Quick Answer

Yes, a renter can write off a home office when IRS tests are met and documented. Use a compliance-first process: confirm you are in the right filing lane, pass exclusive use, regular use, and principal place of business gates, then calculate through Form 8829 and tie to Schedule C. If facts are mixed or records are thin, pause and escalate before filing.

Renters can claim the home office deduction with a compliance-first playbook#

A renter can claim the home office deduction when IRS eligibility tests are met and the business use of the home is clear to document. You are the CEO of a business-of-one, so run this like an operating decision: qualify first, document second, then calculate. If you want a low-friction approach, start with compliance, not aggressive tax savings.

Before you start#

Use this as educational guidance, not personal tax advice. Anchor decisions in IRS Topic No. 509 and Publication 587, then move forward only when your facts stay clear. If your facts are unclear, pause and clarify your documentation before filing.

- Classify your filing lane. Confirm you are not claiming this deduction as an employee. The IRS allows the home office deduction for qualified renters and homeowners, but employees cannot claim this deduction.

Outcome: You know whether to continue or stop now.

- Define your claim area with strict boundaries. The IRS treats an apartment as a qualifying home type for this purpose. Your workspace must meet the exclusive use requirement and regular use requirement, and it must support a principal place of business case. If you mix personal and business use in the same area, that area fails unless a specific exception applies, such as eligible daycare or storage situations.

Outcome: You get a clean pass or fail on core eligibility.

- Choose the safe-default decision. Tag the claim as Proceed or Pause based on your evidence quality, not your preference. Keep the decision tied to IRS rule-based eligibility and the records you can support.

Outcome: You reduce filing stress and protect compliance.

A simple contrast makes this real. A consultant who rents a small apartment, works from one dedicated desk for client delivery, and keeps that spot business-only can usually build a defensible position. A consultant who rotates between couch, bed, and kitchen table should pause, tighten the setup, and reassess.

What to prepare before you decide anything#

Prepare your filing context, IRS anchors, and proof files before you decide on a home office deduction as a renter. You already have the Proceed, Pause, or Escalate mindset. Now turn it into a prep pack you can reuse, so your decision stays consistent and easy to defend.

Run this prep in order#

- Confirm your filing role. Identify whether you report business activity as a sole proprietor on Schedule C (Form 1040). For freelance workflows, this anchors where your business income or loss lives.

Outcome: You can point to the exact filing lane that supports your business-use-of-home review.

- Pull your decision references first. Keep IRS Topic No. 509 and Publication 587 open while you work. Topic 509 points you to Publication 587 for detailed business-use-of-home rules, so use them together as your baseline.

Outcome: You judge your facts against one consistent rule set, not memory.

- Build a substantiation folder you can defend. The IRS expects you to substantiate deductible expenses and keep adequate records. Create one folder with records that support each expense and your business-use-of-home position.

Outcome: Each claim you make has matching support you can retrieve quickly.

- Collect cross-border and payer forms that apply to you. Do not assume every form applies in every case. Keep the right tax-profile artifacts ready for your current client mix.

| Artifact | Use it for | Verification point |

|---|---|---|

| W-9 | Provide TIN details to payers that file information returns | Keep a copy in your files (commonly retained for four years in contractor workflows) |

| W-8BEN | Submit when a payer or withholding agent requests it | Confirm the request from the payer or withholding agent |

| Form 1099-NEC records | Reconcile reported nonemployee compensation with your books | Match records to your business income reporting |

If you use W-9 forms in contractor workflows, keep them in your files so you reduce mismatches before filing.

- Set your safe default before claiming tax savings. If any requirement stays unclear, mark the claim as Pause in your internal process and validate it before filing. This is not an IRS status, but it protects decision quality for globally mobile operators.

Outcome: You choose defensibility over guesswork.

Do you pass the binary eligibility gate right now?#

Pass this home office deduction gate only when you clear exclusive use, regular use, and principal place of business. With your prep folder ready, run a strict yes-or-no screen before you calculate anything. This keeps decisions objective and stops weak claims before you chase tax savings.

