Quick Answer

Use a three-phase process before accepting work: verify the client’s legal identity in official records, set enforceable payment terms, and confirm billing compliance before kickoff. Practical checkpoints like W-9 or W-8BEN-E collection and a documented invoice route prevent many delays. If records do not align or the paying entity stays unclear, pause and request clarification instead of starting delivery.

For independent professionals, the biggest financial risk is rarely a lack of opportunity. It is taking on a new client whose payment process is shaky, slow, or hard to verify. Time spent chasing late invoices or untangling a messy accounts payable process cuts directly into margin.

The fix is not optimism. Use a repeatable process to check the client, set terms that protect your cash flow, and lock down the payment path before you do meaningful work. This three-phase approach helps you act less like a vendor hoping things work out and more like an owner protecting the business.

Phase 1: The Pre-Contract Intelligence Briefing#

Before you price the work, decide whether this prospect should even reach contract stage. Treat this as a go or no-go checkpoint based on records you can verify. Is the legal entity real? Is it the same entity that will sign and pay? Do public records show patterns you should not ignore?

Before you start#

Collect the company name exactly as it appears in the prospect's email signature, website footer, proposal request, and any draft purchase order. That helps you catch an early mismatch. You may negotiate with a brand name, then end up invoicing a different LLC or affiliate.

Step 1. Verify the exact legal entity and current status#

Start with the relevant business registry. In the US, use the state business entity database for the formation state. In the UK, use Companies House to review the registered office, filing history, officers, charges, and business activity.

Check the registry entry for:

- Exact legal name

- Entity number

- Jurisdiction

- Registered address

- Officer or director names

Caution signals:

- Website name and registry name do not match

- Name-search result appears, but current status is unclear

- Sudden director or address changes

Next action:

- Ask which entity will sign the contract and pay invoices

- If the engagement is material or cross-border, request an official certificate of good standing when needed. An online status lookup is not the same as an official certificate

A registry match confirms registration. It does not tell you whether the company is financially healthy or actively trading. Use it to confirm identity, not to make the whole credit decision.

Step 2. Review filing-based financial signals when filings exist#

When filings are available, use them to see whether the client's public story matches the risk you are taking. If the prospect is public, EDGAR should be your starting point.

| Filing | What it covers | Timing note |

|---|---|---|

| Form 10-K | Audited annual financials and risk factors | Review the latest filing |

| Form 10-Q | Quarterly updates | A missing 10-Q may still be within deadline: 40 days after quarter-end for large accelerated and accelerated filers, and 45 days for other registrants |

| Form 8-K | Material events | Recent filings can appear quickly, often within four business days |

Review these filings:

- Latest Form 10-K, including audited annual financials and risk factors

- Latest Form 10-Q for quarterly updates

- Recent Form 8-K filings for material events

Check recency before you read too much into a gap. A missing 10-Q may still be within deadline: 40 days after quarter-end for large accelerated and accelerated filers, and 45 days for other registrants. If risk language keeps showing up, or you see a cluster of recent 8-K filings tied to material events, treat the prospect as a request-clarification case. Then plan tighter payment terms in Phase 2.

Step 3. Check court records and secured-creditor signals#

Court and lien records help if you read them as patterns, not headlines. Search PACER for federal cases tied to the exact legal entity and obvious affiliates. For light screening, PACER is often manageable at $0.10 per page, capped at $3 per document, with fees waived if total quarterly charges are $30 or less. Also review UCC lien filings through the relevant Secretary of State office.

A single lawsuit or UCC filing does not prove payment risk. What matters is repetition: repeated disputes, repeated collection issues, or a broader pattern of payment friction. When you see that, stop assuming and ask for clarification before you proceed.

| Signal source | Reliability | Common false positives | Recommended follow-up |

|---|---|---|---|

| State registry or Companies House | High for identity/status | Registered but inactive entity, outdated details | Confirm exact contracting/payor entity; request official good-standing proof if needed |

| EDGAR (10-K, 10-Q, 8-K) | High for public companies | Timing gaps, complex group structures | Check filing dates, then read recent filings in sequence |

| PACER and UCC filings | Medium to high when pattern-based | Routine litigation, secured financing not tied to distress | Look for repeated disputes and match records to the exact entity |

| Business credit report | Medium | Opaque reporting and scoring | Cross-check against registry, filings, and court records |

Step 4. Use business credit reports as a secondary screen#

Business credit reports can help, but keep them in a supporting role. Treat them as one input, not the final call. Reporting can be opaque, and protections are not the same as in consumer credit reporting.

