Quick Answer

Use Brex for daily approvals and accounting sync, then block repeat contractor payouts until worker files pass compliance review. For brex for remote startups, keep cards, bill pay, travel, and reimbursements in Brex, but require a documented classification decision, Form W-9 or Form W-8BEN, and a withholding check before payment release. Re-run this gate each quarter and whenever duties or location change.

How to Build a Resilient Financial Stack for Your Remote Startup#

Short answer: If you are evaluating brex for remote startups, make this decision early. Use Brex as your operational finance layer, not as your only compliance layer. A resilient setup has two parts: one for spend control and clean accounting, and another for worker classification, tax documentation, and tax-presence review before payment.

That split matters because remote companies often feel the first pain on the spend side, then discover later that the larger risk sits somewhere else in the workflow. Cards, reimbursements, bill pay, and accounting syncs are visible every day, so they get attention first. Worker status, tax forms, and tax-presence review can stay invisible until a repeat payment, a changed role, or a new location exposes a gap.

If you separate those layers on purpose, you can keep operations fast without assuming that a smooth payment flow means your compliance posture is sound.

Step 1. How should you use Brex for day-to-day spend control?#

Brex positions its startup platform around operational finance workflows: banking access, cards, bill pay, travel, and reimbursements. Its policy engine is meant to enforce rules at the point of spend across cards, bill pay, travel, and reimbursements.

| Spend type | Requirement or review |

|---|---|

| Reimbursement | Needs proof of the underlying expense |

| Bill pay | Needs the invoice and the approver trail |

| Card spend | Needs the receipt and the policy check at the time of purchase |

| Travel | May need both policy enforcement and later documentation review |

Give ownership to finance or an operations lead. The main inputs are your vendor list, team roster, approval rules, GL structure, and documentation requirements. The outputs you want are approved transactions, receipts or invoices on file, mapped accounting fields, and clean exports to your accounting system. If you use NetSuite, Brex states that it can pull in NetSuite fields and support GL and accounting-field mapping.

The practical way to set this up is to decide, in order, what must be true before money moves and what must be true before the transaction is considered complete in accounting. That usually starts with normalizing your vendor list so repeat payments land under the same vendor record, not several slightly different names. Then align your team roster and approver chain so the right person is reviewing the right category of spend. After that, map the GL structure and any accounting fields you need on export, and only then finalize documentation rules.

If you do those in reverse, you often end up with transactions that are approved quickly but coded inconsistently or missing backup.

That sequence also helps you separate policy questions from bookkeeping questions. Policy answers whether the spend is allowed, who approves it, and what support is required. Bookkeeping answers where it lands, which fields must travel with it, and whether the accounting output is usable without cleanup. If your team tries to solve both at once inside day-to-day approvals, the work tends to drift into exceptions, manual fixes, and inconsistent treatment across similar payments.

For remote startups, this matters because the same platform may be handling different transaction types that should not be governed in exactly the same way. A reimbursement needs proof of the underlying expense. Bill pay needs the invoice and the approver trail. Card spend needs the receipt and the policy check at the time of purchase. Travel may need both policy enforcement and later documentation review. Brex can help you enforce those lines at the point of spend, but it works best when you define those rules before the volume grows.

Your pass or fail test is not whether a payment went through. It is whether each transaction got the right policy treatment, has the required documentation, and landed in the right accounting destination. Run a monthly sample check for receipt completeness, approver-policy match, and post-sync GL accuracy.

Make that monthly sample check specific enough to catch drift. Pull a mix of cards, reimbursements, bill pay, and travel transactions. For each one, confirm that the required document is actually in the file, not merely requested. Confirm that the approver matched the policy you intended for that type of spend. Then confirm that the accounting export landed with the correct GL treatment and fields after sync, rather than assuming the mapping was correct because the sync completed.

A useful review order is:

- Start with the original transaction and its category.

- Check whether the policy route matched your rule.

- Check whether the receipt or invoice in the file is the support you actually require for that transaction type.

- Check whether the exported accounting fields reflect what finance expects to see.

- Note any exception that required manual correction after sync.

That review gives you a better control signal than headline metrics like payment success or sync success. A payment can move and a sync can complete while still leaving you with missing support, a broken approval chain, or a posting error that someone has to fix later. If you wait until close to find those issues, the correction work is slower and the process looks cleaner than it really is.

