Quick Answer

Run a three-part audit: check margin leakage, rank client risk, and review cognitive load. In Toggl Track, use Detailed Report for entry proof, Summary Report for mix patterns, and Profitability Report on Premium for revenue-minus-cost cuts. Tag admin, scope-creep, and rework consistently so hidden costs stay visible. For fixed-fee work, keep the date window aligned to fee cadence before you change pricing or scope.

The CEO's Audit: A 3-Pillar Framework for Mastering Your True Project Profitability in Toggl Track#

Use this audit to make three decisions: whether your pricing is working, which clients or project types to repeat, and whether your workload is sustainable.

Toggl Track can support those calls once you move past total hours. Its Profitability Report breaks results down by member, project, client, task, and tag, and defines profit as revenue minus cost. That gives you a solid core metric, but you still need to review where time actually goes to interpret that number correctly.

A profitability audit is different from basic time logging:

| View | Focus | Inputs | Decisions enabled |

|---|---|---|---|

| Detailed Report (time-entry view) | Hours and entries | Time entries | Time-entry audit, billable-hour checks, invoice prep |

| Profitability audit | Revenue, cost, profit, and work mix | Time entries, billable rates, labor costs, project/client/tag structure | Pricing updates, client/project selection, staffing and budgeting choices |

Before you run it, make sure your setup is ready: billable rates and labor costs should be configured, and the Profitability Report is available on Premium.

Run the audit in three pillars, each with one outcome and one primary signal:

- CFO pillar

Outcome: find margin leakage. Primary signal: profit plus billable vs non-billable mix by project, client, or tag.

- Risk pillar

Outcome: identify client work that consumes effort without enough return. Primary signal: client-level profitability, then Detailed Report entries when you need proof at the time-entry level.

- CEO pillar

Outcome: protect workload sustainability. Primary signal: where hours cluster across projects and non-billable buckets over time.

For fixed-fee projects, keep your date range aligned with the fee cadence. Short windows can distort profitability.

This only works if the underlying setup is clean, so start with rates, labor costs, and a project/client/tag structure that keeps billable and non-billable work easy to analyze. Once that foundation is solid, the three-pillar audit becomes reliable.

Related: How to Manage Project Profitability for Your Agency.

The Foundation: Setting Up Toggl Track for CEO-Level Insights#

If you want this data to drive decisions, set the structure first. Without a clear profit model and a consistent setup, reporting stays reactive.

| Step | Focus | Key practice |

|---|---|---|

| 1. Define your profit model | Profit model | Document assumptions and review them on a fixed cadence |

| 2. Standardize project initiation | Kickoff setup | Define success, key deliverables, and budget sub-items |

| 3. Stop rebuilding the process every time | Workflow consistency | Use one repeatable setup framework |

| 4. Keep reporting tied to the model | Reporting discipline | Review results against the same model and kickoff artifacts |

Step 1: Define your profit model before execution#

Write down how each project is expected to generate revenue, absorb costs, and produce profit. Keep the model explicit so planning stays strategic instead of reactive.

Keep two controls in place:

- Document the assumptions you will use across projects.

- Review those assumptions on a fixed cadence so reporting stays comparable over time.

Step 2: Standardize project initiation#

Treat initiation as a required setup stage, not a quick handoff. At kickoff, define:

- what success looks like

- the key deliverables (final outcomes and milestones)

- the budget broken into sub-items

This gives you a shared baseline before execution starts.

Step 3: Stop rebuilding the process every time#

A common failure mode in creative work is weak structure, especially when each project is treated as a one-off. Use one repeatable setup framework so you are not rebuilding core process decisions from scratch each time.

Step 4: Keep reporting tied to the model#

As work progresses, review results against the same model and kickoff artifacts. The goal is to see why outcomes are on track or off track so follow-up decisions stay strategic.

| Area | Basic setup | Profitability-ready setup |

|---|---|---|

| Profit model | Implicit or undefined | Documented before execution |

| Project initiation | Minimal setup | Success definition, deliverables, and budget sub-items defined upfront |

| Workflow consistency | One-off project setups | Repeatable structure used across projects |

| Reporting visibility | Activity logs only | Results interpreted against the same model and setup artifacts |

| Decision quality | Reactive interpretation | More strategic, structure-based decisions |

You are ready for Pillar 1 when:

- your profit model is documented and current

- kickoff notes consistently include deliverables and budget sub-items

- teams use a repeatable setup instead of rebuilding process from scratch

- reporting can be explained against the same model and initiation assumptions

You might also find this useful: A Guide to Time Tracking Software for Billable Hours.