Run the gates in order#

| Gate | What to confirm | Verification point |

|---|---|---|

| Exclusive use | One specific area serves trade or business use only | Workspace boundary and daily use pattern stay business-only |

| Regular use | That specific area is used on a recurring basis for business use of home | Records show recurring use, not sporadic use |

| Principal place of business | Home anchors your most important activities and most of your business activity time | Activity summary shows home as your operating center, not a backup location |

| Exception check | Daycare facility or inventory storage exception applies only in limited cases | You can state exactly why one exception applies |

- Test exclusive use requirement. Mark Yes only when one specific area serves trade or business use only. Mark No when you use that same area for personal life, such as a den that also hosts family recreation.

Verification point: Your workspace boundary and daily use pattern stay business-only.

- Test regular use requirement. Mark Yes only when you use that specific area on a recurring basis for business use of home. Mark No when you use it only occasionally or rotate across casual spots without a consistent work zone.

Verification point: Your records show recurring use, not sporadic use.

- Test principal place of business. Mark Yes when home anchors your most important activities and most of your business activity time. If you perform administrative or management work at home and have no other fixed location for that work, home can still qualify.

Verification point: Your activity summary shows home as your operating center, not a backup location.

- Check exceptions only when facts match. The daycare facility exception and inventory storage exception can bypass exclusive use in limited cases. They do not create a blanket pass for unrelated setups, and other applicable requirements still need to be met.

Verification point: You can state exactly why one exception applies.

| Gate result | Meaning | Internal status tag |

|---|---|---|

| All required tests are Yes | Your home office deduction position looks defensible | Proceed |

| One test stays unclear | You need cleanup before filing | Pause |

| Facts conflict or stay gray | You should escalate for review | Escalate |

A consultant who runs delivery, invoicing, and planning from one dedicated desk is easier to evaluate under this gate than someone who alternates between a couch, kitchen table, and bed.

Tag your decision and move forward#

Use Proceed, Pause, or Escalate as internal workflow labels, not IRS labels. Move only a Proceed case into deduction calculation in the next step.

Does your apartment setup actually qualify under IRS logic?#

Your apartment can qualify for a renter home office claim when you define a bounded workspace and keep that area business-only in daily practice. If you passed the binary gate, use this section to make sure your claim matches the physical reality of how you work.

Run the apartment setup test#

- Map one clearly identifiable workspace. Mark the exact area you will claim for business use of home. Use a room or a separately identifiable part of a room. You do not need to build permanent walls, but you must draw a clear boundary you can explain.

Verification point: You can describe the boundary in one sentence and show it in photos.

- Stress test daily exclusivity with IRS logic. Use IRS Publication 587 to check whether personal use ever enters the claimed area. If the same area is used for both business and personal purposes, exclusive use is at risk.

Verification point: Your calendar, task logs, and physical setup all tell the same story.

- Run a shared-space risk check before filing.

| Setup pattern | Risk to exclusive use requirement | Safer move |

|---|---|---|

| Dedicated desk corner with clear business boundary | Low if you keep personal activity out | Keep personal items outside the boundary and document the layout |

| Kitchen table that also serves meals | High | Claim only a truly separated business-only portion or pause |

| Multipurpose bedroom workspace | Medium to high | Separate business furniture and keep nonbusiness use outside claimed area |

| Rotating work spots across the apartment | High | Consolidate work into one fixed claim area |

- Tag the setup outcome and decide next action. Use your internal Proceed, Pause, or Escalate label. If facts stay mixed, pause tax savings decisions and tighten the setup first.

A studio setup with one corner reserved only for client delivery and admin can qualify. A kitchen table that also serves meals is usually a pause signal unless you can truly separate a business-only portion.

If you want a quick next step for "home office deduction renter," try the home office deduction calculator.

