Quick Answer

Separate spending, reserve, and income before departure, then define a primary and backup payment path for each client. To manage finances while traveling, use a weekly 20-minute review that checks invoice records against settlement proof and current available balance, and assign ownership to every unresolved item. Keep one incident file with receipts, support messages, and transfer details so you can react quickly when a hold, delay, or deduction appears.

Why Most Travel Money Advice Breaks for Client-Funded Work#

If you are funding travel from live client payments, the real job is continuity, not chasing the lowest visible cost. You need spending access and incoming cashflow that can keep working through separate failures in separate systems.

A lot of travel money advice assumes your cash is already settled and available. That is not your setup. A card can still work while a payout is delayed, or a client can pay while your spending access is interrupted. Those are independent risks, so budget-only advice misses the operational problem.

| Plan type | Primary goal | Key risks | Control cadence | Fallback requirements |

|---|---|---|---|---|

| Vacation money plan | Control trip spending | Overspending, visible fees, poor exchange choices | Pre-trip planning and occasional spend checks | Often one backup card |

| Client-funded travel finance plan | Keep spend access and receivables running at the same time | Delayed settlement, payout review holds, dispute deductions, card interruption, weekend or holiday timing gaps | Weekly checks on expected invoices, settled funds, and spendable balance | More than one money-access rail, plus a separate fallback for incoming payments |

What breaks#

In practice, timing and availability can break before your budget does. Cross-border transfers can take several days, and some foreign banks may require a local account. Fedwire Funds Service processing currently runs on funds-transfer business days, Monday through Friday, excluding Federal Reserve holidays, so weekend and holiday assumptions can fail when you need cash urgently.

Processor risk controls can delay access even after a payment is accepted. First payouts can have a waiting period, flagged charges can be held before release, and some providers can hold early payments for up to 21 days. Disputes can also remove both the payment amount and an added dispute fee.

Why it breaks in client-funded travel#

The cheapest route on paper can be the most expensive route operationally. Intermediary institutions can set exchange rates or add fees, so the amount received can differ from what you expected.

Before you choose any payment route, check availability, not just send status. If a transfer is a remittance transfer over $15, use the disclosure to confirm the exchange rate, fees, taxes, and expected received amount.

What stable looks like before optimization#

Stability means one failure does not freeze both your spending and your collections. Keep at least two ways to access money, and keep a separate fallback for incoming client payments.

Use this rule before you pick a rail. If a lower-cost option can strand you through a weekend or holiday window, a first-payout wait, or a review hold with no second rail, it is not cheaper for your operation.

Keep each invoice, transfer receipt, and processor notice together so you can resolve holds or deduction surprises quickly. Once that foundation is in place, pre-departure prep gets much simpler.

What to Prepare Before You Leave#

The time to prepare for a finance failure is before you leave, not when you are already dealing with one abroad. Your goal is simple: one issue should not freeze both your spending and your incoming payments.

Build an access kit you can trust#

Assume your usual payment habit may fail. Carry at least two means of payment, and do not rely on one method alone. If you usually pay by digital wallet, bring physical credit and ATM cards too, since wallet acceptance and payment technology vary by country.

| Check | What to confirm |

|---|---|

| International debit usage | Enable it if your issuer requires it |

| Issuer fees and limits | Ask about foreign transaction fees, international ATM withdrawal fees, ATM compatibility, and daily card limits |

| Login and security access | Confirm you will have wifi or cellular access for account logins and security checks |

| Backup verification | Set up a backup verification method, since some normal verification methods may not be available abroad |

| Lost or stolen card reporting | Save international numbers for lost or stolen card reporting for every card you carry |

| Foreign currency cash before arrival | Order early; branch pickup can take 2-7 business days |

| Backup card ATM compatibility | Confirm your backup card's compatibility with international ATMs before departure if possible |

Those checks cover most preventable problems. If possible, also confirm your backup card's compatibility with international ATMs before departure.

Map every active client before you fly#

Do not leave your payment setup in your head. Create a one-page pre-departure payment matrix so you can switch quickly if a route is interrupted.

| Client | Primary method | Backup method | Wire enrollment checked (if needed) | Disputes/transfers contact | Escalation contact |

|---|---|---|---|---|---|

| Client A | |||||

| Client B | |||||

| Client C |

Complete this before travel, not during a delay. If wires are in scope, confirm whether your bank requires wire-transfer enrollment before travel.

