Quick Answer

Start by locking ownership terms and operational control before coding begins. For ip protection outsourcing eastern europe, use a three-part sequence: verify partner records, sign assignment and confidentiality terms with clear authority, and keep admin control of repos, cloud roles, and credentials in your environment. Then run immediate offboarding steps at exit so access, code transfer, and documentation handover are provable rather than assumed.

The $100k Question Every Solo Founder Must Ask#

If you hire a developer in Eastern Europe, can you prove you own the code, keep control of access, and recover everything quickly if the relationship breaks down? That is the core risk in ip protection outsourcing eastern europe. In practice, it is often less about abstract theft and more about the practical mess where features get delivered, credentials live in a contractor's accounts, and the contract never clearly transfers ownership.

For a solo founder, that risk can feel bigger because there is no legal team or IT admin behind you. To protect yourself, lock down six basics from day one: IP ownership, assignment of inventions, confidentiality, governing law, repository control, and offboarding. Miss one, and you can end up arguing about title to code while also trying to regain access to your own product.

Start with plain language. In EU law, software is protected under copyright. Ownership transfer and permission to use are not the same thing. An IP assignment transfers ownership, while a license lets someone use IP without giving up title. Confidentiality helps protect trade secrets and business information, but it does not transfer ownership by itself. Choice of law matters too. Under the Rome I Regulation of 17 June 2008, parties can choose the law that applies to a contract, but that does not erase local enforcement differences across countries.

What you need to lock down#

| Control area | Action | Grounded detail |

|---|---|---|

| Ownership on paper | Say who owns new code and include an assignment of inventions | If the transfer terms are not explicit and properly documented, you are relying on assumptions |

| Control in the tools | Keep the master repository in your own GitHub organization or equivalent | Admin access lets you change roles or remove access |

| Recoverability at exit | Use least privilege, revoke repository, server, and tool access promptly, and confirm handover of code, credentials, and documentation | Treat termination as an account event |

- Ownership on paper

Your contract should say who owns new code and include an assignment of inventions. If the transfer terms are not explicit and properly documented, you are relying on assumptions.

- Control in the tools

Keep the master repository in your own GitHub organization or equivalent. Admin access lets you change roles or remove access, which is exactly what you need in a dispute or offboarding event.

- Recoverability at exit

Use least privilege from the start, then treat termination as an account event. Revoke repository, server, and tool access promptly, and confirm handover of code, credentials, and documentation.

That is the path this guide follows. Vet the partner, draft the contract correctly, then keep operational control every week, not just at signature.

Related: IP Protection for Software Developers: A Deep Dive into Copyright. If you want a quick next step, try the SOW generator.

Pillar 1: The Gatehouse - Vetting a Partner Before a Single Line of Code is Written#

Run a paper-trail check before you draft terms or share access. This will not prove IP ownership by itself, but it will quickly show whether the partner's legal and VAT narrative is consistent enough to proceed.

| Mechanism | What to capture | Article details |

|---|---|---|

| SME scheme | MSEST, EX-number status, and effective date | References a EUR 100,000 Union turnover ceiling and one quarterly report covering turnover across all 27 Member States |

| OSS | Member State of registration and whether regular VAT returns still apply | Registration is in one Member State for covered cross-border VAT declarations and payments, and OSS returns are additional to the regular VAT return |

| CBR | Filing country and whether one company filed for multiple parties | It is filed in a participating country where the requester is VAT-registered, and national VAT-ruling conditions apply |

Use this as your rule: VAT evidence is a first filter, not your full risk file.

- Validate source authenticity first.

If the partner sends you EU tax guidance, confirm the pages are on europa.eu. That is a concrete signal you are looking at an official EU institutional source, not copied or stale material.

- Map each VAT claim to a specific mechanism.

If they cite the cross-border SME scheme, ask for the exact elements: Member State of establishment (MSEST), EX-number status, and the date they say exemption can be used. The scheme references a EUR 100,000 Union turnover ceiling (current and previous calendar year) and one quarterly report covering turnover across all 27 Member States.

- Treat OSS and CBR statements as testable details, not labels.

