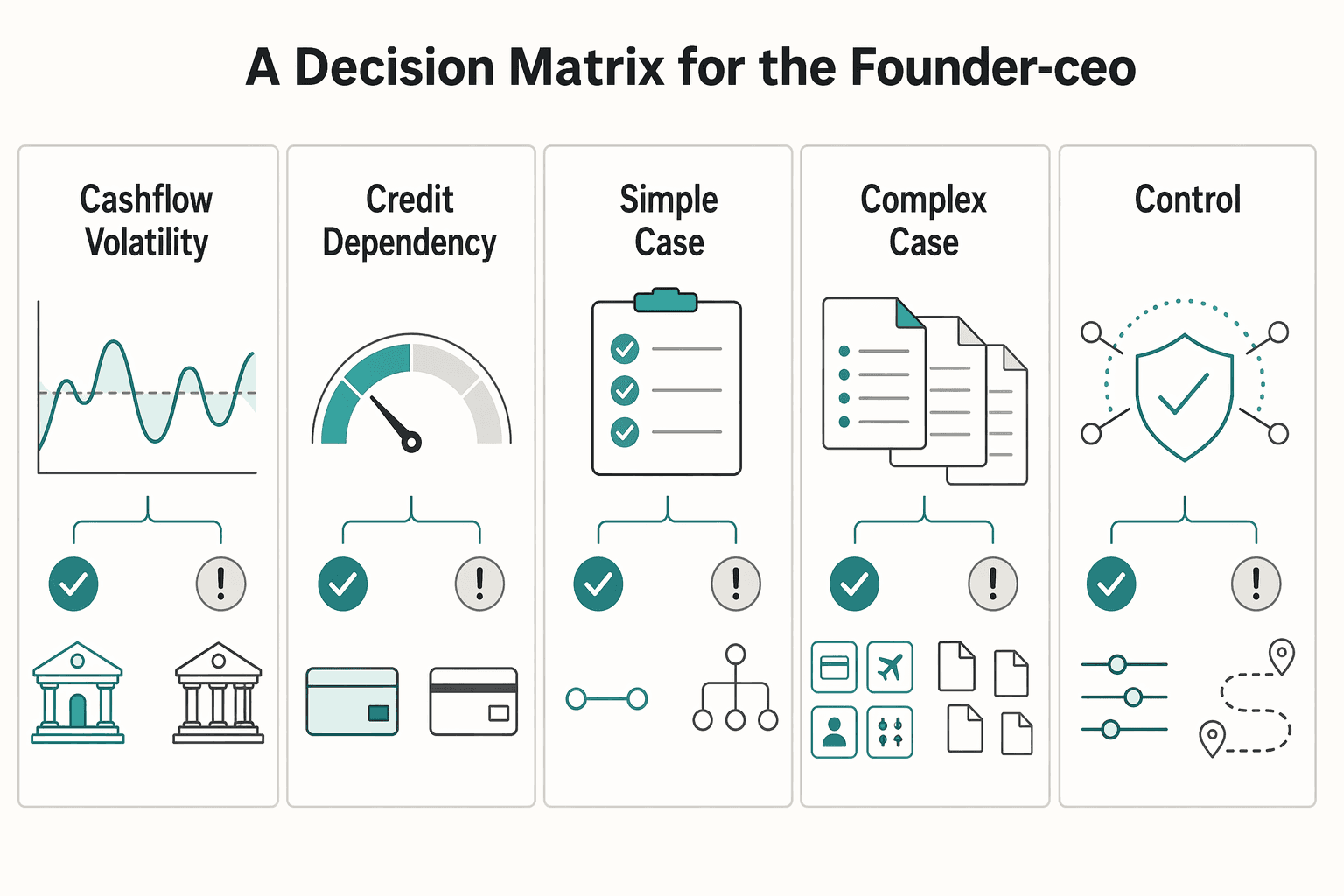

The Verdict: A Decision Matrix for the Founder-CEO#

By this point, the split should be clear. This is a model choice, not a brand choice. Mercury is the cash-control banking model, with spend tied closely to checking cash. Brex is the integrated spend-management model, with cards, reimbursements, bill pay, travel, and controls in one system, plus charge-card balances due in full on schedule.

If your priority is minimizing cash-flow surprises, Mercury can be a practical default. If your priority is reducing operational overhead across a growing team workflow, Brex can be the better fit when you can run tighter process controls.

| Decision criterion | Mercury tends to fit when... | Brex tends to fit when... |

|---|---|---|

| Cashflow volatility | Revenue or collections are uneven, and you want spending constrained by available cash. | Cash timing is stable enough to support integrated spend operations. |

| Credit dependency tolerance | You do not want credit availability influencing spend behavior. | You are comfortable operating with charge-card repayment discipline. |

| Operational complexity | You want a simpler operating model with fewer moving parts. | You need a unified workflow for cards, reimbursements, bill pay, and travel. |

| Compliance readiness | You can satisfy U.S. entity requirements and provide beneficial-owner data (25%+ owners). | You can satisfy U.S. EIN, U.S. incorporation, U.S. operations, U.S. physical address, and address verification requirements. |

| Team workflow needs | Payment controls and separation of duties are the main requirement. | Policy-based approvals across card spend, reimbursements, and bills are central to daily operations. |

The real stress test is repayment and control discipline. Mercury keeps spend closer to cash and supports separation of duties for outgoing payments. Brex can centralize approvals across spend workflows, but repayment cadence, one month or one business day depending on account type, has to match your cash-management process.

