Quick Answer

Decide status first, then source-tag income, then map deadlines and cross-border reporting. For malaysia tax for expats, the safest path is a one-page decision sheet tied to documents you already hold: travel chronology, EP/PVP/MEV records, contracts, invoices, payment proof, and withholding notes. Use stricter interim treatment when facts conflict, keep Malaysia and IRS tracks separate, and escalate before filing if residency, treaty position, or incentive eligibility could change the outcome.

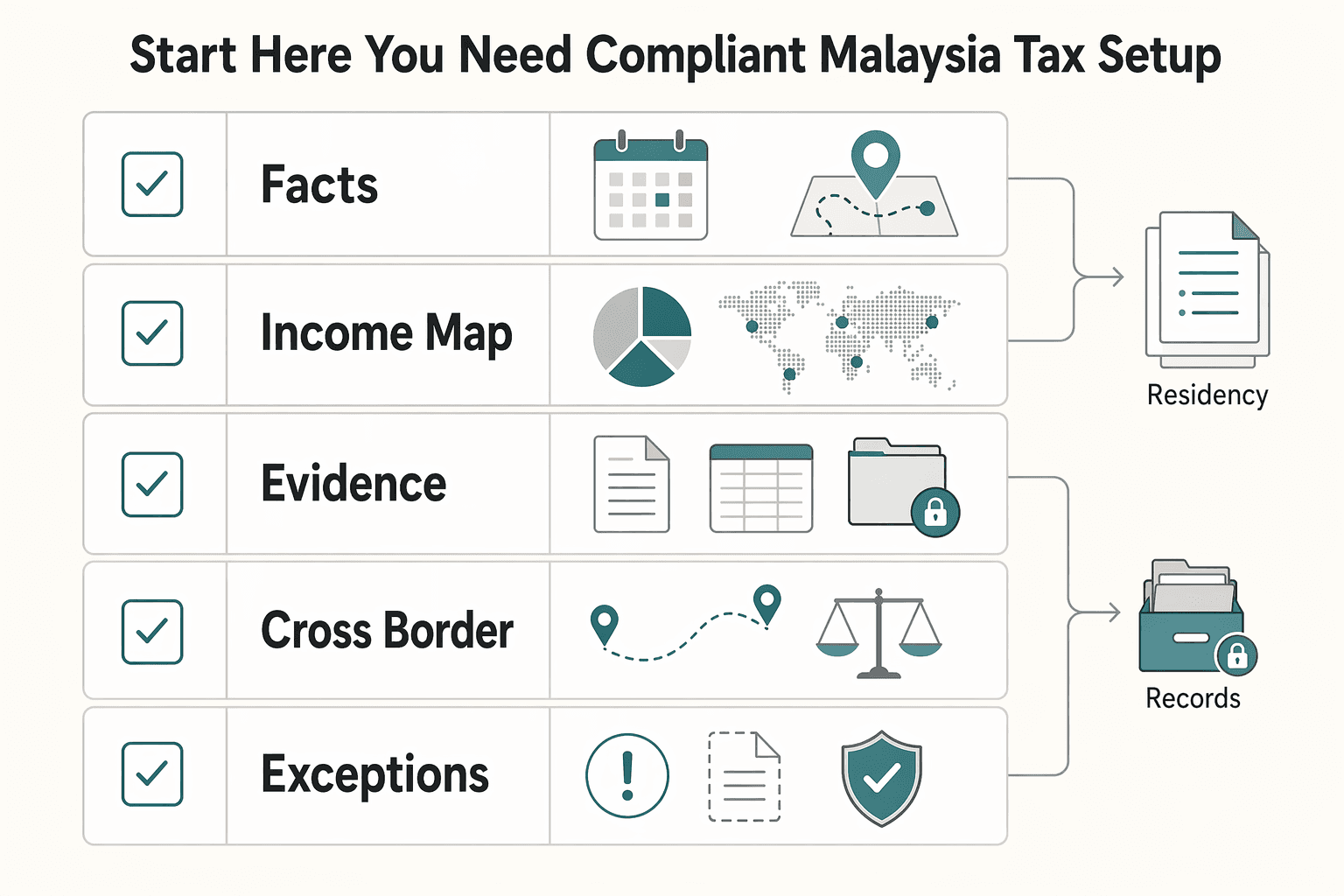

Start Here if You Need a Compliant Malaysia Tax Setup#

Start with compliance, not rate shopping. Decide your likely residency position first, separate income by source second, and document each assumption so you can defend the filing position if you are later asked how you reached it.