Build an incident folder, not just a document folder#

A normal document folder is not enough when something breaks. Keep secure copies of the records you may need to recover access and resolve payment issues, even if your primary device or connection fails.

| Keep in folder | Use |

|---|---|

| Copies of key documents | Verification or card replacement |

| Important international phone numbers | Lost or stolen card reporting |

| Provider support contacts | Disputes/transfers path |

| Backup payment details | Cards and cash access |

Include copies of key documents used for verification or card replacement, important international phone numbers for lost or stolen cards, provider support contacts including your disputes/transfers path, and backup payment details for your cards and cash access.

Before departure, define your trigger actions:

- If a card is interrupted: report it through the saved international number, then switch to backup card and cash access.

- If verification fails abroad: use your backup verification method.

- If a transfer issue appears: open your disputes/transfers path and contact support promptly.

Build a Three-Layer Money Setup for Travel#

On the road, a resilient setup has three layers: spending, reserve, and income. Give each layer one job so one failure does not freeze everything at once.

Use one rule across all three: each layer should fail alone. If your card is declined, client receipts should still land. If a payout is delayed or under review, your day-to-day spending should still clear. If you need emergency funds, you should not have to expose the account that receives invoices.

Give each layer one clear job#

Your spending layer is for everyday card and ATM use only. Keep routine travel money here, not your full cash position. Your reserve layer is your continuity buffer, separate from daily swipes and withdrawals. If you hold large balances at one insured U.S. bank, remember FDIC coverage is $250,000 per depositor, per insured bank, per ownership category. Your income layer is for receiving client payments only. Keep routine merchant spend out of it so a hold or review affects collections, not daily access.

Before travel, tell your bank or card issuer that you will be abroad so account access is less likely to be interrupted.

Before anything goes wrong, map each layer with this short framework:

- Owner: who legally holds the account and matches invoice and card records

- Primary instrument: the main card, account, or rail

- Fallback instrument: the tested backup card, second account, or alternate rail

- Allowed transfer direction: where funds may move next, and where they may not

Define switch triggers in advance#

Do not wait to decide when to switch. Set the trigger before you need it.

| Layer | Primary route | Fallback route | Typical failure mode | Immediate switch trigger |

|---|---|---|---|---|

| Spending | Primary card or debit for purchases and ATM | Backup physical card plus cash route | Lost or stolen card, fraud flag, unexplained decline | Confirmed loss or theft, or one unexplained decline on an essential purchase |

| Reserve | Separate reserve account | Secondary reserve access path, including a bank-partner withdrawal route | Access issue or transfer hold | Scheduled top-up cannot complete in your planned window |

| Income | Primary client payment rail | Preapproved secondary rail | Payment hold or provider review | Funds not settled by the promised date, or payout marked under review |

Do not treat fallback rails as interchangeable. ACH runs in batches, while Fedwire is real-time, final, and irrevocable once processed. If you switch a client from ACH to wire, recheck beneficiary and payee details before sending.

Move money by rule, not by mood#

A lot of avoidable mess comes from moving money casually between accounts. Use rules so the layers stay clean:

- Move income to reserve only after settlement is confirmed and reconciliation is recorded against invoice and net received.

- Move reserve to spending only on schedule or after a defined incident trigger.

- Keep routine spend, ATM withdrawals, and merchant charges out of the income layer.

If your spending layer relies on a debit or ATM card, report loss or theft immediately. Reporting timing can change your unauthorized-transfer exposure, including the 2-business-day, $50, $500, and 60-day thresholds, so speed matters.

If you need help choosing your account mix, start with The Best Multi-Currency Accounts for Digital Nomads and Freelancers. Final checkpoint: if client receipts and travel spend still share one balance, separate them before the next billing cycle.

Choose the Right Client Payment Rail for Each Job#

Choose client payment rails in this order: reliability first, total cost second, speed third. A rail is the infrastructure that moves money between payer and payee. The point is not to pick the fastest-looking option. It is to pick the one most likely to settle cleanly for that client and job.

Start with what the client can use consistently and what your receiving setup can support. Then compare expected cost and processing behavior. Only after that should speed break a tie.

Compare rails by evidence, not preference#

Preference is a weak basis for a time-sensitive invoice. Use what the client can actually send and what you can actually receive.

