Quick Answer

A Hungary White Card does not automatically make you a Hungarian tax resident. The article says residency should be tested in order under Section 3(2): relevant status criteria, then permanent residence, then center of vital interests, and finally habitual residence. The 183 day rule is only one input, and permit status should be kept as context rather than treated as proof.

Start Here If You Want a Defensible Hungary Tax Position#

Start with a decision sequence you can defend if reviewed, then estimate tax and prepare filings. For globally mobile freelancers and consultants, a major avoidable risk is taking a residency position you cannot support with records when someone asks how you reached it.

Keep three outputs in view from day one: a clear decision order, a document checklist mapped to that order, and explicit escalation triggers for mixed facts. If you can produce those three items, you reduce late surprises and make the filing process calmer.

This article is limited to individual Hungarian tax residency under Act CXVII of 1995 on Personal Income Tax, Section 3(2). It does not cover company residency under Act LXXXI of 1996 on Corporate Tax and Dividend Tax.

Use this order before you file:

- Classify your case under the individual criteria in Section 3(2), including, where relevant, conditions such as a right of residence longer than three months and presence for at least 183 days in the calendar year, counting entry and exit days.

- If status tests do not settle the result, test permanent residence first. For certain individuals, having only a permanent residence in Hungary can itself be a residency criterion.

- If permanent residence does not resolve residency, test center of vital interests. If that is still unclear, test habitual residence in domestic territory.

- If your facts point in different directions across countries, pause and build support for the strongest position before filing.

Build your records in the same order. Keep at least:

- records tied to permanent residence

- records showing where personal and economic ties are strongest

- day count records that include entry and exit days

- draft notes for a tax residence certificate request

Before you move to return preparation, write one short line under each test saying either resolved or unresolved. That simple discipline makes gaps visible early and prevents you from treating assumptions as conclusions.

Escalate early when facts conflict. If one country looks stronger on home ties but another looks stronger on day count or habitual residence indicators, treat it as a high-friction case and get written advice before filing. If you need a tax residence certificate, confirm current process details with the National Tax and Customs Administration.

Want a quick next step for "hungary tax residency"? Try the tax residency day counter.

Learn the Terms Before You Make Any Move#

Define the core terms before you submit anything. If the terms are loose, the filing position is usually loose too, and contradictions appear later when you try to reconcile records.

| Term | Definition | Article note |

|---|---|---|

| Permanent home | The place treated as your stable home | Having your only permanent home in Hungary supports Hungarian residency |

| Center of vital interests | The country where your family and business ties are strongest when more than one home exists | Use this when more than one home exists |

| Habitual residence | A fallback test for where your day-to-day life is centered | Used if the first two tests do not resolve residency |

| 183 day rule | A threshold used in specific criteria | Not a universal override |

| Double taxation treaty | A next check when two countries still have plausible residency claims | Use when two countries still have plausible residency claims |

If you are treated as a Hungarian tax resident, Hungary can tax income from domestic and foreign sources. If not, your Hungarian tax position may be narrower. Set that distinction first, then handle returns, treaty claims, and planning.

When you collect records, use each term as a test label. Do not file a travel document under permanent home unless it actually supports that test. Do not file a contract under day count unless it helps timeline consistency. The label should match the point you are trying to prove.

Apply the terms consistently and document facts clearly. If home, ties, and daily living point to different countries, stop and escalate before filing. That pause is cheaper than amending a return built on mixed logic.

If you want a deeper dive, read Can Digital Nomads Claim the Home Office Deduction?.

Understand Where the Hungary White Card Fits#

Permit labels are useful context, but they are not personal tax conclusions on their own. Permit category alone does not determine personal tax residency outcomes.

| Permit category | What the guidance covers |

|---|---|

Hungary White Card | No personal tax residency outcome is established here |

Guest Investor Program | No personal tax treatment is established here |

Hungarian Card | No personal tax treatment is established here |

EU Blue Card | No personal tax treatment is established here |

National Residency Card | No personal tax treatment is established here |

Most material supports VAT administration topics such as OSS registration, cross-border SME thresholds, and VAT rulings. That supports indirect-tax process points, not personal residency status.

