Quick Answer

Use escrow by setting clear milestone terms before kickoff, confirming each milestone is funded before work starts, and releasing payment only when written acceptance criteria are met. For large freelance projects, this gives you more payment control than invoicing after delivery, helps contain scope creep through funded change orders, and creates a cleaner record trail for disputes, invoicing, and reconciliation.

The Escrow Protocol: Why Your Standard Invoice Process is a Catastrophic Business Risk#

If you invoice after delivery, you hand over the work before payment is under your control. On a large freelance project, that is a payment-control gap first and a collections problem second.

Diagnose the leverage mismatch#

The core issue is not invoicing itself. It is the sequence. You deliver the work, send the invoice, and then wait while payment moves into the client's internal process.

Longer terms widen that gap. Under Net 45, the buyer has 45 calendar days from the invoice date to pay, so a July 1 invoice is due August 15. Net 30 shortens the wait. Net 60 extends it. In practice, longer terms give the client more flexibility while putting more strain on your cash reserves.

One detail matters more than many teams realize: when the payment clock starts. If your contract and invoice do not clearly state whether timing starts on invoice date, delivery, completion, or approval, disputes can follow. Payment can slip by days or weeks.

That ambiguity creates operational drag. One side may believe payment starts after approval while the other assumes it starts when the invoice is sent. If those checkpoints are not aligned in writing, delays can follow even after work is delivered.

This is why the risk should be framed as leverage, not just lateness. Once the client has the usable deliverable, your main tool is follow-up. If approval ownership and invoice timing were not settled before kickoff, you are trying to solve process questions after value has already changed hands.

Map the failure sequence before it happens#

Payment delays often follow a very ordinary sequence. It can look like this:

- You deliver the agreed work.

- The client now has the usable output.

- You issue the invoice and payment timing begins.

- Delays or approval bottlenecks become your follow-up burden.

- Unclear ownership of approval slows resolution.

This is the practical risk. Once the work is in the client's hands, vague payment timing language can turn into a cash-flow problem.

The weak point is usually not the invoice itself. It is the handoff between delivery, approval, and payment steps. If the contract is silent on who approves and when the payment clock starts, delays become a clarification exercise.

Map that sequence before the project starts. Ask yourself where the deal could stall: review, invoice processing, milestone acceptance, or a late scope disagreement. You are not assuming trouble. You are removing predictable ambiguity while you still have negotiating leverage.

Treat scope creep as a payment-structure issue#

Scope creep is not just a scoping problem. It is also a payment-structure problem.

When most of the money sits at the end, extra requests can get folded into "final delivery" while your unpaid balance stays open. Late in the project, that can weaken your options. You either absorb more work to keep momentum or pause and renegotiate while you are still waiting to be paid.

A tighter structure can force change requests into a payment decision earlier. That can improve revision discipline and protect margin. For a deeper margin view, see The Silent Profit Killer: How to Stop Margin Erosion in Your Freelance Business.

The sequence matters here. If a client asks for "one more round" after a milestone is effectively done, you want the structure to make that request visible as a decision point. Is it already covered by the milestone language? Is it a revision inside the agreed round? Or is it a new request that needs a new funded step? If those answers are not tied to payment, extra work can slide into the project by default.

That is why late-stage flexibility can become margin pressure. You are no longer negotiating from an open proposal stage. You are negotiating after time has been spent, delivery has happened, and final payment is still unresolved. A stronger structure does not eliminate scope discussions, but it keeps them attached to a documented decision and a payment checkpoint.

Compare decision paths, not just payment terms#

Payment terms alone do not tell you enough. What matters is how each structure handles forecasting, disputes, leverage at acceptance, change requests, and admin time.

| Decision criterion | Plain-language definition | Invoice after delivery | Escrow-based structure |

|---|---|---|---|

| Cash-flow predictability | How clearly you can forecast when cash arrives | Often lower on longer terms (Net 30/45/60), because payment happens after delivery | Can be higher when payment handling is defined as part of the deal structure |

| Dispute path | What happens when timing/scope/acceptance is contested | Can become ad hoc, especially if start-point language is unclear | Can be clearer when payment rules are set before work starts |

| Leverage at acceptance | Who has practical control at final handoff | Client holds delivered work while payment is still pending | Can be more balanced when payment checkpoints are pre-agreed |

| Change-request control | How easily "one more round" is separated from core scope | Harder when most money is due at the end | Easier when change decisions are tied to pre-agreed payment checkpoints |

| Admin overhead | Time spent setting up vs. chasing payment later | Lower at setup, but follow-up can grow if delays start | Higher at setup, with less reliance on end-stage chasing |

Read the table as a workflow comparison, not just a finance comparison. One model concentrates admin at the end, when leverage is weakest. The other shifts more admin to the front, when terms can still be clarified without disrupting delivery. That tradeoff can be worth making on larger or longer projects because front-loaded structure is often easier to manage than end-stage collections.

