Quick Answer

Yes. Treat life insurance for freelancers as a current action when your death would leave a partner, child, co-borrower, or business partner with immediate financial pressure. Start with term life, set the payout around documented debts and essential expenses, and cap premiums using a weak-quarter budget so coverage remains active. Keep every application detail consistent across forms, and exclude Form 1099-LS from income-proof files because it is for reportable policy sales. Review policy wording for conversion rights, renewal pricing, exclusions, and claim steps before you sign.

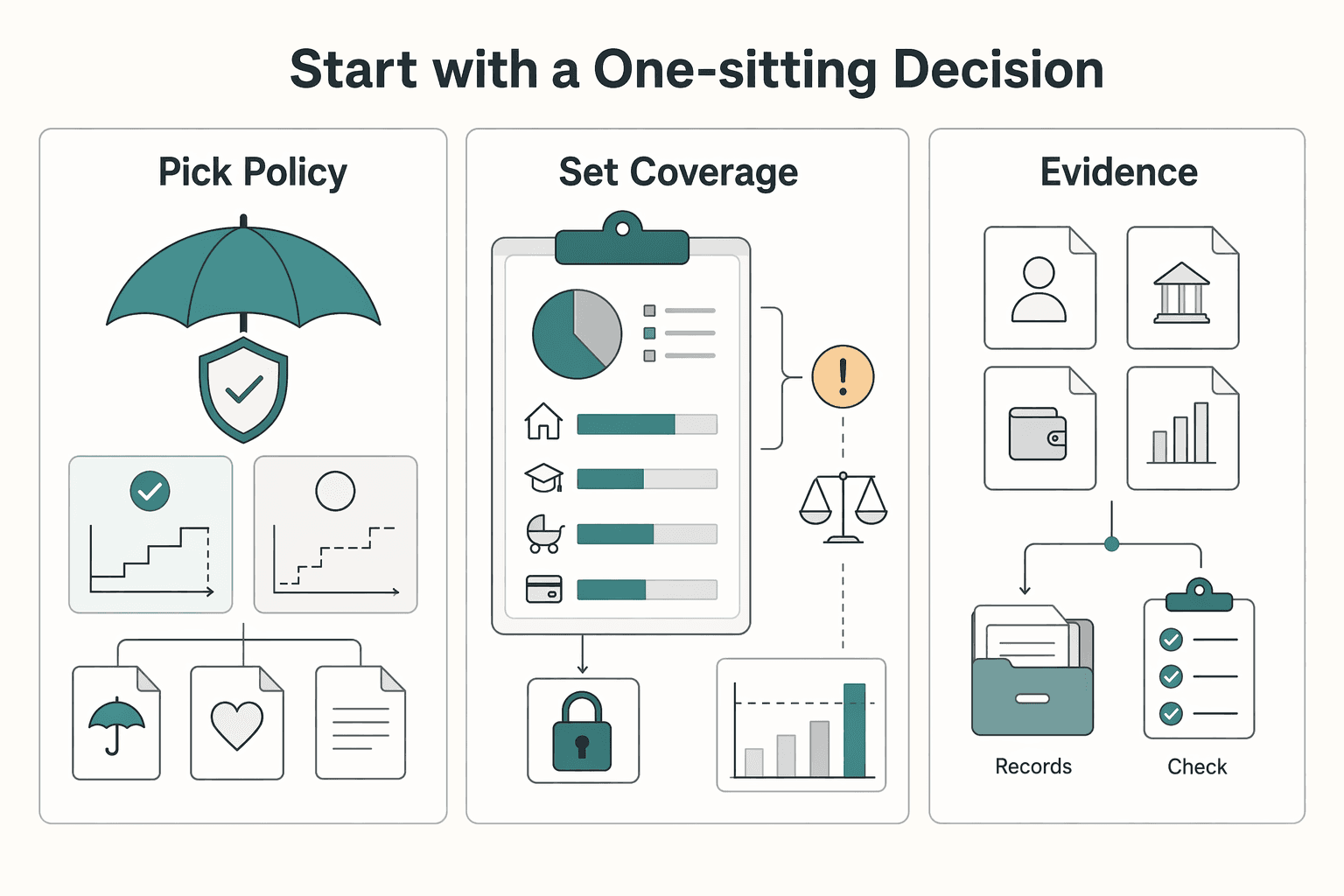

Start with a one-sitting decision, not a vague goal#

Make this decision in one sitting. Pick policy type, set a death benefit tied to real obligations, and prepare your application details before you shop. A single sitting matters because it forces tradeoffs into the open. If you split the call across weeks, it is easy to keep toggling between products without locking anything in.