A lot of people jump straight to rates when they look into Malaysian tax. For freelancers, consultants, and anyone with cross-border work, that usually creates avoidable mistakes. Once you start with a calculator instead of facts, you end up forcing messy real life into neat categories that may not hold. If you also have U.S. filing obligations, the cleanup gets harder because one weak assumption can affect two systems at once.

The fix is straightforward. Build a short decision sheet with facts only, and keep it updated as the year develops instead of rebuilding the story at filing time.

- Status snapshot: facts that support resident or non-resident treatment.

- Income map: payments tied to work done in Malaysia versus foreign-sourced income.

- Evidence pack: contracts, invoices, payment records, and travel-day logs.

- Cross-border flag: whether you are a U.S. person who still files on global income.

- Escalation trigger: the one assumption that would change liability most if wrong.

That sheet is not busywork. It gives you a controlled starting point. If facts change later, you update one page and trace the impact through the rest of the file. Without it, people tend to mix status, source, and filing mechanics into one rough estimate that becomes harder to unwind each month.

Use common expat guidance as a first screen, then verify before filing. Some summaries, for example, treat 182+ days as a resident indicator and non-resident treatment as a flat 30% with no deductions. That can be a useful working assumption, but it is still only a starting point until you confirm the current IRBM/LHDN position that applies to your facts.

Early on, record quality matters more than perfect forecasting. Some commercial guidance warns that late payment can trigger a 10% penalty that may rise to 15% if unpaid, and serious non-compliance can involve fines up to RM20,000. Even if your final numbers later change, good records usually reduce both the risk and the cost of cleaning up the position.

If residency is unclear or sourcing is mixed, use the stricter interim path, write down why, and escalate early. Also add tax clearance to your contract-end checklist so compliance does not get missed when an engagement wraps up and everyone is focused on operational closeout. A clean setup at the start makes every later decision easier, from forecasting cash to filing the return to answering questions if a review ever comes.

Related: Kuala Lumpur, Malaysia: The Ultimate Digital Nomad Guide (2025).

The Mental Model That Actually Matters#

If you remember one thing, remember the order. Most filing mistakes happen because people total income first and ask source and status questions later. Reverse that order. The model that actually holds up is simple: status, income source, then timing.

| Step | Decision | Key rule |

|---|---|---|

| Status | Resident individual or non-resident individual | Resident treatment uses progressive rates with personal relief. Non-resident treatment is taxed at the top marginal rate without personal relief. |

| Source | Malaysia-sourced income or foreign-sourced income | Malaysia taxes income accruing in or derived from Malaysia for both residents and non-residents. For resident individuals, foreign-sourced income received in Malaysia is exempt from 1 January 2022 to 31 December 2026 only under stated conditions, including tax paid in the country of origin. From 1 January 2027, remitted foreign-sourced income is taxable in Malaysia. |

| Timing | Form and deadline path | Use Form BE if there is no business income and Form B if business-source income exists. Common balance tax dates are 30 April for Form BE and 30 June for Form B, with a 31 December year-end basis period. |

Start with personal income tax status: resident individual or non-resident individual. That split drives the treatment. Resident treatment uses progressive rates with personal relief, while non-resident treatment is taxed at the top marginal rate without personal relief. You do not need a perfect conclusion on day one, but you do need a provisional one and a short note showing which facts could change it.

That distinction matters because once you total everything too early, you start building estimates on the wrong base. A bad status assumption will distort rates, relief expectations, and sometimes the filing path itself. In practice, a clean status memo saves more time than a more elaborate spreadsheet.

Next, separate Malaysia-sourced income from foreign-sourced income before you total anything. Malaysia taxes income accruing in or derived from Malaysia for both residents and non-residents. For resident individuals, foreign-sourced income received in Malaysia is exempt from 1 January 2022 to 31 December 2026 only under stated conditions, including tax paid in the country of origin. From 1 January 2027, remitted foreign-sourced income is taxable in Malaysia. That makes source tagging part of the tax decision itself, not a bookkeeping detail you can clean up at the end.

Only after status and source are set should you focus on timing and filing mechanics. Your ledger, payroll entries, and year-end summaries are inputs. They do not decide the filing position on their own. If you skip the first two steps, timing work just gives false precision to the wrong answer.

When facts are incomplete, use a disciplined fallback instead of guessing:

- If status is unclear, choose the stricter interim path and record why.

- If source is mixed, tag each payment before aggregation.