If they claim OSS, the narrow point is that registration is in one Member State for covered cross-border VAT declarations and payments, and OSS returns are additional to the regular VAT return. If they mention a cross-border ruling, confirm they mean CBR and can explain where it was filed (participating country where the requester is VAT-registered) and that national VAT-ruling conditions apply; where multiple companies are involved, one files on behalf of the others.

| Screening signal | What it tells you | Decision |

|---|---|---|

Source links are on europa.eu, and mechanism names are specific | Basic authenticity and internal consistency | Proceed |

| SME-scheme claim includes MSEST, EX status, and effective date | Explanation is concrete enough to test | Proceed |

| Registration is "pending" with no clear status context | Needs follow-up; process target is up to 35 working days, but can take longer for anti-evasion/avoidance investigations | Pause |

| "OSS covers everything" with no clarity on regular VAT return | Material gap in VAT understanding | Pause |

| Vague "EU ruling" claims with no filing country or non-official links | Insufficiently reliable paper trail | Exit |

A small paid canary project can still be useful, but only after this paper trail is coherent from proposal through first invoice.

Use this gatehouse checklist before moving to contract drafting:

- Save the official EU pages they rely on and confirm

europa.eudomains. - Get a written statement of the VAT basis they are using (SME scheme, OSS, CBR, or none).

- For SME claims, capture MSEST, EX-number status, and effective date.

- For CBR claims, capture filing country and whether one company filed for multiple parties.

- Log any pending-registration timing issue, including where it exceeds 35 working days.

- Record that VAT checks are preliminary and do not replace your separate contract/IP authority verification.

We covered this in detail in How to Draft an NDA for a Software Development Project.

