Quick Answer

Yes. To use a trust to avoid probate, create a revocable living trust, transfer intended assets into it, and name a successor trustee who can act at incapacity or death. Then verify each transfer is reflected in deeds, financial account records, and LLC documentation, because unfunded assets can still be pulled into probate. Keep a pour-over will and a practical successor file so missed items and handoff steps are documented.

Why a Revocable Trust is Your Business-of-One's Ultimate Control System#

If your goal is to use a trust to avoid probate, focus on continuity. A revocable trust can keep funded assets out of probate and let your chosen successor step in if you become incapacitated or die. The document matters, but the real result comes from title, records, and a handoff your successor can actually use.

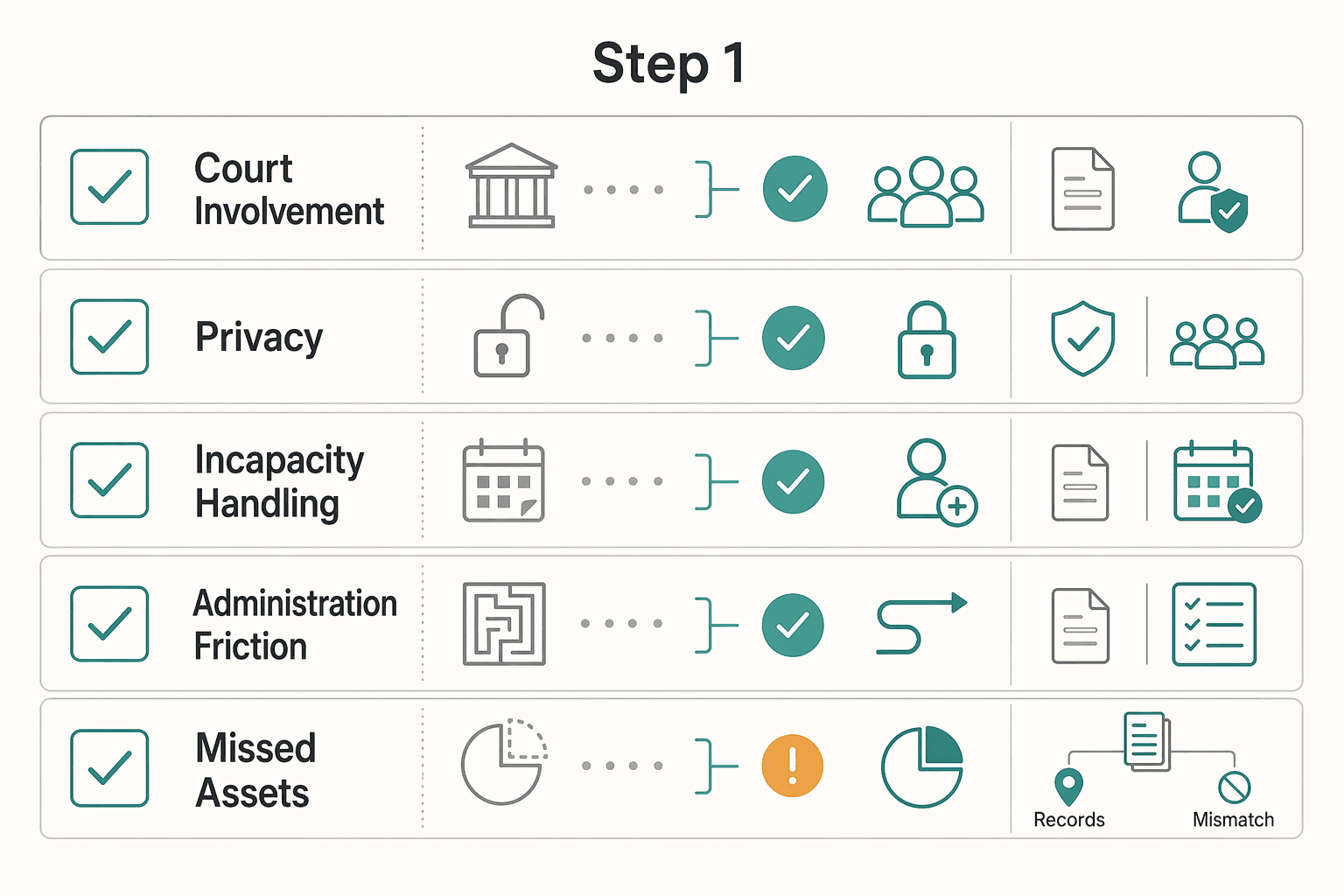

Step 1#

Start with role clarity. A trust changes title and succession, but in many revocable-trust setups you keep day-to-day control while alive. The role that matters later is the successor trustee, who can manage and distribute funded trust property without first getting probate-court authorization.

| Decision point | Will | Revocable trust |

|---|---|---|

| Court involvement at death | Generally must be filed and admitted to probate before terms are carried out | Usually administered outside probate for funded assets |

| Privacy | Probated will becomes a public document | Trust is generally not a public record |

| Incapacity handling | Will generally applies after death | Successor trustee can manage trust property during incapacity |

| Administration friction | Court filings and process are built in | Lower friction for funded assets, but disputes can still go to court |

| Missed assets | Handled through probate | Often routed by a pour-over will into the trust |

That comparison sets the baseline. A trust can reduce court friction, but it does not eliminate the need for clean drafting and clean records. If the trust language is unclear or trustee conduct is challenged, court review can still happen.