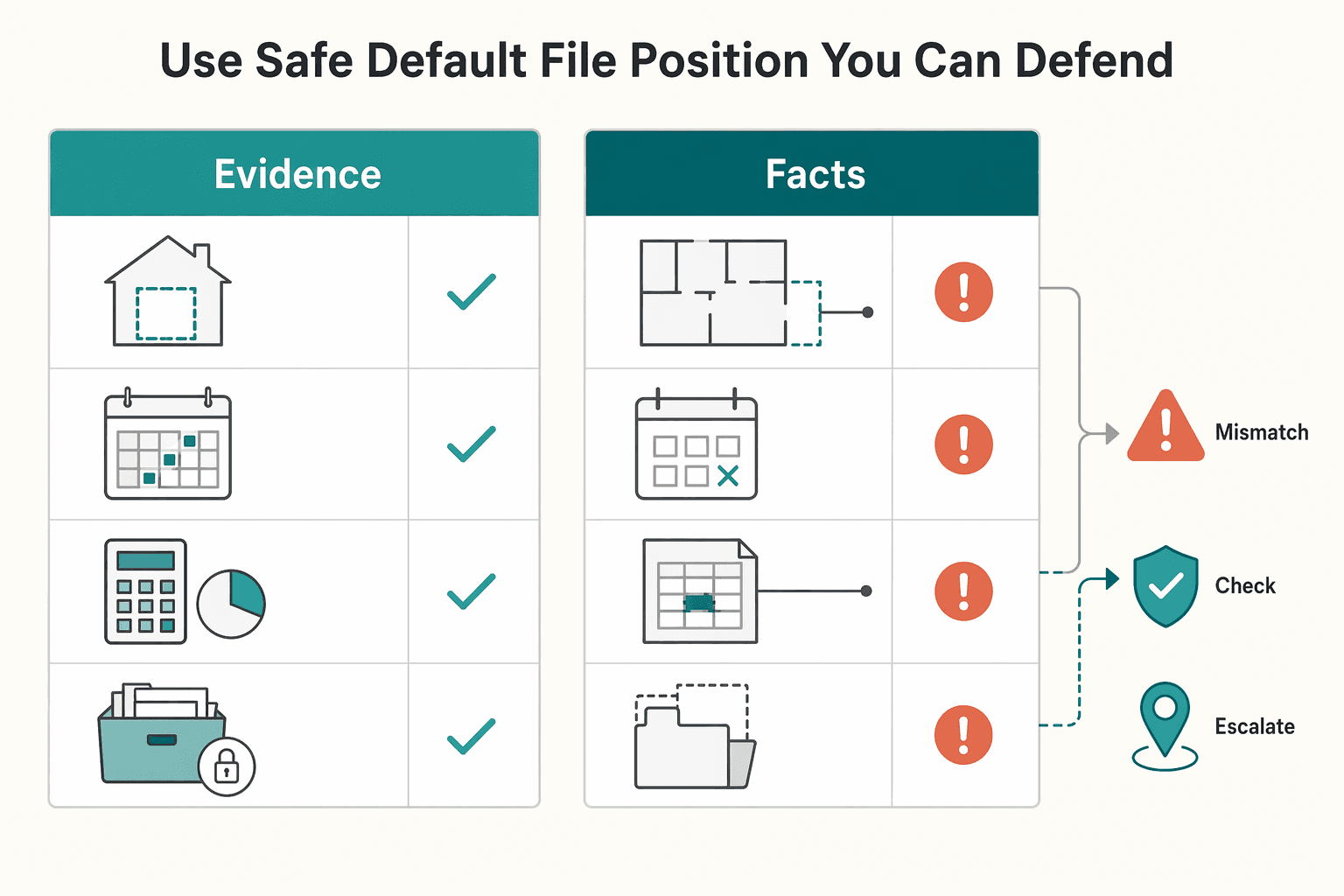

How do you build an audit-ready documentation pack without overcomplicating it?#

Build one monthly packet that ties workspace proof, expense support, and tax forms into a single traceable workflow. Eligibility is only half the game. Documentation is what turns an allowable claim into a defensible one.

Use a five-step monthly routine#

| Step | Action | Outcome |

|---|---|---|

| 1 | Create one recurring folder with workspace photos, layout notes, and monthly supporting records | Show how your deduction logic stays consistent across the year |

| 2 | Use Form 8829 to compute allowable home-office expenses, then tie that result to Schedule C | Home office deduction numbers flow cleanly into your return |

| 3 | Match income in your books to Forms 1099 and confirm W-9 details still align with your current tax profile | Catch mismatches early and reduce cleanup later |

| 4 | Keep Form 8938 review notes in your return support file, and track FBAR separately because you file FinCEN Form 114 outside the IRS return channel | Avoid category errors that derail a business-use-of-home review |

| 5 | Keep receipts, canceled checks, and other supporting records, using the general three-year assessment window as your baseline and extending retention when form-specific rules call for more time | Protect your position and retrieve records fast when questions come up |

- Step 1. Create one recurring folder for business use of home evidence. Add workspace photos, your layout notes, and the month's supporting records in one place. Keep Publication 587 in your review stack so you check each month against the same rulebook.

