Quick Answer

Yes, many freelance IT consultants should carry liability insurance, especially Professional Liability (E&O), because client disputes can trigger legal defense costs even when you acted in good faith. The strongest approach is to map your real service risks first, then match policies, then compare quotes on exclusions and claims handling, not price alone. Add other coverages only when your operations justify them.

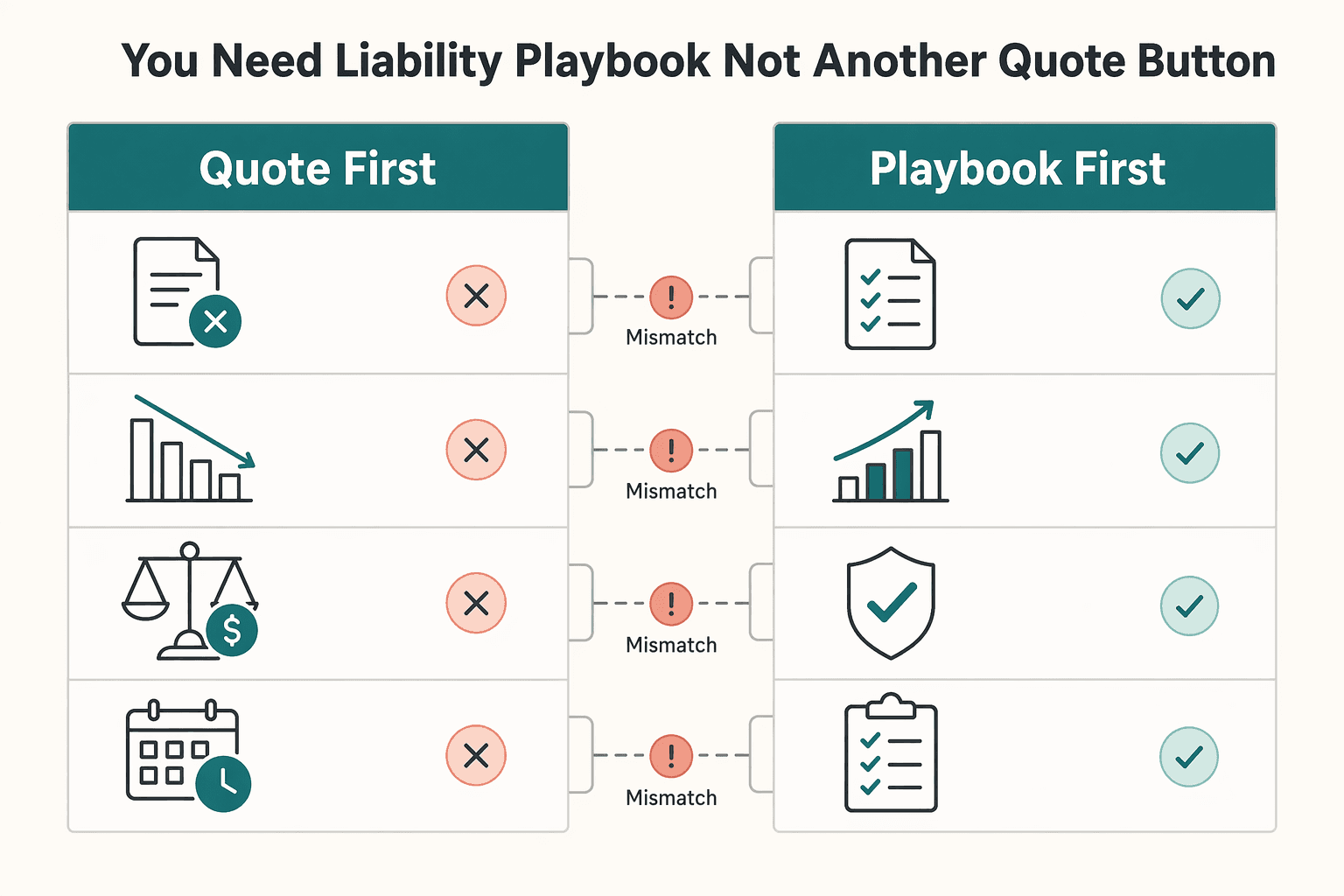

You Need a Liability Playbook Not Another Quote Button#

Treat your insurance decision like risk management, not online shopping. As an independent IT consultant, you can face a negligence allegation, a client financial-loss claim, and legal defense costs even when you delivered in good faith. One bad dispute can drain time, focus, and cash before anyone proves fault. If you run solo, you are the CEO of a business-of-one, and risk decisions are part of the job.

If you click quote buttons first, you compare prices before you define exposure. That sequence creates blind spots. A playbook flips the order. You map services, failure modes, and contract promises first. Then you evaluate relevant liability options with intent.

| Approach | What you do first | What usually goes wrong | Better outcome |

|---|---|---|---|

| Quote-first | Pick a policy by price and brand | You can overlook exclusions that conflict with your actual delivery work | Faster buying, weaker protection |

| Playbook-first | Map risks, then map policies, then compare quotes | You invest more effort upfront | Clearer coverage fit and cleaner decisions |

Run this first-pass framework before you buy:

- Risk scenarios: List where your work could trigger client loss, downtime, or dispute.

- Policy mapping: Match each scenario to likely coverage language where relevant in your market.

- Quote comparison: Compare multiple options on exclusions, defense handling, and claims process, not price alone.

- Verification: Confirm final coverage details with a licensed insurance professional before you bind.

Here is the pattern in practice. You recommend a system change, rollout issues interrupt the client workflow, and the client claims your advice caused loss. Even if you disagree, you still need a defense plan. That is the operating reality this article helps you manage.

Coverage language and requirements can vary by carrier, program, and jurisdiction. Use this framework to ask sharper questions, then confirm final details in writing with a licensed insurance professional before you bind coverage.

The Core Terms You Must Get Right Before You Buy#