Switch when risk signals show up#

Do not wait for a bad payment experience to tighten the structure. Move away from pure invoice-after-delivery when these signals show up:

| Signal | Detail |

|---|---|

| Large fee | The fee is large enough that waiting through Net 30/45/60 would strain cash flow. |

| Long timeline | The timeline runs weeks or months, not a short task window. |

| Multiple reviews or changes | The project has multiple review rounds or likely change requests. |

| New or unclear client | The client is new or unclear about invoice approval timing. |

| Undefined start point | Your contract or invoice does not explicitly define the payment-term start point. |

If two or more signals are present, treat stronger payment protection as a requirement. The next step is deciding how to structure it before work starts.

Do not overcomplicate the decision. You are looking for concentration of risk, not a perfect score. A new client with clear finance ownership may still be workable on normal invoicing for a small task. A repeat client on a long, revision-heavy project can still justify milestone protection because approval drag and scope expansion can still happen. The right trigger is not trust alone. It is whether delay or disagreement would put you in a weak position after delivery.

Related: How to Conduct a 'Pre-Mortem' to De-Risk a Large Freelance Project.

Step 1: PROTECT - Building Your Financial Fortress with Milestone Escrow#

The next move is milestone design, but provider-specific rules should stay unresolved until you have verified the escrow workflow you will actually use. Avoid treating a generic sample as the rule for release conditions, payment-model comparisons, or dispute procedures.

Until that workflow is confirmed, keep the milestone plan conservative: define the deliverable, acceptance evidence, release trigger, and change-order path in writing, then check that the provider can support those steps.

The unresolved items are the same decisions you need before kickoff: milestone structure, release mechanics, provider workflow, and dispute handling. Treat those as verification questions, not assumptions.

For broader workflow context, see The Best Project Management Tools for Freelance Designers.

Step 2: PROFESSIONALIZE - How Introducing Escrow Signals Authority and Filters Clients#

If you use escrow, decide when you introduce it and keep that timing consistent. Clients should hear the same payment process on the call, in the proposal, and at handoff. Treat this as a practical workflow, not a benchmark claim or a guarantee that escrow will predict client behavior.

1. Set and repeat the payment path#

Set the payment path and repeat it in the same order every time:

- Discovery call: confirm budget range, approval owner, and whether procurement or finance must review payment setup.

- Proposal: restate the payment path in writing.

- Contract handoff: confirm the same payment path and named owners before kickoff.

Before you send the proposal, your minimum clarity is simple: who approves budget, who handles contract steps, and who can block setup.

Use this sequence as a workflow aid, not as proof that one escrow timing performs better than another. If the person on the call cannot name who approves budget or who owns payment setup, treat that as an unresolved dependency to close before kickoff.

Keep the wording stable across steps. If you say one thing on the call, soften it in the proposal, and change it again in the handoff email, the process becomes harder to follow.

2. Define your SOP so decisions are not arbitrary#

You need one written default communication workflow, not case-by-case improvisation. In practice, your policy should state:

- how you explain escrow to clients,

- who can approve exceptions to the initial payment path,

- what must be documented when terms change.

Keep the wording aligned across the call recap, proposal, handoff email, and kickoff checklist so the client gets one answer at every step.

This matters internally as much as externally. A written SOP gives you a reference point: not "what feels reasonable today," but "what your process requires before you start." That reduces drift between sales conversations and project delivery.

Exceptions should also leave a record. If the payment path changes, write down why, who approved the change, and what alternative protection is in place.

3. Use readiness signals as internal status checks#

Treat these as operating labels, not validated predictors:

Proceed: approver is named, payment questions are answered directly, and the method is confirmed in writing.Pause: budget seems available, but approval ownership is unclear or payment setup is deferred.Decline: terms are not documented, the agreed payment method is repeatedly reopened, or basic finance steps are rejected.