Start with the clearest product first. Term life insurance pays beneficiaries if you die during the term, and a fixed term can lock payments for that period. For example, a 20-year term can lock monthly payments for 20 years. If you want to compare other policy types, do that as a second step.

The death benefit is the payout your family or business receives if you die while covered. Size it to obligations that still exist without your income, not to a generic calculator output. When you keep the target tied to named obligations, comparison decisions get easier because you can reject quotes that miss the core purpose. Use this order before you shop:

- Pick policy type.

- Set coverage amount based on specific obligations.

- Prepare application details and keep them consistent across documents.

Do not skip step three. If details do not match across documents, the process can slow down. Put your core documents in one place and keep the same details across forms.

One form trap is easy to avoid: Form 1099-LS is not a general freelancer income form. The IRS describes it as a form filed by an acquirer in a reportable life insurance policy sale, so it does not belong in your income-proof checklist.

Accuracy is part of protection. During the contestability period, insurers may recheck the application for reasons to deny a claim, so verify dates, disclosures, and personal details before submission. This is not admin trivia. Small mismatches can create claim friction later, and those problems are harder to fix after issue.

Once this first decision stack is done, the next move is straightforward: map exactly who and what would be exposed if your income disappeared. If you want a quick next step for life insurance for freelancers, try the free invoice generator.

Map your real risk before you shop#

Before comparing quotes, map who is exposed if your income stops. This keeps insurance planning for freelancers grounded in practical risk, not abstract benefit shopping. The map should answer one practical question: who has to make a hard decision first if your income disappears tomorrow?

As a freelancer, you are often responsible for your own income, health coverage, and business liabilities. Use a simple one-page map with two buckets:

- Personal obligations: household costs, shared debts, and anyone who depends on your income.

- Business obligations: liabilities and commitments that could pressure operations if your income drops.

- For each item, note who is affected and what hard decision appears first without cash support.

Keep each line concrete. Instead of writing family support, name the specific payment or responsibility. Instead of writing business continuity, name the first operational pressure point. This makes your insurance choices easier to defend and keeps you from buying for vague fears while missing fixed liabilities.

If you recently left full-time employment, run a transition check. List the protections you used to have through an employer, then confirm what still exists today. Gaps are often easier to see once everything is in one list.

Use one quarter-level checkpoint: if losing your income would force a partner, child, or business partner into hard financial choices, coverage belongs on this quarter's list. If the answer is no today, keep the map anyway. Your obligations can change quickly.

This map becomes your control document for the next sections. It helps you decide whether you need coverage now and which policy questions matter most. Related: The Modern Financial Architecture: Augmenting Your Offshore Company with FinTech.

Decide whether you need coverage now#

Use one gate: if your death would force a hard financial decision for someone else, treat coverage as a this-quarter action. This avoids endless debate about perfect timing and keeps the decision tied to impact. Act now if any one of these is true:

| Act-now trigger | Exposure | Timing |

|---|---|---|

| Someone depends on your income | A person who depends on your income | Treat coverage as a this-quarter action |

| You share debt that another person would need to carry | Another person who would need to carry the debt | Treat coverage as a this-quarter action |

| Your business would be financially exposed if you were gone | Your business | Treat coverage as a this-quarter action |

The timing issue is real after self-employment transitions. Fidelity Life's discussion of LIMRA's 2022 Insurance Barometer reports that 23% of respondents had coverage only through work. That same discussion warns that people moving to self-employment can lose financial protection for loved ones when benefits are job-linked. If your old benefits were job-linked, assume nothing until verified.

Before shopping, verify what is active today. List each policy, policy owner, beneficiary, and whether coverage is tied to a former employer. Keep that record current so you do not rely on protection that no longer applies. This single list also speeds later quote comparisons because you know exactly what gap you are replacing.

If you have no dependents and no shared liabilities, urgency may be lower. Keep the decision explicit anyway: defer with a dated reminder, then review as responsibilities change. Deferral is valid when risk is low, but it should be deliberate and time-bound, not accidental.