Local rails such as ACH and SEPA are often faster and lower cost when both sides can transact locally. SWIFT is a common global rail for cross-border payments. Cards and wallets can work, but they should be used intentionally.

| Rail option | Reliability signals | Cost components | Failure pattern | Best-fit use case |

|---|---|---|---|---|

| Local transfer (ACH/SEPA) | Both sides can use local bank accounts and details are verified | Local systems are often lower-fee and faster to process, but provider costs vary | Delays can occur during verification or processing if details are wrong | In-country payments where both sides can transact locally |

| SWIFT wire | SWIFT availability for both sides is confirmed | Fees and processing behavior vary by bank and provider | Delays can occur during verification or processing | Cross-border payments using a global rail |

| Card payment | Client can pay by card and your payout path is active | Fees and processing behavior vary by provider | Payments can pause during verification or processing checks | Workflows where both sides already use card payments |

| Digital wallet | Client and payee both use the same wallet flow | Fees and processing behavior vary by platform | Transfers can pause during verification or processing checks | Workflows already operating in that wallet |

If fee ownership, expected settlement behavior, or the fallback path is unclear, do not use that rail for a time-sensitive invoice.

Name a fallback trigger for every client#

A primary-plus-fallback setup works better when the switch point is explicit. For each client, document one primary rail, one fallback rail, and one trigger event that forces the switch. Use a clear trigger tied to transaction progress, such as a payment that does not move through verification or processing as expected.

Keep that trigger with the client record so you can execute the switch immediately instead of debating it during a delay.

Put the rail policy in your invoice terms#

A short rail policy in your invoice terms prevents avoidable confusion later. Keep it tight and specific:

| Policy item | What to state |

|---|---|

| Accepted methods | Primary rail plus approved fallback |

| Fee responsibility | Who covers payment-related deductions |

| FX handling | Invoice currency and where conversion occurs |

| Short-pay or return workflow | What happens if funds arrive net, are returned, or are held |

State the accepted methods, who covers payment-related deductions, the invoice currency and where conversion occurs, and what happens if funds arrive net, are returned, or are held.

This can reduce disputes before they become cashflow problems.

Use a go/no-go gate before release#

Before you send payment instructions, stop and confirm four things:

- Beneficiary data matches the selected rail.

- Verification and processing expectations are understood by both sides.

- Fee ownership is confirmed in writing.

- One escalation owner is named on each side.

If any item is unclear, treat it as no-go until fixed.