This is also the point where ownership matters. Finance or an operations lead should own the configuration, but someone should also own exception handling. When a transaction comes through with partial documentation, a wrong approver, or a field mismatch, decide in advance what happens next. Either correct the transaction in place, kick it back to the requester, or document it as an exception. Without a clear owner, the same issue gets handled differently depending on who happens to notice it.

Brex also states that it is a fintech company, not a bank, and that checking and banking services are provided by Column N.A., Member FDIC. Reflect that in your treasury documentation for account ownership and counterparties.

Do not leave that as a website detail that never makes it into your internal records. Your treasury documentation should reflect who provides the service and how you identify the relevant counterparties for account ownership, internal approvals, and downstream recordkeeping. This is less about adding process for its own sake and more about keeping your internal documentation aligned with how the service is actually structured. If someone later reviews account setup, payment authority, or counterparties, you want the file to match the provider structure you relied on.

In short, Step 1 is where you make Brex earn its place as the operational layer. Use it to standardize spend, approvals, support, and accounting outputs. Just do not mistake a disciplined spend workflow for a complete remote-work compliance workflow, because that is where the next layer starts.

Step 2. What should sit in the compliance-first layer#

Once spend control is in place, the bigger risk shifts to who you are paying and on what basis. Your second layer should decide whether a worker can be paid, under what classification, and with which tax documents. That is where founder risk usually sits, because a transaction can look operationally correct while the underlying worker or tax setup is wrong.

Give ownership to finance plus outside tax or legal support, or to a dedicated compliance lead. The key inputs are worker location, contract scope, control and independence facts, payment method, and tax forms. The outputs should be a documented classification decision, the required form on file, a withholding review flag, and a recorded tax-presence review.

The important operating principle here is simple: do the compliance review before payment, not after, and not only when someone remembers. A remote startup can look organized on the spend side while still paying people with incomplete worker files, stale assumptions about location, or no documented review of how the relationship is structured. The costliest failures usually happen when a payment process is efficient enough to move money before anyone asks the compliance questions.

So build a front-end intake, even if it is lightweight. Before a new worker is set up for payment, collect the facts that drive the decision. Capture where the person is located, what they are doing, how the scope is described, what the control and independence facts look like, how they will be paid, and which tax form belongs in the file. Then document the classification decision and the tax review outcome in a way that can be found later.

That means a repeat payment should not depend on memory or scattered messages. It should depend on a file that shows what was reviewed and what conclusion was reached.

This is where many teams blur two different questions. One question is whether the invoice or payment request is valid as an operational event. The other is whether the worker setup behind it is valid for classification and tax purposes. Those should connect, but they are not the same thing. If your process only validates the first, you can approve and pay an invoice that is perfectly documented on the transaction side while the worker file is incomplete or the tax review never happened.

For tax forms, use Form W-9 when a payee needs to provide a correct TIN for information-return reporting, and use Form W-8BEN for foreign individuals to establish foreign status. Missing or invalid documentation can trigger real consequences. That includes 24 percent backup withholding in applicable W-9 scenarios and a 30% withholding regime, with Form 1042 filing, for certain U.S.-source payments to foreign persons. Form collection helps, but forms alone are not full compliance.

That last point matters operationally. Form collection is necessary, but it is only one checkpoint in the file. A form can be present while the underlying facts still require review. A team that treats form collection as the finish line can end up with a tidy folder and a weak decision trail. Your compliance-first layer should treat the form as one piece of the payment gate, along with the classification decision, the withholding review, and the tax-presence review.

A good test is to ask what would happen if the same worker changed duties, changed location, or moved from one type of engagement to another. If the answer is that nothing in your payment flow would force a re-review, your setup is still too dependent on the original onboarding moment. Remote work changes over time, and your controls should catch that through triggered review, not just initial setup.

You also want the payment process to reflect the outcome of the compliance review. If documentation is missing, inconsistent, or still under review, the payment should not simply proceed because the invoice looks ordinary. The cleanest setup is one where operations can gather the transaction support, but the payment can move only after the worker file meets your requirements. That is the difference between collecting documents and actually gating payment on them.

A practical way to think about the outputs is:

- Documented classification decision: a written record of how you treated the worker based on the facts you reviewed.

- Required form on file: W-9 or W-8BEN, matched to the worker file before repeat payments.

- Withholding review flag: a visible indication of whether withholding review is needed before payment.

- Recorded tax-presence review: a dated note showing that location and activity were reviewed for presence risk.

