Quick Answer

Separate contract rights from tax operations first. For ip protection eastern europe, decide ownership language and enforceability checks in one lane, then run OSS, CBR, or cross-border SME steps in a second lane with named owners. Do not treat invoices, VAT returns, or EX-number status as proof of title transfer. Sign only after governing law, forum terms, and your evidence chronology align across the main contract, annexes, and order forms.

Protect IP Without Disrupting Your EU VAT Sequence#

Treat VAT administration and IP ownership as separate lanes from day one. That is the core move in ip protection eastern europe: keep tax process moving without treating tax records as proof of who owns the work.

Here is the plain-language baseline:

- Ownership: who legally holds IP rights; assignment or transfer moves title, while licensing can allow use without transferring title.

- Enforceability: your practical ability to defend rights through legal remedies and courts.

- VAT administration: VAT registration, returns, payment, and record-keeping.

- OSS: an optional One Stop Shop route where you register in one Member State for covered cross-border supplies.

- CBR: an advance VAT ruling route for cross-border transactions between participating Member States.

- Cross-border SME route: the VAT-exemption access path that starts with prior notification in your Member State of establishment and can apply only after EX-number grant or confirmation.

The goal here is simple: separate proof of VAT process from proof of rights. Treat current thresholds and processing windows as pending official verification before anyone relies on them.

Use this quick decision flow:

- Decide whether VAT treatment needs advance clarification. If so, confirm whether CBR is available for your transaction before promising dates.

- Pick the filing route. OSS is optional, and the SME cross-border route has gatekeeping, including prior notification and EX-number confirmation.

- Assign owners and dependencies in a short decision log with owner, date, blocker, and next step.

| Evidence type | What it proves | What it does not prove |

|---|---|---|

| OSS registration, VAT returns, payment records | You followed a VAT process | That IP title transferred |

| SME prior notification and EX number | Access to that VAT route | That your client owns the work |

| Contract language on assignment or licensing | Rights transfer or permitted use | VAT compliance on its own |

If someone says, "the invoice shows we paid, so we own it," stop and fix the documents. Payment and VAT records matter, but they do not prove IP rights.

We covered this in detail in The legal difference between 'licensing' your IP and 'assigning' your IP.

Build the Mental Model Before You Draft Contracts#

Start with two lanes before the first redline: one for IP and contract rights, one for VAT administration. That separation keeps tax-process questions from turning into ownership disputes and keeps deals from stalling for the wrong reason.

In the rights lane, decide assignment versus licence, who grants rights, and when rights transfer. In the VAT lane, decide the filing path, owner, and timing assumptions for invoicing or launch. Keep them separate. OSS registration, a CBR request, or SME prior notification can affect billing and timing, but none of them transfers copyright.

Use three labels in redlines#

Put three internal labels at the top of the draft and triage every open point through them.

| Label | Use for | Example |

|---|---|---|

| Legal blocker | Issues that change ownership, use rights, or enforceability | Unclear assignment or licensing language |

| Admin blocker | Filing or timing dependencies that affect VAT treatment, billing dates, or rollout without changing ownership | CBR, OSS, or the cross-border SME route |

| Planning note | Visible but non-blocking assumptions until verified | Current thresholds, current processing windows, or route eligibility |

A legal blocker changes ownership, use rights, or enforceability. If assignment or licensing language is unclear, fix it before signature. If your team is still mixing terms, align first with Work for Hire vs. Assignment of Rights: A Freelancer's Guide to Owning Your IP.

An admin blocker covers filing or timing dependencies that affect VAT treatment, billing dates, or rollout without changing ownership. This includes CBR, OSS, and the cross-border SME route. CBR applies to transactions involving participating Member States. OSS is optional, and OSS returns are additional to domestic VAT returns. The cross-border SME route starts with one prior notification in the Member State of establishment and, if granted, a single EX number used across Member States.

A planning note stays visible but non-blocking until verified. Use it for unresolved assumptions such as current thresholds, current processing windows, or route eligibility.

Simple triage rule: if it changes title or permitted use, treat it as legal. If it changes filing steps or dates, treat it as admin. If it changes neither, park it as a planning note.

Turn the checklist into a decision table#

Once the labels are clear, keep one live table from first draft through signature.

| issue | owner | blocking status | next action | verification needed |

|---|---|---|---|---|

| Ownership label in scope and IP clause | Legal/commercial | Legal blocker if unclear | Decide assignment or licence and align contract language across deal docs | Confirm any local label, for example work for hire, is intended and valid for this deal |

| Complex cross-border VAT treatment | Finance/tax | Admin blocker if billing depends on it | Check whether CBR is available before promising dates | Confirm current participating-country scope |

| Cross-border SME route | Finance | Admin blocker if relying on SME access | File prior notification in the Member State of establishment and track EX-number grant or confirmation | Current threshold pending official verification; current processing window pending official verification |

| OSS route for B2C activity | Finance | Planning note or admin blocker, based on launch dependency | Decide whether to use OSS and map domestic return obligations separately | Confirm activity or customer profile fits current OSS rules |

| Launch date tied to filings | Commercial | Planning note until verified | Give a conditional date, not a fixed promise | Confirm whether current public timing targets apply and note delay risk |

Two operating rules cut rework. Verify the filing path before commercial dates show up in client emails. Keep a small evidence pack with the table: draft version, route note, filing owner, and assumption-check date.