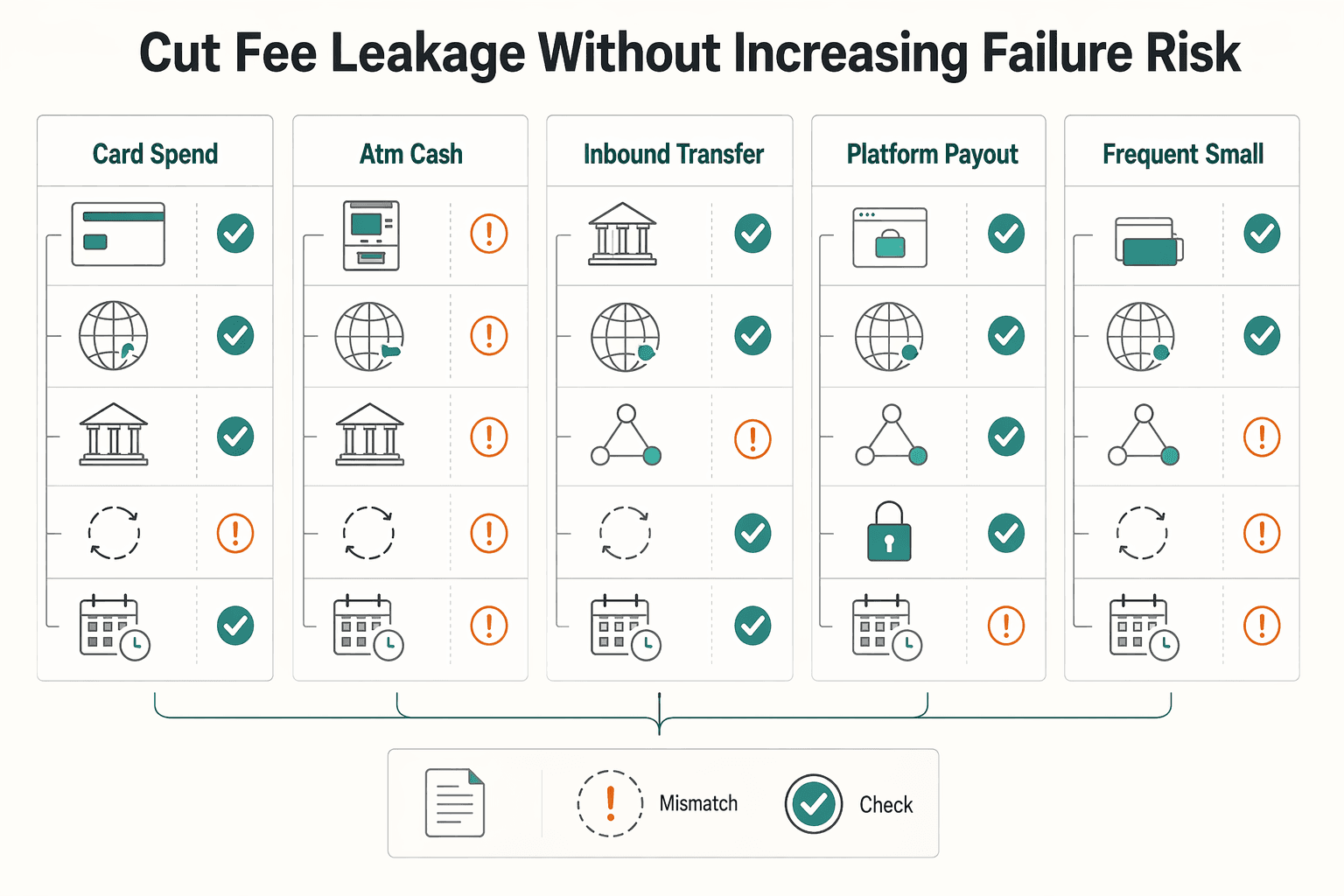

Cut Fee Leakage Without Increasing Failure Risk#

Cut costs only when continuity stays intact. A lower visible fee is a bad trade if it increases retries, holds, short-pay risk, or payout delays.

Map each payment path end to end before you optimize it: where money starts, who handles conversion, where deductions can happen, and what your fallback is if the first route fails. Then set an acceptable total cost for that path. Include visible fees, conversion spread, intermediary deductions, retry effort, and delay impact. Use that as your decision line.

| Path | Fee types to capture | Common failure mode | Control check before use | Use or avoid |

|---|---|---|---|---|

| Card spend | Issuer fees, merchant or terminal conversion spread | Merchant-side conversion changes the rate basis | Confirm who converts currency at checkout; if the merchant or ATM converts, Mastercard rates do not apply | Use for routine spend; avoid when conversion terms are unclear |

| ATM cash | ATM operator fee, network fee, conversion spread | Frequent small withdrawals compound fees | Review the fee notice before you commit; proceed only after you confirm the terms | Use for planned cash pulls; avoid repeated small withdrawals |

| Inbound transfer | Sending fee, receiving fee, intermediary deductions, FX conversion | Beneficiary detail errors, reviews or delays, unexplained net shortfall | Reverify recipient account or institution details and confirm fee ownership in terms before invoicing | Use for larger client payments; avoid when details or fee handling are unresolved |

| Platform payout | Withdrawal fee, payout FX, receiving-bank fees | Holds or payout delays | Confirm the withdrawal route is active and keep a fallback; Stripe says initial payouts are typically 7-14 days, and PayPal holds can make funds temporarily unusable | Use when funds originate on-platform; avoid using as your only spend-access path |

Two controls matter most here: know who owns the fees, and keep a fallback payment route active. That helps reduce delay and access risk when one route is held or unavailable.

Use leakage signals as immediate action triggers:

| Signal | Owner | Immediate action | Evidence to log |

|---|---|---|---|

| Frequent small ATM withdrawals | You | Consolidate withdrawal cadence | ATM location, fee screen, receipt |

| Merchant or ATM conversion prompt | You | Pause and select network or card conversion path if available | Prompt photo or screenshot and final receipt |

| Unexplained inbound deduction | You + sender contact | Request transfer trace details and provider breakdown | Remittance advice, expected vs settled amount, provider messages |

If a transfer qualifies as a remittance transfer, treat timing windows as operational deadlines. Cancellation requests are time-sensitive, up to 30 minutes after payment, and error reports can run up to 180 days after the disclosed availability date.