Use the same rule across permit categories: keep the permit in your file as context only, not as a standalone answer on residency.

A permit record can still sit in the file as context. It should not be presented here as a standalone answer on residency.

If you do not have clear, current guidance on permit status and residency interaction, keep the point open and verify before relying on it in your filing position. Open points are manageable; hidden assumptions are where filings usually break.

Apply the Residency Tests in the Correct Order#

Do not build a personal residency conclusion from VAT-focused guidance alone. VAT rules do not by themselves establish a full personal income tax residency analysis.

What it does establish clearly is VAT process detail: CBR as an advance-ruling path for complex cross-border VAT treatment, OSS registration in one Member State of identification with MOSS extended to OSS from 1 July 2021, and cross-border SME mechanics with one prior notification in the Member State of establishment, a EUR 100 000 Union turnover limit, and a process that should not take longer than 35 working days.

Use this checkpoint before drafting your filing position:

- Label each record as

VAT processorpersonal residency. - Keep OSS, CBR, and SME documents out of your personal residency conclusion set unless supported by personal tax authority.

- Track unresolved personal residency terms explicitly so gaps stay visible.

- Recheck the file after any permit or status change.

When you sort records, use a simple table and keep it current:

| Record | Label | Supports conclusion now | Action |

|---|---|---|---|

| Permit copy | personal residency context | No | Keep as context, do not treat as conclusion |

| OSS or SME record | VAT process | No for residency | Store in VAT file only |

| Housing and tie evidence | personal residency | Yes, if consistent | Map to the relevant test |

This extra sorting step helps prevent a common filing error: mixing useful tax administration records with personal residency proof and assuming they carry the same weight.

Do not treat VAT administration records or permit labels as proof of personal tax residency. Keep those lanes separate from the start and your final file will read more clearly.

Stop Misusing the 183 Day Rule#

Treat the 183 day threshold as one input, not a shortcut. Residency is an ordered legal analysis, not a day count contest.

Under Section 3(2) of Act CXVII of 1995 on Personal Income Tax, the 183 day condition appears in a specific status pathway tied to free movement and a right of residence longer than three months. The count includes both entry and exit days. The threshold matters, but it does not replace the rest of the tests.

The practical risk is treating day totals as the lead argument when stronger facts point elsewhere. If you have one clear permanent home in Hungary, that can matter more than calendar totals alone. If homes exist in multiple countries, the focus shifts to center of vital interests. If that center is still unclear, move to habitual residence. Fragmented travel patterns can create false confidence from totals.

Use this checkpoint before filing:

- Count days with a ledger that includes entry and exit dates.

- Keep permanent home records separate from travel records.

- For multi country living, write a short center of vital interests memo covering family and business anchors.

- If travel is fragmented and your total sits near 183, treat it as a red flag for deeper review, not a planning shortcut.

A simple contrast helps. If your day count is clean but your home and tie evidence is inconsistent, the file is still weak. If your day count is messy but your home and tie evidence is strong and documented, you may still have a defensible position once the timeline is cleaned up. The point is to weigh all tests in order, not to improve one metric.

If day count, permanent home, and ties do not point the same way, resolve that conflict before filing.

Related: A Deep Dive into the USA's Citizenship-Based Taxation System.

Resolve Dual Residency Before It Becomes a Filing Problem#

When indicators point in different directions, resolve the conflict before filing. Two countries may treat you as resident in the same year, so first confirm whether an active double taxation treaty applies to your country pair for that tax year.

| Date or period | What the article says | Filing note |

|---|---|---|

| September 18, 1979 | The 1979 convention entered into force | For the United States and Hungary, timing is decisive |

| January 1, 1980 | The 1979 convention had a general effective date | General effective date |

| Through December 31, 2023 | Cited analyses report that its provisions applied | Treaty provisions applied through December 31, 2023 |

| January 1, 2024 | Cited analyses report that its provisions no longer apply | Do not rely on treaty tie-breaker relief for post-2023 U.S.-Hungary income |

| 2024 income | Reported commentary states that this is the first year outside treaty protection | Build your filing position under each country's domestic residency rules |

For the United States and Hungary, timing is decisive. The 1979 convention entered into force on September 18, 1979, had a general effective date of January 1, 1980, and cited analyses report that its provisions applied through December 31, 2023 and no longer apply from January 1, 2024. Reported commentary also states that 2024 income is the first year outside treaty protection.