- If treaty relief might apply, treat it as conditional until treaty conditions are confirmed.

- If non-resident employment days are more than 60 but less than 183, flag for treaty review instead of assuming exemption.

Finish with a filing-form check. Align income type to the return form early so you do not build the wrong workpapers all year. Use Form BE if there is no business income, and Form B if business-source income exists. For residents, common balance tax dates are 30 April for Form BE and 30 June for Form B, with a 31 December year-end basis period.

That is the core logic: first decide who you are for tax purposes, then decide what each payment is, then build the calendar and records that support the return.

Define Your Status Before You Estimate Any Tax#

Do not estimate tax from a visa label or a rough day count. Set status with evidence first, then model the numbers. Under Malaysia's self-assessment approach, the liability you report is your responsibility, so the estimate is only as good as the status memo behind it.

The practical move is to build a one-page memo before you touch a calculator. Start with immigration and movement records, including EP, PVP, or MEV documents where relevant. Base residency conclusions on physical presence, and assess work activity separately for taxable income. A pass category can be relevant evidence, but it is not a substitute for the tax analysis.

Keep the memo tight and fact-based. You are not writing a long legal summary; you are capturing the few facts that can move the result.

- Entry and exit chronology for the full calendar year.

- Pass validity periods matched to passport stamp dates.

- Client by client work arrangement and where services were physically performed.

- Open facts that could move treatment between resident and non-resident.

Use IRBM/LHDN guidance as your verification checkpoint. Individual residency is tied to physical presence in Malaysia, not nationality or citizenship, and references Section 7 of the Income Tax Act 1967. The 122-day plus 61-day example reaching 183 days is best treated as a documentation example, not a universal shortcut.

After that, run an activity check. If employment is exercised in Malaysia, full income from that employment is taxable. If you run a business, you still report income even if the business records a loss. That is why you should review status and activity together but keep them analytically separate. One tells you how the person is treated. The other helps determine what income must actually be reported.

Before you forecast liability, confirm the basic compliance items are in place: TIN registration, return submission, tax payment, and retention of income-related records. Align the memo to the calendar-year basis period so your evidence and your filing year line up. If any of those pieces are missing, label the estimate as provisional and close the gap before you rely on it for pricing, budgeting, or contract decisions.

A common failure mode is conflicting records. If pass records, travel logs, and work-location evidence do not match, keep the estimate provisional until the facts are reconciled. Do not smooth over the mismatch with a rounded day count or an optimistic assumption. That usually only delays the real work and raises the chance of having to redo the analysis later.

Once status is anchored, the next job is making sure each payment is labeled correctly. That is where many otherwise careful filers lose control of the file.

If you want a deeper dive, read Malaysia's DE Rantau Nomad Pass: A Guide for Applicants.

Classify Your Income Before You Touch a Tax Calculator#

Bad income labeling creates more cleanup than a bad spreadsheet. Once status is sketched in, the next risk is treating unlike payments as if they were all the same thing. Classify every payment before you calculate anything. Using one blanket label all year and trying to fix it at filing time is one of the fastest ways to create avoidable rework.

| Bucket | Description |

|---|---|

| Consulting fees | Payment for your direct services |

| Retainer payments | Recurring fees for access, availability, or reserved capacity |

| Reimbursed expenses | Amounts paid back to you for specific costs |

| Pass-through amounts | Money collected for third parties, not your own earnings |

Start with four working buckets and keep them separate from day one. These are not final legal conclusions. They are practical sorting tools that stop you from mixing revenue, reimbursement, and pass-through amounts too early.

- Consulting fees: payment for your direct services.

- Retainer payments: recurring fees for access, availability, or reserved capacity.

- Reimbursed expenses: amounts paid back to you for specific costs.

- Pass-through amounts: money collected for third parties, not your own earnings.

That first sort matters because it shapes what you review next. A consulting fee and a reimbursed expense may hit the same bank account, but they do not raise the same questions. If they sit in one pile all year, your totals may look clean while the underlying support is weak.

After bucketing, tag each line item with two things: a source tag and the receipt context. For the source tag, use a simple internal label such as Malaysia-source candidate or foreign-sourced income candidate. For the receipt context, capture the client entity, contract clause or SOW, invoice ID, payment date, and where the work was physically performed. That gives you enough context to revisit the classification later without reopening the entire file from scratch.

If an item is missing core evidence such as a contract, invoice, or payment proof, move it to a review queue before you run totals. That step feels conservative, but it is usually faster than unwinding a full-year model later. It also keeps uncertain items visible, which is better than burying them inside a larger number and forgetting they were never properly supported.

