Quick Answer

Start by assuming malta tax residency is a facts-and-records decision, not a day-count shortcut. The article treats 183 days as a strong indicator, then requires supporting evidence on intention, ties, and income movement before you file. It recommends a traffic-light triage, a monthly evidence pack, and a quarterly review so gaps are fixed early. If your facts could support residence in more than one country, pause and escalate before deadlines rather than forcing a weak filing position.

Start With Your Residency Facts#

If you want a defensible Malta tax position with less stress, treat the 183-day rule as a strong signal, not a complete answer. Spending more than six months in a calendar year is often presented as likely resident, but the final position is still facts based.

That is the central tension: start with day count, then test whether your lived facts support the same outcome. If they do not line up, treat your status as unclear instead of forcing a filing position.

Use one rule from day one. If you cannot explain your status in one short paragraph using both day count and facts, pause and escalate. One failure mode is filing as if one threshold settles everything, then discovering another country can still make a plausible residence claim.

Use this guide in sequence. First, define terms and lock your labeling. Next, run the traffic-light triage before each filing decision. Then maintain the evidence pack and escalation log so your year-end position is mostly administrative, not a reconstruction exercise.

By the end of this guide, you will have:

- A decision path that starts with physical presence and then checks whether surrounding facts support the same conclusion.

- An evidence checklist you can maintain through the year.

- Clear escalation triggers for dual residence or unclear status.

Define the terms that control your tax outcome#

Mixed labels can lead to expensive filing mistakes. Lock the terms first, then keep testing your facts against those terms through the year.

Residence status and domicile are not interchangeable. Domicile is usually acquired at birth, while tax residence is assessed separately in practice. Use the labels below consistently in your records and advisor conversations.

| Label | What it means in practice | Why it changes tax outcome |

|---|---|---|

| Resident and domiciled | You are treated as both resident and domiciled in Malta. | This position is described as being taxed on worldwide income and assets. |

| Resident non-domiciled (res-non-dom) | You are tax resident in Malta but not domiciled there. | This is described as remittance-basis treatment, with income tax on earnings originating in or remitted to Malta; Maltese-source income is described as taxed at progressive rates from 0 to 35%. |

Use professional advice for legal interpretation, and avoid relying on memory for article-level interpretation.

In practice, keep one live note where you state your current label and the facts supporting it. Update that note whenever travel pattern, housing, or income movement changes. This can reduce drift between what you believe, what your accountant prepares, and what your records can prove.

Run one verification check each quarter to prevent classification drift:

- Confirm your chosen status label still matches your lived facts.

- Reconcile each income stream to that label, especially anything remitted into Malta.

- Flag anything that could support a different residence claim in another country.

A practical risk is choosing res-non-dom early, then treating every foreign inflow as automatically covered. If your records do not clearly show where income arose and what was remitted to Malta, your position becomes harder to support. If your facts no longer match the label you are using, pause and get advice before filing. For a broader planning overview, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

