Quick Answer

Classify your position as SPDN or SPLN first, then file only what your records can prove. For indonesia tax residency, the guide applies Article 2 paragraph (3) letter a through three practical tests: residence, more than 183 days in any 12-month period, and intention to reside. It then uses Article 2A paragraph (1) as a timing checkpoint and requires a dated evidence pack before submission.

Why Indonesia tax residency feels confusing for digital nomads in Bali#

Confusion starts when equally confident people give opposite answers and you still need one filing position you can defend. In Bali, the same fact pattern can sound low risk in one conversation and high risk in the next.

The core issue is that immigration labels and tax status can overlap without being identical. Visa type may matter as context, but labels alone do not settle tax treatment. In practice, exposure is often framed as a mix of time in Indonesia, income source, and personal or economic ties.

The 183-day discussion adds more noise. A common reading is that staying more than 183 days in a year can point toward resident treatment, including when income is earned abroad. Day count is not the only factor. Practitioners also flag accidental taxpayer situations where obligations arise before someone plans for them.

The practical risk is waiting too long to decide your filing position. Late decisions can force you to reconstruct day counts and income-source facts from incomplete records. Before you file any return, use this order:

- Classify your likely position from facts, not visa label alone.

- Build the document set that supports that position.

- Set an escalation trigger when facts point in different directions.

Treat these as linked actions, not standalone tasks. A status view without records is weak, and records without a clear status decision leave room for inconsistent filing choices later.

The rest of this guide follows that sequence: legal terms, decision steps, document prep, exit-year handling, common errors, and monthly controls. The goal is simple: explain your position clearly, prove it quickly, and know when to stop guessing and get professional advice. For a broader primer, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

Start with the legal terms that decide your status#

Start by classifying status as SPDN (resident taxpayer) or SPLN (non-resident taxpayer). That classification drives the filing position you take and defend.

| Trigger | Article note |

|---|---|

| You reside in Indonesia | "Reside" can be more fact-based |

| You are present in Indonesia for more than 183 days in any 12-month period | Day counting is usually straightforward |

| You are present during a fiscal year and intend to reside in Indonesia | "Intend to reside" can be more fact-based |

SPDN means resident tax status in Indonesia. SPLN means non-resident status. Immigration status can inform the analysis, but it does not decide the tax answer by itself. In practice, the analysis usually turns on the three triggers above.

Day counting is usually straightforward. "Reside" and "intend to reside" can be more fact-based, so personal and economic ties may raise resident risk even when day count looks clean.

A practical way to apply those triggers is to test each one separately, then capture the result in one note. If the day test points one way but your ties and conduct point another, do not blur that into a vague answer. Mark the conflict clearly and treat it as an escalation point before filing.

Some advisors reference Article 2A paragraph (1) for timing, but this guide does not establish start or end timing rules from primary legal text. Use it cautiously as a checkpoint for arrival, mid-year changes, and departure, then confirm your interpretation against current legal text and DJP guidance before filing.

When advice conflicts, separate statute-level rules from commentary. Notes around PER-23/PJ/2025 or day-one resident claims can help you spot risk, but they do not replace binding text. Treaty (DTA) application can also affect residency outcomes.

Before you lock in SPDN or SPLN, keep a compact evidence pack ready:

- A rolling 12-month day log matched to passport entry and exit records.

- Records showing factual ties, such as lease terms, contract duration, and where work is managed.

- NPWP status records and related correspondence.

Keep those records dated and easy to retrieve. If you later need to explain why your filing position changed between periods, the timestamped trail matters as much as the document itself. If one trigger may apply and your evidence points in different directions, escalate before filing.

