Quick Answer

Build a mortgage-ready file, not a formal stability report for freelance mortgage approval. Start with a one-page thesis memo, then attach reconciled tax records, income worksheets, and reserve documentation that map cleanly to deposits and contracts. Keep qualifying-income and repayment-income views distinct, and present everything in an indexed package so an underwriter can verify assumptions without chasing missing context.

The Myth of the "Stability Report": Why You Need a Thesis, Not a Document#

If you are looking for a "stability report," pause here. In the Fannie Mae Selling Guide materials shown here, there is no borrower document labeled a "stability report." What you do see is the Selling Guide itself, with a downloadable PDF, plus Ask Poli and Guide Resources for policy questions and related forms.

That helps. Once you stop looking for one perfect document, you can build an organized portfolio of evidence around a central argument: your Stability Thesis.

Think of the Stability Thesis as the cover letter for your mortgage application. It can be a concise executive summary that makes a clear case for your financial strength and gives an underwriter context for the file. The job is not to oversell. It is to reduce uncertainty.

The core argument is simple: resilience can look different from a single-paycheck model. A traditional file may center on one employer. A self-employed file may center on multiple clients and revenue streams. Your job is to explain that structure clearly and back it with documentation.

| W-2 Employee | Global Professional (Business-of-One) |

|---|---|

| Income often comes from a single employer. | Income may be spread across multiple clients or projects. |

| A job loss may materially disrupt income. | Losing one client may reduce income, but not necessarily eliminate it. |

| Stability is often tied to one company. | Stability can be supported by diversified demand. |

This reframing matters because it positions you less as an exception file and more as a documented, durable business.

Use your documented track record to support that narrative. The excerpted Fannie Mae page is an entry point, not a complete checklist by itself. It points you to the Selling Guide, Ask Poli, and Guide Resources for policy detail and related documents.

Related: Using a Stability Report to apply for a UK mortgage as a freelancer with international clients.

Building Your Underwriting Package: The Evidence for Your Thesis#

Once you accept that there is no single "stability report," the real task becomes building a file that is easy to verify, reconcile, and defend. If you came looking for a stability report for freelance mortgage approval, this is the practical substitute: a clean evidence set that supports stable repayment income and removes avoidable underwriting questions.

That structure matters because lenders are responsible for documenting qualifying income and supporting their calculations. In USDA SFHGLP guidance, repayment income is defined as stable, dependable income used for affordability analysis, and the lender is responsible for eligibility and documentation. USDA Chapter 9 also states this applies to both manually underwritten loans and AUS-assisted loans. Program rules vary, but the operational takeaway is consistent: give underwriting a file they can document cleanly.

Core documentation#

Start with the base package, then use current lender, adviser, and program records to decide which lender-specific or program-specific requirements belong in the file. For a broader map of loan paths for self-employed borrowers, see Gruv's guide to getting a mortgage as a freelancer.

| Documentation | What to include |

|---|---|

| Tax returns, transcripts, and IRS documentation used in underwriting | Where required, keep signed IRS documentation in the Origination File and make sure it matches the unsigned tax returns/transcripts used for underwriting. |

| Income-by-income verification records | Include the supportive documentation required for each income type in the lender's permanent file. |

| Repayment-income support | For income types that require explicit support before inclusion, include that support so the repayment-income calculation is defensible. |

| Calculation worksheet | Use a clear income-calculation worksheet format so inputs and adjustments are traceable; USDA Chapter 9 includes Attachment 9-A as a sample worksheet. |

The main risk you are reducing is income exclusion because the support is weak or incomplete. Name, account, and label consistency across documents can also create friction when records are reviewed. That is part of maintaining a coherent financial identity.

Your underwriter-ready P&L#

A standard export may not map cleanly to underwriting calculations on its own. Keep your working income worksheet aligned with the verification records in file, and make adjustments explicit so a reviewer can follow the logic.

Use your notes in three blocks:

- Qualifying income view: Show adjusted annual income used against SFHGLP income limits, when USDA SFHGLP is the applicable program.