Track timing that needs verification#

The usual failure is false certainty, not missing contract language. If timeline commitments depend on SME, OSS, or CBR steps, keep these unresolved fields in draft notes until official guidance is checked:

- Current threshold pending official verification

- Current processing window pending official verification

Close these fields only after a named owner checks live guidance. Keep route boundaries explicit: OSS is optional, CBR is not universal, and the EU SME route should not be assumed for a small enterprise outside the EU.

Use one short handoff script internally#

Clear handoffs keep the two-lane model alive in practice.

- Legal: "We are confirming assignment versus licence. Tax filings do not determine ownership."

- Finance: "We are confirming CBR, OSS, or SME steps, including prior notification and any EX-number dependency. These affect billing and timing, not ownership."

- Commercial: "Scope and price can move now; launch dates stay conditional until finance verifies the filing path."

If any team cannot state its lane that clearly, pause and reset before the next draft round.

What Is Automatic and What Needs Formal Filing#

After you split rights from VAT, split again: what is automatic and what depends on a filing. If you blur those categories, you create false confidence. VAT filings can look official but do not prove IP ownership, and contract wording can look final even when the right still depends on registration or local formalities.

This matters most when your deal includes transfer or exclusivity. Copyright protection in the EU starts automatically at creation, but licensing and usage still rely on national law, so keep these as separate checks: the right exists and the deal validly transfers or restricts it.

Classify each asset first#

Before redlines harden, run every in-scope asset through three checks: jurisdiction, status, and escalation. Use only these status labels: automatic, registration required, uncertain.

| Asset | Status | Key note |

|---|---|---|

| Copyright | Automatic | Run a jurisdiction check; if the deal assigns ownership or grants an exclusive licence, require local counsel confirmation |

| EU trade mark | Registration required | Do not draft as if rights are secured until registration status is confirmed |

| Patent (including the European patent route) | Registration required | The European route still includes post-grant country validation where protection is sought |

| Unregistered Community Design | Automatic from public disclosure | Do not treat it like a registered design right |

| Trade secrets | Uncertain | Confirm secrecy and protective steps |

- Copyright: usually

automaticat creation. Still run a jurisdiction check. If the deal assigns ownership or grants an exclusive licence, require local counsel confirmation. - EU trade mark:

registration required. Do not draft as if rights are secured until registration status is confirmed. - Patent (including the European patent route):

registration required. The European route still includes post-grant country validation where protection is sought. If the deal depends on patent ownership, licensing, or post-grant recordal, require local confirmation because national requirements can apply. - Unregistered Community Design and trade secrets: UCD can be

automaticfrom public disclosure, but do not treat it like a registered design right. Treat trade secrets asuncertainuntil you confirm secrecy and protective steps.

Operator check: for each asset, identify the document that proves the right exists and the document that proves transfer or exclusivity. If those differ, keep both.

Map the VAT path separately#

Once the asset status is clear, record one VAT route in writing before signature, even if it is none.

| pathway | when to use | required filing action | owner | contract dependency |

|---|---|---|---|---|

| CBR | Complex cross-border VAT treatment where advance clarification is needed | File a cross-border VAT ruling request where available under national conditions | Finance/tax | Admin blocker if pricing, invoicing, or launch timing depends on the outcome |

| Cross-border SME route | Small enterprise using the cross-border SME VAT exemption (from 1 January 2025) | File one prior notification in the Member State of establishment; if granted, use the EX number in each EU country | Finance | Admin blocker when SME treatment is required; confirm eligibility (including the EUR 100 000 Union turnover ceiling) and processing timeline for the specific case |

| OSS | Covered cross-border B2C supplies where one portal is useful | Register once, then file one OSS return and make one payment through the portal | Finance | Planning note or admin blocker depending on billing model; OSS is optional, OSS returns are additional to domestic VAT returns, and filing and payment follow the end of the following month deadline |

| None | No special route needed, or normal VAT arrangements chosen | No CBR request, no SME route, no OSS | Finance | Record the decision so nobody assumes a filing is pending |

Keep two warnings explicit: CBR availability depends on national conditions, and OSS recordkeeping can run up to 10 years.

Require written status before signature#

For every in-scope IP right and VAT pathway, require one written status: pending, confirmed, or blocked.

If a business-critical right or VAT path is still pending, treat unconditional delivery or launch promises as premature.

Keep proof of right separate from proof of process#

To keep the next steps clean, run two calendars: one for legal-right confirmation and one for VAT-process completion.

Use one explicit checklist split:

proof of right: signed assignment or licence terms, registration details where required, confidentiality controls where trade secrets matter.proof of process: prior notification records, EX number confirmation, OSS registration, return timestamps, payment records.