Cross-border income needs one more check: pre-map treaty risk by country pair before filing season. One U.S.-expat summary shows "Tax Treaty: No" in its Malaysia snapshot, while Malaysia materials also discuss Double Tax Avoidance Arrangement topics. Treat that kind of mismatch as a verification prompt, not a filing conclusion. The point is not which summary is right; conflicting summaries are your cue to verify rather than assume.

Tie the classification work to filing artifacts early. For Malaysia tax residents, that same expat summary lists BE Form as the primary resident form, a January 1 to December 31 tax year, and an April 30 deadline, with an update date of April 9, 2024. Those are useful planning anchors, but recheck current filing expectations before submission.

Use a hard rule here: if a payment cannot be confidently bucketed and source-tagged from your evidence, do not put it in the calculator yet. A delayed estimate is cheaper than a confident estimate built on weak labeling.

Use a 30 Minute Decision Sequence to Pick Your Filing Path#

Once status and source are tagged, you can usually choose a defensible provisional path in one focused sitting. This 30 minute sequence will not settle every edge case. It will isolate unknowns, stop unsupported assumptions from spreading, and make escalation obvious when it is needed.

Start by giving yourself a tight container. Pull up the status memo, the income map, the current ledger, and any withholding documents. If the core records are not open in front of you, the session turns into memory work, and memory is exactly what you do not want to rely on here.

- Minute 0 to 8: Provisional status call

Use the status memo to set a provisional label for the jurisdiction in scope. If another jurisdiction is involved, capture that now rather than letting it surface late in the process. That can include labels such as part-year resident or nonresident. If travel records, work-location notes, or supporting documents conflict, keep the stricter provisional label and flag the conflict rather than smoothing it over.

- Minute 8 to 16: Source and withholding scan

Recheck each income line against its source tags and mark where withholding may already apply so gross receipts are not treated as fully available cash. If another jurisdiction sits on top of the same work, note any local source rule or withholding issue there too. This is not the stage for final calculations. It is a quick screen to stop you from counting the same amount the wrong way in more than one place.

- Minute 16 to 24: Local filing map

Build a short local obligations table with only item, owner, and verification date. That keeps the work grounded in what you know instead of what you assume. Do not guess deadlines, forms, rates, or treatment. Leave unclear items marked unresolved. A short honest table is more useful than a complete-looking tracker full of unchecked assumptions.

- Minute 24 to 30: Cross-border overlay

If you are U.S.-linked, keep the IRS track separate from the local track so assumptions do not bleed across. IRS treaty-rate certification processes exist, and Form 8802 is used for U.S. residency certification in that context. The practical rule is simple: local filing first, U.S. overlay second, relief only after both sides are built on facts.

Before you accept the path, run one document check. Every line on the decision sheet should tie back to something you already hold. That includes the status memo version, contract or SOW reference, invoice ID, payment proof, and any withholding certificate. If another jurisdiction uses a withholding certificate, treat an incomplete certificate as unusable until fixed. A filing path is only as good as the paper trail behind it.

If key items are still unresolved at minute 30, stop there. Do not force a final calculation just because the timer ran out. The useful output is a one-page summary with provisional status, income-source summary, withholding checks, local unknowns, IRS overlays, and explicit escalate now triggers tied to facts. That is enough to keep the process moving without pretending uncertainty is gone.

Turn that decision sheet into a repeatable monthly process with the Tax Residency Tracker.

Build Your Filing Calendar Around IRBM Deadlines#

A clean return is usually built month by month, not rescued in April or June. Build your calendar around IRBM dates first, then run a monthly close against that calendar so filing becomes assembly work instead of reconstruction.

Malaysia's tax year runs from 1 January to 31 December. Use that window to stage your compliance work, then anchor the filing calendar to the profile you expect to use:

| Filing profile | Return path | Deadline anchor |

|---|---|---|

| Malaysia tax resident without business income | e-BE / BT | 30 April in the year following YA |

| Malaysia tax resident with business income | e-B / BT | 30 June in the year following YA |

Treat those as hard planning dates in your calendar. One published Malaysia tax table lists no return extension option, so the safe planning stance is to assume extra time will not be available. Even if later guidance gives more room in a specific year, you do not want your process to depend on that.

A monthly close does most of the heavy lifting. Keep it simple and repeatable:

- Match invoices to payment proofs and bank records.

- Update classification notes for each receipt.

- Reconcile withholding entries to supporting documents.