- Repayment income view: Show the stable, dependable income used for debt-ratio and affordability analysis.

- Annual income assumptions: Show anticipated coming-year income inputs used in the calculation.

Final check: your worksheet should reconcile to the verification records and supportive documentation already in the permanent file.

The client diversification report#

Use a one-page table if it helps present concentration patterns clearly.

| Client / group | Share of last 12 months revenue | Revenue type | Relationship length | Evidence in file |

|---|---|---|---|---|

| Largest client | Verified share from last 12 months records | Retainer / repeat project / one-time | Verified relationship duration | Contract, invoices, deposits |

| Second-largest client | Verified share from last 12 months records | Retainer / repeat project / one-time | Verified relationship duration | Contract, invoices, deposits |

| Third-largest client | Verified share from last 12 months records | Retainer / repeat project / one-time | Verified relationship duration | Contract, invoices, deposits |

| Other clients | Combined verified share | Mixed | Mixed | 1099s, invoices, deposits |

The readout is straightforward: use it to explain concentration and relationship patterns with records already in the file.

Financial bedrock#

Narrative helps, but underwriting still turns on current lender and program criteria beyond file organization. Treat each one as a lender-calibrated check and verify criteria directly instead of relying on generic online thresholds.

For credit depth, confirm current lender and insurer standards. One program-specific example: Enact guidance effective January 10, 2025 references a minimum of three tradelines or credit references, open or closed, evaluated for at least 12 months per borrower. For DTI treatment and down-payment documentation, confirm the current requirement in lender, adviser, or official program records before using it in the file.

In practice, keep this section program-specific. Document what the active lender or insurer currently requires and keep records in file so they are producible on request. A strong story helps, but verified criteria and complete documentation drive decisions. If you want a deeper dive, read Should Your Freelance Business Accept Credit Cards?.

The Global Professional's Edge: Turning Complexity into a Strength#

Global complexity can work in your favor if the file is easy to read. When income crosses currencies, platforms, and countries, make each payment traceable from contract or invoice to final deposit so a reviewer can follow it without guesswork. That discipline also fits the broader plan in Gruv's guide to getting a mortgage as a freelancer.

The same habit matters beyond mortgage files. The National Taxpayer Advocate's 2025 Annual Report to Congress highlights severe compliance burdens for U.S. taxpayers living abroad and also flags harm from outdated paper processes and procurement delays. The practical takeaway is clear: do not leave context implicit. Put it in the file up front, the same way you build a coherent financial identity.

A practical way to normalize multi-currency income#

One practical documentation template is a master summary sheet with every line tied to documents:

- Build one sheet listing each foreign-currency payment.

- Normalize payments line by line instead of estimating monthly totals.

- Use one exchange-rate method consistently and label the basis you used.

- Match each line to invoice or remittance, platform statement, and receiving bank statement.

Treat this as an organization template, not a universal underwriting standard. The point is consistency. If normalized and deposited amounts differ because of conversion spread or platform deductions, note the variance directly.

| Payment Date | Client / payer | Original Amount | Currency | Exchange-Rate Method Used | Normalized Amount |

|---|---|---|---|---|---|

| Payment date from source record | Client or entity name from source record | Original amount from source record | Source currency | Receipt-date rate, platform-settlement rate, or another labeled method | Calculated home-currency amount |

| Next payment date from source record | Client or entity name from source record | Original amount from source record | Source currency | Documented conversion method | Calculated home-currency amount |

If you use this sheet, cross-check each row against your invoice or remittance, platform or wallet statement, and receiving bank statement. If names differ, add a short alias note so legal entity names, trade names, and platform labels still reconcile.

When an EOR or processor sits in the middle#

Intermediaries can obscure the transaction path, so spell it out. A short reconciliation note can connect the original invoice amount to intermediary adjustments, net payout, and destination account evidence.

Keep it compact. One line per payout can be enough when the documents match. A common documentation gap is a net deposit with no clean path back to the originating amount, especially when the bank statement names the platform instead of the client.