The practical point is that your successor trustee needs more than a name on paper. They need a file they can use. If incapacity happens first, they may need to show financial institutions what gives them authority over trust-owned property. If death happens first, they still need to identify what was actually funded, what was left outside the trust, and which assets pass by title versus beneficiary designation. A trust works best when those questions can be answered from the records without guesswork.

So this first step is less about theory than responsibility. You are not giving up ordinary control by creating a revocable trust. You are building a continuity structure so someone else can step in without rebuilding your life from fragments. If your successor trustee would have to call three institutions, search old email threads, and piece together deeds or account statements just to learn what the trust owns, the plan is still incomplete. That is true even if the document itself is well drafted.

Step 2#

Funding is where plans can fail. An unfunded or partly funded trust can leave the successor trustee with a good document and no practical control, so the sequence matters.

| Asset type | Treatment | Checkpoint |

|---|---|---|

| Real estate | Funding depends on title | Confirm the deed work was completed and retained |

| Financial accounts | Funding depends on account ownership records | Updated account records reflect the trust as owner |

| LLC interests | Funding depends on assignment plus company records | The assignment exists and the company records match it |

| Beneficiary-designation accounts | Treat as designation decisions, not blanket retitling | Check whether TOD paths still match your trust plan |

| Digital business assets | Review title, account access, and platform settings together | Make sure title, account access, and platform settings are not pulling in different directions |

Start by inventorying every asset you own or control. That can include real estate, financial accounts, LLC interests, digital business assets, and assets that pass by beneficiary designation. From there, separate the assets that should be retitled into the trust from the ones that require their own beneficiary or account-level review.

- Inventory every asset. Include real estate, financial accounts, LLC interests, digital business assets, and beneficiary-designation accounts.

- Retitle assets that belong in the trust. Funding means transferring title to the trust, then confirming records actually show the trust as owner.

- Review beneficiary designations separately. Retirement accounts follow plan procedures, and beneficiary rules changed for deaths after 2019; treat these as designation decisions, not blanket retitling. Also check whether TOD paths still match your trust plan.

- Prepare successor access records. Keep a usable packet: trust documents, certification, asset list, advisor contacts, and clear records for deeds, entity documents, and digital-access steps.

Use a simple test. If your successor had to act tomorrow, could they prove ownership, locate the right document, and tell which assets pass by title versus beneficiary designation?

Slow down here, because funding is not complete when you sign a transfer form. It is complete when the receiving institution or record system actually reflects the trust as owner. You also need proof of that change in a place your successor can find. For a financial account, that may mean updated account records. For real estate, it means confirming the deed work was completed and retained. For an LLC interest, it means the assignment exists and the company records match it. For digital business property, it means title, account access, and platform settings are not pulling in different directions.

A useful way to work through the inventory is to ask the same short set of questions for each asset and answer them from the file, not from memory:

- Is this asset titled, designated, or controlled some other way?

- Should it be moved into the trust, left outside with a separate beneficiary path, or reviewed before any change?

- What document proves the current setup?

- Where is that proof stored?

- Could someone else understand this asset from the file alone?

That process prevents a common planning mistake: assuming all assets should be treated the same. They do not. Some belong in the trust by title. Some need beneficiary review instead. Some involve a contract, platform, or operating agreement that has to be checked before you move anything. When people skip that sorting step, they often end up with a plan that looks finished in the estate-planning binder but fails under real administration pressure.

Your successor access packet deserves the same discipline. Do not think of it as a stack of legal papers. Think of it as an operating file. At minimum, it should let your successor identify the trust and prove they are the right person. It should also show what the trust owns, what sits outside it, and who to call. If there are deeds, entity records, assignment documents, or digital-account instructions, include those with enough labeling that a non-expert can tell what matters. The less reconstruction your successor has to do, the more likely the trust will deliver the continuity you expected.

Step 3#

Cross-border property and digital accounts need separate review. These assets often follow rules outside the trust document, so treat them as separate tracks, not edge cases.

For foreign real estate, outcomes depend on local law and practice. Do not assume a U.S. trust structure will be recognized as-is. Confirm local death and incapacity rules with local counsel. Then use the structure that works there, which may mean local title planning, a local will, or an entity layer owned by the trust where appropriate.