Pillar 1: Quantify the Invisible Costs Draining Your Business (The CFO Pillar)#

This pillar should give you one thing: a clear view of where margin is leaking before a project looks obviously bad. The goal is not just to spot hidden cost, but to decide what to change in pricing, scope, or client handling.

| Cost signal | Track it as | Where to review | Next move |

|---|---|---|---|

| Admin tax | Non-billable support work, especially admin and client communication, with consistent tags | Summary Report weekly, then Profitability Report monthly | Adjust pricing or packages; tighten communication cadence; or price in more management overhead |

| Scope creep | scope-creep plus `SC | ...` descriptions, or a dedicated change-work task | Detailed Report for entry proof, then Profitability Report by task or tag |

| Fee erosion outside reported profit | Reported profit in Toggl plus adjusted profit in a closeout sheet or finance note | Processor and bank settlement records | Reprice, change payment method, or reassess client fit |

| Rework | rework entries with clear descriptions | Detailed Report, then Profitability Report by task, project, client, or tag | Fix briefs or handoffs, or tighten revision and response rules |

Step 1: Measure admin tax before it becomes a pricing blind spot#

Admin time can become expensive before it looks dramatic in a report. Track non-billable support work, especially admin and client communication, with consistent tags. Then use Summary Report for billable hours and billable percentage, and Profitability Report to see where admin time clusters by client, project, task, or tag.

Action loop

- Track: tag admin-heavy entries as you log them.

- Find: review weekly in Summary Report, then monthly in Profitability Report views.

- Decide: if admin is spread across clients, adjust pricing or packages; if it clusters, tighten your communication cadence or price in more management overhead.

Margin can erode before a project looks unprofitable, so run a quick quality check in Detailed Report for one sample week: do admin entries have the right tags and billable status? If not, fix entry discipline before you trust the ratio.

Step 2: Make scope creep reviewable the day it appears#

If you wait until closeout to mark scope creep, you can lose the evidence you need. Log it when the request arrives, not later. Use one repeatable rule: apply scope-creep and start descriptions with SC | ..., or route it to a dedicated change-work task if that fits your project method.

Action loop

- Track: create or edit the entry before you start the extra work; set billable status per your contract rule.

- Find: use Detailed Report for entry-level proof, then Profitability Report totals by task or tag.

- Decide: escalate when estimates are nearing alert thresholds, then confirm a change fee or defer the remaining requests.

Keep review conversations anchored in evidence: original deliverables, tagged entries, and the current estimate position. That protects margin and keeps client conversations clearer.

Step 3: Capture fee erosion outside reported profit#

Treat Toggl profit as your operating view, not your final cash view. Reported profit reflects revenue minus tracked labor cost, but payment processing and cross-border costs can still reduce what you keep.

Action loop

- Track: keep reported profit in Toggl and adjusted profit in your closeout sheet or finance note.

- Find: pull processor and bank settlement records for actual fees.

- Decide: if a payment route repeatedly compresses margin, reprice, change payment method, or reassess client fit.

Verify current processor and FX fees before you use them in decisions, and keep placeholders in your sheet until they are confirmed.

Step 4: Measure rework where it starts#

Rework should be visible as its own cost signal, not buried inside normal delivery time. Tag time spent on avoidable corrections, unclear feedback loops, or extra revisions outside the original plan with rework.

Action loop

- Track: log rework entries with clear descriptions.

- Find: inspect entries in Detailed Report, then compare totals by task, project, client, or tag in Profitability Report.

- Decide: if rework clusters by task type, fix briefs or handoffs; if it clusters by client, tighten revision and response rules in the next scope.