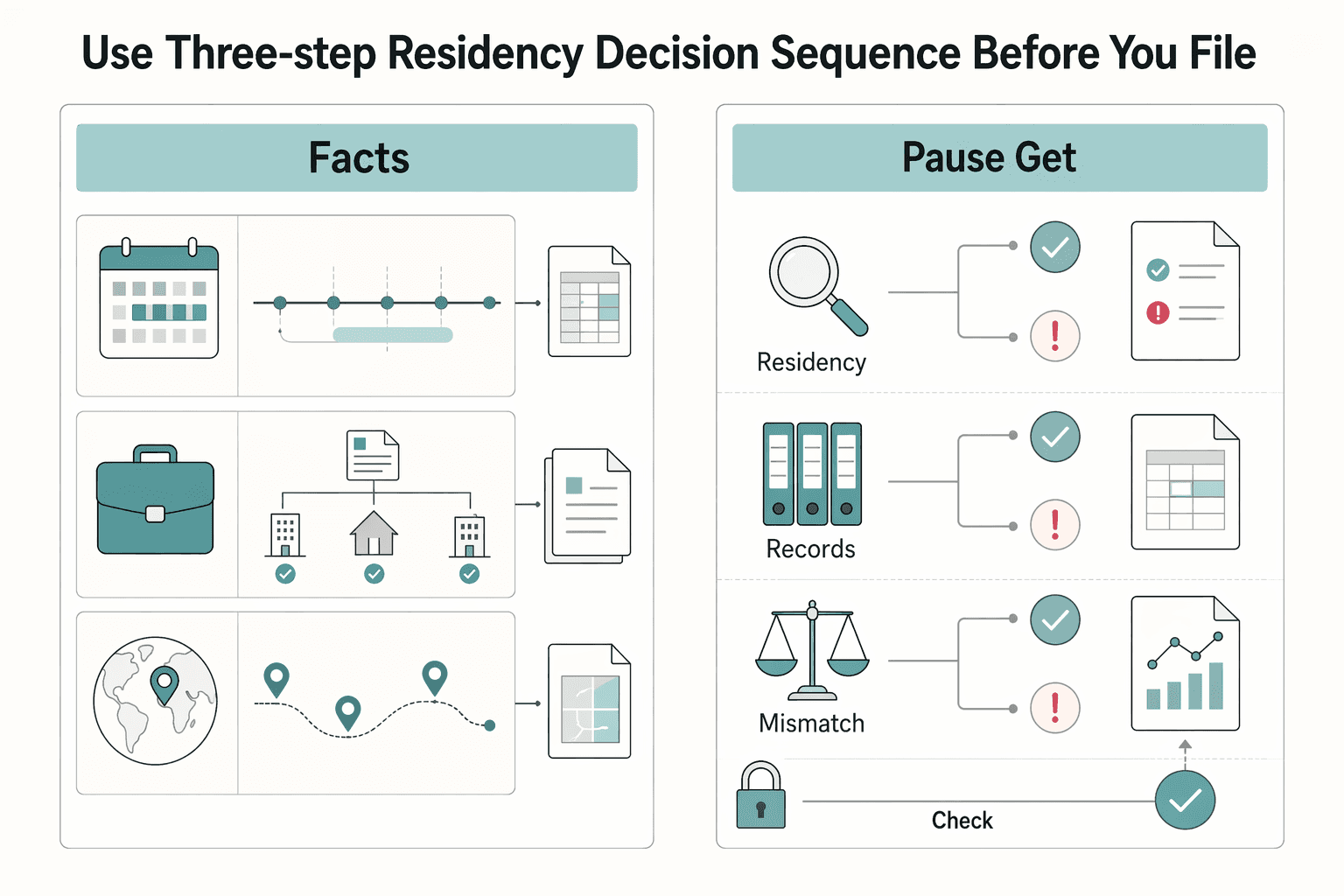

Use a three-step residency decision sequence before you file anything#

You can lower filing risk by working in order: classify the facts, stress-test mixed signals, then choose one filing path.

| Step | Focus | Article direction |

|---|---|---|

| Step 1 | Factual classification | Set a provisional resident or non-resident position from documented timeline data |

| Step 2 | Borderline cases | Use treaty tie-breaker rules when two countries could both claim residency |

| Step 3 | Choosing one action path | File as resident, file as non-resident, or pause and get treaty advice |

Step 1 is factual classification. Set a provisional resident or non-resident position from documented timeline data and keep it mechanical. Build one timeline that aligns travel records, contracts, and where work was managed.

Before Step 2, make sure your file includes a cross-checkable travel log and a short memo on the key residency facts. Keep a simple index so supporting records are easy to retrieve.

Do not turn Step 1 into a legal debate. The point is to assemble facts first and remove obvious internal contradictions. If your travel log says one thing and your invoice footprint says another, fix the record before you try to finalize status.

Step 2 handles borderline cases where two countries could both claim residency. In that dual-residency scenario, double-tax risk can appear, so use treaty tie-breaker rules to evaluate competing claims. Mixed signals are a review point, not a rush-to-file moment.