- Log missing evidence, assign an owner, and set a due date.

- Archive the month before starting the next cycle.

What matters here is consistency, not complexity. If the same tasks happen the same way each month, errors surface early and are cheaper to fix. If nothing gets reconciled until filing season, even small gaps can force you back through the entire year.

Add a quarter-end review of your personal income tax assumptions as an internal control. It is not an official IRBM deadline, but it is the right moment to test whether your actual income mix still matches your planned filing track, especially if business income appeared mid-year. Quarter-end is also a good checkpoint for asking whether the status memo still reflects the facts on the ground.

Before you submit, run one more status checkpoint. If facts changed during the year, re-check the filing assumptions and note the change in writing. Pair that with basic profile maintenance. If your address changed, CP 600B is due within 3 months of the change, so put that date on the calendar when the move happens, not at filing time.

Monthly Tax Deduction can be final tax only for specific employee groups that meet requirements, and filing exemption is conditional. If your case is mixed, cross-border, or simply unclear, assume filing is required until you confirm otherwise. That is the safer operating stance and usually the easier one administratively.

A calendar only works if the records feeding it are clean. That is why the next step is not another deadline, but a record bundle you can actually defend.

Keep an Evidence Pack That Survives an Audit#

If a reported number cannot be traced back to records you actually kept, the calendar will not save you. The easiest way to avoid that problem is to maintain one monthly evidence pack and treat it as the source of truth for the return.

Make one monthly pack your source of truth#

Close each month with one fixed bundle: contracts, invoices, payment confirmations, relevant pass and identity documents, income-source notes, and a locked ledger export for that month. That gives you one clean trail from contract to cash to filing position.

Keep the bundle standardized. Use the same folder structure every month and the same naming pattern for the core files. The goal is not elegance. Six months later, you should be able to open the pack and see, without guesswork, what was earned, what was received, what source treatment was considered, and what assumptions were still open at that time.

Keep a short dated assumptions log next to the pack. Record the key filing positions you relied on, plus any uncertainty and follow-up actions. You are not creating paperwork for its own sake. You are preserving your judgment trail so you can explain why you took a position if facts are revisited later. In practice, that log is often what separates a manageable follow-up question from a full reconstruction exercise.

If something changes after month-end, do not rewrite the old month. Post an adjustment in the next month and note why. That keeps the record trail clean and easier to defend. Rewriting earlier packs tends to blur what you knew at the time and what you learned later, which makes explanation harder, not easier.

Keep U.S. reporting on one account dataset#

If you are a U.S. person, do not build Form 8938 support from one account list and FBAR support from another. Use the same dataset so your account population, maximum values, and currency conversions stay aligned.

This is one of those boring controls that pays off immediately. When account lists drift, even slightly, you end up spending time explaining why one filing shows an account the other does not. Often the problem is not technical at all. It is just that two different exports were used at two different times.

Form 8938 is attached to your annual return and filed by that return's due date, including extensions. Filing Form 8938 does not replace FBAR. Form 8938 thresholds depend on filing context, and higher thresholds may apply to joint filers or U.S. taxpayers residing abroad. A $50,000 baseline is often cited, but confirm your filing context before relying on any threshold. If no income tax return is required for the year, Form 8938 is not required.

FBAR has its own trigger when a single account or aggregate maximum account values exceed $10,000 during the calendar year. Use a reasonable approximation of each account's maximum value, rely on periodic statements when they fairly reflect that maximum, report in U.S. dollars, and round up to the next whole dollar. If no Treasury exchange rate is available, use another verifiable rate and provide the source.

The practical takeaway is straightforward: build once, use it many times. One clean account dataset is easier to maintain, easier to test, and much easier to defend than several almost-matching lists.

Run a mismatch check before filing#

Before you file, do one reconciliation pass across the whole pack. This is the last chance to catch the kind of mismatch that does not show up in totals but does show up in supporting records.

- Confirm the account list used for Form 8938 and FBAR review comes from the same dataset.

- Confirm Form 8938 support files clearly state the applicable calendar year or tax year.

- Confirm the assumptions log still matches what you plan to file.

If records conflict, stop and rebuild both workpapers from the same monthly ledger exports and statements before submission. That is much cheaper than explaining inconsistent account reporting after the fact. The same principle applies on the Malaysia side too. A filing position is much easier to support when every supporting file points back to one dated monthly pack.