For fixed-fee work, align the report range with the fee cadence because short windows can distort interpretation.

| Input | In Toggl reported profit | In your adjusted profit review |

|---|---|---|

| Revenue from billable rates or fixed fee | Yes | Yes |

| Labor cost from tracked hours and cost rates | Yes | Yes |

| Admin, scope-creep, and rework hours if tracked | Yes, through time cost and revenue impact | Yes |

| Payment processor fees | No verified basis to assume included | Yes, add from settlement records |

| International card surcharges and currency conversion costs | No verified basis to assume included | Yes, add from actual fee documents |

| Fixed-fee timing effect on short date windows | Can distort interpretation | Check date range against fee cadence |

Before moving to Pillar 2, run this CFO checkpoint list:

- Confirm labor costs are set correctly so tracked hours produce meaningful cost data.

- Check one recent project in Detailed Report and verify

admin,scope-creep, andreworktags are consistent. - Review fixed-fee projects on a date range that matches fee cadence, not an arbitrary short window.

- Keep one closeout evidence pack: original scope, tagged time entries, invoice amount, and actual processor or FX fee records.

This pairs well with our guide on Using Airtable for Freelance Project Management That Stays Reliable.

Before you change pricing, run your latest project totals through the payment fee comparison tool to see how processing and conversion costs affect real margin.

Pillar 2: Are Your Best Clients Secretly Your Riskiest? (The Chief Risk Officer Pillar)#

Revenue on its own can mis-rank clients. What matters is risk-adjusted profitability: which clients give you dependable delivery profit with manageable operating risk.

Start by normalizing the money view before you compare clients. If a project includes pass-through expenses, treat those amounts as not truly yours, then compare clients using Agency Gross Income, delivery profit, and delivery margin. That keeps a high-invoice client from looking stronger than a client with cleaner margins and less drag.

Step 1: Build a simple client scorecard#

Keep the scorecard simple enough to maintain. Use one row per client with two lanes: profitability signals from tracked time and behavior signals from your operating records. Keep the lanes separate so you can tell whether a client is financially strong, operationally risky, or both.

For profitability, reuse the Pillar 1 inputs: delivery profit, delivery margin, admin-heavy time, scope-creep, and rework. For behavior, track what you can verify consistently: payment behavior, communication overhead, approval friction, and process adherence.

If you want numeric scoring, define it first and keep it stable across review cycles. Add a note like [define and verify scoring scale, range, and weighting] until the scale is documented. Consistency matters more than complexity.

Before you trust the scorecard, spot-check one known client against raw entries. Confirm tags, descriptions, and billable status are consistent, and add simple guardrails in your sheet, such as required fields, validation checks, and an audit log, so your decisions stay evidence-based.

Step 2: Compare client quality, not client size#

Big invoices can still mean weak business if AGI is reduced by pass-throughs, delivery margin is thin, and operating friction is persistent. Smaller revenue can be better business when profit is stable and delivery is calm.

| Client profile | Revenue view | Risk-adjusted profitability view | Operating risk signals | Portfolio action |

|---|---|---|---|---|

| Large account with heavy pass-through spend | Looks largest on invoices | AGI is lower than top-line revenue; delivery margin is pressured by admin and rework | Slow payment follow-up, frequent approval churn | Reprice or redesign scope before renewal |

| Mid-size retainer with clean delivery | Not the largest top line | Stable delivery profit and margin | Predictable approvals, low communication overhead | Retain and protect |

| Small project with frequent extras | Lowest top-line revenue | Profit can erode as change work accumulates | Repeated scope changes, unclear feedback ownership | Tighten scope and guardrails, then reassess |

This is the key shift: revenue rank and portfolio quality rank are not always the same.

Step 3: Choose the right portfolio action#

Avoid a simple keep-or-drop call. Match the action to the pattern in your scorecard.

| Action | Profitability cue | Operating cue |

|---|---|---|

| Retain | Healthy delivery margin | Low operating friction |

| Reprice | Real delivery effort is underpriced | Workable relationship |

| Redesign scope | Value exists | Approvals, revisions, or change handling need tighter structure |

| Exit | Weak profitability | Repeated risk patterns continue after terms and pricing are adjusted |

Base the decision on tracked time and recorded behavior, not memory. When conditions change, actual tracked time is more reliable than intuition.