For post-2023 U.S.-Hungary income, do not rely on treaty tie-breaker relief. Build your filing position under each country's domestic residency rules and document it clearly for the exact tax year.

Use this pre-filing checkpoint:

- Confirm whether a treaty is active for your country pair and tax year.

- If no treaty relief applies, document your domestic-rule residency position in each country.

- Make sure a third party can follow your reasoning from facts to filing treatment.

- If facts are mixed or weak, escalate before filing instead of forcing a deadline position.

Write the memo as if someone else will review it without context. State the year, the country pair, the tests you applied, the records you used, and the points that remain uncertain. That structure reduces the chance of mixing rules across years or assuming treaty relief where it is not available.

If your position changes after additional evidence, update the same memo instead of starting over. A clean revision trail is easier to defend than multiple disconnected drafts with different conclusions.

Build an Evidence Pack That Can Survive Scrutiny#

Build your evidence pack early and keep it reviewable. Hungary uses self assessment, so you are responsible for assessing, declaring, and paying based on records you can substantiate.

Use this bundle as a practical working set, not a fixed legal requirement:

| Document | Main question it can support | What to verify before filing |

|---|---|---|

| Address and housing records (for example, registration records, lease terms, utility history) | Where you maintained a home during the filing period | Names, addresses, and dates align with the period you are filing |

| Travel records with entry and exit dates | Timeline consistency | Records match tickets, passport stamps, and calendar entries |

| Contracts, invoices, client communications, and work location notes | Economic activity timeline | Activity and location records support the filing position you are taking |

| Family and household records, if relevant | Personal-context consistency | Personal records do not materially conflict with the rest of the file |

| A short memo on conflicting indicators | Cross-border position | It states what is stronger, what is weaker, and which assumptions you are making |

How you organize this pack matters almost as much as what is inside it. Keep each document named with date, country, and purpose so a reviewer can find support quickly. If one record supports multiple points, note that once and cross-reference it instead of duplicating the same file in several places.

If evidence supports more than one country, pause and write a short comparison memo before filing. State which position is stronger, which evidence is weaker, and which assumptions you are making. That memo is where you resolve conflicts, not in scattered comments across documents.

Use this pre-submission check:

- Each key conclusion is tied to primary records.

- Dates align across housing, travel, and business activity.

- Where indicators conflict, your memo explains why you chose one filing position.

- A third party can follow your logic from records to filing outcome.

Add one practical check before submission: read the file in chronological order from the start to the end of your filing period and confirm nothing material is missing around moves or major travel periods. Those periods can create the largest interpretation gaps.

Keep a dated monthly folder as an operational habit to reduce last-minute gaps. In cross-border cases, keep documents that materially support your timeline and filing position.