Contracts in another language#

Translation expectations vary by reviewer and jurisdiction. Use a clear English summary for readability, then confirm directly when a certified translation is required.

A consistent summary format can help: client name, contracting entity, effective date, term or renewal structure, scope, payment frequency, currency, termination terms, and the evidence document it maps to. If you reference regulatory text in your memo, record its recency markers. For example, eCFR pages can show an "up to date as of" date and also note the content is authoritative but unofficial.

For a step-by-step walkthrough, see How to Handle a Signing Bonus for Freelance Contractor Work.

Think Like an Underwriter: De-Risk Your Application Before You Submit#

Underwriting is a risk review. Your job is to make risk easy to evaluate, not to argue that freelancing is valid. A core question is whether you look likely to repay consistently over a long horizon, often framed as 15 to 30 years. Your package should answer likely objections before they become conditions.

If you came here looking for that kind of report, treat this as the practical equivalent: a file that pairs each concern with evidence. It follows the same discipline as a coherent financial identity: consistent records that reconcile quickly.

Start with objections, then map evidence#

Lead with the concern, then point to the exhibit that resolves it:

- Income looks uneven: Show tax returns and a clear summary that ties invoices to deposits.

- Assets may not be usable: Show statements for down payment, closing costs, and reserves, plus transfer trails for recent movement.

- Debt load may be tight: Show monthly debt payments against gross monthly income, then verify the actual program rule with the lender. Some programs cite benchmarks like 43%, but no single cutoff is universal.

- Property risk remains unclear: You cannot control appraisal outcomes, but you can avoid adding preventable income or asset ambiguity.

- Small inconsistencies signal bigger risk: Fix mismatched names, unexplained deposits, and date gaps before submission.

One high-impact check is name reconciliation. If your legal name, trade name, and platform labels differ, add one alias note and reuse it across the application, tax returns, statements, contracts, and payout records.

Turn reserves into a verifiable runway#

Reserves help only when they are documented, not implied. Present them as a short calculation tied directly to source statements:

- Pull current statements for each account you want counted, and confirm ownership matches the borrower or business entity in the file.

- Build one worksheet with three buckets: down payment, closing costs, and reserves remaining after closing.

- If you model payment endurance, show proposed housing payment plus other fixed obligations, and leave lender-specific reserve thresholds unresolved until current lender records, adviser notes, or official documents confirm the applicable criteria.

Place this worksheet right after the asset statements so the review runs in a straight line. If funds moved between accounts, show both sides of the transfer so one balance is not mistaken for two separate assets.

Use forward-income documents that are decision-useful#

Forward-income evidence helps when it looks like a real commitment, not a hopeful signal. Signed, dated documents with clear work and payment terms are usually easier to evaluate.

There is no single field list that every underwriter accepts. Use your lender's required format, and make sure the core terms are explicit rather than implied.

These documents are most credible when they show continuity. If a renewal or new contract connects to a client already visible in prior invoices and deposits, note that link directly.