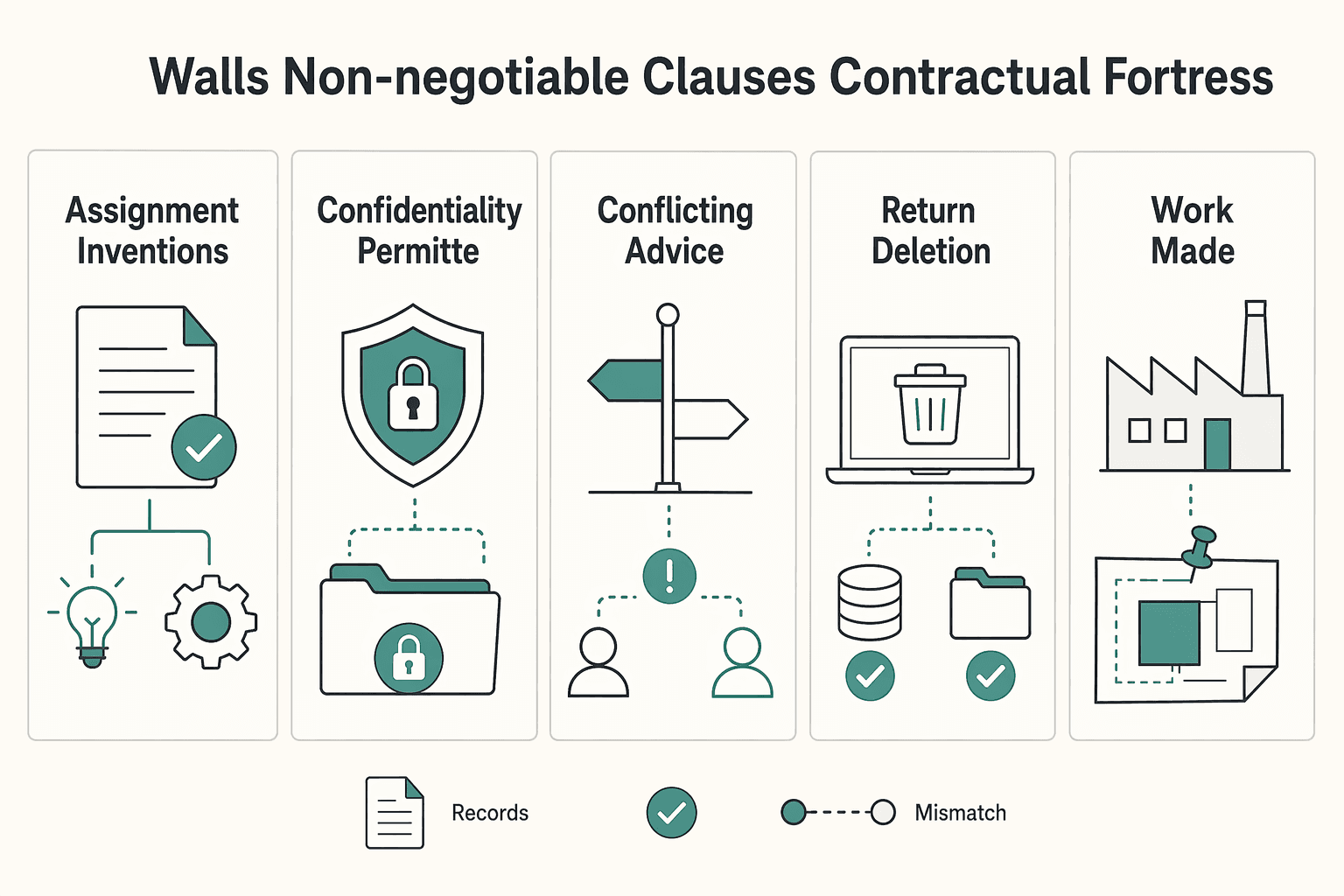

Pillar 2: The Walls - Non-Negotiable Clauses for Your Contractual Fortress#

Treat this as your contract baseline before meaningful work starts: no full repository access, no production credentials, and no major delivery until these clauses are signed by people who can actually transfer rights.

| Clause | What to include | Key point |

|---|---|---|

| Assignment of inventions | Use present assignment language, get signatures from the real rights holder or authorized agent, and add a further-assurances duty | A future promise like 'will assign' is weaker than present assignment language like 'hereby assigns' |

| Confidentiality and permitted use | Define covered information, limit use to performing your services, and require written flow-down terms for subcontractors | A generic NDA is not enough |

| Governing law, forum, and language of proceedings | Name governing law directly and specify the forum and the language of proceedings | EU judgment-enforcement assumptions do not automatically carry outside the EU |

| Return, deletion, and handover proof at exit | Require a certificate of deletion, a repository/account transfer checklist, usable handover materials, and a negotiated completion timeline | Do not assume a fixed 30-day window is legally required |

- Assignment of inventions

Put ownership transfer in present tense and get signatures from the real rights holder, or an authorized agent. A future promise like "will assign" is weaker than present assignment language like "hereby assigns," and that wording gap has surfaced in real ownership disputes, including Stanford v. Roche (June 6, 2011).

Use this drafting checklist:

- Present assignment language, not only a future promise.

- Further-assurances duty to sign follow-up papers when needed.

- Moral-rights waiver or consent where enforceable.

- Signature blocks for the actual creator or authorized agent.

If the vendor uses employees or subcontractors, require confirmation that downstream assignment obligations already exist and align with your contract.

| IP clause approach | Enforceability in cross-border contractor deals | Ownership clarity | Dispute risk |

|---|---|---|---|

| Work made for hire only | Weak outside narrow U.S. use cases | Often ambiguous | High |

| Future promise to assign | Better than nothing, but vulnerable | Delayed or contestable | Medium to high |

| Present assignment plus further assurances | Strongest contract position | Immediate, clearer transfer record | Lower |

Do not treat "work made for hire" as a universal shortcut. For a deeper comparison, see Work for Hire vs. Assignment of Rights: A Freelancer's Guide to Owning Your IP.

- Confidentiality and permitted use

A generic NDA is not enough. Define what is covered and how it can be used. Include the real categories you share: architecture, algorithms, training data, test data, customer lists, business plans, credentials, deployment scripts, tickets, recordings, and project communications. That aligns with trade-secret protection logic, which depends on secrecy-linked value plus reasonable protection steps.

Then set use limits clearly: the contractor can use confidential information only to perform your services, not for another client, internal reuse libraries, demos, or model training. If subcontractors are involved, require written flow-down terms. Where personal data is involved, mirror equivalent downstream duties by contract.

- Governing law, forum, and language of proceedings

Choose the dispute path deliberately instead of leaving it open. Name governing law directly. If both parties and likely assets are in the EU, an exclusive EU court clause can be practical because parallel proceedings may be stayed elsewhere in the EU and Member State judgments are recognized across Member States without a special procedure.