If a report conflicts with registry data, public filings, or court records, trust the underlying records first. Before you move to Phase 2, run the prospect through this triage checklist:

- Proceed: legal entity is consistent across records, status checks are clean, and no meaningful dispute pattern appears.

- Request clarification: names do not align, records are incomplete, or filing and court signals are mixed.

- Decline: prospect will not identify the paying entity, records show repeated payment-friction patterns, or explanations keep changing.

If you want a deeper dive, read The Silent Profit Killer: How to Stop Margin Erosion in Your Freelance Business.

Phase 2: Building Your Financial Moat with a Bulletproof Contract#

Your contract should protect cash flow, not just describe the work. Once Phase 1 says proceed or request clarification, Phase 2 turns that judgment into controls you can actually enforce.

Before you finalize terms, do a simple resilience check: how much protection do you have now, and how quickly can you rebuild it if something goes wrong? Keep it practical. If one disruption would materially hurt your financial position, your contract should not leave you carrying extended unpaid delivery risk.

Exact contract numbers and legal mechanics (for example deposit size, billing interval, late-fee rate, and termination formula) are not fixed by this framework and should be verified for your context.

Step 1. Lock in upfront payment before meaningful work begins#

If you do not collect money before meaningful work starts, you may be financing the project yourself. Upfront payment is both a commitment signal and a risk-allocation tool.

Use your risk tier instead of one universal number. Tighten terms when Phase 1 signals are mixed. Relax them only when risk is clearly lower and other controls still hold.

If the client resists prepayment, do not drop the protection entirely. Use a fallback structure instead:

- Start with a smaller paid discovery or kickoff phase

- Schedule work only after payment clears

- Break phase one into a limited paid block before larger commitments

Before work starts, verify that the same legal entity appears across the signed agreement, invoice setup, any purchase documentation, and payment onboarding.

Step 2. Tie payment triggers to concrete milestones, not goodwill#

Vague billing language creates avoidable arguments. Tie payment to events you can point to and prove. "Phase complete" can be too loose. A defined approval action in email or the project system is easier to enforce.

If the client needs calendar-cycle processing, you can align dates without giving up protection. Set an acceptance window and keep pause rights for missed payments where your agreement allows. Otherwise, you can end up delivering while their internal approval process stretches out.

For each billing event, keep lightweight proof of:

- relevant SOW scope line

- deliverable list

- client approval record

- invoice submission confirmation

Step 3. Write late-payment language that gives you a remedy#

Late-payment language matters only if it changes what happens in practice. State the due trigger clearly, then spell out the remedies: pausing work, withholding further deliverables, or shifting timelines when payment is overdue.

Use your current standard payment timing. If late charges get negotiated down, keep the operational remedies intact. Those remedies are often what protect you when payment slows.

Also define invoice receipt mechanics clearly: when an invoice is deemed received, where it must be sent, and who must receive it.

Step 4. Protect yourself if the project stops early#

Termination terms can hide unpaid work. If the client can stop for convenience, the contract should still cover completed work, approved milestones, unpaid invoices, and capacity you already reserved.

If the client pushes back on a specific termination fee, tighten the mechanics instead. Make payment for work performed and non-cancelable commitments explicit. Flexibility around stopping can be reasonable. Unpaid cancellation risk is not.

| Contract term | Risk it reduces | Common client objection | Your professional response |

|---|---|---|---|

| Upfront payment | Starting with no cash buffer | "We do not prepay vendors." | "Then we can begin with a smaller paid kickoff and schedule full delivery after payment clears." |

| Milestone billing | Extended exposure between delivery and payment | "We only pay on fixed AP cycles." | "We can align dates to your cycle, but acceptance triggers and pause rights need to stay explicit." |

| Late-payment language | Overdue invoices becoming normal operating behavior | "Our legal team will not accept penalties." | "Then we need clear overdue remedies, including pause rights and delivery holds, so risk does not shift to me." |

| Termination protection | Sudden stop leaving unpaid work or reserved capacity | "We need freedom to stop at any time." | "You can stop, but the agreement should still pay for completed work and committed capacity already reserved." |

Before signing, confirm these minimum viable contract controls:

- the paying legal entity is explicit and consistent with Phase 1 verification

- upfront payment is stated and tied to the start of meaningful work

- milestone triggers are specific and easy to prove

- invoice due timing is written clearly

- overdue-payment remedies are operational, not just rhetorical

- termination terms cover completed work, unpaid invoices, and reserved capacity

Before you send terms, draft your payment and termination clauses in one place with the Freelance Contract Generator.