A useful rule is to separate no need now from no need ever. Your obligations can change over time, and the trigger list can change with them. Recheck when major obligations change. With need established, the next decision is product fit, so pick the simplest policy that covers the risk map you already built.

Choose between term, whole, and universal life insurance#

Start with term unless you have a clear reason to buy permanent coverage. The tradeoff is straightforward: term is generally cheaper, whole is usually more predictable at a higher cost, and universal offers flexibility with more moving parts. In practice, cost discipline matters more than product sophistication if your income can swing quarter to quarter.

The goal is the same across all three options: fund a death benefit for people who rely on you. Since that benefit is typically paid as a lump sum after death, the right policy is the one you can keep while meeting current obligations.

| Policy type | What it is | Cost and predictability | Main tradeoff |

|---|---|---|---|

| Term life insurance | Coverage for a fixed period, such as 10, 20, or 30 years | Generally the lowest cost | Coverage ends when the term ends |

| Whole life insurance | Permanent coverage that can last for life and includes cash value | Higher cost than term; premiums, cash values, and death benefits are guaranteed | Higher cost can reduce short-term cash flexibility |

| Universal life insurance | Permanent coverage with adjustable premiums and death benefits | More payment flexibility, but less predictability on cash value and coverage | Cash value growth depends on current interest rates, including downside risk if rates fall |

If budget is tight, secure enough term coverage first. Add complexity later only when income volatility is under control and ongoing costs will not strain operating cash. This keeps protection in force while you build financial room for optional features. Use this quick check before choosing:

- Match policy type to today's obligations, not a sales pitch.

- Test affordability against a weak month, not a strong month.

- For whole and universal options, separate guaranteed features from performance-dependent outcomes.

One failure mode to watch for is choosing permanent coverage for flexibility, then treating projected outcomes as guaranteed outcomes. Keep projections and guarantees separate in your notes. If an answer is verbal but not explicit in policy language, treat it as unresolved until documented.

Another practical rule is not to let product labels decide for you. The risk map and premium durability test should decide. If those two inputs point to term now, that is a disciplined decision, not a temporary compromise. Once type is chosen, sizing gets cleaner because you are estimating a target benefit, not debating product philosophy.

Size your coverage with variable income in mind#

For variable freelance income, size coverage from documented obligations and conservative earnings assumptions, not a single income multiple. The target is a death benefit that still protects dependents during a weak business period. If your sizing only works in a strong year, it is not a reliable plan. Run a records-first sizing pass:

| Sizing step | Grounded input | Why it matters |

|---|---|---|

| Income baseline | A conservative, representative earnings period, not your best year | Freelance income can be unpredictable |

| Core obligations | Debts, housing costs, and essential living expenses | Keeps coverage tied to real liabilities |

| Priority order | Fixed obligations before flexible spending | Protects core needs when conditions are not ideal |

| Stress test | A downside income case | If sizing only works in a strong year, it is not a reliable plan |

| Cross-check | Test the household side and the business side from your map | Adjust the target before you shop quotes if one side fails |

- List core obligations first: debts, housing costs, and essential living expenses.

- Base income replacement on a conservative, representative earnings period, not your best year.

- Prioritize fixed obligations over flexible spending.

- Pressure-test the amount against a downside income case and confirm the benefit still covers core needs.

Keep the math grounded in documents you already maintain. Because freelance income can be unpredictable, your sizing should not depend on optimistic assumptions. A conservative base gives you a benefit target you can explain and defend.

This approach keeps coverage tied to real liabilities instead of generic rules. With term coverage, beneficiaries receive the stated death benefit if death occurs during the policy term. The key question is simple: does that amount cover essential expenses and priority obligations when conditions are not ideal?

A practical cross-check is to test two scenarios from your map. First, test the household side and confirm essentials are covered. Second, test the business side and confirm outstanding obligations are covered. If one side fails, adjust the target before you shop quotes.

Avoid relying on revenue alone in this decision. Income can look healthy in one period and weaker in another, and that mismatch can create coverage targets that do not reflect what dependents actually need. After sizing, set term and premium limits that can survive lean months.