This pairs well with our guide on Automating Freelance Finances Without Losing Cashflow Control.

Before you change rails, run your real invoice sizes through this payment fee comparison so you can weigh visible fees against FX and settlement timing.

Run a Weekly Finance Check That Takes 20 Minutes#

A short weekly check keeps minor issues from turning into cash-access problems. Use it as a two-step control: first check invoice transactions for accuracy, then manually work anything that did not match.

Reconcile from invoice to confirmed balance#

Start with the chain that matters most: invoice recorded, transaction posted, settlement confirmed, and balance updated.

Review every open and recently paid invoice. Match each one in order: invoice status, payment record, settlement status from your provider or bank, and whether the amount is visible in your available balance.

Do not stop at a "paid" status alone. If settlement records, bank credits, or platform balances do not confirm it, flag it as an action item. Close each invoice in only one state: settled, pending with evidence, or follow-up required.

Triage exceptions like real operations work#

The weekly review only works if mismatches get owned. Move every mismatch into exception review, classify what is unresolved, then assign an owner, define the next action, and set the next checkpoint date.

If a tracker item has no owner or no next review date, treat that as a risk. For unresolved items, attach evidence now: invoice, remittance details, transaction ID, provider messages, and the balance snapshot showing the gap.

Compare planned and actual in one control table#

Use one compact table to see whether each reconciliation step performed the way you expected.

| Reconciliation step | Planned outcome | Actual outcome to review | Decision note |

|---|---|---|---|

| Accuracy check | Invoice transactions match expected details | Mismatch or unresolved transaction | Move item to manual follow-up |

| Manual follow-up | Each unresolved item has an owner and next action | No owner, no date, or missing evidence | Assign ownership and set checkpoint |

| Close readiness | Items are either settled or documented as pending | Open items without documentation | Hold close until records are complete |

Log one change for next week#

End each review with one concrete process change for next week, not a vague reminder.

Then run a monthly evidence-pack check so your records are ready when you need them. In formal reconciliation workflows, monthly invoice accuracy review comes before manual cleanup of unresolved items. Use that same rhythm here to keep invoices, settlement proof, receipts, statements, and provider messages audit-ready.

Recover Fast When Something Breaks Abroad#

When a payment incident goes live, sequence matters. Restore spending access, protect receivables, build one incident file, and only then restart normal activity.

Restore access first#

Your first job is to keep daily spending working. Switch to a backup spend method immediately, then confirm at least one payment path works end to end. If login works but spending still fails, treat the incident as active and move to essentials-only spending until a full payment flow succeeds.

Use a hard checkpoint here: one small approval is not enough if your normal path is still unstable. Keep optional transfers, subscriptions, and large discretionary spend paused until the backup method is reliable and at least one primary path is usable again.

Protect incoming cashflow next#

Once spending is stable enough, protect collections. Separate receivables into delayed invoices and upcoming invoices, then update payment instructions in writing when routing changes. Log each update so delivery status and payment status stay aligned.

Do not mix delayed-payment follow-up with new billing instructions in the same thread. Make any payment-route change explicit and easy to verify before the next invoice is sent.

Build one incident file#

Scattered records slow everything down. Keep one incident file for the full event, with timeline notes, case IDs, failed-attempt evidence, communication history, and any ownership/control disclosures you may need for review. Assign one owner for escalation and use one directed contact path so follow-up stays consistent.

If contact or payment details change, send written notice and store that notice in the same file. Formal reviews usually move on documented records, not memory.

Contain risk before you restart#

Do not restart normal volume just because one piece starts working again. Pause noncritical money movement until you know what failed. Preserve proof of delivery, approval trail, invoice copies, and payout references before you make follow-on payment decisions. Expect review and enforcement workflows to involve friction, so keep sequence and ownership evidence clear.

Set restart conditions before normal volume resumes: a working spend path, a current next-action date for delayed receivables, and an incident file complete enough to escalate without rebuilding it.

Keep Tax and Audit Records Clean While You Move#

A practical standard is simple: each settled payment should be traceable as it lands. If you cannot show how a gross invoice became a net receipt with supporting records, audit and tax follow-up can slow down quickly.