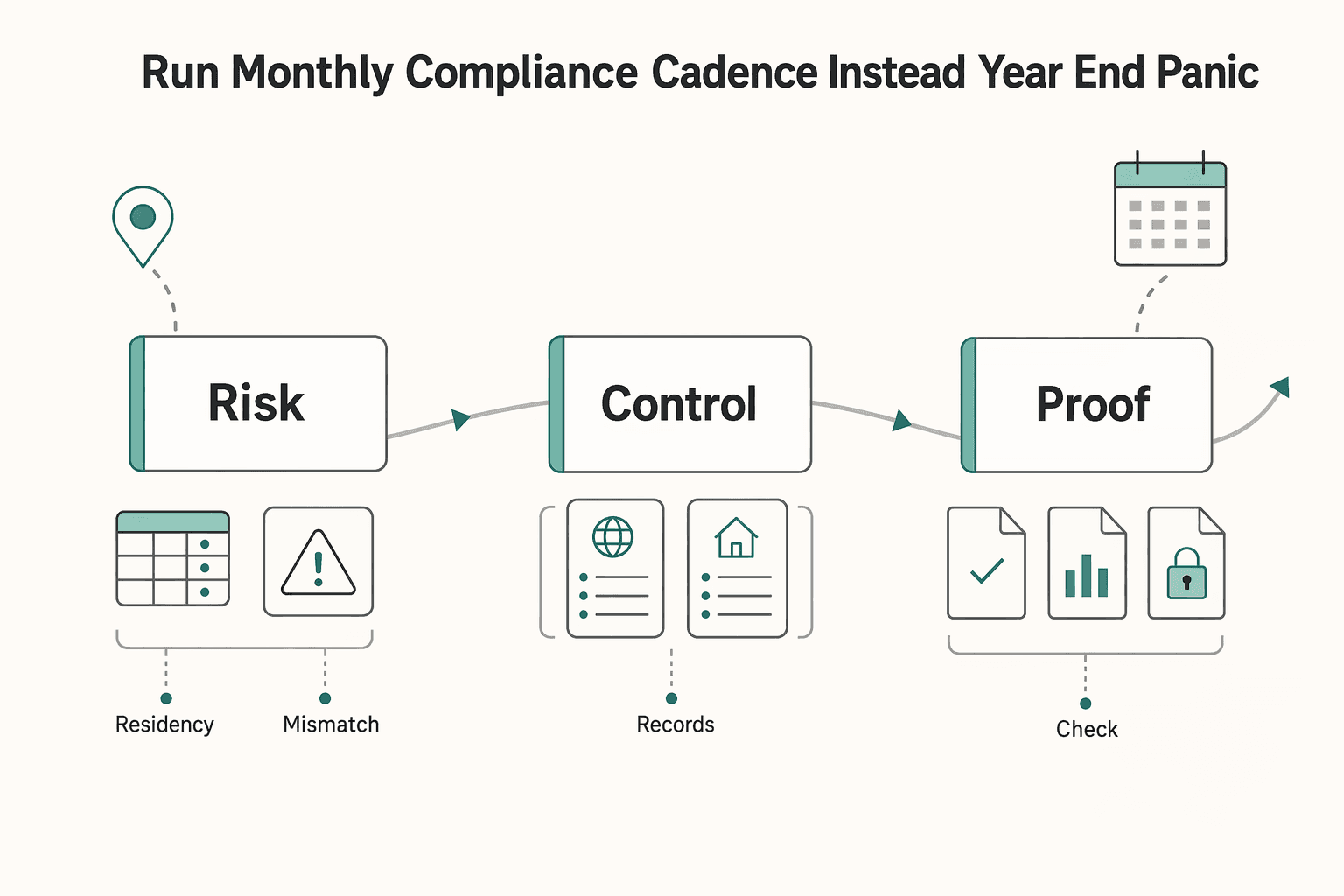

Run a Monthly Compliance Cadence Instead of Year End Panic#

Monthly review can be safer than rebuilding the year near deadline. It helps keep your file consistent and reduces contradiction risk.

In your records, track two live income buckets as internal labels: worldwide income and Hungarian source income. For each material item, add a short note on what you recorded, why, and which document supports it. Treat these labels as working assumptions to review, not final legal conclusions.

Run one monthly reconciliation against your evidence pack and memo:

- Update address and travel records, and flag missing periods.

- Review material income entries and confirm each still has a clear rationale note.

- Check whether any residency, permit, or work pattern fact changed.

- Confirm records, memo, and filing position still tell one consistent story.

Keep the reconciliation output simple: what changed, what did not, what needs follow-up, and who owns each open item. If a month has no change, record that as well. A clear no-change note is better than silence.

This is practical discipline, not extra paperwork. Recurring income tax procedures are part of compliance guidance, and EU tax administrations have cross-border administrative cooperation tools. Coordinated controls can include simultaneous controls or joint audits in appropriate cases.