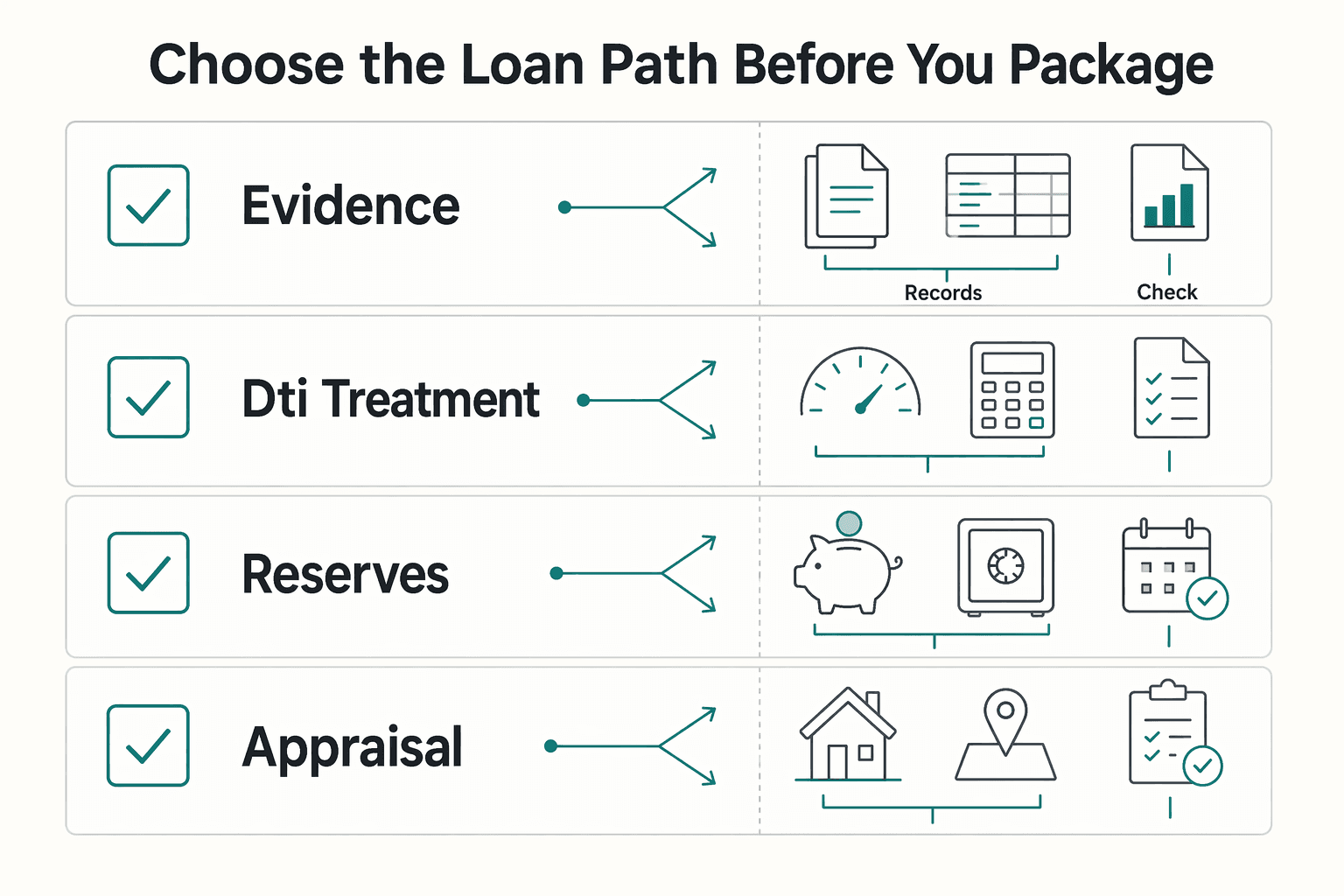

Choose the loan path before you package#

Choose the path first, then shape the file to match it. Loan programs may evaluate income and documentation differently, so confirm the rules before you assemble exhibits.

| Aspect to confirm | Question to ask your lender |

|---|---|

| Income documentation | Which income documents are required for this program? |

| DTI treatment | How are monthly debt payments compared with gross monthly income for this program? |

| Reserves | What reserve documentation and thresholds apply? |

| Appraisal | How does property appraisal affect conditions or approval? |

If you need the broader decision framework, use Gruv's guide to getting a mortgage as a freelancer.

Submit an audit-ready file#

An audit-ready package can reduce confusion during review. Use one indexed PDF, a concise opening memo, consistent exhibit names, and cross-references from every summary sheet to the supporting exhibit.

Before submission, run a quick blind test: ask someone unfamiliar with your business to locate one deposit, one reserve figure, and one contract payment term quickly. If they struggle, tighten the structure before sending.

You might also find this useful: Future of Financial Identity for Nomads Seeking Loans.

Turn your underwriting prep into a repeatable monthly checklist so your records are always mortgage-ready, not rushed at application time. Use the Gruv Tools hub.