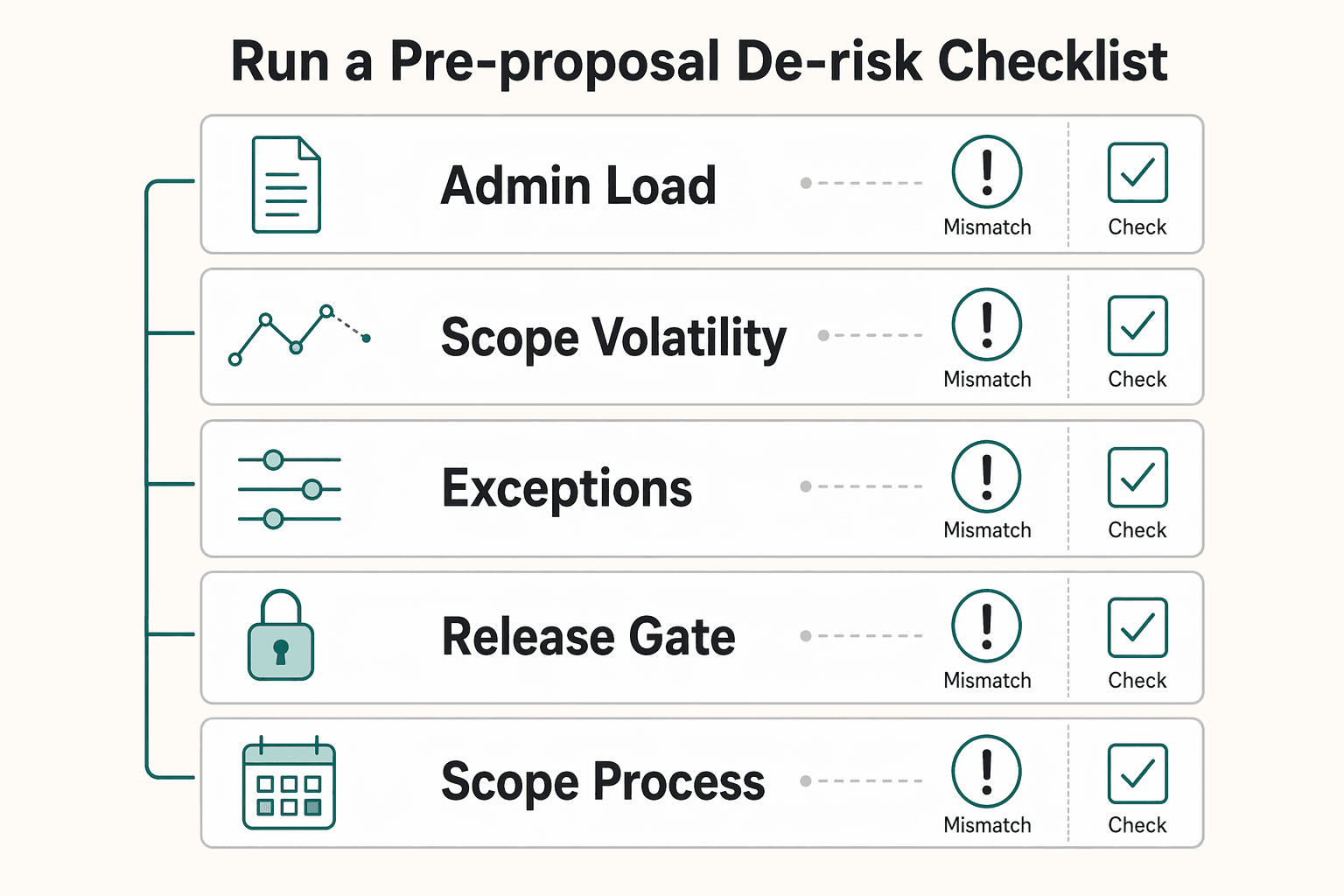

Step 4: Run a pre-proposal de-risk checklist#

The best time to fix repeat risk is before the next proposal goes out. Before any renewal, retainer, or follow-on scope, use prior project data to set terms for the next cycle.

Check these five items:

- Admin load: did coordination and support consume more effort than expected?

- Scope volatility: how often did

scope-creepappear, and how early? - Payment behavior: did invoices require repeated follow-up or exceptions?