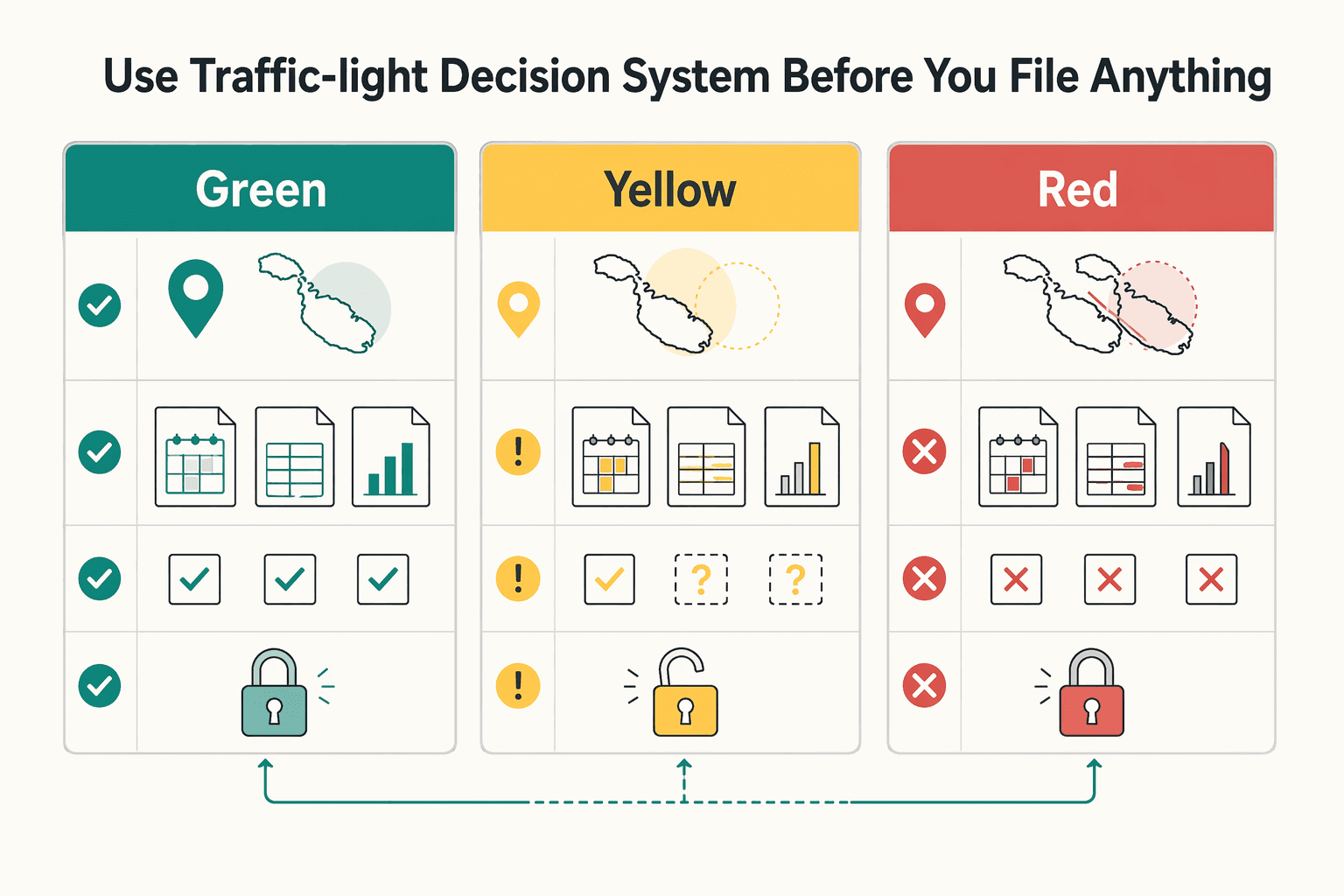

Use a traffic-light decision system before you file anything#

Before filing, map your facts to one clear route and make sure your records tell the same story.

| Status | When it applies | What to do |

|---|---|---|

| Green | Facts align clearly with one residence route and remain consistent across records. The two cited routes are spending 183 days or more in Malta over a 12-month period, or moving to Malta with the intention of residing there indefinitely and basing yourself there. | Map your facts to one clear route and make sure your records tell the same story. |

| Yellow | Facts are mixed or changing. | Treat this as a documentation-heavy review phase, not a filing green light. |

| Red | More than one country could plausibly claim residence or your treaty position is unclear. | Stop and escalate before filing. Prepare treaty materials for review, including the Income Tax Treaty PDF (2008) and Technical Explanation PDF (2008). |

Yellow status can happen while your facts are still being reconciled. The mistake is treating yellow as close enough to green. Use yellow to tighten evidence, resolve contradictions, and close open questions before you move forward.

Before you file, run one short checkpoint:

- Write a one-paragraph residency memo with your route and supporting facts.

- Record your exact day count for the relevant 12-month period.

- List the facts that support being based in Malta.

- Flag any other country that could also claim residence.

Decision rule: if you cannot explain your position in one paragraph tied to your residency route and treaty documents, pause and get professional review before submission. Want a quick next step for 'malta tax residency'? Try the tax residency day counter.