This is also where conservative sequencing helps. You can keep preparing your draft filing pack while treaty analysis is still under review. Do not lock in a definitive cross-border position until your evidence file is coherent.

Once that review is done, Step 3 is choosing one action path before filing:

- File as resident when facts and records support that position.

- File as non-resident when facts and records support that position.

- Pause and get treaty advice when competing claims still look credible.

Write down why you chose that path and what evidence supported it. That short note helps you stay consistent when you revisit the file months later.

If facts conflict, default to the position you can prove with documents. If competing residency questions remain complex, escalate to a cross-border tax specialist before filing.

For a quick next step, try the tax residency day counter.

Understand what changes between SPDN and SPLN in real money terms#

This status call changes tax scope and cash exposure, not just labels. The core split is whether you are treated as SPDN, where worldwide income is generally in scope, or SPLN, where Indonesia-source income is generally in scope.

| Position | Income scope used in Indonesia | Cash-flow impact to watch | Main risk if misclassified |

|---|---|---|---|

| SPDN | Generally includes worldwide income | Year-end liability can reflect domestic and foreign income in scope | Underreporting risk if foreign income was treated as out of scope |

| SPLN | Limited to Indonesia-source income | Indonesia-source payments may face non-resident withholding treatment | Over- or under-withholding if facts later support SPDN |

For non-residents, withholding on Indonesia-source income is often where friction shows up first. Advisory content often cites a 20% gross benchmark for some Indonesia-source income, but that is not a universal answer. Treaty position under P3B can change outcomes.

In practice, the first warning sign is often cash movement that does not match your assumed status. If payers apply withholding as if you are non-resident while your internal file is moving toward resident treatment, address that mismatch immediately.

Your records should tell one consistent story across payer treatment, tax records, and year-end tax position. If counterparties classify you one way while your internal position assumes another, treat that as an immediate review trigger.

Use a monthly checkpoint to prevent drift:

- Re-tag income as Indonesia-source or non-Indonesia-source and keep support.

- Reconcile withholding evidence with payer classification.

- Confirm records and draft filing position still support one status narrative.

If you cannot reconcile one income line cleanly, isolate it and document the issue. Small unresolved lines tend to expand into larger reconciliation problems near deadline.

If facts move into warning territory, including stays beyond 183 days within any 12 months, update your position early. Escalate quickly when treaty treatment is part of your filing stance.

Handle dual-residency conflicts before they become filing mistakes#

When your home country and Indonesia can both claim residency in the same year, review the treaty before filing, not after.

This overlap can happen when you spend substantial time in Indonesia while keeping ties elsewhere. Under cited Indonesia residency rules, resident status can be triggered by residence, by staying more than 183 days within 12 months, or by intention to reside.

Use the applicable treaty structure before filing. In the U.S.-Indonesia convention, Article 4 covers fiscal residence and Article 23 covers relief from double taxation. Use that structure to test your position without assuming every treaty uses the same wording.

A practical way to manage this step is to separate two questions in your file. First, which country can claim residence under its domestic rules. Second, what treaty outcome you can currently support with your records. Keeping those questions separate helps prevent overconfident filing assumptions.

Your filing posture is only as strong as your evidence file. Build it around consistent residency documentation for the filing period, then align it with factual ties that support one coherent residency story.

Before you file, verify:

- Rolling 12-month day count and dated travel log.

- Residency records match the taxpayer and filing period.

- Personal and economic tie records support the same position.

- Payer treatment and draft return posture match the same narrative.

When one item fails this check, do not patch the story with assumptions. Keep the filing stance at the strongest documented position until the missing piece is resolved. If the treaty file is incomplete by deadline, file conservatively first and amend after the documents are complete.

Build a document pack that can survive a DJP review#

Your residency position is only as strong as the file behind it, so organize records for fast checks and consistent retrieval.

Keep records in clear lanes that map to filing work: tax residence, registration and filing, tax payments and return filing, withholding support (including Article 26 where relevant), and audit readiness. That structure keeps monthly and annual obligations connected instead of scattered.

| Pack lane | What to keep together | Why it helps in review |

|---|---|---|

| Residence profile | Documents supporting your tax residence position | Keeps your residency narrative consistent across periods |

| Registration, filing, and payments | Return-filing records and payment records | Lets you trace each filed figure back to support |

| Withholding support | Transaction records and withholding support, including Article 26 where relevant | Makes withholding treatment testable against each transaction |

| Audit and assessment readiness | Records used to explain prior filings and changes | Makes it easier to explain what changed and why |

If you rely on double taxation agreement support, prepare it before filing so your position is document-ready. Confirm exact submission requirements before filing.