If those outputs are not easy to locate, they are hard to rely on. That matters when the same worker is paid repeatedly over time. It also matters when someone new joins finance or operations and needs to understand why payments were allowed to continue.

This layer is where founders often need the most discipline. The risk does not announce itself through a failed card swipe or a missing receipt. It shows up when a worker relationship was set up casually, kept running, and never rechecked as the company expanded across states or countries. A resilient stack prevents that by making worker review a prerequisite, not a cleanup task.

Step 3. What changes when you add an integrated stack#

A spend-only setup can run day-to-day operations well, but it leaves a gap where the most expensive mistakes happen. The practical question is whether you want payments to move on transaction approval alone or only after classification and tax checks are complete.

| Criteria | Spend platform only | Integrated stack |

|---|---|---|

| Daily spend control | Strong for cards, bill pay, travel, reimbursements, and transaction-time policy enforcement | Same control, plus payment gating tied to classification and document checks |

| Compliance visibility | Mostly transaction and policy records | Adds worker-status evidence, tax-form status, and withholding review records |

| Global readiness | Useful for distributed spending operations | Stronger for cross-border hiring because onboarding includes tax documentation and tax-presence review |

| Audit defensibility | Approvals and receipts | Approvals, receipts, worker file, tax forms, and review notes tied to payment decisions |

| Founder exposure control | Reduces out-of-policy spend | Better coverage for payroll-tax failures and worker-classification process gaps, including trust-fund-tax exposure that can reach responsible persons |

The most useful way to read this comparison is to focus on the gating point. In a spend-only setup, a payment is mainly judged by transaction-level criteria: was it approved, is the support attached, and did it route correctly. In an integrated stack, those same checks still matter, but they are not enough by themselves. Payment also depends on whether the worker file is complete, the classification decision is documented, and the tax review has been performed.

That difference changes what your records can prove later. A spend platform can usually show who approved the transaction and what document supported it. An integrated stack can show why the payment was allowed in the first place, with the worker file, tax forms, and review notes connected to the decision. If you ever need to explain a repeat payment, that second record is far more useful than a clean invoice trail by itself.

The practical failure mode to avoid is simple. The invoice looks ordinary, the amount fits policy, the approver clicks through, and the money goes out even though the worker classification or tax-presence review never happened. Nothing in the transaction flow necessarily catches that on its own. That is why the two-layer approach matters. One layer validates spend. The other validates the relationship behind the payment.

The main red flag is a payment that clears even though classification and tax-presence checks never happened. IRS treaty guidance generally ties fixed base and permanent establishment concepts to a fixed place of business, so you need a documented review trail when roles or activities could create local presence risk.

The key phrase there is documented review trail. You do not want to rely on a general sense that someone "looked at it." You want a record that shows the review occurred, what facts were considered, and whether any follow-up was required before payment continued. That does not have to be elaborate to be effective. It just has to be consistent and retrievable.

This is not just a process issue. It is about personal downside. IRS Trust Fund Recovery Penalty rules can apply to responsible persons for unpaid trust fund taxes, so a stack that only catches receipt problems is not enough.

That is why founder exposure control belongs in the comparison, not as an afterthought. Out-of-policy spend is frustrating, but it is usually not the same category of risk as worker-classification failures or payroll-tax failures. If you compare tools only on convenience, cards, bill pay, or accounting sync, you are only comparing the operational layer. You are missing the part that changes the downside for the people responsible for the company's financial process.