Do not let proof of process stand in for proof of right. That separation turns country variation into a verification task instead of a late-stage dispute.

Handle Country Variation Without Stalling Deals#

Treat country variation as a routing task, not a deal stopper. Map countries before scope, exclusivity, and launch dates are locked so you can adjust legal language without reopening commercial terms.

In Eastern Europe deals, a common failure mode is assuming one EU answer covers every country in the chain. IP is territorial, so the exploitation country can matter as much as the signing country.

Use one intake matrix for every cross-border deal#

Use a four-country lens that assigns risk, owner, and the legal check still required.

| matrix field | what you record | main risk | owner | required legal check |

|---|---|---|---|---|

| client entity | contracting party country and legal entity | wrong assumptions about who can receive rights, invoice, or claim under the contract | Legal or deal lead | confirm entity details, governing-law fit, and whether EU process routes are available |

| performance | where services are actually performed | local legal or compliance variation that can affect delivery and records | Operations with legal support | confirm whether local execution issues need review |

| exploitation | where deliverables are used, sold, licensed, or enforced | territorial IP gaps, especially when use extends beyond EU coverage | IP counsel or external local counsel | confirm coverage, transfer validity, registration scope, and enforceability in each use country |

| dispute venue | chosen court, arbitration seat, or likely forum | clause mismatch and enforcement surprises | Legal | confirm jurisdiction clause, conflict-of-laws position, and venue-specific enforceability |

Checkpoint: if exploitation and client-entity countries differ, do not treat the signing country as your only legal check.

Branch early when EU coverage ends#

If any in-scope country falls outside EU process coverage, mark EU assumptions as limited and open a separate local-enforceability track immediately.

Keep the boundary explicit: OSS is EU-only for cross-border VAT obligations, CBR depends on participating Member States, and the cross-border SME path is an EU mechanism using an EX number in EU countries. Those process routes do not prove non-EU coverage.

Apply the same boundary to IP. An EU trade mark covers the 27 EU Member States through one registration, and a Unitary Patent covers participating EU Member States only. If contract wording says "exclusive rights in Europe," verify that wording against actual country coverage before signature.

Keep EU process details pending verification#

Where EU routes apply, keep unresolved fields in the matrix instead of hardcoding memory-based numbers:

- CBR availability: current participating-state coverage pending official verification

- Cross-border SME threshold: current threshold pending official verification

Start from the published EU reference point, then verify current country-level conditions.

- Cross-border SME timing: current process timing pending official verification

Published guidance cites a standard-case timeline, but verify against current official pages.

- OSS status:

Optional route, EU-only scope confirmed, registration or return owner assigned

This prevents launch planning from relying on outdated assumptions.

Give the map one owner#

Assign one country-map owner per deal so assumption changes and contract language stay aligned with the countries actually in scope. That owner should keep territory, licence, and subcontracting language synchronized with the matrix, especially for white-label or multi-market delivery. Use the same working file for your territory drafting notes and How to Structure a 'White Label' Service Agreement.

Done properly, this reduces the late-stage failure risk where the contract is signed and invoicing-ready but only partly enforceable where you need it.

Related: IP Protection When Outsourcing Software Development to Eastern Europe.

Choose Ownership Structure That Matches the Engagement#

Choose your ownership model based on how the work is delivered, then validate it locally before signing. In cross-border deals, assignment, license, and work made for hire are drafting positions that can work differently by jurisdiction.

Use the terms narrowly:

- Assignment: transfer of IP ownership to another person or legal entity.

- License: permission for the client to use IP while you keep ownership.

- Work made for hire: a U.S. copyright concept with specific statutory conditions, so treat it as jurisdiction-specific language pending local confirmation.

That local check matters because some countries require formalities such as written form or registration before ownership language is fully effective.

Pick the starting posture that fits the delivery pattern#

| delivery pattern | client reuse expectation | your need to retain background IP | practical starting model | drafting note |

|---|---|---|---|---|

| one-off custom deliverable created mainly for this client | client expects to own and reuse the final output without asking again | low | assignment | Use only when you intend a full transfer of final-deliverable rights. |

| recurring service using your templates, methods, code snippets, datasets, or know-how | client needs use rights, not your full toolkit | high | license | Put scope, term, territory, and field of use in one controlling clause set. |

| white-label delivery where the client brands the output as its own, but you rely on pre-existing materials | client needs broad use of the deliverable, sometimes for onward supply | high | split model: transfer or broad license of foreground deliverables, retention of background IP | Separate newly created deliverables from pre-existing materials. |

| U.S.-linked copyright arrangement where a party insists on work-for-hire wording | client wants first-instance ownership language | varies | work made for hire drafting position, pending local confirmation | Do not assume this wording applies cleanly outside jurisdiction-specific rules. |

Quick rule: if the value is the finished output, assignment can fit. If the value is your reusable method, a license usually fits better. If both matter, split ownership explicitly instead of using vague "all materials" language.