Phase 3: Fortifying Compliance and Automating Payment#

This is where many payment problems become avoidable. Do the admin in order before you send the first invoice: verify legal and tax identity, confirm invoice readiness, then choose the payment setup. Most friction here comes from bad entity data, missing tax forms, or AP rejection, not weak contract language.

Step 1. Request the right tax and entity documents first#

Get the client's exact legal name, registered address, and tax details before billing setup starts. If the payer is a U.S. person or U.S. business, request a completed Form W-9 so you have the correct TIN for reporting.

| Item | Use when | Note |

|---|---|---|

| Form W-9 | The payer is a U.S. person or U.S. business | Use it so you have the correct TIN for reporting |

| W-8BEN-E | You are in a U.S. withholding or reporting context with a foreign entity | Use W-8BEN-E for entities |

| W-8BEN | You are in a U.S. withholding or reporting context with an individual | Individuals use W-8BEN, not W-8BEN-E |

| VAT number in VIES | EU invoicing when applicable | Collect the VAT number and validate it in VIES |

| UK GB VAT number | You are handling the UK edge case | VIES does not validate UK GB numbers from 01/01/2021, so a VIES miss is not automatically a UK compliance failure |

If you are in a U.S. withholding or reporting context with a foreign entity, use W-8BEN-E. Individuals use W-8BEN, not W-8BEN-E.

For EU invoicing, collect the VAT number and validate it in VIES when applicable. EU VAT invoice content rules under Article 226 expect clear VAT identification fields. Also handle the UK edge case correctly: VIES does not validate UK GB numbers from 01/01/2021, so a VIES miss is not automatically a UK compliance failure.

Step 2. Confirm invoice readiness before submission#

Many invoice delays start with avoidable setup mistakes. Before you submit an invoice, run this pre-invoice checklist:

| Check | What to confirm | Why it matters |

|---|---|---|

| Entity match | The legal entity matches exactly across contract, vendor setup, and invoice | Bad entity data can cause silent delays |

| Billing route | The billing contact and invoice submission mailbox are confirmed | If the client cannot confirm routing, pause and get written invoicing instructions first |

| PO status | The PO workflow is confirmed, and the PO number is open and valid if required | AP teams can reject invoices for missing or invalid PO data |

| Required fields | Unique invoice number, invoice date, supply date if needed, service description, charges, and tax or VAT fields if applicable | In the U.S. federal context, a noncompliant invoice can be returned within 7 days under FAR 32.905 |

This is where you prevent silent delays. If the client cannot confirm routing or required fields, pause and get written invoicing instructions first.