Get the core terms right before you compare quotes, because each one protects a different loss pattern. You already have the right workflow: risk first, policy second, quotes last. This section translates that workflow into policy language so your insurance decision stays precise.

When you mix up terms, you usually buy the wrong protection. You often discover the gap only when a claim lands.

Use this coverage map before you request quotes#

| Term | What it covers | Where freelancers get confused |

|---|---|---|

| Professional Liability / Errors and Omissions (E&O) | Claims that your professional services caused a client financial loss | People treat these as different products when carriers often use different labels for the same core concept |

| Technology E&O (Tech E&O) | IT specific professional liability for technology service errors, omissions, or negligence tied to client financial loss | People assume standard E&O always includes tech specific language |

| Professional Indemnity | Market specific naming for professional liability style protection | People assume wording, triggers, and exclusions stay identical across countries and programs |

| General Liability | Third party bodily injury or property damage exposure | People expect it to handle professional service disputes |

| Cyber Liability | Cyberattack and data leak events | People assume cyber liability replaces E&O insurance for advisory mistakes |

| Business Owners Policy (BOP) | A package that combines general liability and commercial property elements | People buy it by default even when their operating model has minimal property exposure |

A quick scenario makes this real. If you deploy a configuration change, the client reports downtime, and the client alleges financial harm, that dispute usually points to Tech E&O or related professional indemnity wording. General Liability usually targets a different exposure family.

Apply a simple decision filter#

| If this applies | Coverage move |

|---|---|

| Clients rely on your recommendations or implementation | Prioritize E&O insurance language |

| Your delivery centers on technology systems and client financial-loss allegations | Add Tech E&O |

| You are evaluating General Liability and cyber liability | Treat them as separate tools in your risk management stack, not interchangeable options |

| Bundled liability plus property matches how you run the business | Use BOP only when it actually fits |

| You are ready to bind coverage | Confirm final policy wording, triggers, and exclusions for your jurisdiction |

In practice, start with your service risk, add Tech E&O when the work is technology-dependent, and treat General Liability, cyber liability, and BOP as separate choices rather than defaults. Before you bind, confirm the final wording, triggers, and exclusions for your jurisdiction.