Outcome: You can show how your deduction logic stays consistent across the year.

- Step 2. Connect calculations to filing outputs. Use Form 8829 to compute allowable home-office expenses, then tie that result to Schedule C. If you used more than one home for the business during the year, prepare a separate Form 8829 for each home.

Outcome: Your home office deduction numbers flow cleanly into your return.

- Step 3. Reconcile payer records before filing season. Match income in your books to Forms 1099 and confirm W-9 details you gave payers still align with your current tax profile. If you pay contractors, check whether your business must issue Form 1099-NEC.

Outcome: You catch mismatches early and reduce cleanup later.

- Step 4. Split federal return files from cross-border trackers. Keep Form 8938 review notes in your return support file, and track FBAR separately because you file FinCEN Form 114 outside the IRS return channel. Form 8938 and FBAR can both apply, so track each obligation on its own line item.

Outcome: You avoid category errors that derail a business-use-of-home review.

- Step 5. Set practical retention and access controls. Keep receipts, canceled checks, and other records that support income and deductions. Use the general three-year assessment window as your baseline, then extend retention when form-specific rules call for more time. Organize files so supporting records are easy to retrieve.

Outcome: You protect your position and retrieve records fast when questions come up.

A globally mobile consultant who closes books monthly, updates one checklist, and tags anything unclear for follow-up is usually better positioned to file with fewer surprises. Related: How to Handle Taxes for a Side Hustle.

What changes if you are globally mobile or split across jurisdictions?#

Global mobility adds compliance layers, but it does not by itself decide a home office claim. Use the same federal eligibility logic, then run a separate mobility checkpoint so your federal, state, and foreign obligations do not collide.

Run the multi-jurisdiction control check#

| Step | Checkpoint | Outcome |

|---|---|---|

| 1 | Keep home office deduction logic in one track and cross-border reporting in another | Prevent category errors before filing |

| 2 | Ask where you perform your most important business activities and where you spend most business time | Defend why your claimed home remains your operating base |

| 3 | Treat FEIE as a separate analysis; the physical presence test uses 330 full days in any period of 12 consecutive months, and FEIE also requires your tax home to stay in a foreign country during the qualifying period | Keep home-office analysis and FEIE planning aligned without forcing them together |

| 4 | If California exposure exists, run a facts-and-circumstances review under FTB guidance and use a separate state worksheet | Reduce the chance of conflicting positions |

| 5 | Track Form 8938 and FBAR separately, and file FBAR with FinCEN instead of your IRS return package | Keep reporting obligations organized and complete |

- Step 1. Separate your decision tracks. Keep home office deduction logic in one track and cross-border reporting in another. Use business-use-of-home facts to test eligibility, then review FEIE, FBAR, and Form 8938 as separate obligations.

Outcome: You prevent category errors before filing.

- Step 2. Re-test principal place of business across locations. Ask where you perform your most important business activities and where you spend most business time. If you handle administrative or management work at home and have no other fixed location for that work, your home can still qualify.

Outcome: You can defend why your claimed home remains your operating base.

- Step 3. Run an FEIE overlap checkpoint. FEIE uses its own tests. The physical presence test uses 330 full days in any period of 12 consecutive months, and FEIE also requires your tax home to stay in a foreign country during the qualifying period. Do not treat FEIE status as an automatic pass or fail for your home office deduction.

Outcome: You keep home-office analysis and FEIE planning aligned without forcing them together.

- Step 4. Screen state residency risk early. If California exposure exists, run a facts-and-circumstances review under FTB guidance before finalizing tax decisions. Use a separate state worksheet so your residency position does not drift from your filing story. For a deeper state workflow, see Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?.

Outcome: You reduce the chance of conflicting positions.

- Step 5. Split foreign account filings from return filings. Form 8938 and FBAR can both apply. Track them separately, and file FBAR with FinCEN instead of your IRS return package.

Outcome: You keep reporting obligations organized and complete.

If you work across two countries and keep one US home office base, this is the checkpoint that keeps the story coherent across filings.