For digital assets, fiduciary access can be limited without user consent. Align trust fiduciary naming with platform legacy settings. Keep a current asset and account inventory. Use written assignments for digital business property so title and account control match.

Once you map those higher-risk assets, apply the same discipline to any related business interests. What makes these assets different is not that they are unusual. It is that they often involve one more system of control than the trust itself. Foreign real estate may be governed by local recording practice, succession rules, or local probate-style processes. Digital assets may be governed by account terms, platform permissions, or settings you created years ago and forgot about. In both cases, the trust may still be part of the solution, but it is rarely the whole solution by itself.

A practical way to handle foreign assets is to split the review into ownership, authority, and transferability. First, identify how the asset is currently held. Second, identify what local documents or local advice are needed so your successor can act during incapacity or after death. Third, make sure the records in your main trust file clearly say what was done and why. That way, your successor is not left guessing whether the foreign asset was intentionally left outside the trust, is held through another structure, or simply never finished.

Digital accounts need the same kind of mapping. An inventory that only lists the account name is not enough if access depends on legacy settings, specific account identifiers, or written assignments for digital business property. If the trust names a fiduciary but the platform settings point elsewhere, your successor may face delay. The same problem can happen if the business owns digital property informally without written assignment. The fix is practical: align the naming, keep the inventory current, and make sure business-related digital property is documented in a way that matches how you expect it to be controlled.

These assets can also drift out of alignment over time. You may open a new account, change a platform setting, move a domain, or buy property in another country after the trust is signed. That is why they should stay on your periodic review list even after the initial trust funding is done.

Step 4#

An LLC needs its own transfer check because trust ownership does not override the operating agreement. LLC transfer rights depend on the operating agreement and governing law, and an assignee may not automatically receive management rights.

| LLC transfer check | What to confirm |

|---|---|

| Legal transfer completed | Execute and retain membership-interest assignment documents |

| Operating agreement aligned | Confirm the trust is recognized and succession or management rights are explicit |

| Records and institutions updated | Record the transfer, handle any required state updates, and align bank records |

| Continuity controls ready | Make sure your successor can quickly locate governing documents, tax records, banking contacts, and key contracts |

The goal is not just moving the membership interest on paper. You want the trust recognized in the company records, the bank records, and the succession terms your successor will rely on under pressure. Focus on these outcomes:

- Legal transfer completed: execute and retain membership-interest assignment documents.

- Operating agreement aligned: confirm the trust is recognized and succession or management rights are explicit.

- Records and institutions updated: record the transfer, handle any required state updates, and align bank records.

- Continuity controls ready: make sure your successor can quickly locate governing documents, tax records, banking contacts, and key contracts.

Failure points include ignoring transfer restrictions, failing to record the transfer, and assuming banks or counterparties will accept trustee authority without updated documentation. A good check is whether your successor could prove authority over the LLC, core accounts, and digital assets without having to reconstruct the file from scratch.

This is where many business owners overestimate what the trust document can do by itself. The trust may say who should control the membership interest, but the operating agreement may still control how that interest is recognized inside the company. If the trust is not reflected in the company records, or if management rights are not clearly addressed, your successor may inherit confusion instead of continuity.

Treat the LLC transfer as a short chain that is only as strong as the weakest link. The assignment document matters. The operating agreement review matters. The internal records matter. The bank relationship matters. If one of those pieces is out of sync, that is often where administration slows down. A bank may ask for trustee documentation. A counterparty may ask who has authority to sign. A successor may find the trust owns the interest in principle but the company file still points to an outdated structure in practice.

A cleaner approach is to close the loop each time you update ownership. After the assignment is signed, confirm the company file reflects it. After the company file is updated, confirm the bank records are aligned. After that, make sure the successor packet includes the current operating agreement, the assignment, key tax records, banking contacts, and the contracts that matter most to ongoing operations. The question is not whether a lawyer could eventually sort it out. The question is whether your successor could keep the business functioning while that sorting happens.

If you want a deeper dive, read A Guide to Estate Planning for Digital Nomads.

As you build your asset inventory checklist, keep client-payment records clean and exportable with Gruv's Free Invoice Generator.

Your Legacy, Secured: The Trust as Your Final Act of Professional Control#

If your goal is probate avoidance, aim for a fully funded revocable living trust your successor trustee can administer for trust assets without probate delay.

When that is done well, the benefits are practical, not abstract. Continuity comes from having assets actually in the trust, because trustee authority applies to trust property, not assets left outside it. Your successor trustee can manage and distribute trust property without first going through probate court. Privacy can improve because probate filings can place will terms and probate-asset lists in the public record, while trust administration is often less public. Control comes from clear instructions, complete funding, and a handoff your successor can execute.