Handle Cross Border Obligations Without Double Counting#

Cross-border compliance is easier when you separate the local return logic from the U.S. return logic at the start. Build each side on its own facts first, then apply any available relief. That sequence reduces the risk of double counting and keeps one country's assumptions from distorting the other.

This matters because people often try to solve both systems with one rough answer. They look for a single rate, a single exclusion, or a single treaty idea that will make the entire issue disappear. In practice, that approach usually fails because each system asks its own questions first. Relief only makes sense after those baseline questions are answered.

Separate filing logic before you claim FEIE#

Start with one cross-border income sheet that captures payer, service location, and payment date. Then test FEIE eligibility on the U.S. side. For the physical presence route, the test is time-based: 330 full days within 12 consecutive months, and a full day is 24 consecutive hours from midnight to midnight.

This is one area where intent does not save a weak record. If you miss the minimum days, the test fails, including common disruptions such as illness, family issues, vacation, or employer instructions. If your day log is incomplete, run a provisional U.S. calculation without FEIE and update only when the count is defensible. That may feel conservative, but it protects you from building the U.S. file around a day-count result you cannot prove.

FEIE also has scope limits. It applies to wages or self-employment income for services performed in a foreign country, is claimed on Form 2555 or Form 2555-EZ, and still requires filing a U.S. return that reports the income. The maximum exclusion is $130,000 for tax year 2025 and $132,900 for tax year 2026.

The key discipline here is sequence. First identify the income and the days. Then test the exclusion. Do not assume the exclusion first and work backward to justify it.

Keep FBAR and account records aligned#

Account reporting is another place where small inconsistencies create outsized problems. Use one account dataset for FBAR and related reporting support so values, owners, and account lists do not drift apart.

FBAR can be triggered when a single-account maximum or aggregate maximum account value exceeds $10,000 during the calendar year. For mechanics, value each account separately first, then convert non-U.S. currency amounts into U.S. dollars before aggregation.

Before filing, run a short pre-filing check:

- Confirm the same account list is used across account schedules.

- Confirm maximum-value methodology is consistent across account schedules.

- Confirm one conversion method is used across all non-U.S.-currency accounts.

Those checks are simple, but they catch the most common avoidable mismatches. If the account population or valuation method changes from one filing to another, you want to know that before submission, not after.

Test Self-Employment Tax Exposure as a Separate Decision#

If you are self-employed in U.S. terms, test self-employment tax exposure directly instead of assuming FEIE or foreign tax paid will solve it. That is a separate decision, and it deserves its own review before you finalize return mechanics.

This is where people often compress too much into one mental shortcut. FEIE is one relief concept. It is not the whole cross-border answer. Account reporting is another issue. Local filing is another. Self-employment exposure is another. Keep those checkpoints separate. That is what stops one optimistic assumption from quietly spreading through the rest of the file.

The practical point is simple: do not let one relief concept stand in for the whole cross-border analysis. Work through the income, the filing path, the account reporting, and the self-employment question as separate checkpoints.

You might also find this useful: How to Legally Avoid Double Taxation: A Freelancer's Guide to Tax Treaties.

Treat 15 Percent Incentive Regimes as Exceptions Not Defaults#

A 15 percent headline is not a filing position. Treat any incentive regime at that rate as a possibility, not a default, and do not price projects, forecast cash, or commit to a preferential treatment until current official terms clearly match your facts.

This is one of the easiest areas to get wrong because the headline is attractive and the detail is often conditional. Location, recruiter language, and program marketing can all make an incentive sound broader or more automatic than it is. That does not mean the incentive is unusable. It means you should keep it out of your baseline until the conditions are actually confirmed.

If you come across names such as Iskandar Malaysia, Iskandar Development Region, ECER, the Returning Expert Programme, the PENJANA initiative, or the Forest City Special Financial Zone, keep them in the conditional bucket until verified. Apply the same caution to activity near the Malaysia-China Kuantan Industrial Park. Location, recruiter language, or marketing copy is not proof of eligibility.

Use MIDA as the first checkpoint#

Start with MIDA when the issue is investment-linked incentive direction. MIDA is the government's principal investment promotion and development agency under MITI, and its policy booklet says to check MIDA's website for the latest updates. The same booklet also states that guidebook information may contain incorrect information or omissions.

The rule is straightforward: if a term is not confirmed in current official material, do not treat it as committed tax savings. That one habit will save you from building forecasts on conditions that were limited, outdated, or never applicable to your activity in the first place.