Conclusion: You Are Not a Risk. You Are a Business.#

Securing a mortgage starts with how you frame the file before you submit the first document. Traditional lending systems can fit salaried employees more cleanly than self-employed owners. For self-employed borrowers, underwriting centers on stable monthly income and documentation. That is why it helps to stop thinking like an applicant hoping for approval and start acting like the CEO of your Business-of-One, presenting a clear case for approval.

This framework is about controlling what you can control. The process is designed to evaluate repayment risk in detail, especially for self-employed files. Your job is to eliminate avoidable concerns early. Where they see income fluctuation, show consistent patterns with organized records of business income, expenses, and tax returns. Where they see complexity, present clarity through complete financials and tax documentation.

This is more than paperwork. It is the work of curating the financial identity of your business so an underwriter can quickly understand the story behind the numbers. When your application reads as a cohesive financing proposal instead of a stack of disconnected forms, the review can move more cleanly.

In the end, this is less about finding the right form and more about building the right file. The system may require additional documentation and due diligence for self-employed applicants, but with clear records and profitable tax history, often shown through two years of tax returns demonstrating a profit, you can show what is already true: you are running a business.

We covered this in detail in Build a Pitch Deck for a High-Value Freelance Proposal.

If your income setup is cross-border and you want to confirm the right operational path before your next application, contact Gruv.

Frequently Asked Questions

What is a stability report for a freelance mortgage?

There is no official lender or government form called a stability report for freelance mortgage. In practice, people use the term informally for the documentation package an underwriter reviews to assess income consistency and ability to repay. That package is typically built from tax returns, bank statements, and profit-and-loss records that show income is likely to continue, organized so a reviewer can move from summary to evidence quickly, like a consistent financial identity.

How do I show multi-currency income on a mortgage application?

The sources here do not define a standard multi-currency format. A practical approach is to keep one clear consolidation record in the lender’s working currency, tie entries back to your core documents, and confirm the lender’s required conversion method and evidence format before submission.

How do I create a profit and loss statement for a mortgage underwriter?

Use a current P&L that stays consistent with your tax returns and bank statements. Keep it clear enough for an underwriter to follow, then confirm totals and supporting records align before submission.

Is a bank statement loan a good idea for a high-earning freelancer?

Bank-statement-loan criteria vary by lender, so treat this as lender-specific. Before choosing that path, verify the lender's current requirements and compare them against your standard path in the guide to getting a mortgage as a freelancer.

Do I absolutely need two years of freelance history to get a mortgage?

There is no universal rule in the sources here, so do not assume one fixed timeline applies everywhere. What lenders are often trying to verify is income that appears stable and likely to continue, supported by clear documentation. Ask your lender for the exact evidence window they use, then strengthen your file with a clean underwriting package.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- ecfr.gov/current/title-7/subtitle-B/chapter-XXXV/part...trusted

- fcic-static.law.stanford.edu/cdn_media/fcic-reports/fcic_final_report_ful...trusted

- hud.gov/sites/dfiles/OCHCO/documents/4000.1hsgh-0118...trusted

- hud.gov/sites/documents/41551hsgh.pdftrusted

- huduser.gov/portal/sites/default/files/pdf/Short-Term-Im...trusted

- irs.gov/pub/irs-pdf/p2104.pdftrusted

- occ.treas.gov/publications-and-resources/publications/comp...trusted

- oig.treasury.gov/system/files/2026-02/OIG-26-014-%28508%29.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Should Your Freelance Business Accept Credit Cards?

Offer card payments, but stay in control of how money reaches you. The goal is not a smoother checkout screen. It is predictable cash you can use to run the business.

Getting a Mortgage as a Freelancer Without Guesswork

Start by reconciling your income file before you compare rates. For a **mortgage for freelancers**, the first gate is simple: can an underwriter read your documents cold and see one consistent income story?

What is a 'Financial Identity' and Why Do Nomads Need One?

Your financial identity should function as portable proof. It can help you get paid across borders, clear reviews faster, and control risk when your life does not fit the one-address, one-employer, one-country model many institutions still assume.