Read these signals in context. A Pause is not a soft Proceed; it means the project is not operationally ready yet. A Decline is an internal risk call, not a claim about client intent.

4. Use neutral talk tracks for common objections#

When clients push back, stay factual and process-focused:

- Complexity: "I'll send a short setup checklist with owners and steps so your team can review quickly."

- Trust: "This is a process-alignment step so payment terms are agreed before delivery starts."

- Timing: "Let's confirm this before kickoff so dates and approvals stay aligned."

- Fees: "Let's review the fee impact now and confirm acceptance in writing before work begins."

| Point in process | Escrow introduced early | Escrow introduced later |

|---|---|---|

| Discussion context | Payment method is discussed while scope is still being finalized | Payment method is raised during contract review or after verbal alignment |

| Ownership visibility | Approval owners can be requested during onboarding | Approval ownership may be confirmed closer to kickoff |

| Documentation timing | Payment steps can be documented before work starts | Documentation may be completed later in the cycle |

Use a simple decision rule: proceed when ownership and payment steps are clear in writing, pause when ownership is unclear, and decline when terms cannot be stabilized. For implementation detail, keep one reference attached to proposals, such as A Guide to Using an Escrow Service for High-Value Projects.

The value of these talk tracks is not persuasion for its own sake. They keep the conversation anchored to workflow. You are not trying to win a debate about whether the client is trustworthy. You are clarifying how a large project will move from kickoff to payment with less ambiguity, and whether the remaining blocker is mechanics or internal alignment.

If you also need banking setup context, read A Guide to Opening a Bank Account in Spain as a Foreigner.

Step 3: PREVAIL - Turning Your Escrow Agreement into an Enforcement Tool#

Escrow only helps if the documents line up. For freelance project work, your MSA and escrow instructions should match line by line on scope, acceptance, change control, and release conditions. In many projects, the MSA sets commercial terms while the escrow holder follows transaction instructions, so mismatches can create avoidable dispute risk.

Align the MSA and escrow instructions before kickoff#

Do a side-by-side check of each milestone before work starts. Use this minimum alignment checklist for every milestone:

| Alignment point | What should match |

|---|---|

| Deliverable scope | Same deliverable scope in both documents |

| Acceptance criteria | Same acceptance criteria in both documents |

| Reviewer or approver | Same reviewer or approver named |

| Release trigger and timing | Same release trigger and timing |

| Change-control path | Same change-control path for scope changes |

If one document says "homepage concepts plus one revision" and the other says "design phase," rewrite before kickoff.

Also keep governing law and dispute resolution as separate clauses in your MSA. They are different controls and are better drafted separately.

A quick practical test helps here: could a person who has never seen the project compare the two documents and reach the same understanding of what unlocks release? If not, your language is still doing too much by implication. The goal is not elegant drafting. It is consistency across the documents that actually control delivery and release.

Draft milestones so a third party can verify acceptance#

Write each milestone so acceptance can be tested, not argued. If a neutral third party cannot tell whether the milestone was met, the language is too vague. Use this enforceability checklist for every milestone:

- Deliverable definition

Specify output, format, quantity, and version.

- Objective acceptance test

State what must be true for acceptance.

- Evidence format

Define proof of delivery, such as platform submission, dated link, exported file, repo reference, or signed review note.

- Reviewer/approver

Name one acceptance owner.

- Release trigger

State the exact trigger, such as written approval, no action during the review window, or completion of the stated test.

| Vague milestone | Verifiable milestone |

|---|---|

| "Initial design phase" | "Milestone 1: three homepage concepts in Figma for the approved brief, plus one consolidated revision round. Reviewer: named marketing lead. Evidence: Figma link + PDF export submitted through the agreed channel. Release: written acceptance that all listed items were delivered." |

| "Development complete" | "Milestone 2: approved landing page build matching signed design files, deployed to staging and shared by URL. Evidence: staging link + repository commit reference. Release: reviewer confirms page loads and matches approved design scope." |

| "Final handoff" | "Milestone 3: final source files, asset package, and handoff notes in the agreed folder. Evidence: dated folder link + handoff document. Release: all listed files are present." |

For platform work, reflect the provider's workflow rules in the milestone text. On Upwork fixed-price contracts, clients have 14 days to review submitted work before auto-release, then funds move through a 5-day security hold. Protection can depend on using an active funded milestone, following the required submission flow, and matching the submitted work to scope.