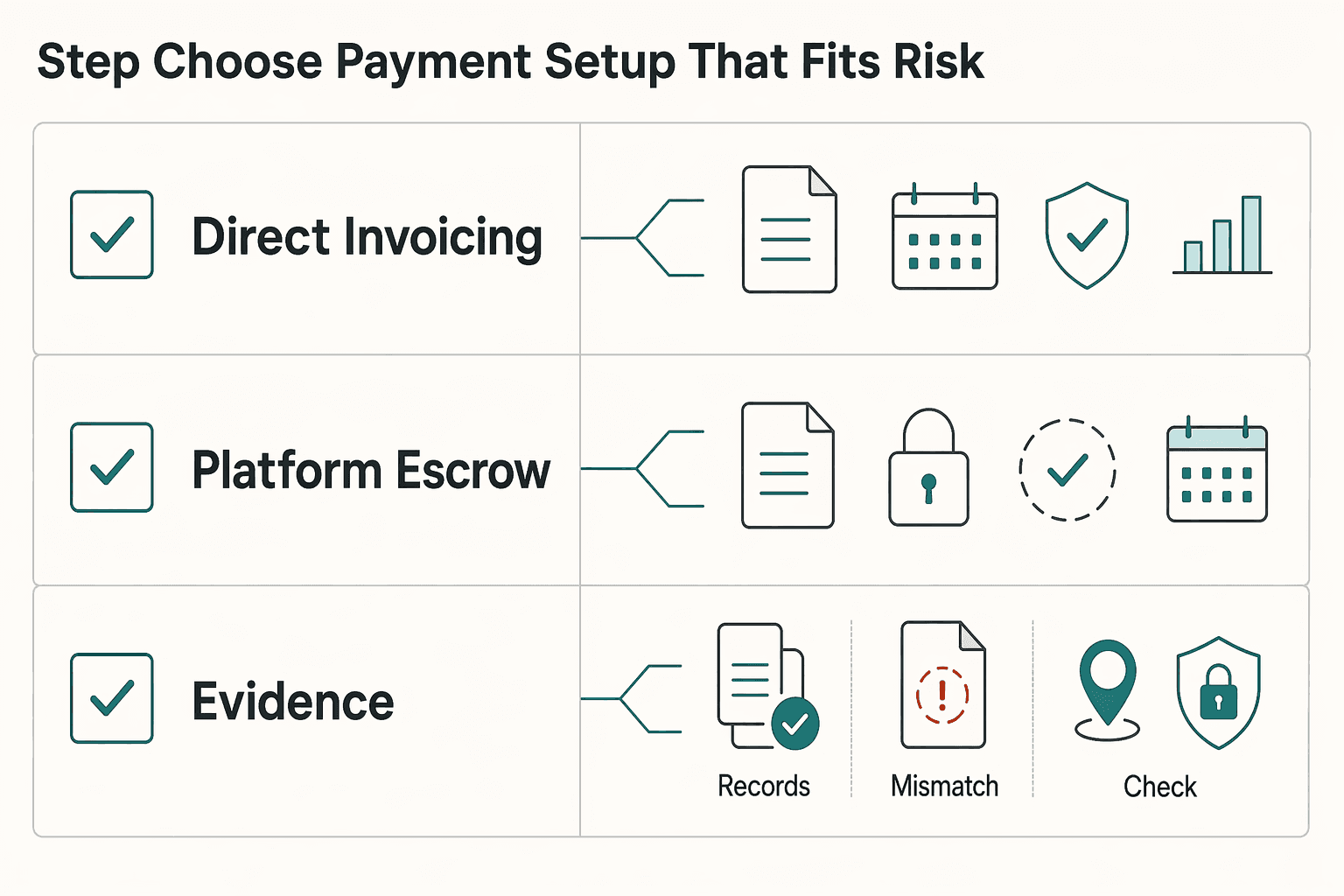

Step 3. Choose the payment setup that fits the risk#

Once your entity and invoice data are clean, choose the payment setup that matches the risk and the operational burden you are willing to carry.

| Setup | Compliance burden | Cash-flow predictability | Dispute handling | Operational overhead |

|---|---|---|---|---|

| Direct invoicing | Highest on you | Lowest to medium | You handle follow-up and collections | Low to medium |

| Platform escrow | Medium | Medium if milestones are pre-funded and submitted correctly | Platform support helps, but payment is not guaranteed in every case | Medium |

| Merchant of Record | Lower on tax and transaction handling | Medium to higher | Provider usually handles payment processing, refunds, and chargebacks | Medium to high |

Use direct invoicing when your controls are already strong and the client process is reliable. If risk still feels high after Phase 2, escrow or a Merchant of Record can shift part of the transaction and compliance burden, but neither removes the risk. Treat a MoR as one risk-management option with tradeoffs, and choose providers carefully because they take legal and compliance responsibility for the transaction.

Conclusion: You Are the CEO - Act Like One#

You do not need a corporate title to make CEO-level decisions. You need a repeatable policy. When you are wearing many hats, inconsistent decisions across intake, contract terms, and invoicing increase payment risk.

Step 1: Screen before you commit. Use Phase 1 to make a clear go or no-go decision from verified information. Confirm identity, match billing details across channels, and note what has actually been verified before you share sensitive details.