- Communication overhead: were approvals slow, unclear, or overly multi-layered?

- Scope and process guardrails: which boundaries need to be clearer in the next SOW, proposal, or invoice schedule?

If risk signals repeat, reflect them before work starts: price coordination explicitly, narrow inclusions, define the change approval flow, and adjust the invoicing structure. For larger renewals, run simple what-if planning with live and historical tracked data (for example, added client load or temporary staff absence) instead of relying on a static spreadsheet view.

Once your portfolio is both profitable and operationally safer, move to Pillar 3 and ask a harder question: which projects still leave you with enough attention to lead well?

If you want a deeper dive, read Value-Based Pricing: A Freelancer's Guide.

Pillar 3: What's the "Cognitive Profit" of Your Projects? (The CEO Pillar)#

A project can pay well and still be bad leadership math. After you rank work by delivery profit and client risk, make one more weekly CEO call: keep work that pays and protects your decision quality, and change work that pays but drains you. Cognitive profit is the signal for that call. It is not a built-in Toggl metric, so you create it through consistent entry labeling and review it against your financial reports.

Step 1: Label energy when you log time#

If you want this signal to be useful, keep it simple. Use each time entry as the base record. When you stop the timer, or when you log later in Manual Mode, add one energy label to the entry description. If you want faster filtering later, add the same label as a tag.

Keep one fixed format:

Energy-HighEnergy-NeutralEnergy-Drain

Use these as decision labels, not journal entries. High means demanding work that still leaves you sharper. Neutral means routine but manageable work. Drain means the task lowers focus, patience, or judgment quality.

Step 2: Track repeatable drain patterns and choose a response#

Do not stop at "this felt bad." Look for the recurring pattern, then apply the matching fix in the next cycle.

| Pattern | What to look for in entries | Practical next-cycle response |

|---|---|---|

| Feedback loops | Repeated short review, reply, and revision entries on the same deliverable | Set a tighter review flow and a clear approval owner |

| Revision churn | Energy-Drain entries recurring with rework or scope-change activity | Tighten revision boundaries and move extra changes into paid requests |

| Context switching | Many small entries across multiple clients or tasks in the same day | Batch similar work and reduce same-day project switching |

Task switching has a real time cost, and that cost rises as work gets more complex, so repeated drain is an operating risk, not just a preference issue.

Step 3: Run a weekly review checklist#

A weekly review only works if the cadence stays fixed. Use the same sequence each time so the conclusions stay evidence-based.

- Open

Detailed Reportand filter for your energy tags. - In

Summary Report, group by billable status, client, project, task, and tags. - Use advanced filter logic to isolate patterns, for example: one client +

Energy-Drain+ rework or scope-change tags. - Compare those slices to your money view.

- If you have Premium, use

Profitability Report. * If not, useSummary ReportplusDetailed Report.

- Spot-check raw entries before you act, especially billable status and rate setup: billable rates apply only to billable entries, and the most granular configured rate is used.

Step 4: Classify each project and act#

Once you have both money and energy signals, classify each project and choose the least disruptive fix first.

| Financial result | Cognitive result | Risk signal | Default action |

|---|---|---|---|

| Strong | High or neutral | Sustainable delivery pattern | Keep |

| Strong | Drain | Good margin with leadership or attention drag | Redesign first, then reprice if drain persists |

| Weak | High or neutral | Work feels good but may be subsidized | Limit or keep only with a clear strategic reason |

| Weak | Drain | Margin pressure plus repeated stress signal | Exit unless one immediate scope or contract fix is realistic |

When financial and cognitive signals conflict, change the most reversible lever first. If money is strong but drain is high, redesign scope and workflow before you decide to exit. If energy is good but money is weak, fix pricing or scope first. If Pillar 2 already shows high client risk and this pillar shows repeated drain, tighten terms now or start the exit plan.

We covered this in detail in How to Invoice for 'Billable Hours' vs. 'Project Fees' in QuickBooks.

Conclusion: You Are the CEO - Use Your Data Accordingly#

The point of this audit is not better reporting for its own sake. It is to make three decisions each cycle: protect margin, catch risk early, and keep your workload sustainable.