Related: A Guide to Securely Wiping Your Devices Before Selling Them.

Do You Actually Need Liability Insurance as a Freelance IT Consultant?#

If clients rely on your recommendations, architecture, security setup, or implementation, treat Professional Liability (E&O) as your default starting point and evaluate Technology Errors and Omissions (Tech E&O) first. Once the terms are clear, the decision gets simpler. Look at your exposure, how dependent the client is on your judgment, and how painful legal defense costs would be if a dispute starts. Then add other policies only when your work actually creates that risk.

A financial-loss allegation can be devastating for a small IT consulting business. Even weak claims can still force legal defense spending and create serious disruption.

Run the yes/no gate#

| Exposure test | If yes | If no |

|---|---|---|

| Clients act on your technical advice or architecture decisions | Start with Professional Liability (E&O) or Errors and Omissions (E&O) | Keep it on your near-term roadmap before you sign higher-stakes work |

| You configure systems, ship implementations, or own technical outcomes | Prioritize Tech E&O as your first policy review | Reassess when delivery scope expands |

| A dispute could trigger legal fees you cannot comfortably absorb | Treat defense-cost protection as a primary buying reason | Reassess regularly as your exposure changes |

| You rely on a generic consulting insurance summary | Map your actual service risks first, then compare policy wording | Keep your current workflow and document why it still fits |

Keep one scenario in mind as you decide. A client can claim your guidance caused financial loss, and you still have to respond even if you believe your work met the brief. That is why risk management beats quote speed.

If you want a simple rule, use E&O insurance as the baseline when clients depend on your professional judgment, move Tech E&O to the front when technical delivery drives outcomes, and add other cover only after you confirm a real exposure. Before you bind, confirm wording and scope with a licensed broker or carrier.

Which Coverage Stack Is Essential and Which Is Situational?#

Start with Professional Liability (E&O) or Technology Errors and Omissions (Tech E&O), then add other policies only when your operations create that specific risk. At this point you are not asking, "What can I buy?" You are asking, "What does my delivery model actually expose me to?" The goal is a stack that matches your work, not a bundle that only looks complete on paper.

For many solo practices, the baseline starts with E&O insurance for client-facing professional service risk. If your work depends on system configuration, implementation, or technical recommendations, Tech E&O can be the better starting point because some products bundle professional liability with cyber coverage. Policy naming and wording can vary by carrier and jurisdiction, so confirm scope before you bind.

Essential and situational matrix#

| Policy | Treat as essential when | Treat as situational when | Decision note |

|---|---|---|---|

| Professional Liability (E&O) | Clients rely on your advice, architecture, or delivery outcomes | You do not yet carry client-facing responsibility | Professional-service liability layer |

| Technology E&O | You deliver technical implementation or high-dependency system work | Your work stays limited to lower-exposure advisory tasks | Some products combine professional liability and cyber elements, so verify scope |

| General Liability | You work onsite, interact with third parties, or handle client property | You operate fully remote with minimal physical interaction | This covers common third-party injury or property incidents |

| Cyber Liability | You touch sensitive data, security controls, or incident response workflows | You have limited data exposure and lower breach impact | Built for cyberattack and data-breach recovery costs |

| Business Owners Policy (BOP) | You own or lease business property and want bundled liability plus property coverage | You run lean with little property exposure | Packaging can simplify operations when assets justify it |

| Commercial Auto | You use a business-owned vehicle in delivery work | You do not use business-owned vehicles | Legal requirements can apply to business-owned vehicles, and coverage applies to accidents involving company vehicles |

Example: you work mostly remote, but you visit client sites for rollout days and carry business equipment. In that case, you might keep Tech E&O as your base. You might add General Liability for onsite exposure. You would evaluate BOP only if your property footprint actually grows.