Step 2: Set contract controls before delivery starts. Use Phase 2 to define payment triggers, invoice timing, approvals, and what happens if work pauses or payment stalls. If a client pushes back on core controls, treat that as decision data and reduce exposure or decline the work.

Step 3: Lock the payment and compliance workflow before kickoff. Use Phase 3 to document invoice routing, required documents, billing owner, and escalation contacts before any delivery starts. If that path is unclear, delay kickoff until it is documented.

| Key moment | Reactive freelancer approach | Policy-led business owner approach |

|---|---|---|

| Intake | Starts from urgency and fills gaps later | Verifies first, logs checks, then decides |

| Contract terms | Accepts vague terms and revisits later | Sets payment controls before work begins |

| Invoicing | Sorts out process after delivery | Confirms route, owner, and required documents before kickoff |

| Escalation | Chases delays ad hoc | Follows a defined escalation path |

Adopt this operating standard now: no verified client, no signed terms, no documented billing path, no start.

For a step-by-step walkthrough, see The Best Tools for Performing a Background Check on a New Client. If you want a cleaner handoff from signed contract to compliant collection and payout tracking, review Gruv for Freelancers.

Frequently Asked Questions

How can you check a client’s financial stability?

Start with verifiable information and define what you are checking. A practical definition of financial stability is the ability to meet current and future obligations, usually supported by steady income, manageable debt, and a savings buffer. Use official, secure sources for any checks and avoid conclusions based on a single datapoint.

How do you vet a client without asking for financial statements?

Begin with source verification before requesting private documents. Confirm that sources are official and secure (https:///lock icon, and .gov for U.S. government pages) before relying on them or sharing sensitive information. If confidence is still low, proceed cautiously and consult your own advisers.

What counts as a warning signal versus a verification step?

A warning signal is a request for your online banking password, access codes, or security verification details by phone, email, or text. A verification step is confirming the source is official and secure before sharing sensitive information, and checking privacy/security policy differences when an external link takes you to another site.

What contract controls actually reduce non-payment risk?

This grounding pack does not validate a specific set of contract terms as universally effective. Keep terms clear in writing, and use your own legal, tax, accounting, or financial advisers for guidance on contract design.

Is it rude to ask a client about financial stability?

It is usually better to frame questions as standard verification and security checks, not personal judgments. Ask through official channels, and share sensitive information only on official, secure websites.

How do you know if a potential client is legitimate?

No single signal proves legitimacy. Verify information through official, secure sources before acting, and be careful with external links because privacy and security policies may differ.

What if the client seems real, but the payment process is messy?

Treat unclear process details as unresolved risk and slow down until instructions are clear in writing. If anyone asks for passwords, access codes, or security verification details by phone, email, or text, stop and treat it as a warning signal.

Can one source decide whether you should move forward?

No. One source should not decide the outcome. Cross-check with official, secure sources, and consult your own advisers when legal, tax, accounting, or financial decisions are involved.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- acquisition.gov/far/32.905trusted

- ada.gov/law-and-regs/regulations/title-ii-2010-regul...trusted

- corp.delaware.gov/onlinestatustrusted

- dos.ny.gov/corporation-and-business-entity-search-databasetrusted

- ftc.gov/news-events/news/press-releases/2025/06/padd...trusted

- ftc.gov/news-events/news/press-releases/2023/03/ftc-...trusted

- icis.corp.delaware.gov/ecorp/entitysearch/namesearch.aspxtrusted

- investor.gov/introduction-investing/getting-started/resea...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Stop Freelance Profit Margin Erosion Before It Hits Cashflow

Revenue can hold steady while the business underneath it gets weaker. What comes in matters, but what you keep after the work is delivered is the clearer signal of health.

Canada Digital Nomad Visa Planning for Visitor Status and Work Permits

The phrase `canada digital nomad visa` is useful for search, but misleading if you treat it like a legal category. It is shorthand for existing Canadian status options, mainly visitor status and work permit rules, not a standalone visa stream with its own fixed process. That difference is not just technical. It changes how you should plan the trip, describe your purpose at entry, and organize your records before you leave.

How to Get a National Insurance Number (NINO) in the UK

Start with a simple sequence: check whether you already have a National Insurance number, submit one first application only if you need it, then keep your NINO, UTR, and share code in separate lanes. Many setup problems come from document mix-ups rather than difficult legal edge cases.