The operational mistake to avoid is relying on informal approval language outside the agreed workflow. A positive message in chat may be helpful context, but your strongest position comes from acceptance being tied to the exact evidence and trigger already named in the milestone. When you submit work, package it in the same way the milestone expects so there is no gap between what the document says and what your delivery record shows.

Use change control before doing extra work#

This is where many projects slip. Treat scope creep as a classification process, not an informal discussion:

- Classify the request as in-scope or out-of-scope against the current milestone language.

- If scope, timeline, or deliverables change, document it with a written change order.

- For platform-based work, create a separate funded milestone for the change.

- Begin changed work after funding confirmation.

That sequence keeps the audit trail clean: client request, scope decision, written change order, and funding proof.

It also keeps project communication calmer. Instead of debating whether a request is "small," you compare it to the existing milestone. If it fits, proceed. If it changes the agreed output, revision count, or timeline, document the change and tie it to funding. That makes the decision easier to explain and easier to defend later.

Choose a provider model using enforceability criteria#

Choose the provider model based on governing terms, dispute path, and workflow constraints. Two guardrails matter here:

- Do not assume your MSA automatically controls a platform dispute unless platform terms explicitly incorporate it.

- Check current provider policies before final recommendations. Terms and procedures can change.

| Decision point | Platform-integrated escrow | Standalone escrow service |

|---|---|---|

| Governing terms | Platform terms often govern platform workflows and disputes | Provider agreement controls; may differ by location |

| Dispute model | Often internal platform dispute process | May include negotiation period and optional third-party arbitration |

| Workflow constraints | Tied to platform milestone and submission rules | Driven by provider instructions and terms |

When comparing models, do not stop at fees or convenience. Ask which system gives you the cleaner enforcement path for the type of project you are running. If the work needs strict submission flow and the client is already inside a marketplace, platform rules may be the main operating constraint. If the project needs different release instructions, standalone terms may fit better, depending on the provider's current rules. The right choice is the one that makes scope, acceptance, and release easiest to prove within that provider's actual workflow.

You might also find this useful: How to De-Risk a Fixed-Price Project with a Phased Payment Schedule.

Before you lock the next milestone, turn acceptance criteria into clear deliverables with the SOW Generator so disputes are easier to resolve.

The Compliance Blind Spot: Navigating Tax and Invoicing with Escrow#

Once your milestone terms are tight, the next failure mode is record mismatch. In escrow workflows, invoice the client who bought your services, treat escrow as an intermediary, and record each stage separately: invoice issued, escrow funded, milestone accepted, and funds released.

Escrow is a neutral third-party arrangement that holds funds until agreed terms are met. Your invoice customer is still your client, even if the sender on your bank statement is the escrow provider. In most flows, the client funds escrow, acceptance triggers release eligibility, and the provider sends funds on release.

For income timing, do not assume funding always equals recognized income. Under the cash method, income is generally reported when you receive it. Under accrual, timing depends on when your right to income is fixed and measurable. If access to funds is substantially restricted, constructive receipt may not apply yet.

Invoice fields + escrow linkage#

Use an invoice format that ties the contract, milestone, and escrow records together:

| Invoice field | Detail |

|---|---|

| Your legal name and address | Include on the invoice |

| Client company name and address | Include on the invoice |

| Unique invoice number | Include on the invoice |

| Invoice date | Include on the invoice |

| Milestone description | Matches the MSA |

| Amount, currency, and any required tax line | Include on the invoice |

| Contract reference | Example contract reference, such as MSA-2026-01 |

| Escrow reference | Example escrow transaction reference, such as ESC-TXN-78421 |

| Payment note | "This invoice relates to a client-funded escrow transaction and is payable on release under the agreed milestone acceptance terms." |

This helps prevent a mismatch: the invoice is addressed to the client, but the payment remitter shows up as the escrow entity with no reference linking the two.

You want someone reviewing the file later to be able to trace the transaction without guessing. If the milestone label on the invoice differs from the label in the contract or the escrow record, reconciliation becomes slower and error-prone. The cleaner the naming and reference structure, the easier it is to match commercial documents to payout records.