Build your minimum viable stack#

- Map each service to one failure mode before you add a policy.

- Keep only policies tied to your current operations, then expand as scope changes.

- Review exclusions and claims reporting steps in writing with a licensed broker or carrier.

- Recheck the stack at renewal so your risk management stays aligned with how you actually deliver work.

How Do You Map Real Client Risks to the Right Policy?#

Map each client risk to a specific policy before you buy, then align contracts and records so coverage can respond when a dispute starts. You have the stack options. Now you need an operating map that ties real delivery scenarios to coverage lanes. That keeps your insurance decisions practical when a client relationship gets tense.

Build a simple scenario map#

Use your current services, not generic consulting insurance pages, and connect each scenario to one primary policy first.

| Client risk scenario | Primary policy match | Why this match works | What to confirm before binding |

|---|---|---|---|

| Implementation error causes client financial loss claim | Technology Errors and Omissions (Tech E&O) or Professional Liability (E&O) | This coverage addresses negligence or service error allegations tied to financial harm and defense costs | Confirm claim triggers, exclusions, and exact policy wording |

| Visitor injury or accidental third-party property damage during onsite work | General Liability | This policy targets third-party bodily injury and property damage exposure | Confirm onsite activities and third-party interactions fit declared operations |

| Theft or damage to business-owned equipment | Commercial Property | Liability policies do not primarily protect your own business property | Confirm covered property classes, locations, and loss conditions |

| Overpromised scope in SOW leads to delivery dispute | Tech E&O / E&O plus contract controls | Unclear terms and unrealistic promises can trigger E&O-style disputes | Confirm policy language matches the liability assumptions in your contract |

One delivery window can trigger multiple lanes. A client can claim your configuration caused operational loss (Tech E&O path) while a separate onsite incident triggers a General Liability path. Risk management means you prepare for both, not just the one that feels most likely.

Add contract and dispute readiness controls#

Policy selection alone does not close your exposure. Add a checkpoint before purchase and at each renewal:

| Control | What to keep or do |

|---|---|

| SOW alignment | Match SOW scope, deliverables, and liability assumptions to policy wording |

| Signed work records | Keep signed SOW versions, change logs, and approval trails in one folder |

| Incident file | Save incident timelines, remediation notes, and client communications as you work |

| Record review | Review records regularly so you can support a defense quickly if a negligence allegation appears |

Keep those records as you work, not after the dispute starts. A clean file makes it easier to respond quickly if a negligence allegation appears.

Run this mapping routine every time your services change. It keeps E&O insurance decisions grounded in real work, not brochure language.

Need a quick next step? Browse Gruv tools.

How Do You Compare Quotes Without Getting Trapped by Price?#

Use a structured scorecard to compare coverage quality first and premium second, then verify everything in writing before you buy. Once your risk map is clear, quote comparison gets cleaner. You are not shopping for "insurance." You are checking whether specific policies match specific risks, with pricing as a constraint, not the strategy.

Use a practical quote scorecard#

Compare multiple options side by side, and keep the coverage structure as similar as possible so your comparison stays fair.

| Scorecard item | What to check | Why it matters |

|---|---|---|

| Policy fit | Professional Liability (E&O/professional indemnity) and other coverage language relevant to your risks | You avoid paying for the wrong protection class |

| Limits and deductibles | Limits, deductibles, and out of pocket exposure | You measure real claim impact, not just monthly cost |

| Exclusions and endorsements | Service exclusions, contract assumptions, and added endorsements | Small wording gaps can break your risk management plan |

| Claims process quality | Reporting path, response expectations, and claim support | Claims handling quality affects outcomes when stress is high |

| Carrier and channel fit | Insureon, ERGO NEXT Insurance, Progressive Commercial, Embroker | These are channels, not universal winners, and terms and availability vary by state or program |

If one quote looks much cheaper, slow down and stress test the wording. The classic failure case is saving premium and later learning the policy narrows the exact implementation risk your clients depend on.