Draft white-label clauses as two buckets, not one#

For white-label work, separate the contract into two buckets: foreground deliverables created under this engagement and background IP made up of data, know-how, information, and other materials you held before signing and need to perform or exploit the work.

Document background IP in writing before signature, ideally in a schedule listing pre-existing materials and related access rights. Keep all limits for that background IP in one controlling clause set: scope, term, territory, and, where needed, field of use. This avoids conflicts where one clause grants broad use and another narrows use to a specific project.

If outputs are jointly generated and inseparable, use written joint-ownership terms instead of forcing sole ownership. For deeper white-label structures, see How to Structure a 'White Label' Service Agreement.

Keep VAT in a separate lane. VAT chargeability and invoicing can affect timing, and EU invoicing rules apply to most B2B supplies, but VAT workflow does not decide IP title. If compliance could affect deal timing or billing, track current thresholds and process timing as pending official verification before relying on them.

Run this pre-sign ownership check#

Before signing, confirm these five points:

- What transfers: exact deliverables or rights being assigned or licensed.

- What stays with you: all listed background IP and pre-existing materials.

- What use is limited: scope, term, territory, and field of use in one controlling clause set.

- What local law status is: any written-form, registration, or jurisdiction-specific confirmation still required.

- What timing dependency exists: any VAT or invoicing step that could affect deal timing or billing, tracked separately from ownership.

Use a Pre-Sign Contract Checklist for IP Clauses#

Treat signature as a control gate. You should sign only after two lanes are cleared separately: IP-clause readiness and VAT-process readiness. They connect on timing, but they are not the same decision. VAT process can affect operational timing, but it does not change whether the draft is an assignment, a license, or a split model.

Run one live checklist with five required fields#

Keep one checklist artifact in the deal folder and use it during the pre-sign call. Each line should include:

- Item

- Owner

- Status

- Dependency

- Evidence note

For the IP lane, track at least these items: ownership model confirmed in draft, written-form check completed, country-specific registration check flagged where relevant, confidentiality protection in place for pre-sign disclosures, and annex consistency confirmed. If a deal mixes pre-existing and newly created IP, keep that separation explicit in the checklist itself. If you need deeper clause separation, see How to Structure a 'White Label' Service Agreement.

Write evidence notes so someone outside the call can verify closure, for example an accepted redline version, counsel confirmation on formality, or a schedule listing pre-existing materials. Avoid vague notes like "discussed." Where country formalities are still uncertain, escalate to legal review before signature.

Keep VAT readiness explicit and separate#

Track VAT in the same packet only when it can move signature, launch, or billing dates. If OSS is in scope, assign owners for registration, filing, and payment. OSS is optional. If you use a scheme, supplies under that scheme must be declared through OSS, and OSS returns are additional to domestic VAT returns.

Where details are not yet verified, keep unresolved fields in the checklist instead of fixed numbers:

- Current threshold pending official verification

- Current filing window pending official verification

- Member State of identification pending tax review

If billing assumptions depend on OSS choices, log that dependency explicitly.

| status | what it means operationally | action before signature |

|---|---|---|

| complete | Agreed, owner accepts it, and evidence is in file | Signature may proceed on this item |

| pending with condition | Not fully closed, but condition is specific and accepted | Add condition to signing approval and assign named owner |

| blocker | Impacts ownership terms, authority, or launch or billing timing materially | Do not sign until resolved or redrafted |

Version-lock before approval#

Before approval, lock the exact contract version, annex version, and checklist version that cleared review. If contract text, annexes, or VAT assumptions change, rerun the checklist before signing.

Rerun immediately if the ownership model changes, country-specific formality assumptions change, or OSS assumptions are introduced or revised. This is how you catch late edits that quietly change execution risk before signature.

Related reading: Creative Commons for Freelancers Without Client Contract Conflicts.

Before you send the draft, generate a clean first-pass agreement and redline only the jurisdiction-specific clauses that need counsel review: Use the freelance contract generator.

Set Governing Law, Jurisdiction, and Dispute Resolution Up Front#

Set venue terms as one clause package before signature. In cross-border Eastern Europe work, splitting these terms across documents or leaving them half-defined can create avoidable enforcement risk.

Define the three terms before you negotiate#

Governing Law is the legal system that governs your contract obligations. Under Rome I, you can choose it, but the choice should be explicit or clearly inferable from the contract and circumstances.

Jurisdiction is the court forum. Under Brussels I (recast), if you agree on a Member State court for disputes tied to the contract, that chosen court has jurisdiction.

Dispute Resolution is the route: court litigation or arbitration. If you choose arbitration, use a written arbitration agreement, and treat it as a different path from court jurisdiction, not a fallback copy.

Choose the route both sides can execute, then draft procedure in the same package#

Pick one forum path both sides can actually execute in practice, then lock the procedure with it: notice channel, response timing, cure steps, and evidence handling. That matters because Rome I does not govern evidence and procedure, so you need those logistics in your own drafting.