Records workflow by event#

Record each event on its own terms and keep the supporting documents together:

| Event | Record treatment | Documents to retain |

|---|---|---|

| Invoice issued | You billed the client for a defined milestone | Invoice copy, contract reference, milestone scope excerpt |

| Escrow funded | Client funded the intermediary for that milestone | Funding confirmation, escrow transaction summary, client funding confirmation |

| Milestone accepted | Release condition was met under agreed criteria | Acceptance evidence, delivery proof, review or approval record |

| Funds released | Cash receipt or receivable clearance (based on your method) | Release statement, bank deposit record, reconciliation note |

After each release, reconcile immediately. The invoice number, contract reference, escrow reference, milestone label, date, and amount should match across your invoice, acceptance evidence, provider records, and bank entry.

Immediate reconciliation is useful because memory fades quickly on multi-phase projects. If you wait until quarter-end or tax season, small mismatches become harder to explain. A missing milestone label, an altered description, or a payout that lands under the provider name instead of the client name is much easier to resolve while the project thread is still active. It is also easier when the documents are still easy to retrieve.

Tax documentation and reconciliation guardrails#

Keep one evidence pack per milestone: invoice, acceptance proof, escrow statement, bank deposit evidence, and your accounting or tax treatment note. Mismatches often involve names, such as client on the invoice versus escrow sender on the payout, or missing reference IDs.

If you receive Form 1099-K, use it alongside your own records to determine correct income. Do not treat it as standalone truth. 1099-K amounts can be gross and may include items that are not automatically taxable. If payer or name details are wrong, contact the issuer immediately and keep all correction correspondence.

If US recordkeeping rules apply, a common IRS baseline is 3 years, with longer retention, for example 6 years, in some omission cases.

A practical habit helps here: at the end of each milestone, save the full packet together rather than scattering files across email, accounting software, and provider dashboards. The article already gives you the components. The value comes from keeping them as one pack so you can answer the basic questions fast: who was billed, what was accepted, when release happened, and how the payout ties back to the invoice.

Nexus and jurisdiction scope#

Escrow use alone does not determine where tax obligations apply. Nexus and indirect-tax rules vary by jurisdiction, and physical presence is not the only trigger. Threshold frameworks differ across states and measurement windows, so use local rules for your filing year and facts.

Consult a qualified tax advisor before relying on any specific threshold, and verify current filing-year rules before using exact numbers. Also get advice when your filing position depends on whether your services are taxable in a client jurisdiction.

The key control here is restraint. Do not let the presence of an escrow intermediary distort the underlying tax question. Your analysis still depends on your facts, your client location, the services involved, and the rules that apply for the filing period. Where the provider sits is not, by itself, a shortcut answer.

For a separate workflow build-out, see The 3-Stage Notion Framework for Freelance Project Management.

Conclusion: From Protocol to Automated System#

Escrow works best when you treat it as a standard process, not a one-time safeguard. Agree terms, confirm funding, deliver against written acceptance criteria, invoice the release, and reconcile the payout records. That is what makes the structure hold up when a client slows down, changes scope, or pushes review into a different internal process.

Standardize onboarding around agreed terms#

Standardize onboarding around agreed transaction terms and escrow instructions. Keep release conditions explicit enough that a neutral escrow agent can apply them with minimal interpretation. Before kickoff, each milestone should include a clear deliverable, delivery date, payment amount, and funded status.

Standardization matters because repeated clarity is easier to maintain than custom negotiation on every deal. The more your onboarding, proposal, and handoff all describe the same path, the less room there is for payment mechanics to drift after work begins.

Use funded milestones for clear phases#

Use funded milestones by default for clearly defined fixed-price phases, especially when delayed payment would strain your cash flow. If scope is still evolving, do not force a vague fixed-price setup. Narrow the phase until the deliverable is clear, or use hourly terms for evolving work.

Set review timing on purpose. If your provider uses an Inspection Period, define it up front and tie it to acceptance or rejection actions so release timing is clearer.

The practical test is whether someone outside the project could tell when the phase starts, what counts as delivery, who reviews it, and what happens next. If not, the phase is still too loose for clean milestone handling.

Connect delivery, approval, invoicing, and payout#

Connect delivery, approval, invoicing, and payout reconciliation as one chain. Approval is not the same as money received, and provider release timing can include holds. Treat payout confirmation as the financial checkpoint before you close the milestone.

Keep one evidence pack per milestone: signed scope, milestone terms, delivery proof, approval request, invoice, transaction reference, and payout confirmation. Keep these records even if no Form 1099-K arrives, so your income and expense trail stays clear.