Apply day count correctly without treating it as the whole test#

Day count helps, but it does not carry the full argument on its own. The 183-day point supports a specific programme condition, not a complete GRP eligibility conclusion.

The concrete support here is narrow. Under Malta's Global Residence Programme (GRP), one listed condition is that you do not spend more than 183 days in any other single jurisdiction. The same GRP material says the programme was enacted in 2013. It also describes a 15% flat tax rate subject to conditions and includes eligibility rules such as nationality and property or rent thresholds.

The practical takeaway is simple. A clean day log alone does not prove GRP eligibility. Non-day conditions still need to match your file.

Treat the day log as evidence, not just a number. Keep dates in a format you can reconcile against tickets, calendar entries, and account activity. If two records conflict, resolve the conflict immediately and keep a short note explaining the correction.

Before year-end, run a short verification check:

- Reconcile travel records and confirm day totals by jurisdiction.

- Confirm supporting documents still meet non-day GRP conditions, including nationality and qualifying property or lease requirements.

- If you relied on MPRP FAQ wording, verify against governing legislation, since the MPRP FAQ states legislation prevails in conflicts.

If your day count is close to the 183-day limit in another jurisdiction, or records do not line up, pause and tighten documentation before filing.

Separate tax residency from special status programs#

Make two decisions in order. Confirm baseline residency first, then assess any special status programme.

One Malta tax guide presents this as two connected tracks: personal tax positioning and a separate structuring layer. Keep those tracks separate so you do not build your position around a programme label before your core residency case is defensible.

Use the Malta Global Residence Programme (GRP) as the example. One programme summary describes it as aimed at non-EU, non-EEA, and non-Swiss applicants. The same source says it is anchored in Malta's Income Tax Act and Legal Notice 267 of 2014. It also describes treatment features such as a 15% rate on foreign-sourced income remitted to Malta and no Malta tax on foreign income not remitted. Those are treatment features, not proof of baseline residency.

Apply the same logic to Expat Tax Incentive and similar schemes. They may change outcomes for eligible profiles, but they do not replace residency analysis.

A sequencing error is collecting programme paperwork first and writing the residency memo later. Reverse that order. If your baseline position is weak, programme details will not fix the underlying problem and can create false confidence.

Use this sequence before relying on any programme:

- Document your baseline residency position first, including day count and, where relevant, intention to reside ordinarily.

- Assess programme fit separately against conditions you can evidence.

- Reconcile remittance records to the treatment you plan to claim.

- Treat unresolved eligibility gaps as filing blockers.

Programme summaries are not the final legal word. If eligibility is unclear, confirm current terms with the Commissioner for Revenue (CFR) or a licensed advisor before filing.

Map your income under source and remittance logic#

Map every inflow by origin and movement before deciding treatment. This keeps your filing position explainable and reduces avoidable risk.

Use three buckets from day one and keep them separate:

| Income bucket | What to classify first | What to track when money moves |

|---|---|---|

| Domestic-source income | Why you classified it as domestic-source, payer, contract or invoice reference | Receiving account and date credited |

| Foreign-source income | Where it arose, income type, first account credited | Each transfer, transfer reference, receiving account |

| Asset-sale and other proceeds | Asset or transaction record, acquisition and disposal records, proceeds amount | Whether proceeds stayed in the original account or were later transferred |

If you are building a source-based filing position, document each income stream and each transfer clearly enough that another reviewer can follow the trail line by line. Keep invoices, statements, and transfer confirmations together, then run a short monthly check to confirm sampled transfers still tie to a bucket and source document.

Do not mix personal and business flows in the same unlabeled transfer path. When entries are mixed, the classification story gets harder to defend. Pause new mixed transfers, mark unclear past items as provisional, and resolve them before filing.

A useful monthly routine is simple. Reconcile recent inflows, verify transfer references, and move unresolved items to a visible pending list. That keeps uncertainty contained instead of letting small gaps spread through the full-year file.

Keep corporate updates in a separate lane from personal filing logic. Some Malta corporate materials discuss Legal Notice 188 of 2025 and a dual-track system. They also mention corporate figures like thirty-five percent and a fifteen percent levy option. Those are corporate-context points, not personal-rule shortcuts.