Treat Trustpilot and similar review platforms as context only. Customer reviews can help you spot service patterns, but they cannot replace policy wording review for E&O insurance or professional indemnity terms.

Keep the unknowns in view while you compare:

- You will not find a single universal premium benchmark you can rely on.

- You will not get a complete, apples-to-apples underwriting or claims performance study across every channel listed here.

- No single provider is best for every business model.

Run a safe verification step before binding#

| Verification step | What to confirm |

|---|---|

| Written quote review | Get the full written quote and policy wording, not a summary card |

| Licensed producer review | Review terms with a licensed producer (agent or broker) |

| License verification | Verify license status and good standing through state tools or NIPR workflows |

| Final written confirmation | Confirm final coverage specifics in writing with the carrier or licensed broker before you bind |

Do not bind from a summary card alone. Verify the full wording before you bind.

Your 30 Minute Implementation Checklist for 2026#

Start with Professional Liability (E&O), then add only the policies your actual delivery model justifies. If the earlier sections are your decision framework, this section is your execution routine. The goal is a clean, repeatable process you can run now and rerun at renewal without starting from scratch.

Build your minimum viable stack#

List every service you sell, then write one failure mode for each. If clients rely on your advice or implementation, treat E&O insurance as the baseline. Add the rest only when operations create that exposure.

| Policy | Add it when this is true | Keep it optional when this is true |

|---|---|---|

| Professional Liability (E&O) | Clients depend on your professional advice, architecture, or implementation | You do not provide professional services tied to client outcomes |

| General Liability | You face third party injury or property damage exposure through business operations | You have little or no physical interaction risk |

| Cyber Liability | You handle sensitive systems or need breach response support | You have minimal data and security exposure |

| Business Owners Policy (BOP) | You need business property protection and want bundled coverage | You have little or no business property to insure |

| Commercial Auto | You use company owned vehicles for delivery work | You do not use company owned vehicles for client delivery |

Example: an IT consultant handling cloud cutovers and occasional onsite troubleshooting might choose Professional Liability (E&O) first. They might add cyber liability for incident-related costs. They might add General Liability only for onsite exposure.

Execute verify and file#

- Collect comparable quotes and normalize limits and deductibles before you compare premium.

- Mark exclusions and endorsements line by line, then flag anything that conflicts with your scope.

- Confirm the claims reporting process in writing so you can act fast during a dispute.

- Capture renewal dates and pre-renewal tasks in your operating calendar now, not at expiry week.

- For work across jurisdictions, confirm local requirements and policy fit with a licensed broker or carrier before binding, since rules can vary by jurisdiction.

- Keep an audit-ready file with policy documents, endorsements, broker notes, and an annual review checkpoint so your decisions stay traceable as your business grows.

Build a Durable Risk System and Then Scale#

Scale safely by treating insurance as a system, not a one-time purchase. Define exposure, map it to coverage, then shop. It stays useful when you make it repeatable and update it as your services change.

For a solo IT consultant, start with your service reality, not generic templates. If your clients rely on your advice or implementation, keep Professional Liability (E&O) at the core of your plan. It is commonly referred to as E&O or professional liability.

Add General Liability for bodily injury, property damage, or personal injury exposures tied to operations. Add cyber liability when your work involves systems that could face data breaches or cyberattacks. If property risk matters, evaluate Commercial Property or a Business Owners Policy (BOP), which can bundle general liability with commercial property.

Run a simple review cadence#

- Keep a single-page decision log for each policy: why you bought it, what risk it covers, and what would trigger a change.

- Review your coverage annually, then run an off-cycle review whenever your client mix, scope, or delivery model changes.

- Re-shop with at least three comparable quotes when practical, and normalize limits and deductibles before you compare price.

- Confirm adjustments with a licensed insurance agent when your risk profile shifts.

A quick scenario shows how this works. You start with advisory architecture work, then begin hands-on system rollouts and incident-response retainers. You update your risk management file, revisit your E&O insurance and cyber liability terms, and document why each limit still fits.