Set term length and premium limits that survive lean months#

Set a term and premium you can keep through a weak quarter. Coverage only helps while it stays active. The wrong policy is not always the cheapest or most expensive one. It is the one you cannot keep in force when income dips.

Choose a term based on your current financial responsibilities, then revisit it as those responsibilities change. You do not need a perfect formula, but you do need a clear rationale and a habit of updating it. If your obligations change, your term decision should change with them.

Set a hard premium ceiling using a conservative month, then test it against essentials. If premiums only work when cashflow is unusually strong, lower the target so coverage remains sustainable. This is where overreach can happen, especially after a strong billing stretch.

When income is unstable, keep product choice simple and affordable now, then revisit more complex options after reserves are consistently stronger. A policy that strains your budget creates a new risk. The point is dependable protection, not maximum policy complexity.

Recheck this decision alongside disability insurance and emergency cash. A serious illness or accident can cut income and raise expenses at the same time. Savings can disappear faster than expected after a major health shock. Keep enough liquidity for shocks, while recognizing the opportunity cost of holding cash that could be used elsewhere.

If you are UK-based, Statutory Sick Pay can be a useful benchmark check. It is cited at £116.75 per week for up to 28 weeks in the 2024/25 tax year, which can leave a significant income gap for freelancers. If you are not UK-based, use your local statutory support rules as a benchmark, since amounts and duration vary by jurisdiction.

Use this annual check before renewing or increasing coverage:

- Rebuild your budget using a low-income quarter.

- Confirm premiums still clear after essential costs and minimum obligations.

- Verify disability coverage and emergency savings remain funded.

- Reconfirm the term still fits your current responsibilities.

- If any check fails, reduce premium load before expanding coverage.

Treat this as a maintainability test. If a policy fails the weak-quarter test repeatedly, resize instead of hoping income smooths out. With type, size, and premium limits set, the next pressure point is submission quality.

Build your underwriting evidence pack before applications#

Submission quality affects how smoothly underwriting review can go, so prepare your evidence pack before starting applications. Applications are given individual consideration, and underwriters may request additional information as needed. You can reduce avoidable follow-up by making the file easy to review on first pass.

| Evidence item | What to include | Why it matters |

|---|---|---|

| Account-specific application | Completed in full | Avoids blanks and unclear entries |

| Tailored cover letter | Key context for your submission | Makes the file easier to review on first pass |

| Carrier-required supporting documents | Documents currently listed for your case | Carrier requirements can change |

| Written notes | Clarify details that could be interpreted more than one way | Reduces avoidable follow-up |

| Final consistency check | Match names, dates, and core details across forms | Consistency matters as much as completeness |

Build one current file set and keep answers aligned across every form. Never rely on the underwriter to fill in blanks. Consistency matters as much as completeness.

- An account-specific application completed in full.

- A tailored cover letter with the key context for your submission.

- Any carrier-required supporting documents currently listed for your case.

- Clear written notes anywhere details could be interpreted more than one way.

- A final consistency check so names, dates, and core details match across forms.

Before submitting, run a line-by-line check for blanks and unclear entries. If anything is unclear, clarify it in writing before filing.

Also confirm form names and carrier requirements right before applying. Form 1099-LS is for reportable life insurance policy sales, not standard freelancer earnings documentation, and underwriting requirements can change.

Keep a copy of exactly what you submitted. If an underwriter requests clarification, respond from that copy so each reply stays consistent with the original application.

Compare offers like contracts, not marketing pages#

Compare offers on written policy terms first, not headline premium alone. A low first-year price can be weak evidence if renewal terms, conversion rights, or exclusions are unclear. Price matters, but contract language is what you can rely on when coverage is needed.

Fidelity Life cites LIMRA's 2022 finding that 23% of respondents had life insurance only through work. For self-employed buyers, that employer layer may disappear, so contract clarity can matter more than a small upfront price difference. This is why freelancers should read policy terms like agreements, not promotions.

| What to compare in writing | Why it matters | Red flag |

|---|---|---|

| Conversion terms | Future flexibility may depend on what the contract allows. | Conversion language is vague or explained only verbally. |

| Renewal pricing behavior | Premium durability can affect whether coverage stays workable during uneven income periods. | You get first-term pricing only, with no clear renewal detail. |

| Exclusions and limits | Constraints can change whether coverage protects real obligations. | Exclusions are buried or described inconsistently. |

| Optional features | Added features may help align a policy with family or business needs. | Features discussed in calls are missing from policy paperwork. |

Treat faster-approval options as one path, then compare them with other options using the same checklist. Faster approval can help, but speed should not outrank clear terms. A quick issue decision is useful only if the policy still fits your obligations and budget over time. Before signing, run one final checkpoint:

- Coverage amount: Does the death benefit cover fixed obligations under a conservative income case?