If enforcement may be needed outside that court network, arbitration may be the better route. The New York Convention has broad coverage (172 parties), and written, signed arbitration wording matters. In either path, specify the forum and the language of proceedings. Keep the core rule in mind: EU judgment-enforcement assumptions do not automatically carry outside the EU.

- Return, deletion, and handover proof at exit

Make exit obligations verifiable. Do not stop at "return or destroy." Require a certificate of deletion, a repository/account transfer checklist, and delivery of usable handover materials: source code, transfer-intended keys, build notes, issue logs, and access inventories. Where personal data is in scope, include return-or-delete duties and audit-verification rights.

Do not assume a fixed 30-day window is legally required. Set a negotiated completion timeline in the contract, document who owns each handover task, and track completion against the agreed deadline. A clause you can verify is safer than a promise you cannot test.

If you want a deeper dive, read A Freelancer's Guide to Canada's Anti-Spam Legislation (CASL).

Pillar 3: The Watchtower - Maintaining Day-to-Day Operational Control#

Signed contracts are not enough; day-to-day control comes from who owns accounts, permissions, and logs. The EU VAT sources for this article do not prescribe software repository or access controls, so use the system below as an internal governance standard, not a statutory rule.

| Operational area | Owner you should keep | Minimum vendor access | Verification check |

|---|---|---|---|

| Repository and workspace | Your company org or workspace | Repo or project role only, never org ownership | Confirm owner/admin list, branch protection on the default branch, and available audit history |

| Cloud environment | Your cloud account | Task-specific role, no root, no billing admin | Export IAM users/roles and review last sign-in activity |

| CI/CD | Your pipeline project | Project-level deploy or build rights only | Check who can edit pipelines, runners, and production deployment settings |

| Secrets and credentials | Your vault or approved secret store | Item-specific or vault-limited access only | Verify no secrets were sent in email, chat, or ticket text; log any exposure and rotate |

| Support and compliance tools | Your helpdesk, docs, billing, and tax workspace | Assigned queue, folder, or case access only | Export user list and confirm you control OSS, CBR, MSEST, EX number, and filing records |

Keep ownership where it matters#

Start with the repository operating model: client-owned org or workspace, role-based vendor access, pull requests into protected branches, and audit history enabled. Before each milestone, verify the owner and admin list yourself, and confirm the vendor cannot change ownership, weaken branch protection, or remove your access.

Most failures come from control drift, not a dramatic breach. Work starts in a vendor namespace "temporarily," credentials follow, and later you cannot prove what the source of truth is.

Apply least privilege across the whole stack#

Least privilege only works if you apply it across code, cloud, CI/CD, secrets, and support tools together. Run permission reviews at three points: joiner, mover, and leaver events. Then keep one dated export showing who had what access.

If a vendor touches finance or tax operations, keep those records in your environment. In the SME cross-border scheme, you file one prior notification in your Member State of establishment (MSEST), may receive an EX number, and file one single quarterly report covering turnover in all 27 Member States. If you use OSS, you register in one Member State of identification, and returns and payments move between authorities via a secure communications network.

Treat offboarding like containment#

When an engagement ends, treat offboarding like containment. Suspend accounts, remove group memberships, revoke repository and cloud access, disable CI/CD rights, rotate shared keys and tokens, and reassign open tickets and branches. Capture evidence the same day: member-list exports, IAM role exports, ticket ownership snapshots, audit-log extracts, rotated secret IDs, and the completed exit checklist.

Where your contract sets a handover deadline, track it operationally. If timing is still being finalized in templates, mark the deadline as pending operational approval instead of leaving a blank or assumed number.

For a step-by-step walkthrough, see A Biotech Consultant's Guide to IP Protection in Contracts.

Conclusion: Your IP is Your Business - Outsource with Confidence#

The practical takeaway is simple: cross-border outsourcing gets more predictable when you replace assumptions with checkpoints you can verify. These are VAT process controls, not legal conclusions on IP ownership. Focus on registration, reporting, and exclusion or offboarding checkpoints so transitions do not become operational surprises.

- Gatehouse

Before treating cross-border SME VAT exemption as active, verify that a prior notification was filed in the MSEST and that the EX number has been granted and confirmed. Timing matters: exemption starts only after the EX number is granted, and registration should generally finish within 35 working days, though it can take longer when authorities run additional anti-evasion checks.