Build retrieval discipline into the pack. Use consistent naming and one index page so you can move from return line to source document without hunting across folders. Speed of retrieval matters when you need to answer questions under time pressure.

Run one short monthly checkpoint:

- Reconcile your residence support against current records.

- Match each income line to its transaction and withholding support.

- Flag any Article 26 entry that cannot be tied to a specific transaction.

- Fix gaps while evidence is fresh, not at filing deadline.

Add a simple month-close note that says what changed and what was carried forward unchanged. That one paragraph prevents repeated rework in later periods.

If the file is incomplete near deadline, prioritize the position you can fully support and resolve missing evidence as soon as possible.

Plan your exit year and non-resident status change correctly#

Treat an exit year as a consistency test. Close the resident-period facts first, then align any non-resident position to the same evidence trail.

Use a two-phase sequence for the exit year#

Use two phases: resident closeout, then non-resident positioning.

- Finalize one dated file for the resident period, including the timeline, income through departure, and income-source support.

- Keep your position aligned with facts. Do not force SPLN treatment while facts still support SPDN (SPLN is described as Indonesia-source only, while SPDN is described as worldwide income).

- Keep one continuous evidence pack for the full year so a reviewer can trace your position without gaps.

Avoid splitting the year into disconnected folders. Keep one continuous record chain, then mark transition points clearly.

Do a final fact-check before departure#

Before you depart, verify that your status narrative is based on facts, not labels. Referenced material describes PER-23/PJ/2025 as effective December 9, 2025 and notes stronger focus on how you actually lived and worked, with formal indicators not sufficient on their own and a more-than-183-days-in-12-months criterion.

Run one final cross-check before you lock the exit-year filing posture. Your day log, income-source mapping, and departure records should point to the same narrative.

If facts are mixed or unclear, default to the position you can fully support and get professional advice before locking in a status change.

Avoid the five mistakes that trigger costly rework#

Rework gets expensive when the filing story looks cleaner than the facts. Keep your file anchored to Article 2 paragraph (3) letter a and Article 2A paragraph (1): reside, more than 183 days in 12 months, intention to reside, and real evidence when claiming status ended because you left Indonesia permanently.

| Mistake | Article warning |

|---|---|

| Treating immigration labels as automatic tax proof | Status labels can be context, but they are not the legal tests |

| Using only day counting and ignoring intent | The more-than-183-day test matters, but it is not the only trigger |

| Assuming the >183-day presence must be consecutive | The day-count test is within a 12-month period and does not have to be consecutive |

| Claiming resident status ended without real departure evidence | If status ended because you left Indonesia forever, the record needs real evidence of that intent |

| Waiting until departure month to organize your evidence | If departure evidence is thin, forcing a non-resident position to match travel timing raises risk |

- Treating immigration labels as automatic tax proof.

Status labels can be context, but they are not the legal tests. Start from your lived facts and timeline.

- Using only day counting and ignoring intent.

The more-than-183-day test matters, but it is not the only trigger. A day-count-only position can still misclassify you.

- Assuming the >183-day presence must be consecutive.

The day-count test is within a 12-month period and does not have to be consecutive.

- Claiming resident status ended without real departure evidence.

If you take the position that status ended because you left Indonesia forever, your file needs real evidence of that intent.

- Waiting until departure month to organize your evidence.

If departure evidence is thin, forcing a non-resident position to match travel timing raises risk.

These mistakes usually appear together. A weak day log often sits next to unclear intent records and thin departure evidence. Catching one issue early often exposes the others while there is still time to fix them.

Use one final checkpoint before filing: confirm your rolling day log, confirm intent-related facts in your record, and confirm departure evidence if you are ending resident status. If any check fails, file the position you can support and escalate early.