Step 4. What should you review each quarter#

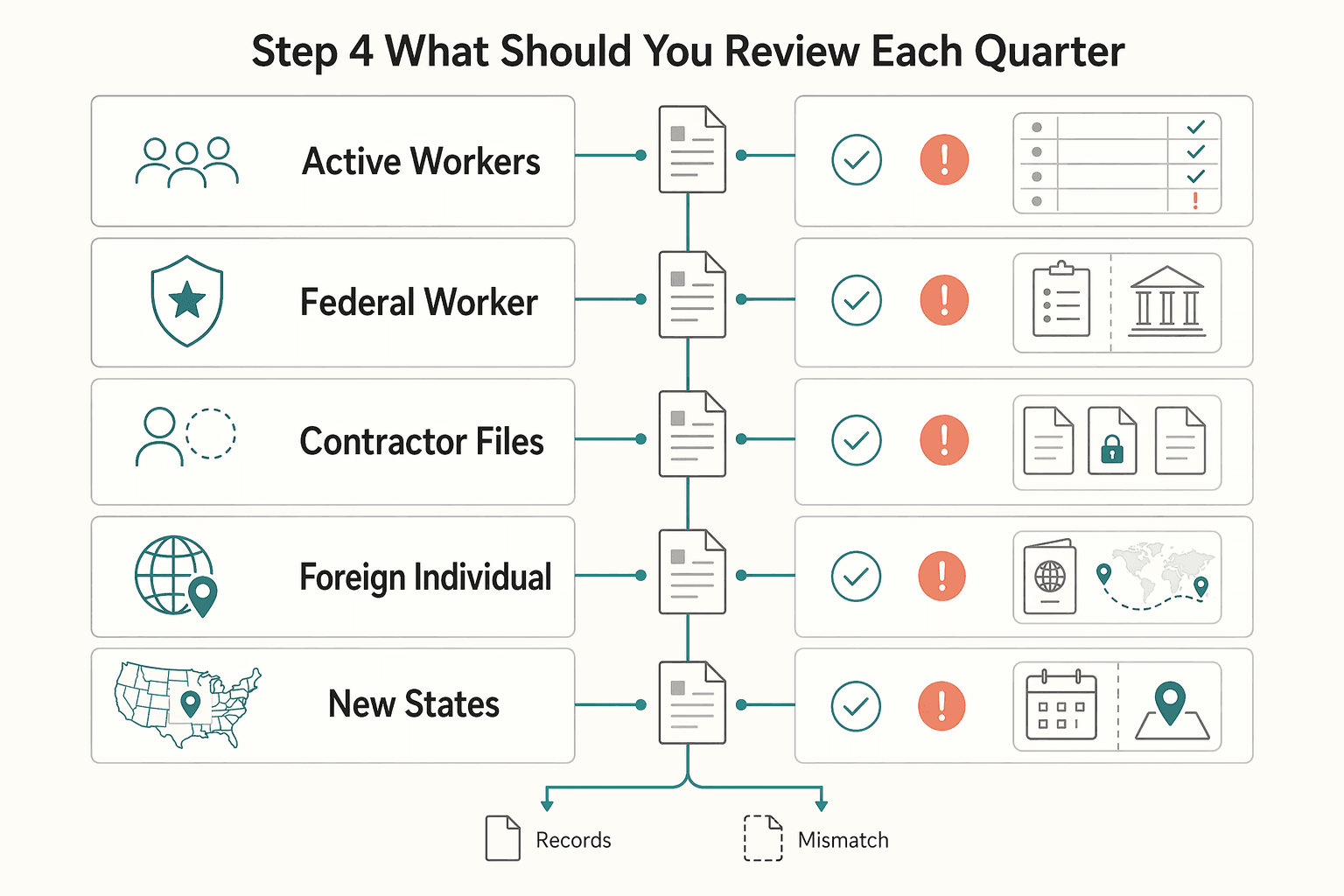

Use this as a gate, not a formality. Run it quarterly and before any hire in a new state or country. The point of a quarterly review is not to recreate onboarding. It is to catch change: changed duties, changed locations, changed payment patterns, changed rule status, and missing evidence in files that looked complete when work first began. A remote startup can drift into risk simply because the business moves faster than its records. This checklist is how you slow that drift down.

| Review area | What to confirm |

|---|---|

| Active workers | Each active worker has a current classification memo based on control and independence facts; re-review when duties change |

| Federal worker-classification rule status | Track current status before decisions; the DOL 2024 rule is shown as effective March 11, 2024, and a 2026 rescission proposal had comments due April 28, 2026; verify the exact current rule status from official guidance or counsel notes before use |

| Contractor files requiring Form W-9 | A valid Form W-9 and TIN status review; if not, review whether 24 percent backup withholding applies |

| Foreign individual contractor files | Form W-8BEN and expiry tracking, generally through the end of the third succeeding calendar year unless facts change |

| New states and countries | Review where work occurred and verify the exact current registration or filing requirement from official guidance, counsel/adviser notes, or governing records before use |

| Repeat-payment evidence pack | Confirm approval, receipt or invoice, GL mapping, worker file, and tax-form status; if any element is missing, pause repeat payments until fixed |

- Confirm each active worker has a current classification memo based on control and independence facts. Re-review when duties change.