Use one decision rule: if a material fact changes mid year, document the month and reassess immediately. Waiting until year end can make the file harder to reconcile and increase the chance of conflicting statements.

Avoid the Mistakes That Trigger Expensive Rework#

Costly rework often starts when VAT or corporate records are treated as proof of personal income tax residency. Keep those lanes separate and use VAT tools only as VAT evidence.

Your monthly process only works when records stay in the right file. OSS was expanded on 1 July 2021, and the EU-wide threshold for covered supplies is EUR 10,000. The cross-border SME scheme includes a EUR 100,000 turnover ceiling and a 35 working day processing target after prior notification. CBR is for advance VAT rulings, filed in the participating country where you are VAT-registered, and Hungary is listed as a participant. These are VAT mechanisms, not personal residency conclusions.

The pattern behind expensive rework is predictable. A filing memo uses one line about permit status, one line about day count, and one line about legal framing, but none of those lines is tied to a complete personal fact narrative. Review then forces clarification under time pressure.

Where the four mistakes happen#

| Mistake | Why it triggers rework | Better move |

|---|---|---|

| Treating permit labels as an automatic tax conclusion | Permit labels alone do not prove your personal tax residency position | Keep permit records as context, and support residency conclusions with personal fact records |

| Relying only on day counts | Day counting alone can leave gaps in your residency analysis | Use day counts together with your broader personal residency fact pattern |

| Invoking legal frameworks without a defensible fact pattern | Legal references without complete support are hard to defend in review | Build the fact file first, then apply the relevant legal framework only where it is needed |

| Mixing individual analysis with corporate-tax concepts | Combining personal and corporate tracks creates internal inconsistency | Split personal and corporate notes, and keep each conclusion in the correct file |

A common failure mode is treating OSS and personal residency indicators as interchangeable proof. Review usually exposes an incomplete personal residency narrative and forces amendments under deadline pressure.

To reduce that risk, run one language check on your draft memo before filing. Any sentence that jumps straight from label to conclusion without linking tests and evidence should be rewritten or marked as unresolved.

Fast verification before filing#

Run this checkpoint before submission:

- Keep one short memo for personal residency facts and one for VAT choices.

- Attach one supporting document to each claim in the same monthly folder.

- Flag any sentence that uses a permit label, day count, or legal reference as a standalone conclusion.

- If a claim fails that test, rewrite it as an open item for advisor review instead of filing it as fact.

If this check produces too many open items, that is a signal to pause and escalate. Filing with visible uncertainty is usually safer than filing with untested certainty.

Know Exactly When to Bring in a Tax Professional#

Bring in a tax professional as soon as your residency conclusion stays unclear after a first self-review, or your evidence points in more than one direction. If you are unsure about residency, get support from an accountant or an international tax advisor before filing assumptions harden into rework.

A good escalation is specific. Instead of asking for a broad opinion, ask for a conclusion tied to facts, criteria, and documents. That request format produces advice you can actually apply in returns and record keeping.

Escalation triggers that should stop self-filing#

- Your evidence for

permanent homeis incomplete or contradictory. - Your evidence for

centre of vital interestsis split across countries and does not support one clear outcome. - Status indicators and personal-life indicators do not align cleanly. For example, one route includes an EEA registration card issued in Hungary plus at least

183 days, while residency may still apply even when initial status criteria are not met.

Add one more practical trigger from the same logic: your own written memo changes conclusion each time you revise it. If the answer moves around with no new evidence, stop and get external review.

Ask for specific deliverables, not general advice#

Request these items in writing:

- A residency position memo with the final position and the key facts relied on.

- A clear rationale for the residency position, including where uncertainty remains.

- A filing assumptions note listing what could change the conclusion and what extra evidence would be needed.

Before submission, match each conclusion in that memo to at least one document in your file. If a conclusion cannot be matched, treat it as unresolved and do not present it as settled.

If you were tax resident in Hungary at any point in 2025, filing is expected in the first half of 2026. Draft returns are typically available on March 15, with filing on May 20, so escalate early if your position is still uncertain.