Before you rely on the plan, use this checkpoint to test funding, beneficiary alignment, document access, and handoff readiness:

- Funding completeness: confirm each intended asset was transferred into the trust and keep proof.

- Beneficiary alignment: review beneficiary-designated assets, such as retirement plans and life insurance, separately, since they are non-probate and can pass outside the trust.

- Document access: make sure trust documents, amendments, deeds, statements, and your asset list are easy for your successor trustee to access.

- Advisor handoff readiness: give your successor trustee current contact details for your lawyer, accountant, and key financial institutions.

Keep the scope clear. This is primarily a probate-avoidance and transition-planning tool. Creditor protection and tax outcomes are not automatic, and they depend on trust design and applicable law.

The strongest final review is not theoretical. Walk the file the way your successor would. Can they identify the current trust documents? Can they tell which assets are funded and which are not? Can they see who to contact about the real estate, the LLC, the foreign assets, and the digital accounts? Can they distinguish between assets controlled by title and assets controlled by beneficiary designation? If not, the next task is not drafting more language. It is finishing the operational side of the plan.

That is what turns a revocable trust from a signed document into an actual control system. Not more complexity. Just cleaner ownership, clearer records, and a successor who can step in without starting from zero.

For a related topic, see A Guide to Superannuation for Australian Freelancers. If you want your cross-border money movement to be as controlled and audit-ready as your estate plan, discuss fit and market coverage with Gruv via Contact.

Frequently Asked Questions

How do you put international assets into a living trust?

Treat international assets as a verify-first item. Confirm requirements with the relevant institution or local counsel before making changes. After any change, keep records in your trust file so your successor can see what was completed.

What is the difference between a revocable and irrevocable trust?

A revocable living trust can usually be changed or revoked as circumstances change. Probate avoidance depends on whether assets were actually transferred into the trust. Specific comparisons for irrevocable trusts should be verified with a qualified adviser before you rely on them. | Decision cue | Revocable trust | Irrevocable trust | | --- | --- | --- | | Control | You can usually update or revoke terms | Confirm with a qualified adviser | | Probate avoidance | Depends on assets actually being transferred into the trust | Confirm with a qualified adviser | | Creditor exposure | Do not assume lawsuit shielding | Confirm with a qualified adviser | | Tax handling complexity | Confirm with a qualified adviser | Confirm with a qualified adviser | | Best fit if | You want continuity and probate avoidance with a trust you can update | Verify fit with current legal advice |

Can I be my own trustee in a living trust?

Yes. That is common in a revocable trust, and the grantor commonly serves as trustee while managing trust assets. Also name a successor trustee who can step in at incapacity or death and work from clear records.

What is the step-by-step process for funding a trust?

Use a simple sequence: inventory assets, transfer assets into the trust, and verify records changed. For real estate, a key checkpoint is confirming a new deed was recorded in the trust name. Keep copies of transfer and title records in your trust file.

Does a living trust protect my assets from lawsuits?

Treat a revocable trust as a continuity and probate-avoidance tool when properly funded. If your goal is asset protection, review structure-specific tradeoffs first, including A Guide to Setting Up a Trust for Asset Protection.

How much does it cost to set up a living trust?

Costs vary by situation. Plan for both the trust setup and the follow-through work needed to fund it, including transfer and record updates. Verify current local pricing before relying on any generic estimate.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- alameda.courts.ca.gov/living-truststrusted

- consumerfinance.gov/ask-cfpb/what-is-a-revocable-living-trust-en...trusted

- delcode.delaware.gov/title6/c018/sc07/index.htmltrusted

- ecfr.gov/current/title-26/chapter-I/subchapter-B/part...trusted

- investor.gov/introduction-investing/investing-basics/glos...trusted

- irs.gov/businesses/small-businesses-self-employed/ab...trusted

- irs.gov/individuals/international-taxpayers/some-non...trusted

- marin.courts.ca.gov/divisions/probatetrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

When a Trust for Asset Protection Makes Sense for Your Business

Use a trust only after your core liability setup is solid. A trust for asset protection is an escalation layer, not a substitute for entity separation, insurance, or clean operations.

Estate Planning for Digital Nomads: Legal Intent and Cashflow Continuity

Treat estate planning for digital nomads as a two-part continuity system: legal intent plus operational execution, so your business keeps moving when you cannot. The common trap is thinking, "I have a will, so I'm covered." If you run a business-of-one, cashflow, logins, and process often live in your head until you deliberately externalize them.

A Guide to Superannuation for Australian Freelancers

**Treat superannuation for freelancers australia as a repeatable operating decision, not a guess you make under invoice pressure.** As the CEO of a business-of-one, your job is to turn fuzzy compliance questions into a simple system you can run on demand. Freelance income moves, contract terms shift, and one wrong super call can squeeze cashflow or create a compliance problem you only notice later.