Do not treat "active worker" as a static list from your first setup. Compare who is actually being paid against who is on your current worker file list. Then confirm that the classification memo still matches what the person is doing now, not what the original contract described. If duties have changed, route the file back for review before the next repeat payment. A current memo is useful because it ties the decision to present facts, not outdated assumptions.

- Track current federal worker-classification rule status before decisions. The DOL 2024 rule is shown as effective March 11, 2024, and a 2026 rescission proposal had comments due April 28, 2026. Verify the exact current rule status from official guidance or counsel notes before use.

This item matters because rule status can change while your process stays the same. Keep a dated note in your review file showing what current requirement you verified before making or refreshing a classification decision. That helps prevent a common failure mode in remote startups: a team relies on an earlier understanding, keeps using it, and never records whether it is still current. Verification should happen before the decision is treated as settled.

- Confirm each contractor file requiring Form W-9 includes a valid Form W-9 and TIN status review. If not, review whether 24 percent backup withholding applies.

Make this more than a presence check. Confirm that the file actually contains the form you expect and that the TIN status review was completed, not left as a placeholder for later. If the file is incomplete, route it immediately for review rather than allowing it to sit unresolved because previous payments already went out. Repeat payments are where small file defects become embedded process failures.

- Confirm each foreign individual contractor file includes Form W-8BEN and expiry tracking, generally through the end of the third succeeding calendar year unless facts change.

The operational step that matters is the tracking, not just the file upload. If you have foreign individual contractor payments that recur, set your review cadence so the form is checked before the next payment cycle, not after someone notices the form timing issue. Also watch for changed facts. The file should show not only that the form exists, but that someone is responsible for noticing when the file needs review again.

- Review new states and countries where work occurred. Verify the exact current registration or filing requirement from official guidance, counsel/adviser notes, or governing records before use.

Do not rely only on onboarding location. Compare actual work locations during the quarter against what your records expected. This is especially important for remote teams because work can shift without a formal "hire" event. When a new state or country appears, route it for verification and add the current requirement only after that verification is completed. The point is not to guess the requirement. The point is to avoid treating a new location as harmless until someone has checked it.

- Reconcile spend records to accounting and confirm the evidence pack exists for repeat payments: approval, receipt or invoice, GL mapping, worker file, and tax-form status. If any element is missing, pause repeat payments until fixed.

This is where the two layers meet. The evidence pack should show both transaction support and worker-compliance support in one reviewable set. For repeat payments, confirm that the approval and receipt or invoice are in place. Confirm that the GL mapping is correct, the worker file is current, and the tax-form status is still valid for continued payment. If any one of those pieces is missing, the right response is not to document the gap and keep paying. The right response is to pause repeat payments until fixed.

That pause discipline is what turns a checklist into a control. Without it, the review becomes a record of problems that did not change behavior. With it, your finance stack actually becomes resilient. Brex handles day-to-day spend control, your compliance layer decides whether the worker setup supports payment, and your quarterly gate catches changes before they become recurring mistakes.

If you want a deeper dive, read Value-Based Pricing: A Freelancer's Guide. For tax-form workflow prep before international contractor payments, see the W-8 Form Generator. If your next step is implementation planning, review Payouts.

Related Guides and Official References#

- Use this related guide to align your scope and pricing assumptions before execution.

- Cross-check execution steps with this workflow and tighten approval checkpoints.

- Review a contingency pattern in this backup playbook before rollout.

- Benchmark assumptions against this supporting article to avoid planning drift.

- Track legal/compliance edge cases in this linked explainer if your setup is cross-border.

Use official documentation for policy and filing details, including primary guidance, administrative rules, and reference material.

Frequently Asked Questions

Step 1. How should you use Brex for day-to-day spend control?