If you choose arbitration, confirm the agreement is in writing and check enforcement logic under the New York Convention. If you choose an exclusive court clause in a cross-border deal, confirm treaty coverage and current contracting-party status before relying on enforcement assumptions. The Hague Choice of Court Convention is relevant only to exclusive choice-of-court agreements in international civil or commercial matters.

Check hierarchy across the full deal set before sign-off#

| Document | What to verify | Typical conflict to remove |

|---|---|---|

| Main terms | Governing Law, forum path, notice, cure, and evidence steps | Main terms select one court path |

| Annexes/schedules | Repeated or conflicting dispute text | Annex inserts arbitration or a different notice method |

| Order forms/SOWs | Short-form legal language and local procurement terms | Order form points to a different court or silent override text |

If anything conflicts, add explicit precedence language so one document controls.

Keep VAT operational in this section, not as ownership evidence. OSS and VIES are compliance tools: OSS returns are additional and do not replace domestic VAT returns, and VIES is a validation search tool for VAT registration status. OSS record-retention runs for 10 years, so define who keeps records and where. Treat jurisdiction-specific thresholds and filing windows as pending official verification before they are used in approvals or filing calendars.

Before legal review, run this pre-sign check:

- One controlling venue path only: court or arbitration.

- No competing forum language across main terms, annexes, and order forms.

- Notice, cure, and evidence steps are explicit, not implied.

- Red flag test: if you cannot name who keeps records, where notice is sent, and what evidence is preserved, pause signature.

Write Risk Allocation Clauses That Actually Protect You#

Draft Limitation of Liability, Indemnification, and Termination as one package. Together they determine whether you can actually run a claim response or a clean exit. If you review them in isolation, you can miss the real gap: a claim is recognized, but control, payment exposure, or post-termination rights are unclear. VAT process matters for context, but it does not determine contract-specific liability, indemnity, or termination outcomes.

The practical test is simple: if a dispute or exit starts tomorrow, can you identify who acts, who pays, what approvals are required, and what survives termination?

Tighten definitions before debating numbers#

For limitation of liability, make the clause state cap scope, exclusions, and cap mechanics. If it is unclear whether the cap is aggregate or per claim, your exposure is unclear. Check main terms, SOWs, and order forms for conflicting cap language.

For indemnification, lock the mechanics, not just broad promises. State the notice path, claim-response control, cooperation duties, and settlement-consent rules. Without that process, disputes over control and deadlines can escalate quickly.

For termination, define what happens on the termination date to licenses, deliverables, source files, access credentials, and unpaid amounts. If rights depend on payment, acceptance, or a separate assignment step, state that in the same package. If you need more ownership-structure context before drafting survival language, see Work for Hire vs. Assignment of Rights: A Freelancer's Guide to Owning Your IP.

| Clause | Balanced drafting | Risky drafting | Quick decision test |

|---|---|---|---|

| Limitation of Liability | Defines scope, exclusions, and whether the cap is aggregate or per claim | States a cap only, or leaves cap mechanics unclear | Can you calculate likely exposure from one read, without assumptions? |

| Indemnification | Names notice path, response control, cooperation duty, and settlement consent | Promises indemnity but does not define who runs the response | If a claim arrives today, can one person run the clause step by step? |

| Termination | States post-exit treatment of rights, files, access, and unpaid amounts | Ends the contract but leaves post-exit rights and obligations unclear | On exit day, can you tell what each side must stop, deliver, or pay? |

Use this as an execution test for real claim handling. If the package cannot be executed, it is not ready.

Keep VAT in its lane#

Keep VAT process as operational context, not contract risk allocation. OSS is optional and works through one Member State of identification. If you choose an OSS scheme, declare all supplies covered by that scheme via the OSS return. OSS returns are additional to regular VAT returns. EU OSS materials also reference record-keeping, invoices, and bad-debt-relief rules.

Keep VAT thresholds and filing windows in working notes as pending official verification. Do not treat OSS status, invoice status, or VAT filings as proof of ownership, indemnity scope, or termination rights.

Pre-approval check#

Before approval, confirm all of the following in one document set:

Limitation of Liabilityscope, exclusions, and cap mechanics align across main terms, SOWs, and order forms.Indemnificationnotice path, response control, cooperation duties, and settlement consent are stated consistently.Terminationlanguage matches ownership and license structure, including source files, deliverables, access, and unpaid amounts.- Your evidence pack is ready, for example acceptance records, delivery logs, invoice records, and written approvals.

- Nothing in this package conflicts with governing law, jurisdiction, or dispute-resolution terms.

If you cannot answer these checks from signed documents and current records, pause before signature.

Prepare an Evidence Pack Before Any IP Infringement Fight#

Build your evidence pack before any dispute starts, and keep the core pack limited to dated, transaction-linked records you can retrieve fast. For cross-border Eastern Europe work, that is a practical way to protect your position without slowing operations.