Manage dual residence risk before it becomes a filing problem#

A clean income map is necessary, but it does not remove dual residence risk. You can meet a day-count threshold (for example, 183 days) and still be treated as resident elsewhere in the same tax year because each country applies its own domestic tests.

Dual residence usually appears when your facts meet more than one domestic test at once. Common triggers include days present, home ownership or availability, and ongoing economic ties across countries. Treat day-count analysis as one input, not a full conclusion.

Tax treaties become critical at this point. If a bilateral treaty applies, tie-breaker rules may resolve the conflict for treaty purposes. If no treaty applies, resolution depends on national tax law in each country, which can increase the risk of worldwide income being taxed in both jurisdictions and add reporting complexity.

The practical risk is timing. If you wait until filing deadlines, you may need to choose a position before your evidence file is complete. Early escalation gives you room to test assumptions, request missing records, and align your position across countries.

When two countries can plausibly claim residence, freeze assumptions and escalate before filing deadlines. Prepare a treaty brief with:

- Full-year physical-presence timeline by country.

- Home-availability summary and dates each home was usable.

- Economic-ties record, including where core contracts and clients sit.

- Prior returns or residency positions already taken.

- Unresolved questions that need treaty analysis.

Run one checkpoint before filing season: can an independent reviewer follow your facts without missing records? If not, pause and close gaps first. Early advisor review can reduce the chance of correcting an inconsistent position later.

Build your Malta evidence pack throughout the year#

Build this monthly, not at year-end. Your residency position is only as strong as the documents behind each claim.

| Evidence area | What to keep |

|---|---|

| Home records | Signed lease or purchase documents, plus renewal or payment proof. |

| Utility and address records | Bills or account records tied to your Malta address. |

| Local activity records | Card statements or receipts showing day-to-day activity. |

| Travel timeline | Entry and exit dates with supporting tickets or calendar records. |

| Filing context | Prior returns, residency position notes, and copies already shared with advisors. |

Treat this as a working file, not an official checklist. The goal is a consistent record across place of abode, travel pattern, and local footprint.

- Home records: signed lease or purchase documents, plus renewal or payment proof.

- Utility and address records: bills or account records tied to your Malta address.

- Local activity records: card statements or receipts showing day-to-day activity.

- Travel timeline: entry and exit dates with supporting tickets or calendar records.

- Filing context: prior returns, residency position notes, and copies already shared with advisors.

If you may request a Malta Tax Residency Certificate, keep a separate authority-facing packet aligned to your main file. A useful standard from programme guidance is that declarations should be supported by documentary evidence. Treat FAQ text as process guidance only. If FAQ wording conflicts with legislation, legislation prevails.

Document quality matters as much as document type. Prefer readable files, consistent names, and clear links between claim and evidence. If a record is incomplete, mark it as provisional instead of letting it sit as silent evidence.

Use a simple monthly folder structure (YYYY-MM) with subfolders for home, utilities, spending, travel, and correspondence. Run one monthly checkpoint: confirm records are complete, readable, and consistent with your claimed residency narrative.

Use timing thresholds as tracking markers, not automatic conclusions. Some programme materials reference three months plus a Maltese address for certain EU, EEA, and Swiss residency applications, and other programme context references 183 days in specific cases. Track those milestones, but do not treat any single programme rule as a universal test for all tax residency cases.

Related: How to Handle the 'Saving Clause' in US Tax Treaties.

Run a quarterly compliance cadence for low-stress execution#

Run a quarterly review, not just a monthly file check, so your compliance position stays coherent before filing pressure builds. This is where you catch drift in activity, records, and cross-border reporting signals early.