Use one standard record bundle per payment#

Do not build records from scratch at month-end. For each payment, store one bundle by client and period:

- invoice

- payout confirmation

- fee detail

- exception note if anything is off

Use it as your working evidence set. It is not a regulator-prescribed format, but it supports the recordkeeping and substantiation burden for income, deductions, and statements you may need to defend later.

When funds settle, run one quick check: invoice amount, payout confirmation, and fee line should reconcile to net received. If they do not, log the exception the same day with date, owner, known cause, and next action.

Keep a live tax artifact tracker with named ownership#

A tax tracker works best as an open-items register, not a year-end worksheet. Assign one owner, add reviewer or support fields, and track U.S.-specific items such as W-8 BEN/W-8 BEN-E, W-9, 1099-NEC, and FBAR only where they apply to your situation.

| Artifact | Who usually owns the action | Status fields to track | Red flag before close |

|---|---|---|---|

W-9 | You provide it to a payer that needs your correct taxpayer identification number for information returns | requested date, sent date, legal name checked, TIN checked, accepted yes/no | Payment is in motion and the client still does not have your form |

W-8 BEN or W-8 BEN-E | You provide it when requested by a U.S. withholding agent or payer to document foreign status, individual vs entity version | form variant, requested date, sent date, accepted yes/no, recheck needed yes/no | Wrong variant sent or no current form on file |

1099-NEC | Payer usually handles filing when required; you track whether you expect one and from whom | expected yes/no, payer name, tax year, recipient copy received, mismatch noted, follow-up owner | Year-end arrives and expected forms are unclear |

FBAR FinCEN Form 114 | You or your preparer if U.S. foreign-account reporting applies | possible obligation yes/no, account list complete, max-balance data ready, current threshold verified, current due date verified | Foreign account data is scattered with no peak-balance review |

For year-specific or jurisdiction-specific checks, leave the exact threshold or due date unresolved until it has been verified from official sources, payer records, or adviser records.

Write VAT assumptions before you issue the invoice#

If you do cross-region work, document VAT assumptions before invoicing. Capture the place-of-taxation logic because that determines which country's rules apply, and note that obligations can differ by country and by goods versus services.

For each client, record:

- client jurisdiction

- goods or services classification

- invoicing assumption

- status: confirmed or uncertain

If uncertain, mark it clearly and route it to advisor review before issuing the invoice.

At month-end, assemble one evidence pack from records you already keep:

- bank and payment-platform exports for the period

- exception log for holds, disputes, returns, and manual adjustments

- record bundles for high-value or unusual settlements

- current tax artifact tracker with missing items highlighted

- VAT assumption notes for cross-border invoices issued that month

This keeps audit, hold, and dispute responses fast, without forcing you to rebuild the story from scattered threads.

Your Copy-Paste Weekly Checklist#

Use this as your weekly closeout: prove what happened, then use the data to improve next week's decisions.

- Reconcile the next cycle of cashflow in one block.

Open invoices, payout confirmations, bank activity, and card activity together. Mark each expected item as scheduled, sent, settled, late, or needs confirmation, assign an owner for every unresolved item, and set the next follow-up point: date, channel, confirmation needed. If a client says payment was sent but you do not have settlement proof, keep it open as pending proof.

- Decide whether planned travel is necessary, then confirm spending access is ready.

Start by evaluating whether each planned trip is still needed. If travel is still necessary, confirm your primary method works, then verify your backup is usable now (for example: physical access, valid expiry, known PIN, and travel-use setting where relevant). End with a binary decision: ready this week or not ready. If not ready, fix it before your next billing or travel day.

- Review cost leakage using total cost, then pick one routing change.

Check total cost signals together: visible fees, FX impact, ATM charges, transfer deductions, retries, and delay cost. Controls can help support legitimate reimbursements, but they do not replace active cost management, and skipping routine data review can mean missed savings opportunities. Finish with one explicit decision for next cycle: change method, keep method, or shift by client. If you need deeper transfer-loss analysis, read Decoding International Wire Transfers: Why You're Losing Money.

- Clear your unresolved queue while evidence is fresh.

List open holds, disputes, verification requests, payout mismatches, receipt gaps, and unusual declines. For each, keep only: issue, owner, next action, deadline. Save proof in the same week folder, including screenshots, emails, payout confirmations, receipts, and the incident note, so you can show the full sequence without rebuilding it later.