Apply decision rules to common Bali nomad scenarios#

Start with the facts, then file. Apply the resident triggers in Article 2 paragraph (3) letter a and the start or end timing in Article 2A paragraph (1), and only take positions you can evidence now.

| Scenario | What can misclassify your status | Decision rule to apply now |

|---|---|---|

| A: About six months in Bali with Indonesia-source consulting income | A short-stay assumption can fail if total days cross the more-than-183-days-in-12-months trigger. | Use a rolling 12-month day log, not a calendar-year guess. If total stay passes the threshold, align filing to the timeline that starts from the first day of stay. |

| B: Year split between Canggu and home country, with possible dual-residency claims | Conflicting narratives can appear when filings are prepared before facts are reconciled. | Do not finalize unsupported cross-border conclusions. Keep filing posture tied to documents already in hand and escalate early if conflict remains. |

| C: Mid-year shift from B211A visa to KITAS | Visa changes can be treated as automatic tax-status changes when underlying facts did not change. | Re-test at the change date using day count and intention to reside first, then use financial ties and behavioral patterns as supporting indicators. Update the evidence file at the same point. |

| D: Resident filing year includes foreign income streams | Cross-border positions can be asserted before supporting records are complete. | Treat document readiness as a gate. If support is incomplete, keep the position conservative and escalate before filing deadlines. |

The sequence is your control point: classify facts, test start and end timing, then file. Reverse that order and you create expensive rework.

Use one pre-filing checkpoint:

- Verify rolling day totals across any 12-month period.

- Verify whether records show intention to reside from circumstances.

- Verify whether any claimed end of residency is backed by real evidence of leaving Indonesia forever.

- Verify each cross-border position is backed by documents you can produce quickly.

Add one scenario-specific note to your file each period, even if nothing changed. It can be short, but it should confirm which risk pattern still applies and why your current filing path remains valid.

If one scenario still has mixed facts, do not force certainty for speed. File the position you can support now, document the open issue, and escalate before deadline.

Set monthly compliance checkpoints for a business-of-one#

Revalidate your filing posture monthly, not only at year-end. Under Indonesia's self-assessment model, you are responsible for calculating, settling, and reporting your own tax position.

Start with status and income source. Track days on a rolling 12-month basis, test status against the more-than-183-days trigger, and then recheck source rules. Income connected to work or services in Indonesia can be treated as Indonesia-sourced even when paid offshore.

Use one short monthly checklist:

- Update your rolling 12-month day log.

- Reassess likely resident or non-resident posture from current facts.

- Reclassify income lines by source and flag amounts already taxed through withholding at payment.

- Store day log, source mapping, and withholding records where retrieval is easy.

Treat document readiness as a control, not as admin overhead. Tax authority reviews can fall within a five-year limitation window, so weak records now can become expensive later.

Run a filing-risk check immediately after the document check. If support is incomplete for your preferred position, use a conservative filing assumption for that period. This matters because resident individuals are taxed on worldwide income, while non-residents are taxed on Indonesia-derived income and are exempt from worldwide income reporting.

Set a quarterly escalation rule: if dual-residency uncertainty is still unresolved near deadline, get advisor review before filing. Keep visa records aligned with real activity and length of stay, but do not use visa labels as your tax conclusion.

To keep this sustainable, time-box the monthly review and document only what changed. You do not need long memos every month. You need consistent evidence that your classification and filing posture stayed aligned with current facts.

Keep payment and tax records audit-ready with your finance stack#

Traceability is what makes a filing position defensible. The stronger position is usually the one you can prove through dated payment records and linked tax documents.

Use one ledger-first trail for each invoice, payout, and reconciliation entry. Each line should show what was paid, when it was earned, and which monthly tax posture it supported. This matters because the more-than-183-days test within 12 months does not require consecutive days, and intent is assessed from circumstances rather than label alone.

At month-end, run one verification pass before close:

- Match each invoice to its settlement line and keep both document IDs.

- Tag each income line to that month's resident or non-resident posture.

- Keep related tax documents with the invoice and payout they support.

- Save a dated snapshot of tax profile details used for the period.

Keep status artifacts in the same record set as money movement. If you claim subjective tax obligation ended because you left Indonesia permanently, keep clear evidence of departure intent and timing.

If you use Gruv, map payment events to exportable evidence packs and monthly close checklists so retrieval stays repeatable. Confirm market and program coverage before you rely on automation, and set a fallback export step for anything not captured automatically.

Make one person responsible for final monthly reconciliation, even if you're a team of one. Clear ownership reduces partial closeouts where payment records are updated but tax or status tagging is left unfinished.