Brex positions its startup platform around operational finance workflows: banking access, cards, bill pay, travel, and reimbursements. Its policy engine is meant to enforce rules at the point of spend across cards, bill pay, travel, and reimbursements. Spend type; Requirement or review Spend type: Reimbursement; Requirement or review: Needs proof of the underlying expense Spend type: Bill pay; Requirement or review: Needs the invoice and the approver trail Spend type: Card spend; Requirement or review: Needs the receipt and the policy check at the time of purchase Spend type: Travel; Requirement or review: May need both policy enforcement and later documentation review Give ownership to finance or an operations lead. The main inputs are your vendor list, team roster, approval rules, GL structure, and documentation requirements. The outputs you want are approved transactions, receipts or invoices on file, mapped accounting fields, and clean exports to your accounting system. If you use NetSuite, Brex states that it can pull in NetSuite fields and support GL and accounting-field mapping. The practical way to set this up is to decide, in order, what must be true before money moves and what must be true before the transaction is considered complete in accounting. That usually starts with normalizing your vendor list so repeat payments land under the same vendor record, not several slightly different names. Then align your team roster and approver chain so the right person is reviewing the right category of spend. After that, map the GL structure and any accounting fields you need on export, and only then finalize documentation rules. If you do those in reverse, you often end up with transactions that are approved quickly but coded inconsistently or missing backup. That sequence also helps you separate policy questions from bookkeeping questions. Policy answers whether the spend is allowed, who approves it, and what support is required. Bookkeeping answers where it lands, which fields must travel with it, and whether the accounting output is usable without cleanup. If your team tries to solve both at once inside day-to-day approvals, the work tends to drift into exceptions, manual fixes, and inconsistent treatment across similar payments. For remote startups, this matters because the same platform may be handling different transaction types that should not be governed in exactly the same way. A reimbursement needs proof of the underlying expense. Bill pay needs the invoice and the approver trail. Card spend needs the receipt and the policy check at the time of purchase. Travel may need both policy enforcement and later documentation review. Brex can help you enforce those lines at the point of spend, but it works best when you define those rules before the volume grows. Your pass or fail test is not whether a payment went through. It is whether each transaction got the right policy treatment, has the required documentation, and landed in the right accounting destination. Run a monthly sample check for receipt completeness, approver-policy match, and post-sync GL accuracy. Make that monthly sample check specific enough to catch drift. Pull a mix of cards, reimbursements, bill pay, and travel transactions. For each one, confirm that the required document is actually in the file, not merely requested. Confirm that the approver matched the policy you intended for that type of spend. Then confirm that the accounting export landed with the correct GL treatment and fields after sync, rather than assuming the mapping was correct because the sync completed. A useful review order is: Start with the original transaction and its category. Check whether the policy route matched your rule. Check whether the receipt or invoice in the file is the support you actually require for that transaction type. Check whether the exported accounting fields reflect what finance expects to see. Note any exception that required manual correction after sync. That review gives you a better control signal than headline metrics like payment success or sync success. A payment can move and a sync can complete while still leaving you with missing support, a broken approval chain, or a posting error that someone has to fix later. If you wait until close to find those issues, the correction work is slower and the process looks cleaner than it really is. This is also the point where ownership matters. Finance or an operations lead should own the configuration, but someone should also own exception handling. When a transaction comes through with partial documentation, a wrong approver, or a field mismatch, decide in advance what happens next. Either correct the transaction in place, kick it back to the requester, or document it as an exception. Without a clear owner, the same issue gets handled differently depending on who happens to notice it. Brex also states that it is a fintech company, not a bank, and that checking and banking services are provided by Column N.A., Member FDIC. Reflect that in your treasury documentation for account ownership and counterparties. Do not leave that as a website detail that never makes it into your internal records. Your treasury documentation should reflect who provides the service and how you identify the relevant counterparties for account ownership, internal approvals, and downstream recordkeeping. This is less about adding process for its own sake and more about keeping your internal documentation aligned with how the service is actually structured. If someone later reviews account setup, payment authority, or counterparties, you want the file to match the provider structure you relied on. In short, Step 1 is where you make Brex earn its place as the operational layer. Use it to standardize spend, approvals, support, and accounting outputs. Just do not mistake a disciplined spend workflow for a complete remote-work compliance workflow, because that is where the next layer starts.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Value-Based Pricing for Freelancers Under Real Payment Risk

Value-based pricing works when you and the client can name the business result before kickoff and agree on how progress will be judged. If that link is weak, use a tighter model first. This is not about defending one pricing philosophy over another. It is about avoiding surprises by keeping pricing, scope, delivery, and payment aligned from day one.

The Best Business Credit Cards for Freelancers

Pick for reliability first. For a freelancer, the right business card is usually the one that keeps recurring bills moving, keeps records clean, and avoids extra costs when income swings from month to month. Rewards still matter, but they sit on top of those basics. They do not replace them.

A Freelancer's Guide to the US-UK Tax Treaty

Start with your facts and filing setup before you interpret the treaty. For freelancers and consultants with US and UK income exposure, one common risk is assuming the treaty will sort everything out before your residency position, filing obligations, account status, and records are clear.