- Premium durability: Can you keep paying through weak quarters and renewal periods?

- Policy constraints: Are exclusions, conversion rules, and optional-feature terms explicit in policy documents?

- Claim process clarity: Would your beneficiary know what to submit and how claims are handled?

If two offers are close, prefer clearer written terms even at a slightly higher premium. Clear terms lower the risk of surprises for both you and your beneficiary.

A practical tie-breaker is document quality. If one carrier provides complete policy wording early and answers in writing, and the other relies on verbal assurances, choose the one with better written clarity. With personal coverage reviewed, move to business continuity where dependence on your work creates separate exposure.

Protect business continuity when others depend on your work#

If others depend on your work, decide first whether coverage is for household needs, business continuity, or both. Avoid expecting one policy to cover every obligation. Splitting the objective upfront can keep your planning realistic.

For freelancers and small owners, employer-style backstops are often limited. In that context, life insurance can help cover business debts and provide funds to keep operations moving or wind down responsibly after death. The right structure depends on who would need to act immediately.

| Ownership structure | Continuity question | Insurance planning focus |

|---|---|---|

| Solo operator | Who can keep client delivery, billing, and communication moving? | Evaluate coverage for transition costs and business debts. |

| Small team led by one founder | What happens if one person holds most decisions and relationships? | Evaluate how coverage supports continuity if that person is no longer available. |

| Partner-based business | How are ownership and payment decisions handled during a transition? | Document ownership and payment decisions as part of continuity planning. |

Before signing, make continuity actions executable:

- Confirm terms in actual policy documents.

- Document who handles account access, client handoff, and payment routing during transition.

- Keep business continuity needs and personal needs separate when one policy cannot cover both clearly.

Add one more practical checkpoint: make sure the person expected to act can find the right documents quickly. A policy that fits on paper can still be hard to use if beneficiaries or partners cannot identify owner details, contact paths, or required claim documents.

When obligations have a defined horizon, term life insurance can fit because coverage is time-bound. When lifelong coverage is the goal, whole life insurance can fit because it is designed for lifetime coverage and includes cash value. In each case, rely on written terms before committing.

As continuity planning settles, align this coverage with the rest of your benefits choices so one priority does not quietly cancel another. If you want a deeper dive, read Canada's Digital Nomad Stream: How to Live and Work in Canada.

Coordinate life insurance with your broader benefits stack#

Set one decision order across your benefits stack: keep core life coverage in place first, then fund optional priorities. This keeps your priorities explicit when income is uneven.

Align health coverage, health savings, and income-protection choices with what you can sustain month to month. You do not need every detail finalized immediately, but you do need clear ownership and an order of decisions you can follow.

| Area | What to verify now | Common failure mode |

|---|---|---|

| Health coverage | Current cost and expected duration in your plan | Setting life premiums before confirming health-coverage spend |

| Health savings | Whether your plan setup matches your intended use | Funding savings goals on assumptions |

| Retirement savings | Contribution target you can sustain alongside core protection | Prioritizing savings targets, then cutting protection when cash tightens |

Apply the same discipline to riders. Riders are optional add-ons to a base policy, and a term rider is sometimes discussed for temporary high-cost periods. Prioritize fit over volume, and compare quotes with and without each rider so you can price each add-on clearly. If a rider does not solve a named risk from your map, it may be optional for now.

If you operate across locations, recheck assumptions by country. Benefits offerings can vary by market, and one global benefits page reports that 60% of workers prioritize better benefits while 67% expect benefits aligned with local norms. Treat that as a planning signal, not a universal rule.

Use one annual review date to update insurance, savings, and dependent obligations together:

- Confirm policy terms and rider language in policy documents.

- Recheck current health-coverage cost assumptions.

- Set retirement contribution targets that remain sustainable with baseline protection.