Common mistakes that trigger problems and how to recover fast#

Catch these five errors early so you can still file a defensible renter home office claim without forcing weak facts. Use this sweep right before filing to align your workspace story, your records, and your forms.

| Mistake | Recover fast | Verify before filing |

|---|---|---|

| Mixed-use space treated as deductible | Re-test the exclusive use requirement and pause if personal use exists | Claimed area supports only business use |

| Weak coworking narrative | Rebuild principal place of business support with activity logs | Home remains the center of important work and time |

| Rushed filing with thin records | Reconstruct evidence using Publication 587 structure | Records clearly support business use of home |

| Form mismatch across filings | Reconcile Schedule C, Form 1099, Form 8938, and FBAR workflow | Forms agree and deadlines are tracked |

| Forcing a gray-area claim | Escalate to a qualified pro and document why | Decision log explains pause or file choice |

- Re-test the workspace boundary against exclusive use. If you use the same area for personal life, stop the claim and mark it as Pause.

Outcome: You avoid submitting a home office deduction that fails on a basic rule.

- Rebuild your principal place of business narrative. Use a short weekly log of client delivery, planning, billing, and admin work. Coworking does not automatically disqualify you, but another fixed location for substantial admin or management work can.

Outcome: You can explain why your home office deduction stands.

- Reconstruct your documentation trail in defense order. Build it the same way you would explain it: workspace evidence, expense support, and filing tie-out under Publication 587. Keep each item traceable to your business-use-of-home claim.

Outcome: You file from records, not memory.

- Reconcile adjacent compliance forms before final submission. Put the deduction on Schedule C line 30, ensure relevant Form 1099 income aligns with Schedule C, and treat Form 8938 and FBAR as separate obligations. File FBAR with FinCEN when aggregate foreign accounts exceed $10,000, due April 15 with automatic extension to October 15. If state exposure complicates this workflow, review Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?.

Outcome: Your packet stays internally consistent.

- Escalate gray areas instead of forcing a deduction. Write a short decision note that states what is unclear and what triggered escalation.

Outcome: You protect compliance now and preserve options later.

Copy and paste renter home office compliance checklist#

Use this checklist to approve or pause your renter home office deduction before you file. Treat it like a go or no-go gate. Run each item in order, and if anything stays unclear, pause instead of forcing a filing for short-term tax savings.

- Confirm baseline eligibility.

- Verify you file as self-employed, since employees generally cannot claim this federal home office deduction. * Confirm you are claiming a defined area for ongoing business use of home. Outcome: You confirm whether your path is valid before you spend time on forms.

- Run the two core gates.

- Test the regular use requirement with real weekly usage, not intent. * Test the exclusive use requirement and stop if personal use overlaps, unless a specific exception applies. Outcome: You protect your position by removing weak claims early.

- Validate principal place of business with written proof.

- Write a short operations summary that explains where you do your most important work. * Keep weekly activity evidence for delivery, planning, billing, and admin tasks. * If you take meetings in coworking but run operations from a dedicated home desk, document that pattern. Outcome: You build a defensible narrative instead of a vague story.

- Check exception status only when facts clearly match.

- Review the daycare facility exception or inventory storage exception only if your business actually fits those use cases. * Do not retrofit your facts to an exception. Outcome: You avoid overreaching on eligibility.

- Assemble forms and support in one packet.

- Use Form 8829 to compute allowable home-office expenses for Schedule C. * Report the business-use-of-home deduction on Schedule C line 30. * Reconcile nonemployee compensation (including 1099-NEC where relevant) to Schedule C, and keep your Publication 587 support notes with the file. * Keep records for the required retention window (3 years from return due date or filing date, and 2 years from tax payment date where applicable). Outcome: Your deduction and income reporting stay consistent.

- Reconcile cross-border workflows before you file.

- If FEIE applies, run it through Form 2555 with your return workflow. * Attach Form 8938 to your annual return when required. In general, reporting starts above $50,000, though some thresholds are higher. * Treat FBAR as a separate filing duty when otherwise required. Form 8938 does not replace FBAR. * If state exposure overlaps with mobility, review Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?. * If any item remains uncertain, pause and escalate to a qualified pro. Outcome: You file from a compliance-first position, not a guess.

