Quick Answer

A freelancer can use a prior-year net operating loss to reduce future income tax by carrying it forward to offset later taxable income. For business losses arising in tax years 2021 or later, the carryforward is generally indefinite, but the deduction in any future year is limited to 80% of taxable income. The loss must be calculated under IRS NOL rules, and it does not reduce self-employment tax.

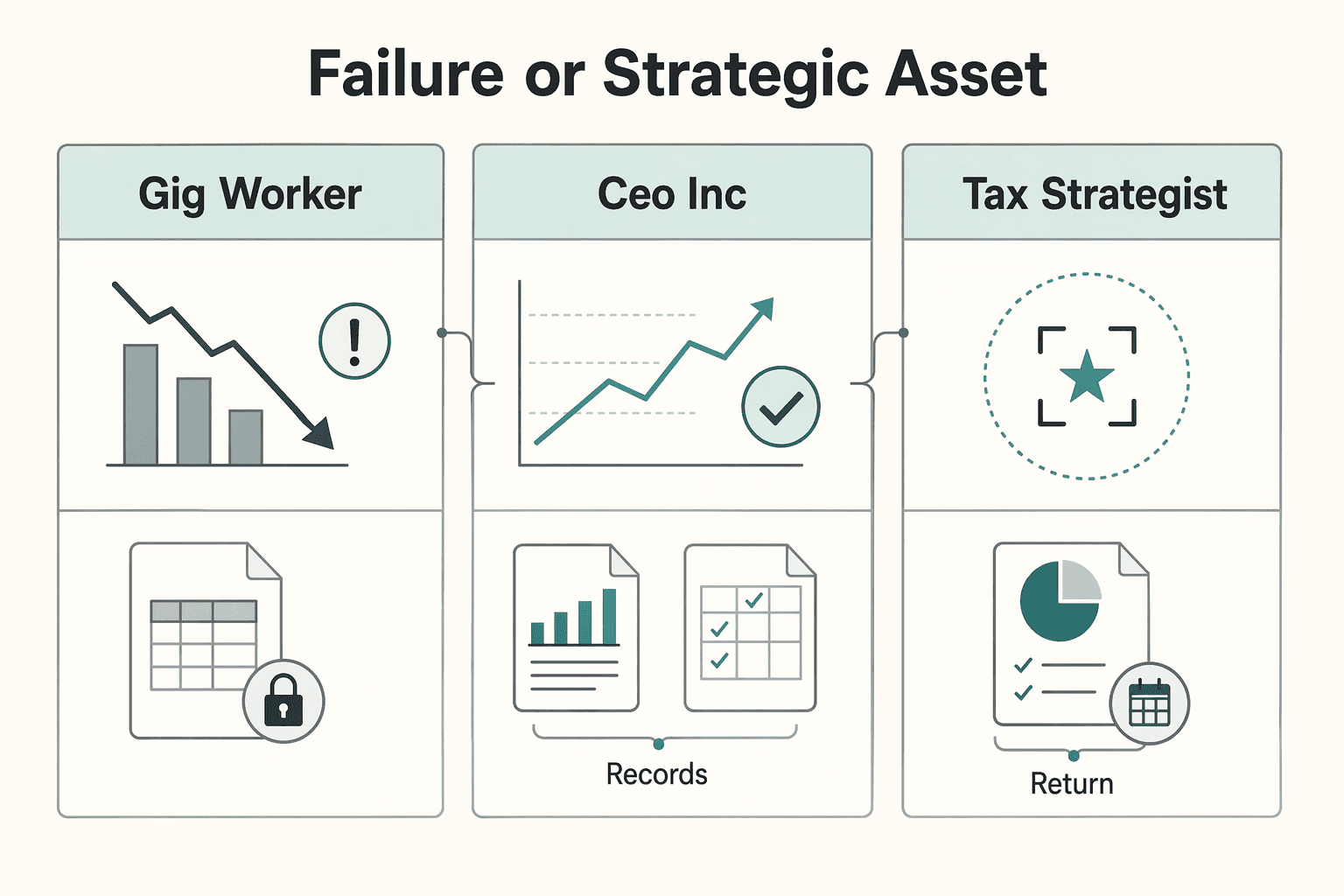

The CEO's Playbook for Loss Carryforward: Turning a Business Loss into a Strategic Tax Asset#

Adopting a CEO's perspective requires a shift in how you read your business's financial story. It's the difference between reacting like a gig worker and planning like an executive. A loss can feel like something that happened to you; the CEO of "Me, Inc." treats it as a data point that demands a strategic response. This isn't just semantics. It's how you turn a potential liability into a useful asset. A business loss is not a sign of failure; it is the cost of ambition, and with the right playbook, it can fuel future tax savings.