This step is easy to skip when the client relationship feels smooth. Do it anyway. A clean chain is valuable precisely because it reduces ambiguity later, whether the issue is accounting, a provider question, or a client disagreement about what was completed and when.

Put the operating checklist in place#

Implement this operating checklist now:

| Workflow step | What to lock in | Owner |

|---|---|---|

| Onboarding | Terms + escrow instructions agreed in writing | You |

| Funding check | Milestone funded before work starts | You |

| Delivery acceptance | Written acceptance or rejection trigger and review window | You + client |

| Invoicing | Invoice tied to the approved milestone release | You |

| Reconciliation | Payout statement matched to invoice and transaction record | You |

Use these trigger rules consistently: no funded milestone, no start; no written approval, no release assumption; no payout record, no file closed.

This does not remove risk. It can make payment more predictable, smooth cash flow, and reduce dispute friction when something needs clarification.

For the broader ops stack, see The Best Project Management Tools for Freelance Developers.

If you want to run this escrow-first process with fewer manual handoffs, explore Merchant of Record for Freelancers. Confirm fit for your countries and payout flows.

Frequently Asked Questions

What is the best escrow service for high-value freelance projects?

There is no universal best escrow service for high-value freelance projects. Choose the provider that best fits your deal using a short checklist: clear dispute process, supported geographies and currencies, transparent fees, payout rails that work for your location, and records you can use in your audit trail. If two options are close, prefer the one that gives you the cleaner chain from funded milestone to released payout.

How can you use escrow to prevent scope creep?

Use escrow to prevent scope creep by defining each milestone as one deliverable with clear acceptance criteria and requiring funding before you start. If a request falls outside the written milestone, pause, issue a change order, and tie it to a new funded milestone. The key is deciding scope before extra work is done, not after.

Is escrow necessary for repeat clients?

For large fixed-price work, keep the milestone-funded escrow structure even with repeat clients. Familiarity can reduce communication uncertainty, but it does not remove approval delays or payment risk. At minimum, keep written acceptance criteria and funded milestones for material phases.