Use the safe default and file from a position you can defend#

Use a defensible filing standard: claim the deduction only when eligibility, math, and records all line up. Define success as a claim you can explain later, not the largest possible write-off. The home office deduction has specific requirements, and deductible amounts may still be limited even when you qualify. Use your checklist to make a clear go-or-pause decision before filing.

- Choose defensibility before optimization.

- Confirm your claimed area meets the exclusive and regular use tests for business use of home. * Apply the same eligibility standard whether you use actual expenses or the simplified option. The simplified option can reduce calculation and recordkeeping burden, but it does not change who qualifies. * Gross income limitation is a cap: you may not deduct business-use-of-home expenses above that limit. Outcome: You remove weak assumptions before filing.

- Lock your records before submission.

- Keep canceled checks, receipts, and other evidence supporting each amount. * Keep your calculation trail and eligibility notes together so your file stays consistent. * Follow practical retention windows: 3 years from the return due date or filing date, and 2 years after tax payment when that rule applies. Outcome: You can support your position with records, not memory.

- Apply a strict go-or-pause rule.

| If this condition is true | Action | Safe-default reason |

|---|---|---|

| Eligibility is clear and records are complete | File | Your claim is explainable end-to-end |

| Eligibility is unclear or records have gaps | Pause and escalate early | You avoid forcing an uncertain position |

| Facts are still ambiguous for your filing context | Pause and reconcile first | Unresolved uncertainty is a compliance risk |

If you want one operating script, use this: proceed only when your facts, calculations, and documentation agree. If they do not, pause and escalate before filing to protect long-term compliance over short-term tax savings. For state-overlap questions, review Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?.

If you want a deeper dive, read Moving From Hourly to Project-Based Rates. Want a compliance-first workflow with audit-ready records where supported? Talk to Gruv.

Frequently Asked Questions

Can renters claim a home office deduction, or is it only for homeowners?

Renters can claim it if they meet the IRS rules. The home office deduction applies to both homeowners and renters, so the renter claim works when you pass the tests. Treat it as a compliance decision, not an automatic deduction.

Does a small apartment qualify if I do not have a separate office room?

Yes. You can use a whole room or part of a room for business use of home, as long as you satisfy the rule tests. The IRS definition of home includes an apartment.

What does regular and exclusive use mean in real day to day terms?

Regular use means you use the area for business consistently, not occasionally. Exclusive use means you use that same area only for business when exclusivity applies. If you use the space for both personal and business activity, you fail that gate unless a listed exception applies.

What counts as principal place of business if I also use coworking spaces?

Focus on where you perform your most important activities and where you spend most of your business time. Using coworking space does not automatically disqualify your home office deduction. Your home may still qualify as a principal place of business when you handle administrative or management work there and no other fixed location handles substantial administrative or management activities.

When should I not claim the deduction even if I work from home often?

Do not claim when you fail the regular or exclusive use requirement and no exception fits your facts. Also do not claim when non-home business deductions exceed gross income from qualified home use. If facts stay unclear, pause and escalate before filing.

What records should I keep to support my claim in case of review?

Keep records that provide the information needed to figure your deduction for the business use of your home. Keep the same records you used to make your proceed or pause decision so your story stays consistent. If you use the simplified method, track area clearly because it uses $5 per square foot up to 300 square feet, with a maximum $1,500 deduction.

When do daycare and inventory storage exceptions apply?

These exceptions apply only in specific cases, and they can remove the exclusive use requirement. Inventory storage requires that your dwelling unit is the sole fixed location of that business for storage use. Use these paths carefully, document facts tightly, and avoid stretching them for extra tax savings.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?

Living abroad does not end `state income tax` exposure by itself. The first decision is practical: choose a filing position your facts can support, then build records that support the same story all year.

Moving From Hourly to Project Rates Without Hurting Cashflow

The right pricing model matches uncertainty and cashflow risk. It should fit how clearly the work can be defined, approved, and defended, not just what you are used to selling. Hourly billing gives you room to work while requirements are still moving. Fixed project pricing gives the client stronger budget clarity once deliverables are stable enough to pin down.

How to Handle Taxes for a Side Hustle

If you want less stress at filing time, use sequence instead of shortcuts. When one year includes payroll income, contractor income, and time in more than one country, the order of operations matters. This guide gives you a defensible path so you can make each decision once, document it, and avoid rebuilding the return later.