In the end, this is about reframing the emotional context of a difficult financial year. You must consciously move from the anxiety of "I lost money" to the more grounded, strategic position of "I have a $20,000 tax asset I can use to offset future income." This is the playbook. It's how you take control.

A Business Loss: Failure or Strategic Asset?#

For the CEO of "Me, Inc.," a business loss is not a mark of failure; it is a financial event to manage and use. The distinction between a reactive gig worker and an owner thinking like a CEO comes down to this viewpoint. One sees a setback; the other sees an opportunity.

| Mindset | View of a Business Loss | Primary Action | Strategic Outcome |

|---|---|---|---|

| The Gig Worker | A personal failure; a source of financial anxiety. | Reacts with damage control and stress. | Missed opportunity and prolonged financial uncertainty. |

| The CEO of "Me, Inc." | A data point; a planned investment or a manageable market event. | Acts with precision to document the loss as a future tax asset. | Enhanced financial resilience and future tax savings. |

| The Tax Strategist | A temporary earnings trough with documented carryforward value. | Models carryforward usage across multiple tax years before filing. | Higher confidence in cash-flow planning and audit readiness. |

This mindset shows up in two common scenarios:

- Scenario 1: The Intentional "Investment Loss"

This is a loss you create on purpose. You are not just losing money; you are allocating capital. Imagine you're a freelance software developer. You might choose to invest $50,000 in high-performance computing equipment and specialized AI certifications within a single tax year. That large outlay could push your Schedule C into the red, creating a significant net operating loss (NOL). The gig worker sees a year with no profit. The CEO sees a year in which they acquired meaningful assets and created a tax asset that may reduce income tax in future, higher-earning years. You are deliberately trading today's profit for stronger positioning later.

- Scenario 2: The Unplanned "Market Loss"

This is the loss you didn't ask for. A major client terminates a contract, or a market shift makes your primary service obsolete for a few quarters. The emotional response is anxiety. The strategic response is to pivot from damage control to asset creation. The moment you confirm the revenue shortfall, your objective is to carefully document every expense so the downturn results in a clean, defensible NOL. This transforms the narrative from "I lost a client and my income plummeted" to "The market shifted, and I've now unlocked a tax asset that I can carry forward." This approach ensures that even a difficult year has future upside.

Decoding the Net Operating Loss (NOL)#

To use this tool well, you need a precise understanding of how it works. A Net Operating Loss (NOL) is a formal tax concept, and the details matter. It's not enough to simply have more expenses than income; the IRS has a specific definition and a detailed calculation in IRS Publication 536 that every business-of-one must follow. Get those details right, and you reduce compliance risk while preserving the full value of the carryforward. If you also plan around pass-through deductions, this pairs well with A Guide to the Qualified Business Income (QBI) Deduction for Freelancers.

- It's More Than the Negative Number on Your Schedule C. An NOL is a specific calculation. The official starting point isn't your business loss, but your Adjusted Gross Income (AGI) from your Form 1040. From there, you must make several modifications - typically on a worksheet found in IRS Publication 536 - to isolate the true business loss. This process involves adding back certain non-business deductions, such as the standard deduction or the Qualified Business Income (QBI) deduction, to show that the loss came from your core business operations.

- The Current Rules (Post-TCJA). The Tax Cuts and Jobs Act (TCJA) significantly changed the rules for NOLs. For any business loss arising in tax years 2021 or later, the rules are clear:

- Indefinite Carryforward: You can carry the loss forward indefinitely; the old 20-year limit is gone. * No Carrybacks: The general ability to "carry back" a loss to a prior tax year to get an immediate refund has been eliminated for most freelancers. * The 80% Limitation: The NOL deduction you can take in any single future year is limited to 80% of that year's taxable income. For example, if you have a $50,000 NOL and $100,000 in taxable income the next year, the 80% cap would be $80,000, so the cap would not limit you in that year. This rule matters when you model how quickly you can use the loss and how much tax savings it can produce over time. For workflow planning, keep the model inputs in one place, such as your tax worksheet plus your project finance notes in Browse Gruv tools.

- The Critical Self-Employment Tax Limitation. This is an important detail that trips up many freelancers. An NOL carryforward can dramatically reduce your income tax in future years, but it does not reduce your self-employment tax. The Tax Court has repeatedly confirmed this. You will still owe self-employment tax on future net profit, a vital fact for accurate financial planning, and the IRS Self-Employed Individuals Tax Center is a useful operating reference.

- Operating Loss vs. Capital Loss. You must understand the bright line between these two concepts. An Operating Loss comes from the primary activities of your trade or business - client revenue, software subscriptions, marketing costs. A Capital Loss comes from the sale of investments like stocks or cryptocurrency for less than their purchase price. The rules for deducting these losses are completely different, and you cannot use a capital loss from your investment portfolio to create or increase a net operating loss for your business.