Build an incentive evidence file before changing forecasts#

If an incentive still looks relevant after the first screen, build a dedicated evidence file next to your tax assumptions log. For each regime, record the program name, review date, source title, and exact condition wording you relied on. Add a short memo with three fields only: confirmed facts, unconfirmed facts, and go or no-go decision date.

Before you book any 15 percent assumption, run this check:

- Confirm the rule comes from current official material, not a secondary summary.

- Confirm conditions match your activity type, location, and timeline.

- Confirm whether wording suggests discretionary approval or limited validity periods.

- Confirm review date and reviewer are captured in your records.

The tradeoff is clear. Potential incentives may reduce tax cost, but they add verification and documentation work. If the facts are borderline, keep a conservative baseline and change course only when eligibility is clearly in range. That is almost always better than forcing the economics to work on an incentive that was never fully verified.

Avoid the Mistakes That Trigger Expensive Cleanup#

Expensive cleanup usually starts with ordinary process errors, not exotic technical issues. The patterns are predictable: stale assumptions, records that do not support the filing position, and relief claims that were never mapped properly across countries.

- Relying on old internet rates instead of current treatment

Public tax threads can sound certain and still be stale or unqualified. One public answer on this topic says the writer is not a tax expert and cites a 2021 table. Use public summaries to frame questions, not to lock in a filing position. A quick summary can be helpful at the start, but it is a poor substitute for a current, fact-based review.

- Assuming a visa or pass decides tax outcome on its own

Visa status alone does not settle the tax analysis. Tax exposure can change when residency status changes, so test the filing position against current-period facts instead of treating the immigration label as the answer. Pass records are useful evidence, but they do not replace the physical-presence and work-activity analysis.

- Letting record gaps build until filing positions are hard to defend

Mixed or incomplete records turn a manageable filing job into reconstruction work. Keep a clear evidence trail for local tax filings, registrations, and payroll-related obligations so your position is supportable without rebuilding the year from memory. The longer gaps sit unresolved, the more likely it is that explanations start depending on recollection instead of documents.

- Filing in one country before mapping treaty relief in the other

Relief that is identified too late often stops being useful. If it is not mapped early, delayed assessments can turn a manageable plan into retroactive cleanup. One 18-month assignment example ended more than 25% over budget after tax, payroll, and compliance issues were identified late.

Use one rule across all four: if your evidence is weak, use a more conservative filing position until the documentation supports something narrower. That may feel slower up front, but it is usually the fastest way to avoid a second round of work.

When to Escalate to a Tax Professional Immediately#

Escalate when an unresolved point could change your filing position, reporting obligations, or the cash you need to set aside. That is the point where a review adds real value. Waiting until the return is due usually means the professional is cleaning up a bad process instead of confirming a good one.

Escalate immediately if any of these are true:

- Your Malaysia filing position is unclear and changes your tax outcome.

Do not finalize a return on a status assumption that could reasonably go more than one way. If resident versus non-resident treatment changes the result in a material way, get that reviewed while the file is still easy to fix.

- Your plan depends on a named incentive regime, for example Iskandar Malaysia.

If the economics only work at a preferential rate, get that reviewed before you rely on it for pricing, budgeting, or estimated payments. Incentive uncertainty is manageable early and expensive late.

- U.S. reporting overlaps with Malaysia filing and FEIE treatment is uncertain.

FEIE physical presence is time-based: 330 full days in a 12-consecutive-month period, and a full day is 24 consecutive hours (midnight to midnight), with a foreign tax home condition. Travel disruptions can break eligibility, FEIE is claimed on Form 2555/2555-EZ, and excluded income is still reported on the U.S. return.

- FBAR/FATCA/Schedule SE handling is inconsistent or unclear.

For FBAR, the trigger references whether foreign accounts reached a $10,000 maximum or aggregate maximum at any point in the year. Maximum values can be a reasonable approximation based on periodic statements, and reported amounts are rounded up to whole dollars.

- Prior-year returns used assumptions you no longer trust.

If earlier filings may be wrong, address that before you file the current year and compound the issue. A clean current-year file does not fix a weak prior-year position, and sometimes it makes the mismatch more visible.

Bring a focused review pack. At minimum, that means prior-year returns and workpapers, your assumptions log, FEIE day-count support with any Form 2555 filing, and FBAR maximum-value calculations from account statements. If the issue concerns status, include the travel log and pass records. If it concerns sourcing, include contracts, invoices, and payment proof. A tighter pack usually leads to a faster and more useful answer.

What to Do This Week to Stay Compliant#

Use this week to turn uncertainty into dated decisions, named owners, and a record trail you can defend. You do not need perfect final numbers yet. You do need a clean provisional position and the evidence behind it.