- Update tax and audit records with verified source checks, not guessed thresholds.

Refresh your current record set and trackers, then leave any changing legal threshold, filing deadline, or local reporting trigger unresolved until it has been verified from official sources or adviser records. Keep each transaction traceable from gross invoice to net received with supporting records attached.

- Write one automatic improvement rule for next week.

Use an if-then trigger, not a vague reminder. Example: If the same payout route causes one more delay or unexplained deduction next week, then switch that client to the pre-agreed fallback route before sending the next invoice. If a change depends on country-specific requirements, confirm first through the existing contact path: Talk to Gruv.

This sequence is the control: reconcile first, evaluate travel need and access second, review cost signals third, clear unresolved items fourth, update records fifth, and lock one improvement rule last.

You might also find this useful: How to Manage Your Finances Across Multiple Currencies.

If you want one workflow for invoicing, payout status visibility, and cleaner records while you travel, explore Merchant of Record for freelancers.

Frequently Asked Questions

What is the minimum setup you should leave with so one failure does not freeze you?

Leave with at least two means of payment on different rails, plus some foreign currency cash, so one failure does not block all access. Before departure, turn on international usage for your debit card, carry physical cards even if you usually use a digital wallet, and save international lost-card phone numbers in an accessible place. Carry travel documents on you, not in checked luggage, and make sure ticket and ID or passport names match to reduce avoidable identity checks.

How many payment rails should you keep active, and which one should do what?

Keep a primary collection rail and a tested fallback, and keep spending access separate so a payout issue does not also stop day-to-day spending. In practice, keep a mix of credit, debit, and ATM card access, and use wire capability only when enrollment and verification are already handled. Foreign currency cash should remain part of the setup as a backup.

How do you reduce ATM and FX costs without increasing failure risk?

Reliability comes first. Once your setup is solid, choose local currency at foreign ATMs and monitor ATM and foreign transaction fees, since they can add up quickly. In a closed-currency country, plan to spend or exchange remaining cash before departure.

What should you do first if a client payout is delayed or your card stops working abroad?

Handle it in order: stabilize spending first, then address the blocked rail. Move essentials to your backup method and report the issue through your saved international support path. Then confirm whether verification is the blocker, since some verification methods may be unavailable while abroad, and switch to a contact or device path that can complete checks.

How do you track travel spending and client income without making month-end painful?

Keep a running log of expected invoices, settled payouts, card and ATM activity, fees, and open exceptions so mismatches do not pile up. Store payout confirmations and incident notes together so follow-up is faster. If you want ownership proof for newer electronics on re-entry, decide before departure whether CBP Form 4457 is relevant, since CBP notes it is only suggested when goods are less than six months old.

Watch

CCNV v. Reid Explained

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- cbp.gov/travel/us-citizens/know-before-you-go/know-y...trusted

- commerce.gov/ofm/offices/office-financial-reporting-polic...trusted

- consumer.ftc.gov/lost-or-stolen-credit-atm-debit-cardstrusted

- files.consumerfinance.gov/f/documents/cfpb_adult-fin-ed_remittance-tra...trusted

- irs.gov/businesses/small-businesses-self-employed/bu...trusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

- travel.state.gov/en/international-travel/help-abroad/financia...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Best Multi-Currency Accounts for Digital Nomads and Freelancers

This shortlist is for cash flow decisions, not brand popularity. It is for freelancers, creators, and lean teams in the United States who need a cross-border payment setup that still works when real work hits: invoices go out, money lands, conversions happen on your timing, and urgent payouts do not depend on luck.

Why International Wire Transfers Arrive Short and How to Reduce Fee Leakage

Most money lost on cross-border payments does not disappear in one obvious charge. It leaks out in small deductions at different points along the route. The client may pay an outgoing fee at their bank. One or more correspondent banks may take a cut as the payment moves across SWIFT. Your own bank may charge to receive it. If a currency conversion happens anywhere along the way, that can add more drag. By the time the funds land, the amount credited can be lower than the amount invoiced even when the client is sure they paid in full.

The Best Travel Insurance for Digital Nomads in 2026

The **best travel insurance for digital nomads** in 2026 is not the plan that tops a roundup. It is the one that clears your paperwork and still works when your route changes. For long stays, keep the order simple: paperwork first, continuity second, price third. Eligibility is part of that first check, because a cheap plan you cannot actually use is not a bargain.