- Walls

Keep the core compliance record set together: prior-notification details, EX-number confirmation, and filing evidence. If you need advance VAT clarity on a complex cross-border transaction, a CBR request is submitted in the participating EU country where the applicant is VAT-registered.

- Watchtower

If you use OSS, run ongoing reporting controls. All supplies covered by the chosen OSS scheme must be declared through the OSS return, filing frequency varies by scheme, quarterly for Union and non-Union and monthly for import, and a Member State can exclude a taxable person from OSS.

| Approach | Compliance clarity | Audit readiness | Operational risk |

|---|---|---|---|

| Assumption-based process | Unclear at key checkpoints | Weak when records are incomplete | Higher |

| Control-based process | Clear checkpoints and status | Stronger with complete filings and confirmations | Lower |

What you do next:

- Confirm whether prior notification in MSEST is complete.

- Treat exemption as active only after EX-number confirmation.

- Plan timelines around the 35 working day target, with buffer for investigations.

- If using OSS, declare all covered supplies and track scheme-specific filing cadence.

- Use CBR for complex cross-border VAT setups that need advance clarity.

Start with your current registration and reporting workflow, then check whether each checkpoint is documented and current. You might also find this useful: IP Protection in Eastern Europe With a Clear EU VAT Sequence.

Frequently Asked Questions

How do you handle ownership language in a cross border development contract?

Do not assume a clause by itself settles IP ownership transfer, invention assignment, or copyright ownership in Eastern Europe. Treat ownership effects as unresolved until country-specific legal review confirms required formalities and enforceability.

What should your NDA actually include?

Do not treat any NDA clause set, duration, survival period, or enforceability outcome as confirmed until legal review verifies it. Keep unverified NDA terms marked as pending legal review.

What is the minimum vetting checklist before you share real code or data?

Some contract-vetting specifics in this question may need separate review. If the vendor will handle EU VAT administration, keep records that are supported here: OSS scheme scope and returns, any CBR request submitted in the VAT-registration Member State, and SME cross-border documentation (prior notification in MSEST and EX number confirmation). OSS is optional, but if you choose it, all supplies under that scheme must be declared via the OSS return.

Is your home country contract enforceable in Eastern Europe?

Do not assume a home-country contract is enforceable in every Eastern European jurisdiction. Treat enforceability as unresolved until local legal review confirms the relevant jurisdiction and treaty details.

Should you rely on work for hire or assignment of rights?

For cross-border software outsourcing, do not assume work for hire or assignment of rights creates the same ownership result in every jurisdiction. Keep both as legal-review items until verified in each relevant jurisdiction. For background, see Work for Hire vs. Assignment of Rights: A Freelancer's Guide to Owning Your IP.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- copyright.gov/circs/circ30.pdftrusted

- copyright.gov/title17trusted

- csrc.nist.gov/CSRC/media/Projects/risk-management/800-53%2...trusted

- intellectual-property-helpdesk.ec.europa.eu/ip-management-and-resources/trade-secrets_entrusted

- law.cornell.edu/treaties/berne/6bis.htmltrusted

- law.cornell.edu/supct/html/09-1159.ZS.htmltrusted

- legislation.gov.uk/eur/2008/593/article/3trusted

- single-market-economy.ec.europa.eu/industry/strategy/intellectual-property/trad...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Work for Hire vs Assignment of Rights for Freelancers

A freelance agreement is not just about price and scope. It decides who controls the rights in the work. If the ownership language is loose, rights can move earlier than you expect, cutting down your control once the work is delivered or used.

A Freelancer's Guide to Canada's Anti-Spam Legislation (CASL)

Treat this article as a pre-send gate, not background reading. Use CASL as the baseline. If you are in Canada, or you send a Commercial Electronic Message to Canadian residents, the message is in scope. The same applies when a CEM is sent from or to computers or devices in Canada. This material treats messages routed only through Canadian systems as not subject to CASL, so flag those for separate review before you send.

IP Protection for Software Developers Using a Copyright-First Plan

Start with a copyright-first baseline, then add other protections where they reduce a specific risk. For small teams doing client work or shipping SaaS features, that makes software IP protection more usable in day-to-day operations.