Assume the rights holder will need to drive enforcement, and do not rely on registration alone. Copyright protection starts when the work is created, so your core proof usually starts with the creation trail, authorship records, and signed contract terms, with delivery history, invoices, payment records, and acceptance records supporting the timeline. Optional registration can support timing, but it should not replace the pack.

Build the file around dated events#

Use a chronology-first index so a reviewer can follow the transaction without guesswork: what you agreed, created, delivered, invoiced, collected, accepted, and filed. If a point needs a long memo to explain it, you probably need a better underlying record.

Use an artifact matrix at the top of the pack so legal, finance, and operations can all follow the same map.

| Artifact type | Owner | Date | Linked transaction stage | Storage location |

|---|---|---|---|---|

| Signed master agreement, SOW, order form, NDA | You or both parties | Execution date and amendment dates | Agreement and scope definition | Contracts folder, signed PDF repository |

| Creation record (draft file, source file, export, commit snapshot, dated version) | You or creator | Creation and revision dates | Authorship and work existence | Project archive, version history, source repository |

| Delivery and acceptance record (submission email, upload log, acceptance message, approval note) | You and client | Delivery date and acceptance date | Delivery and acceptance | Client communications folder, project platform export |

| Invoice and payment confirmation | You, payment provider, bank | Invoice date and payment date | Commercial performance and consideration | Accounting folder, bank export, payment processor |

| VAT or filing context record (OSS record, return support, optional registration receipt) | You or filing agent | Filing date or transaction date | Compliance context and timing | Tax folder, filing portal export |

Keep names and paths consistent between the table and stored files. If they do not match, review speed and confidence drop fast.

Keep VAT and filing records in the context lane#

Include VAT and filing records as context, not ownership proof. OSS records are for tax verification and transaction-level VAT details, so they help with chronology but do not prove authorship or assignment by themselves.

When ownership is challenged, your strongest records are still creation history plus signed rights language. VAT returns, OSS records, and invoices support the timeline around the work.

Where compliance assumptions are needed, log current thresholds and filing deadlines as pending official verification instead of stale numbers. If records span periods before and after 1 July 2021, label them clearly. If OSS records are included, keep them for 10 years from the end of the transaction year.

Be strict about what belongs in the core pack#

Only keep records in the core pack if they are dated, source-identifiable, and linked to a transaction stage. Move unlinked screenshots, commentary, and opinion notes to a non-core appendix.

This is an operational point, not a theoretical one. Admissibility depends on forum, but noisy files slow review and raise reliability questions when capture source or timing is unclear.

Track key records you do not control in a separate request sheet. Courts can order the other side to produce evidence in its control, so flag external items early.

Assign one custodian and test the handoff#

Assign one evidence custodian to own the top-level index, path accuracy, preservation, and archiving discipline. That role supports legal review by keeping the file reliable and retrievable during active work.

Run one handoff test: give the index to someone outside the deal and ask them to trace a transaction from signed agreement to payment and acceptance using only listed paths. If they cannot do it cleanly, the pack is not ready. Once it passes, move to Execute in Order With a 30-Day Protection Checklist.

This pairs well with our guide on AI Content Copyright Issues in Client Work Contracts.