Start with a one-page decision sheet. Record your current tax-residency position, the income-treatment assumptions you are using, and what remains unresolved. One expat summary says non-residents face a flat 30% rate on Malaysian-sourced income with no personal reliefs or deductions. Treat that as a risk checkpoint until you confirm current LHDN guidance for your filing year.

Include:

- Tax-residency position used today.

- Immigration facts for the same period, including EP/PVP/MEV dates.

- Income by period and source, with unclear items flagged.

- Open assumptions, owner, and target decision date.

Next, set up the evidence pack structure and backfill recent records. Organize contracts, invoices, payment proofs, bank records, pass documents, and a short assumptions log by month. Do not overdesign this. A simple month-by-month file is enough if it is complete and consistent. For immigration, verify that any required work permit was in place before employment started and that EP/PVP sponsorship details in Malaysia are documented.

Then put deadlines and monthly close checkpoints on one shared calendar with owners and due dates. Anchor tracking to Malaysia's year of assessment, 1 January to 31 December, so records map cleanly to the year being assessed. Add immigration timing guardrails too: EP renewal about three months before expiry, and PVP planning that respects the 12-month cap with no extension beyond 12 months.

Finally, treat published filing-date summaries as provisional until you confirm current LHDN notices for your filing year. If any material uncertainty is still active after this setup work, schedule a tax review now instead of waiting for filing week. The goal this week is not to solve every edge case. It is to set up a process that keeps uncertainty visible, evidence organized, and next decisions obvious.

If your status or cross-border obligations are still ambiguous after this checklist, contact Gruv to discuss a compliance-first setup.

Frequently Asked Questions

Are expats taxed differently in Malaysia if they are a Malaysia tax resident versus a non-resident individual?

Resident versus non-resident tests, rates, and thresholds can be material to your outcome. Treat status as potentially material, verify the current-year position with current IRBM/LHDN guidance, and escalate before filing if facts can support more than one status.

What changes first when my status flips between resident and non-resident under Malaysia personal income tax rules?

Use a dated status-change note and separate income by period so assumptions stay clear and auditable, then get a technical review before filing.

What are the key filing dates with IRBM/LHDN if I have business income?

Use the current official IRBM/LHDN schedule as your record source and keep its publication date in your compliance notes. If you also file in the US, map both calendars before submission.

Can foreigners realistically qualify for the 15% regimes in Iskandar Malaysia or ECER?

This guide does not provide eligibility criteria or mechanics for Iskandar Malaysia or ECER 15% treatment. Treat any 15% assumption as unconfirmed until your facts match current official program terms. If your plan only works with incentive treatment, escalate before relying on it.

Does a DE Rantau Nomad Pass change my tax residency result by itself?

This guide does not support that a DE Rantau Nomad Pass alone determines Malaysian tax residency. Keep immigration status and tax status as separate determinations backed by dated records. If records point to different conclusions, get professional review before filing.

If I am a US person, how do IRS filing, FEIE, FBAR, FATCA, and Form 8938 fit with Malaysia filing?

FEIE applies only to qualifying individuals with foreign earned income, and the physical presence test is time-based: 330 full days in any 12 consecutive months, with each counted day equal to 24 consecutive hours from midnight to midnight. Even if FEIE applies, you still file a US return reporting the income. The maximum exclusion is $130,000 for 2025 and $132,900 for 2026. FBAR is required when foreign account maximum value, or aggregate maximum value, exceeds $10,000 at any time during the year, and maximum values may be reasonably approximated from periodic statements with amounts rounded up to whole US dollars. Confirm FATCA and Form 8938 thresholds with the relevant authority before filing.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Malaysia DE Rantau Nomad Pass Application Playbook

Low risk starts with one rule: separate what third-party and community sources say from what you have personally verified on the live official application path. This guide follows that rule so you can plan your move without treating summaries or walkthrough videos as policy.

Kuala Lumpur Digital Nomad Guide for a Low-Risk Move in 2026

Kuala Lumpur can work well for remote professionals, but only if you decide your stay path before you price apartments or book flights. Treat the move less like an open-ended trial and more like a sequence: choose the legal route, assemble proof, then spend money.

How Freelancers Can Legally Avoid Double Taxation With Tax Treaties

Classify the tax problem before you touch a return. If your income is mostly personal service fees across borders, this guide fits. If your issue is C corporation profits and shareholder dividends, you are solving a different problem.