- Run a tax checkpoint with a qualified tax professional before acting on jurisdiction-specific assumptions.

The annual review is where you protect consistency. When priorities compete, return to the same rule: keep core protection maintainable first, then expand.

Make the decision now and review it once a year#

Make the decision this week, then keep coverage at a level you can maintain through uneven months. The practical target is reliable protection with terms you can explain and keep in force. Waiting for perfect certainty can mean carrying avoidable risk longer than necessary.

Set your coverage target from obligations you can document, not your strongest recent quarter. For self-employed applicants, insurers may evaluate stability by averaging pre-tax profits across prior years, sometimes over a 1-3 year window. Size against a conservative income view. That same conservative lens can also make your premium choice easier to maintain.

Before you apply, run one verification pass:

- Confirm the premium still works in a slow month.

- Check that beneficiaries, debt goals, and term choice match current commitments.

- Keep income records consistent across official documents and business bank statements.

- If your market uses country-specific proofs such as SA302s, confirm the local equivalent your insurer accepts.

Set one annual review date, and consider revisiting sooner if there is a major income change, a new dependent, new debt, or a business structure change. These shifts can change who depends on your income and how much risk sits with you personally versus the business. If one trigger happens, rerun your map, then recheck policy type, coverage amount, and affordability.

If you also carry income protection, keep that math separate from life coverage. Some income-protection products are based on average pre-tax profits and may cap benefits, which serves a different purpose than a life policy death benefit. Keeping those two decisions separate helps you avoid underinsuring dependents while still planning for temporary income loss.

Take one concrete next step now: gather your core records, lock a preliminary coverage target, and start comparisons using written terms. That is enough to move from intent to an active decision you can maintain.

Frequently Asked Questions

Do freelancers need life insurance?

Usually yes when someone depends on your income or financial support. Many freelancers do not have employer-sponsored life coverage, so the gap can appear quickly after leaving traditional employment. If your income stopping would pressure others immediately, treat coverage as a priority. If nobody depends on your income today, coverage may be less urgent now, but revisit the decision as your situation changes.

How much life insurance should a freelancer buy?

There is no source-backed fixed multiple in this grounding pack for an exact coverage amount. Anchor the decision to who depends on your income and your financial obligations, then review the plan with a qualified professional. Avoid one-size-fits-all targets.

Can self-employed workers qualify with irregular income?

Qualification standards vary by insurer, and approval is not guaranteed. Keep form usage accurate: Form 1099-LS relates to reportable life insurance policy sales, not standard freelancer income proof. For coverage and tax decisions tied to your policy, consult qualified professionals.

Is freelancer life insurance tax deductible?

Tax treatment can vary, so do not assume deductibility from general guidance alone. Confirm your setup with a qualified tax professional before filing or making planning decisions.

Is term life or whole life better for freelancers?

There is no universal winner. Term, whole, and universal products fit different budgets, coverage timelines, and flexibility needs. Choose based on obligations and timeline, not product labels.

What if I left a job and lost employer coverage?

Reassess needs as soon as employer-linked benefits end. Freelancers generally do not have the safety net of employer-sponsored life insurance, so plan for replacement coverage. Compare term, whole, and universal options based on budget, coverage length, and flexibility needs.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 4 external sources outside the trusted-domain allowlist.

- scc.virginia.gov/consumers/insurance/health-insurance-consume...trusted

- accuquote.com/life-insurance-for-freelancers-and-gig-workersexternal

- blog.freelancersunion.org/2025/02/28/life-insurance-101-for-freelancer...external

- empower.com/the-currency/money/difference-between-term-w...external

- vardeinsurance.com/education-center/life-insurance-for-freelanc...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Canada Digital Nomad Visa Planning for Visitor Status and Work Permits

The phrase `canada digital nomad visa` is useful for search, but misleading if you treat it like a legal category. It is shorthand for existing Canadian status options, mainly visitor status and work permit rules, not a standalone visa stream with its own fixed process. That difference is not just technical. It changes how you should plan the trip, describe your purpose at entry, and organize your records before you leave.

Build a Get-Paid Financial Architecture for Offshore Companies

If cashflow is unpredictable, one common issue is payment setup, not just a missing tool. Late payments, surprise holds, avoidable fees, and weak terms can pile up fast and force reactive decisions.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.