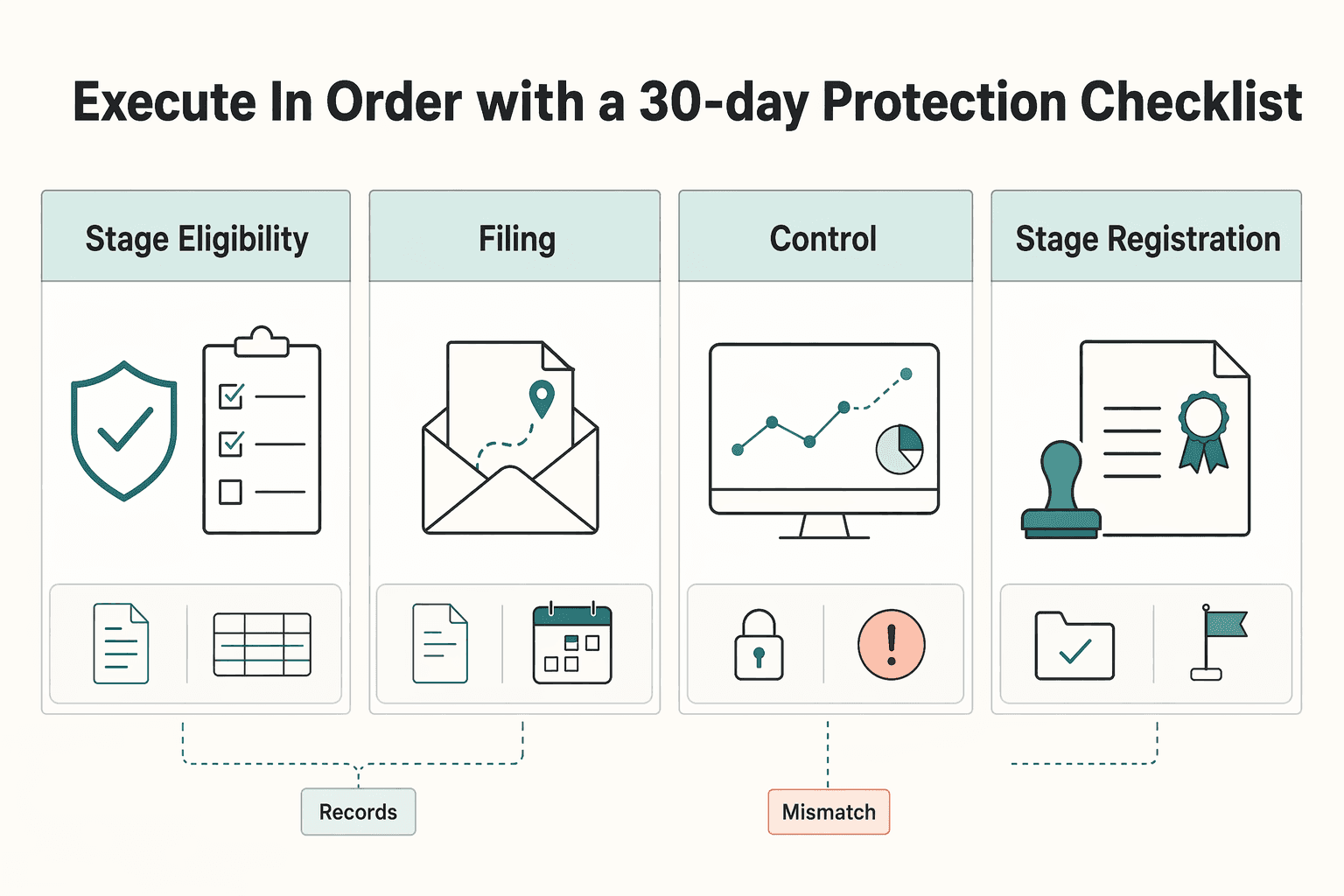

Execute in Order With a 30-Day Protection Checklist#

Use this as a review cadence, not a delivery promise. Work in dependency order: eligibility confirmation, notification filing, status tracking, then registration and closeout.

| Stage | Main action | Control point |

|---|---|---|

| Stage 1: Eligibility confirmation | Record the Member State of establishment, each target Member State, whether the cross-border SME path is available, and who owns each filing action | Confirm eligibility against the EUR 100,000 EU-wide turnover cap and the relevant national threshold in each Member State (up to EUR 85,000); use the published 35 working days registration target as planning input |

| Stage 2: Prior notification filing | File one prior notification through the MSEST and log submission proof, filing owner, submission date, and storage path | Do not treat filing as approval; apply VAT-exempt treatment in selected Member States only after the EX number is granted and confirmed |

| Stage 3: Status tracking and control gate | Update owners, blockers, and decision logs without merging steps if anything slips | A reviewer should be able to trace eligibility, prior notification, EX number status or OSS registration, billing, payment, and acceptance records without gaps |

| Stage 4: Registration and closeout | Where OSS applies, complete registration and archive registration confirmation, invoices, payment records, and acceptance records together | Keep OSS records detailed enough for return checks for up to 10 years |

Stage 1: Eligibility confirmation#

Start with a live decision log, not a calendar. Record your Member State of establishment, each target Member State, whether the cross-border SME path is available, and who owns each filing action. Confirm eligibility against the EU-wide turnover cap (EUR 100,000) and the relevant national threshold in each Member State (up to EUR 85,000). For timing, use the published 35 working days registration target as planning input, and note that specific investigation cases can take longer.

Keep jurisdiction fit in view while you do this. Patent protection is territorial by country, and copyright starts at creation, so your contract terms and evidence trail still need to align with where and how you operate.

Stage 2: Prior notification filing#

If you are using the cross-border SME route, file one prior notification through your MSEST. Log submission proof, filing owner, submission date, and storage path in the same evidence index.

Do not treat filing as approval. You can apply VAT-exempt treatment in selected Member States only after your MSEST grants the EX number and confirms it can be used.

Stage 3: Status tracking and control gate#

Track status as its own stage. If anything slips, move the schedule but do not merge steps. Update owners, blockers, and decision logs so accountability and evidence continuity stay intact.

Before you proceed, run a file-walk check. A reviewer should be able to trace eligibility, prior notification, EX number status or OSS registration, billing, payment, and acceptance records without gaps.

Stage 4: Registration and closeout#

Where OSS applies, complete registration only after upstream status supports it. Then archive registration confirmation, invoices, payment records, and acceptance records together, and keep OSS records detailed enough for return checks for up to 10 years.

If the reviewer cannot follow the file end to end, you are not at closeout. Shift the date, fix the record, and keep the sequence intact.

Conclusion#

Use this sequence on cross-border deals where EU VAT administration is relevant: classify -> contract ownership terms -> VAT path -> verify locally -> archive evidence. That keeps VAT administration separate from the contract decisions that control rights.

- Classify the issue first: ownership transfer, license scope, pre-existing materials, reuse rights, or VAT administration only.