Pull those signals into one view for the same period, then assign one action to each active project.

| Data signal | What it indicates | Your next move |

|---|---|---|

| Margin is holding | Pricing, scope, and delivery mix are supporting profit | Keep the model and protect the delivery conditions that support it |

| Risk signals are rising | Client behavior or project structure is adding avoidable drag | Tighten terms, scope, or approval flow before the next cycle |

| Energy drain is repeating | Work may still pay, but it is getting expensive to lead | Redesign batching, review ownership, or workflow before taking on more |

When signals conflict, use fixed tradeoff rules. If margin is strong but energy strain is rising, change the most reversible lever first: scope boundaries, revision flow, batching, or review ownership. If energy is fine but margin is weak, fix pricing or scope first. If client risk keeps repeating and cognitive drain is high, control the relationship now and pause expansion until one immediate scope or contract fix is realistic.

Open your reports, run the review, flag the highest-friction project, and commit to one change for the next cycle only. That gives you something you can verify in the next set of entries.

For a step-by-step walkthrough, see How to Use Harvest for Time Tracking and Invoicing in a Small Agency.

Frequently Asked Questions

How do I calculate project profitability in Toggl Track?

Start with one project and one date range. Calculate profitability as revenue minus costs: pull the revenue for that project, then subtract the delivery costs tied to that work. Use the same project name and date window on both sides of the calculation so the result is comparable. Next step: run this on your most recent completed project before you review active work.

How do I test whether a fixed-fee project is still paying well enough?

For fixed-fee work, subtract delivery costs from the agreed fee to see profit, then calculate your effective hourly rate by dividing the fixed fee by the total tracked hours for that project. Compare that result to your own internal floor if you use one. If the rate looks weak, review where delivery costs increased before you price the next proposal. Next step: do this check before sending any renewal or follow-on quote.

What is the cleanest way to track non-billable time without muddying delivery data?

The cleanest approach is consistent separation. Mark non-billable time so it does not blend into delivery hours, keep the labels simple and repeatable, and review them in the same period as the related project or client. If everything is logged as generic project time, your margin picture can look better than reality. Next step: pick your non-billable labels now and use them for one full review cycle.

How should I track scope creep in Toggl Track?

Track out-of-scope work as it happens in one consistent way so you can separate agreed work from expanded work later. Add short context on each entry so those reviews are easier before approvals, renewals, or repricing, not after the project closes. Next step: choose one marker today and apply it to every new out-of-scope entry.

Should I use tags, tasks, or notes for profitability tracking?

There is no single supported rule here for when to use tags, tasks, or notes. Choose one method per profitability signal and apply it consistently so reporting stays readable. Next step: pick one signal, like rework, and track it the same way for the next 30 days.

How often should I review reports for margin, risk, and energy?

Review on a fixed cadence using the same date window each time so comparisons mean something. If your workspace has the refreshed reporting experience announced on Jul 10, 2025, use the unified Reports, Insights, and Analytics view to review those signals together. End each review with one action on one active project, because more clients do not automatically mean more profit. Next step: schedule your next review now and decide one project-level change before you close the session. If your audit shows your effective rate is below target, use the freelance rate calculator to set a defensible floor for your next proposal.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 5 external sources outside the trusted-domain allowlist.

- delcode.delaware.gov/title11/c005/sc07trusted

- stripe.com/pricingtrusted

- apa.org/topics/research/multitaskingexternal

- support.toggl.com/profitability-reportexternal

- support.toggl.com/tracking-time-in-list-viewexternal

- toggl.com/resources/project-profitabilityexternal

- toggl.com/track/custom-built-profitability-reportexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Value-Based Pricing for Freelancers Under Real Payment Risk

Value-based pricing works when you and the client can name the business result before kickoff and agree on how progress will be judged. If that link is weak, use a tighter model first. This is not about defending one pricing philosophy over another. It is about avoiding surprises by keeping pricing, scope, delivery, and payment aligned from day one.

Manage Agency Project Profitability With Cashflow Checkpoints

Invoiced revenue can look healthy while cash is still unavailable. That gap is where a project that looks profitable can start to pressure routine operating costs such as payroll, rent, utilities, and equipment.

Choosing Time Tracking Software for Billable Hours in 2026

---