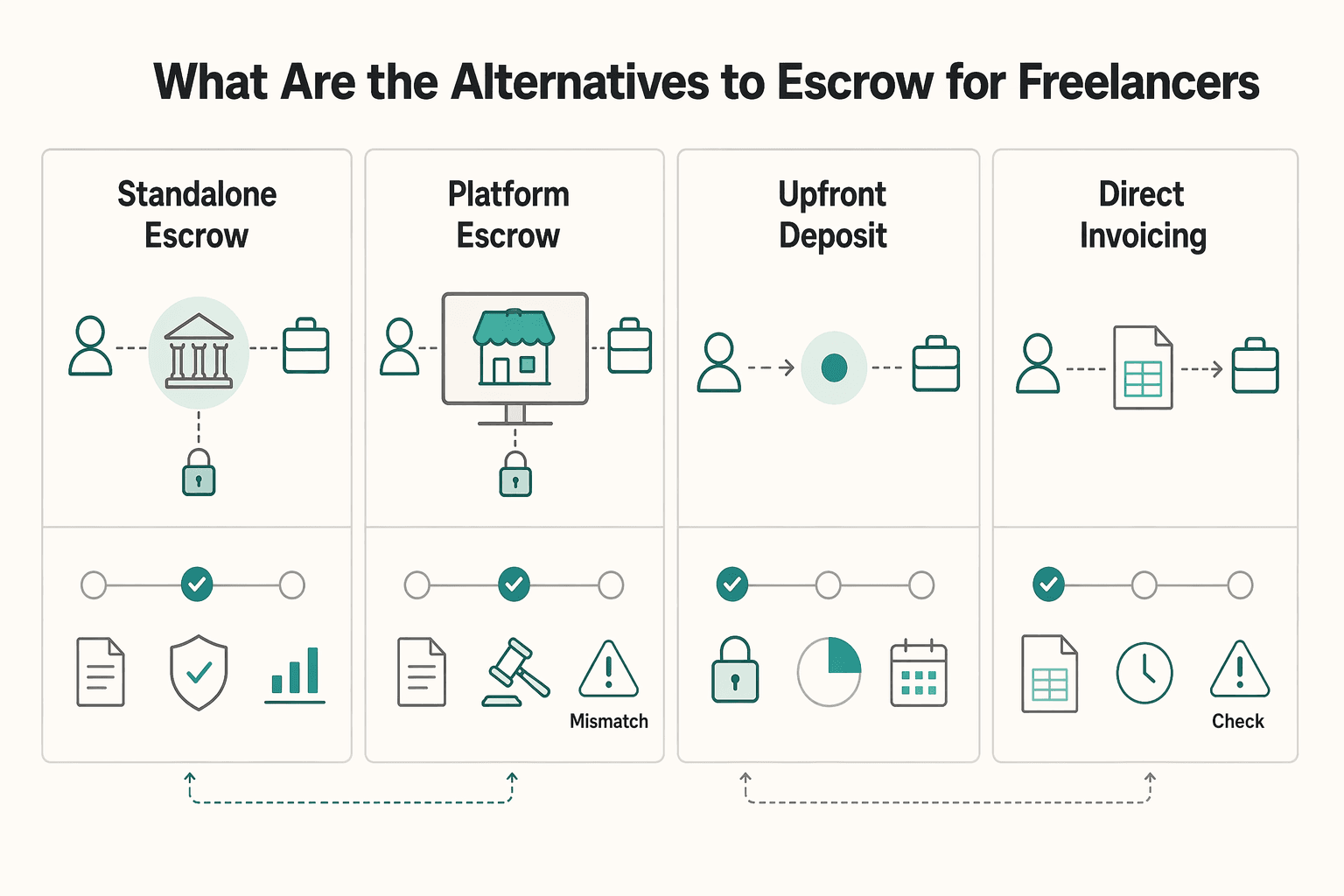

What are the alternatives to escrow for freelancers?

The main alternatives are platform escrow, upfront deposit plus invoicing, and direct invoicing only. Standalone escrow offers more control but requires you to vet provider terms and operations, while platform escrow may be governed by marketplace rules. Deposits and direct invoicing can work for lower-risk projects, but later phases remain more exposed.

How much do escrow services typically cost for a large project?

Escrow costs vary by provider, so do not rely on a headline rate alone. Review the full fee stack, including service, payout, FX, and possible dispute charges, and verify live terms before you price the deal. Separate the fees that affect proposal pricing from the ones that matter only if something goes wrong.

What happens if a client refuses to release funds from escrow?

Keep the dispute narrow and anchor it to the specific milestone, its acceptance criteria, and your delivery evidence. Submit a complete evidence pack, including the signed scope, milestone text, delivery proof, version history, client feedback, approval request, invoice reference, and escrow transaction reference. If release is still withheld, escalate through the provider's dispute process using that same documentation.

Can escrow be used for international clients and different currencies?

Yes, escrow can be used for cross-border and multi-currency projects. Before signing, confirm that the client country, payout country, and currencies are supported, where conversion happens, which party pays FX-related fees, and which payout rails are available. Resolve those points before the client funds anything.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- acquisition.gov/far/subpart-46.5trusted

- acquisition.gov/far/subpart-43.2trusted

- comptroller.texas.gov/taxes/sales/remote-sellers.phptrusted

- dfpi.ca.gov/regulated-industries/escrow-law/general-defi...trusted

- dfpi.ca.gov/site-maptrusted

- ecfr.gov/current/title-26/chapter-I/subchapter-A/part...trusted

- ecfr.gov/current/title-26/chapter-I/subchapter-A/part...trusted

- govinfo.gov/content/pkg/CFR-2016-title45-vol1/html/CFR-2...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Stop Freelance Profit Margin Erosion Before It Hits Cashflow

Revenue can hold steady while the business underneath it gets weaker. What comes in matters, but what you keep after the work is delivered is the clearer signal of health.

Opening a Bank Account in Spain as a Foreigner for Reliable Cashflow

If you searched open bank account spain foreigner, the goal is not approval on paper. You need an account setup that keeps invoices moving, limits avoidable fees, and stays usable when checks, document questions, or channel changes appear.

A Guide to Using an Escrow Service for High-Value Projects

**Treat escrow as your payment system, not a last-minute fix for overdue invoices.** On high-value projects, money risk usually shows up at handoff points like scope approval, milestone acceptance, and payout release. If you run a business of one, you need a get-paid system that works the same way on every deal, even when a client is in a hurry. This guide treats escrow as that repeatable system, so payment protection supports delivery, trust, and disciplined risk management from day one.