Tax administrations report a major shift in the operating environment since 2010, including more available data, broader automatic exchange of information, and more early compliance-risk treatment. When records diverge across quarters, the risk can be harder to contain later.

| Quarter point | Focus question | Evidence to check | Escalate when |

|---|---|---|---|

| Quarter-start | Does your planned activity still match your current compliance position? | Updated activity calendar, account records, planned cross-border transactions | Your projected pattern no longer supports your current compliance narrative |

| Mid-quarter | Do your records still align across systems and accounts? | Income map, transfer notes, cross-border account reconciliation | A transfer cannot be clearly explained by origin, amount, date, and purpose |

| Quarter-end | Are any cross-border compliance questions still open, and do you need specialist review before filing? | Country-by-country activity summary, ties and control notes, prior position notes | Key items remain unresolved close to filing |

Each quarterly review should end with a short action list. Close what is clear, assign ownership for unresolved points, and set a follow-up point before filing pressure returns. The value of the cadence is not the meeting itself. The value is reducing uncertainty while correction is still easy.

Keep an escalation log and close issues before filing windows:

- Issue: one-sentence conflict statement.

- Why it matters: which filing position could change.

- Owner: you, advisor, or both.

- Due date: set before filing windows.

- Status: open, waiting on records, or cleared.

At each quarter close, run one verification pass on material claims in your file and mark unresolved items for correction before the next quarter starts.

Know when to escalate and exactly what to ask#

Escalate early when your file could support more than one outcome. If ties conflict, domicile is unclear, or your position depends too heavily on a permit or programme label, get advisor review before filing pressure builds.

Escalation triggers that should not wait#

- Conflicting cross-border ties where more than one country could plausibly claim residence.

- Unclear domicile facts or weak documentation of long-term personal and economic links.

- Possible dual-residence exposure, even if day-count tracking looks strong.

- Use of a special scheme or status programme where eligibility boundaries are not clear.

- Treating permit status as a tax conclusion.

The Nomad Residence Permit is publicly described as allowing remote workers to live in Malta for up to 3 years while working remotely. Treat that as an immigration fact, not a standalone tax-residence determination.

Build a concise advisor packet#

| Packet item | What to include |

|---|---|

| Timeline | Month-by-month presence, key travel dates, and upcoming filing milestones. |

| Income map | Source by country and payment flows. |

| Remittance summary | What moved, when, from which account, and why. |

| Evidence status | What is complete, missing, or low confidence. |

| Treaty questions | Where tie-breaker risk could arise. |

The quality of this packet affects the quality of advice you get. If records are clear and questions are specific, advisor time can go to legal analysis instead of document cleanup, which may reduce follow-up cycles.

Questions that force a clear position#

Use questions that force facts, law, and process into one clear line. As a practical framing aid, MTCA presents Tax Residence and Special Schemes as separate topics, so keep baseline residency analysis separate from programme benefits.

- Which legal tests control my case, and which facts carry the most weight?

- Which facts are neutral, and which weaken my current position?

- If dual residence is plausible, what analysis must be completed before filing?

- What evidence best supports my tax-residency position, and is a certificate request appropriate?

- Where does a special scheme help, and where does it not change baseline residency analysis?

- What must be resolved now versus deferred to the next review cycle?

Avoid the mistakes that create expensive rework#

Expensive rework usually starts when a position is built on labels or assumptions instead of records you can show.

Four mistakes that usually force a rewrite#

| Mistake | What goes wrong | Practical fix |

|---|---|---|

| Treating a temporary residency card as automatic final approval | Interim status is treated as final, even though screening still applies. | Mark temporary status as provisional and wait for final outcomes before making final assertions. |

| Assuming immigration progress answers separate tax questions | Process milestones are used as if they settle issues they do not address. | Keep immigration process facts and separate legal/tax analysis in distinct workstreams. |

| Stating progress without clean application and remittance records | The timeline is hard to verify when submission and payment evidence is incomplete. | Keep dated proof of application receipt, remittance, and status updates in one file. |

| Ignoring key timing details in the reform terms | Teams miss constraints when they skip validity and eligibility timing checks. | Validate timing details up front, including one-year renewable temporary status and the stated backdating window from 1 January 2025. |

One trap is treating immigration progress as a final conclusion on other legal or tax questions. MPRP process updates may be useful context, but they are not a substitute for a separate legal analysis. Public descriptions note major reforms and a temporary card valid for one year on a renewable basis. They also note continued screening after application and remittance steps, including a EUR 15,000 application charge.