Take the Next Step With a Defensible Position#

A lower-stress filing cycle comes from applying a clear review sequence and documenting each conclusion. Keep facts, assumptions, and escalation points separate so your position stays defensible when deadlines tighten.

Check source quality before changing any conclusion. IRS Publication 519 includes headings such as Nonresident Alien or Resident Alien and Substantial Presence Test, which can help with US context, but those labels do not decide this topic on their own. One cited EU Official Journal page is a publication of written parliamentary questions and answers dated 5 September 2013, and another captured page is cookie consent text rather than substantive tax guidance. Treat non-decision-grade material as context only.

Use this one week checklist:

- Classify each open point as fact, assumption, or escalation item.

- Run your review sequence consistently and pause where evidence is thin.

- Build an evidence pack that maps each retained claim to a document.

- Remove lines supported only by stale or non substantive material.

- Flag cross border conflicts for advisor review before filing.

- Do one final verification pass, then lock the evidence set.

As a final quality check, read your memo and ask one question: could a third party follow this file from records to conclusion without asking what you meant. If the answer is yes, your position may be ready for filing. If the answer is no, the next action is clear: resolve open items before submission.

For broader cross border planning context, use The Ultimate Digital Nomad Tax Survival Guide for 2025 and compare decision patterns across countries.

Frequently Asked Questions

Does spending fewer than 183 days in Hungary mean I am not tax resident?

No. The 183 day threshold is only one listed criterion tied to a residence-right condition longer than three months, not the only path. Residency can still be supported by other tests such as only permanent residence in Hungary or center of vital interests there.

What is the exact order of tests for Hungarian tax residency decisions?

Start with the criteria in Section 3(2) of Act CXVII of 1995 on Personal Income Tax. Then assess permanent residence and center of vital interests, and if the conflict remains, check the relevant treaty text against your documented facts. If no step clearly resolves the issue, escalate before filing.

If I am a Hungarian tax resident, what income is taxable in practice?

In practice, a Hungarian tax resident is generally taxed on worldwide income, including Hungarian and foreign income. Keep records aligned to the tax year and use consistent income categories throughout the year.

What should I do if Hungary and another country both treat me as resident?

Treat it as a dual residency case and build a complete fact file first. Then confirm whether a treaty is active for the country pair and tax year and document the domestic rule analysis in each country. If the result is still unclear, get professional support before filing.

Which documents best prove permanent home and center of vital interests?

Use permanent home records that show where you could actually live on an ongoing basis. Use center of vital interests records that show where your family and business ties are strongest. A consistent set of records is more persuasive than any single document.

Does the Hungary White Card automatically make me a Hungarian tax resident?

No. The article says a residence permit, including the White Card, is only one fact and does not automatically make someone a Hungarian taxpayer. Residency still depends on the legal tests and the full fact pattern.

When should I request a tax residence certificate?

Request a tax residence certificate when you need formal proof of residence for cross-border administration or treaty-related documentation. Do it after your residency position is documented and supported by evidence so the request matches your filing position. If the underlying position is still unresolved, finish that analysis first.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- europarl.europa.eu/cmsdata/296344/Study%20Tax%20barriers%20and%...trusted

- irs.gov/pub/irs-trty/hungary.pdftrusted

- sme-vat-rules.ec.europa.eu/sme-scheme/cross-border-sme-scheme_entrusted

- taxation-customs.ec.europa.eu/archives/taxable-persons/vat-cross-border-ru...trusted

- taxation-customs.ec.europa.eu/system/files/2016-09/report_evaluation_vat.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Can Digital Nomads Claim the Home Office Deduction?

Claim the deduction only when your facts and records can carry it. With the home office deduction for digital nomads, the real decision is usually a three-way call: claim it, do not claim it, or pause and get help because your file is not ready.

US Citizenship-Based Taxation Explained for Mobile Freelancers

Start with two decisions: confirm your tax status for the year, then follow a filing sequence you can defend. If you came for a practical explanation, focus on execution, not theory.