- Lock ownership intent in contract language, then confirm locally that your chosen model works under the governing law. For ownership structure choices, use Work for Hire vs. Assignment of Rights: A Freelancer's Guide to Owning Your IP. If you are delivering under another brand, align drafting with How to Structure a 'White Label' Service Agreement.

- Choose the VAT path separately:

OSS(One Stop Shop) is an optional EU VAT system where you register in one Member State of identification and use that portal for covered cross-border VAT declarations and payments. If you opt in, you must declare all supplies covered by that scheme through OSS, and OSS returns are additional to your regular VAT return. -CBR(VAT Cross Border Rulings) is an EU mechanism for advance rulings on VAT treatment for complex cross-border transactions in participating EU countries. The request is filed in the participating EU country where you are VAT-registered, and if multiple companies are involved, one company submits on behalf of the others.

- Verify locally before launch: VAT process choices do not decide IP ownership, reuse rights, or contract enforceability outcomes.

- Archive one dated evidence trail across signed terms, invoices, approvals, delivery, payments, and VAT records.

Final check: if those records do not tell the same chronology, resolve that gap before work starts.

If you want one operational flow for invoicing, payment tracking, and compliance-gated payouts while you manage cross-border client work, check fit here: Gruv for freelancers.

Frequently Asked Questions

What IP protection is automatic in Eastern Europe, and when is automatic protection not enough?

Treat automatic protection as jurisdiction-specific, and confirm local law plus signed contract terms for the specific country, asset type, and parties before relying on it alone.

Is one EU approach enough, or do I need country specific steps for Ukraine, Georgia, or the Western Balkans?

OSS and CBR can help with EU VAT administration, but they do not determine IP ownership terms. Tag each assumption as either EU VAT or local contract/IP law, and get country-specific validation where needed.

How do I choose between assignment of rights, work for hire, and a licensing contract for client work?

This grounding pack does not define assignment, work for hire, or license, and their legal effect is jurisdiction-specific. Choose business intent first, then confirm how each term works under the governing law before signing. | Model label in draft | What this source set can confirm | Local counsel must confirm | |---|---|---| | Assignment | Not defined here | Meaning, validity, formalities, and timing in the chosen jurisdiction | | Work for hire | Not defined here | Whether recognized and how qualification works for your facts | | License | Not defined here | Scope, restrictions, and enforceability under local law |

Do I need formal registration for every project, or only for assets like trademark, patent, or industrial design?

Do not assume “file everything” or “file nothing.” This source set does not provide one universal registration rule across all assets and countries, so decide per asset and jurisdiction. Keep VAT administration records separate from title and ownership records.

What should be non negotiable in governing law, jurisdiction, and dispute resolution clauses?

At minimum, keep governing-law, jurisdiction, and dispute-resolution clauses consistent across your contract stack and get jurisdiction-specific legal validation before signing.

What is the minimum contract stack before signing a cross border deal with IP risk?

Keep two linked files: one for contract/IP and one for VAT administration. For VAT, record whether OSS is used (it is optional), the Member State of identification, and OSS filing cadence (quarterly for Union/non-Union, monthly for import). If you use OSS, include all supplies that fall under the chosen scheme in the OSS return. If you use CBR, record the participating EU country where the applicant is VAT-registered, and in multi-company cases note which company submitted on behalf of the others.

What evidence should I keep to respond fast if an IP infringement claim appears?

Keep a dated chronology that an independent reviewer can follow in one pass. For VAT operations, retain OSS returns, invoices, and related records, plus any CBR request materials where relevant. For ownership and infringement outcomes, treat evidence requirements as jurisdiction-specific and validate locally.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- europa.eu/youreurope/business/running-business/intelle...trusted

- europa.eu/youreurope/business/running-business/intelle...trusted

- intellectual-property-helpdesk.ec.europa.eu/news-events/news/ownership-horizon-europe-wh...trusted

- sme-vat-rules.ec.europa.eu/sme-scheme/cross-border-sme-scheme_entrusted

- newyorkconvention.org/englishexternal

- wipo.int/en/web/business/assignment-licensingexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Work for Hire vs Assignment of Rights for Freelancers

A freelance agreement is not just about price and scope. It decides who controls the rights in the work. If the ownership language is loose, rights can move earlier than you expect, cutting down your control once the work is delivered or used.

How to Structure a White Label Service Agreement for Cross-Border Delivery

Set your non-negotiables before you draft, or speed turns into avoidable risk. Before you open the first version, decide what cannot move, assign one redline owner, and treat every material point that is not in signed text as unresolved.

A Freelancer's Guide to Canada's Anti-Spam Legislation (CASL)

Treat this article as a pre-send gate, not background reading. Use CASL as the baseline. If you are in Canada, or you send a Commercial Electronic Message to Canadian residents, the message is in scope. The same applies when a CEM is sent from or to computers or devices in Canada. This material treats messages routed only through Canadian systems as not subject to CASL, so flag those for separate review before you send.