A common failure mode is fragmented records across email, banking apps, and ad hoc sheets. A small rule misread can then turn into correction work and possible penalties. Use a hard rule: if you cannot assemble the full support chain for a filing position in one sitting, treat that position as weak. File conservatively for that period, and escalate before the next deadline.

Make the decision early and document it like an operator#

Choose the filing position you can defend, then document it before you file. Early decisions reduce contradictions and give you time to fix weak evidence.

Use this sequence every cycle: classify facts, test residency-conflict risk, prepare records, then file. Keep a dated monthly note of what changed, what did not, and why your current position still holds.

A compact monthly close is enough if you do it consistently:

- Confirm which returns apply for the period, including income tax, VAT, and withholding where relevant.

- Reconcile reportable payments to invoices, bank records, and withholding documents.

- Flag mixed evidence early, especially when residency status and transaction type could change withholding treatment.

- Decide whether the position is ready to file or needs advisor review first.

Use filing dates and retention rules as anchors. Annual returns are due by the end of March for individuals and April for corporate entities, and monthly returns may also be required depending on obligations. Keep bookkeeping support documents for 10 years.

Pay extra attention to withholding on cross-border payments. Withholding is deducted at source, and treatment varies by transaction nature and the parties' residency status. Weak mapping can create unexpected liabilities later.

Escalate early when evidence is mixed. Issues with the Directorate General of Taxation can take months to years to resolve, and documentation quality directly affects that process.

Before each filing cycle, pick one concrete next action and schedule it immediately: reconcile the day log, close missing withholding support, or verify key residency evidence. Progress is usually blocked by one unresolved item, not by the whole file.

Frequently Asked Questions

Do the days for Indonesia tax residency need to be consecutive?

No. A commonly cited threshold is more than 183 days within any 12 months, and those days do not need to be consecutive. Consider keeping a rolling 12-month day log so your count is easier to defend if questioned.

If I stay under the day-count threshold, am I automatically SPLN?

No. Advisory guidance treats intention to continue residing as a separate test, and SPDN status may still apply before 183 days is reached. Day count matters, but it is not the only factor.

What practically changes when I am treated as SPDN instead of SPLN?

The main change is tax scope. SPDN is generally described as taxable on worldwide income, while SPLN is generally taxed only on Indonesia-source income. That difference affects how income is classified and reported.

How does Article 26 Withholding Tax apply to non-residents?

This draft cannot confirm full Article 26 mechanics from the provided material. One advisory source cites a 20% flat rate on gross Indonesia-source income for non-residents, but exceptions and process details are not covered here. Confirm current DJP treatment before relying on calculations.

What should I do if Indonesia and my home country both treat me as tax resident?

Treat it as a P3B treaty issue, not a guess. Relief is not automatic, so filing posture should be backed by consistent records across both countries. If timing is tight, use the most defensible documented position and escalate quickly for treaty advice.

How do I stop being an Indonesian tax resident when I leave Bali?

Leaving Bali alone may not settle tax status by itself. Residency tests are described as separate from immigration permit labels, and intention to continue residing may still be considered with day totals. Before filing as non-resident, make sure records show a clear change in residence facts and timing.

How much can I rely on newer interpretations like PER-23/PJ/2025 without full implementation detail?

Use PER-23/PJ/2025 as an important current reference, not as a substitute for current official DJP material. One advisory source reports an effective date of December 9, 2025 and says older formal indicators alone may no longer be sufficient. For borderline cases, verify before filing.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 3 external sources outside the trusted-domain allowlist.

- irs.gov/irm/part3/irm_03-038-147rtrusted

- state.gov/reports/2025-investment-climate-statements/i...trusted

- balibusinessconsulting.com/bali-tax-residency-rules-2026-what-makes-you...external

- balivisa.co/tax-residency-indonesia-explained-avoid-doub...external

- wearesynergypro.com/news/avoid-disaster-tax-audit-critical-rules...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

How to Write Compelling Case Studies for Your Portfolio

Treat your case study as buyer decision evidence, not as a polished recap of work you enjoyed doing. To build trust, give the reader enough real context and proof to answer one question: should they trust your judgment on a project like theirs?

Unbundling IT Agencies Without Breaking Delivery or Payments

Unbundling is no longer a theoretical strategy choice. For freelancers and small cross-border teams, it is an operating decision about where accountability must stay tight and where specialized execution can be split without creating hidden risk.