Validate deposit protection based on the actual structure, not assumptions. Mercury says sweep networks can make checking and savings funds eligible for up to $5M in FDIC insurance. Brex says Vault can reach up to $6M through partner banks. In both cases, outcomes depend on account setup and conditions.

| Scenario | Default choice | Key caveat |

|---|---|---|

| Early solo founder with lumpy MRR | Mercury | Confirm eligibility and sweep structure before assuming higher FDIC coverage behavior. |

| Lean remote team with reimbursements and frequent approvals | Brex | Works best only with consistent approval policy enforcement and repayment discipline. |

| Post-PMF operator with predictable revenue and higher spend volume | Brex | Validate that finance ops can reconcile checking, treasury or vault positioning, and card-policy workflows cleanly. |

Before you choose, validate four things with current product docs and your actual workflow:

- Eligibility fit: U.S. entity status, EIN, U.S. address requirements, and beneficial-owner or control-person data.

- Cash management process: where operating cash sits, who moves it, and how repayment timing is handled.

- Accounting stack fit: Mercury supports QuickBooks Online, Xero, and NetSuite; Brex supports those and additional ERP/accounting integrations.

- Risk controls: approval rules, separation of duties, and clear ownership for exceptions.

For a step-by-step walkthrough, see How to Use Mercury Treasury for Startup Runway Without Cash Gaps.

Before you lock in a platform, run your real invoice and payout scenarios through the payment fee comparison tool. That will show you where margin leakage is most likely.

Frequently Asked Questions

Can a solo bootstrapped SaaS founder use Brex?

Possibly, but approval is not guaranteed. Brex says it evaluates factors like business model, source of funds, and spending patterns. If your setup is lean, confirm that your U.S. operations and physical-address requirements are clearly satisfied before applying.

Does either option require a personal guarantee?

Usually no for the headline card products, but confirm the exact product agreement. Brex markets its card as no personal guarantee, and Mercury states the same in its IO card context. Terms can vary by feature and account type.

I am a non-U.S. founder with a U.S. LLC. Which one is more realistic?

Mercury may be the more realistic first pass based on published eligibility. Mercury says you do not need to live in the U.S. or be a U.S. citizen if the company is U.S.-formed. Brex also requires U.S. operations and a U.S. physical address, and virtual-address applicants still need verifiable U.S. physical presence.

What documents and checks should I expect during onboarding?

Expect entity documents, EIN-related documentation, identity verification, and risk review. Mercury requires formation documents, EIN-related documentation, and identity verification for owners at 25%+ ownership. Brex says applications are typically reviewed in 1-3 business days after submission.

Are there hidden fees that matter to a bootstrapped business?

Yes, fee exposure can still matter even when base pricing looks simple. Mercury says core banking has no monthly, opening, overdraft, or minimum-balance fees, but some advanced features may cost extra and non-USD international wires carry a 1% conversion fee. Brex says common business-account transfer rails have no transaction fees, but FX markup on international card transactions can be up to 3% and paid plans may apply by tier.

Which one is the better default for a purely bootstrapped SaaS company?

Mercury is often the better default if your first priorities are eligibility, runway protection, and a simple core fee structure. Brex may fit better if broader ERP coverage and API-driven workflow automation matter from day one. The article treats this as a model choice, not a brand choice.

How should I compare their cash-yield options?

Compare them by disclosures, liquidity, minimums, and risk, not just the headline rate. Mercury Treasury has eligibility requirements, a variable yield, and investment risk including potential principal loss. Brex also markets an "up to" yield figure, so current terms and program structure should be verified before deciding.

Which one is better for automation and accounting once the team grows?

It depends on whether you want core accounting coverage or broader workflow integration. Mercury supports direct integrations with QuickBooks Online, Xero, and NetSuite and can suit teams that want more control over custom workflows. Brex publishes broader ERP integration coverage and API workflow tooling, which can fit faster standardization as the team grows.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- fdic.gov/financial-institution-employees-guide-deposi...trusted

- fdic.gov/resources/deposit-insurance/understanding-de...trusted

- irs.gov/faqs/small-business-self-employed-other-busi...trusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

- online.hbs.edu/blog/post/cost-of-capitaltrusted

- sba.gov/blog/5-ways-separate-your-personal-business-...trusted

- sba.gov/business-guide/launch-your-business/choose-b...trusted

- brex.com/support/brex-account-requirementsexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Mercury vs RelayFi for Non-Resident LLC Banking

Pick the setup that keeps money moving under pressure, then worry about nicer features.

A Freelancer's Guide to the US-UK Tax Treaty

Start with your facts and filing setup before you interpret the treaty. For freelancers and consultants with US and UK income exposure, one common risk is assuming the treaty will sort everything out before your residency position, filing obligations, account status, and records are clear.

How to Use Brex for a Venture-Backed Startup with a Remote Team

**Short answer:** If you are evaluating **brex for remote startups**, make this decision early. Use Brex as your operational finance layer, not as your only compliance layer. A resilient setup has two parts: one for spend control and clean accounting, and another for worker classification, tax documentation, and tax-presence review before payment.