Fixing these issues in reverse order creates avoidable time pressure. Build the evidence file first, then finalize conclusions from a position you can document.

Verification checkpoint before you finalize#

- Confirm each core claim is backed by at least one dated document in your file.

- Confirm application, remittance, and status records align on dates and amounts.

- Keep unresolved items in one list with an owner and due date.

- Pause final assertions that still depend on assumptions, and escalate those points for advisor review.

Conclusion#

Low-stress tax decisions come from early choices backed by records, not assumptions made at filing time. If your facts are mixed, simplify your position now, document it as you go, and escalate quickly when dual residence or unclear domicile appears.

Use day count as an anchor, not a shortcut. The excerpts point to two practical routes in residency analysis. One is spending 183 days in a basis year. The other is showing intention to reside through economic, personal, social, or similar presence. Keep those facts aligned month by month so your year-end position does not rely on memory.

Keep source and remittance logic just as concrete. For resident non-domiciled cases, the excerpts describe Maltese-source income and remitted foreign income as core moving parts. They also describe foreign capital gains as exempt even when remitted. Use that for planning, but confirm current treatment for your specific facts before filing.

Treat conflicting minimum-tax wording as an escalation trigger. The excerpts include different framing around the EUR 5,000 and EUR 35,000 thresholds, so do not lock in assumptions without case-specific review.

When your life and work span countries, complexity itself increases risk. Nonaligned procedures can raise compliance cost and increase compliance risk, so escalate early when one fact pattern can support more than one residence claim.

Before your next internal review, complete this minimum pack:

- Presence timeline with day count, travel gaps, and supporting records.

- Intention evidence file covering economic, personal, and social presence.

- Income and remittance map with source, account path, date, amount, and purpose.

- Advisor question list covering unresolved domicile points, dual-residence risk, and items that need current confirmation.

Take the next step now while the file is still manageable. Update your residency memo, reconcile your latest transfers, and close any unresolved item that could change your filing position.

The core promise is simple: decide early, keep evidence current, and escalate before uncertainty turns into expensive rework.

Frequently Asked Questions

Does spending more than 183 days in Malta automatically make me tax resident?

Not automatically. The available third-party summaries conflict on whether 183 days is mandatory or only one indicator, so day count alone does not settle the result. Treat days in Malta as one strong signal, then check whether intention and ties point the same way.

What matters besides day count when Malta determines tax residency?

Documented intention to reside and personal and economic ties are central in the available material. A travel total on its own is usually not enough to explain the position. Keep dated records that show presence, living arrangements, and financial links in one coherent file.

Can I be tax resident in Malta and another country in the same year?

The provided excerpts do not directly answer this. They do show that day count may not be the only factor, with intention and ties also discussed. If your facts touch more than one country, get cross-border review before filing.

How does source and remittance basis work for resident non-domiciled taxpayers?

The excerpts describe a remittance-basis approach where movement of funds can affect treatment. They also describe foreign income not remitted to Malta as potentially outside tax for non-domiciled cases. Because these are third-party summaries, confirm current treatment before finalizing returns.

Are foreign source capital gains taxed in Malta for non-domiciled cases?

One source states foreign capital gains are not taxable for non-domiciled residents, even if brought into Malta. Use that as a verification point, not a filing shortcut. Confirm current treatment for your specific facts before relying on it.

What documents are typically used to support a Malta Tax Residency Certificate request?

No single checklist is definitive, so do not treat any one list as authoritative. A practical working file still helps: day-count timeline, evidence of regular presence and ties, and clear income and remittance notes. Confirm current requirements through official guidance or a licensed advisor before submission.

Is company tax residency under management and control the same as individual tax residency?

Do not assume they use the same test. The provided materials do not include the company management-and-control legal standard. Keep company and individual analysis separate and get entity-specific advice before filing.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Handle the Saving Clause in US Tax Treaties Without Guesswork

Start with documents, not conclusions. Before you take any `saving clause us tax treaties` position, write down your residency facts, period-by-period status, and filing logic in plain language so someone else can follow your reasoning.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.