Keep records that make growth defensible#

Treat documentation as part of operations, not admin overhead. Store policy forms, endorsements, quote comparisons, renewal decisions, and broker notes in one organized folder. Keep tax and insurance records long enough to substantiate reported items, and keep employment tax records for at least four years.

If you do need outside help, keep the process simple. Read the policy documents first. Then talk to a broker or carrier when you need confirmation on program availability and fit. Clarity beats speed. That is how your insurance strategy scales without surprises.

Frequently Asked Questions

Do I need professional liability insurance if I already use strong contracts?

Yes, in most cases. Strong contracts help define scope and reduce ambiguity, but they do not replace Professional Liability (E&O) when you need defense-cost support and payment of covered judgments up to policy limits. For a practical liability insurance IT consultant decision, treat contracts and insurance as two separate controls that work together.

What does IT consultant liability insurance usually cover in practice?

For an IT consultant, E&O commonly responds to allegations tied to professional mistakes, negligence, or issues in past-rendered services. It also commonly includes legal defense support for covered claims. Exact triggers and exclusions vary by policy wording, so read endorsements before you bind.

How are E&O, general liability, and cyber liability different for solo IT consultants?

Errors and Omissions (E&O), also called professional liability, focuses on losses tied to your professional services. General Liability addresses third-party bodily injury, property damage, and personal or advertising injury exposures. Tech E&O and cyber liability both address cyber risks, but from different angles. They are complementary, not interchangeable.

What policies are essential for a freelancer and what can wait?

Start with Professional Liability (E&O) or Technology Errors and Omissions (Tech E&O) for service-related risk. Add General Liability when contracts, leases, or on-site operations create that exposure. Add Cyber Liability when your work creates meaningful cyber risk exposure. Priorities can vary by jurisdiction and contract terms, so confirm requirements before binding.

How should I compare insurance quotes beyond price?

Force an apples-to-apples comparison first. Keep limits and deductibles aligned, then compare exclusions, endorsements, and claims reporting steps in writing. After that, evaluate price. This approach strengthens risk management and prevents a low premium from hiding weak coverage.

What factors typically influence IT consultant insurance cost?

Insurers commonly price from core inputs such as your profession, employee count, and coverage needs. Claims history also affects how underwriters view your risk profile. So cost changes when your delivery model, team shape, or prior claim experience changes.

Where do coverage requirements vary by country or program and how do I confirm safely?

Requirements and policy suitability vary by jurisdiction, and U.S. insurance regulation runs through a state-based system. Cross-border work can add complexity because terms and program availability may differ by country. Confirm requirements with a licensed broker or carrier in each relevant jurisdiction before binding.

Try a related tool

Kofi writes about professional risk from a pragmatic angle—contracts, coverage, and the decisions that reduce downside without slowing growth.

Priya specializes in international contract law for independent contractors. She ensures that the legal advice provided is accurate, actionable, and up-to-date with current regulations.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- insurance.maryland.gov/Consumer/Documents/publications/commercialin...trusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

- sba.gov/business-guide/launch-your-business/get-busi...trusted

- iii.org/article/professional-liability-insuranceexternal

- legalclarity.org/how-to-read-an-insurance-quote-limits-and-co...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Canada Digital Nomad Visa Planning for Visitor Status and Work Permits

The phrase `canada digital nomad visa` is useful for search, but misleading if you treat it like a legal category. In this draft, it is shorthand for existing Canadian status options, mainly visitor status and work permit rules, not a standalone visa stream with its own fixed process. That difference is not just technical. It changes how you should plan the trip, describe your purpose at entry, and organize your records before you leave.

Securely Wipe Devices Before Selling Them With Clear Risk Checks

Make one call before you touch the device: choose a wipe level that matches the risk, then document each step you complete. That keeps your decisions consistent when you are under pressure from a buyer, a trade-in deadline, or a handoff date.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.