Your 3-Step Playbook to Calculate and Model Your Tax Savings#

Understanding the rules is one thing; putting them to work is where you regain control. This is a practical framework for turning a business loss from a source of anxiety into a clearly defined tax asset.

- Phase 1: Calculate Your Asset with Precision. Your first move is to establish the official, IRS-recognized value of your loss. The negative number on your Schedule C is merely the starting point. The real work happens on the worksheets provided in IRS Publication 536, which guide you through the necessary adjustments - like adding back your standard deduction - to isolate the loss generated purely by your business operations. This isn't just about compliance; it's about creating a definitive, auditable number that anchors your strategy.

- Phase 2: Model the Financial Impact. Once you have your official NOL amount, make the benefit tangible. An abstract asset doesn't help you plan; a concrete projection does. Run a simple scenario analysis so you can see what the carryforward means for your future cash flow. For instance, a calculated $30,000 NOL has a clear effect.

| Taxable Income (Future Year) | NOL Deduction (Limited to 80% of Income) | Adjusted Taxable Income | Potential Federal Tax Savings (at 24% bracket) |

|---|---|---|---|

| $50,000 | $30,000 | $20,000 | $7,200 |

| $100,000 | $30,000 | $70,000 | $7,200 |

| $180,000 | $30,000 | $150,000 | $7,200 |

This simple act of modeling transforms a vague future benefit into a specific amount you can factor into your financial plans. It turns anxiety into a clear projection of real tax savings.

- Phase 3: Document to Defend. An undocumented claim is just a number on a form. A documented claim is much easier to defend. As Ken Berry, a tax attorney and correspondent for CPA Practice Advisor, states, "A taxpayer claiming a Net Operating Loss bears the burden of establishing both its existence and the amount that can be carried over... you must be able to provide the underlying records that substantiate what you have reported." This is non-negotiable. Create a dedicated digital "NOL Compliance File" for the year the loss occurred. This folder should contain organized copies of every document that supports the expenses contributing to your loss, including:

- Invoices and receipts for all equipment, software, and significant purchases. * Bank and credit card statements with business expenses clearly marked. * Contracts with clients and subcontractors. * Detailed mileage logs and travel expense records.

This preparation materially reduces compliance risk. It shows that you can support the number if the IRS ever asks.

The S-Corp Factor: A More Sophisticated Playbook#

If you move from a sole proprietorship to an S-Corp, the same strategic idea still applies, but the mechanics change. The core benefit of a loss carryforward remains, but it demands a more sophisticated approach. The S-Corp itself does not carry forward a loss; instead, the loss passes through to you, the shareholder, to be used on your personal tax return. If you operate internationally, map this tax structure alongside domicile and filing exposure in The Ultimate Digital Nomad Tax Survival Guide for 2025.

- The Pass-Through Principle: An S-Corp is a distinct legal entity, but for tax purposes, it's a conduit. The corporation doesn't pay income tax; instead, profits and losses flow directly to the shareholders' personal tax returns via a Schedule K-1. A business loss at the corporate level, therefore, lands on your personal return, where it can offset other income sources - like your S-Corp salary - to create a personal net operating loss (NOL).

- The "Reasonable Salary" Constraint: This is a non-negotiable rule. You cannot simply stop paying yourself a salary to manufacture a larger paper loss. The IRS requires S-Corp shareholder-employees to be paid a reasonable salary for the services they perform before any other profits are distributed. The IRS actively scrutinizes this to ensure owners are not avoiding payroll taxes, and its S-corporation compensation guidance is a practical checkpoint. Trying to game this rule invites scrutiny.

- The "Basis" Limitation Trap: This is the most critical and often misunderstood compliance checkpoint for S-Corp owners. You can only deduct corporate losses on your personal return up to the amount of your "basis" - your total financial investment in the company. It is generally calculated as:

- Stock Basis: The cash and property you've contributed to the company for stock. * Debt Basis: The amount of any direct loans you have personally made to the corporation.

If your share of the corporate loss is $40,000, but your total basis is only $15,000, you can only deduct $15,000 in the current year. The remaining $25,000 is not lost forever. It becomes a "suspended loss," which you can carry forward indefinitely and deduct in a future year once you have sufficient basis. This makes basis planning a critical component of your NOL strategy if you operate through an S-Corp.

From Liability to Asset: You Are in Control#

A business loss is only a liability if you treat it as one. By understanding the mechanics of the Net Operating Loss and applying a disciplined, strategic framework, you turn what feels like a setback into a valuable financial asset. This shift in perspective is the essence of operating as a true Business-of-One. It is about taking every circumstance - especially the challenging ones - and deliberately using them to your long-term advantage.

Knowledge is only the first step. Control comes from application.

- Embrace Early Planning: Instead of just reacting to a down year, you can now plan for strategic investments, knowing you may be generating a future tax asset to deploy against higher-income years.

- Commit to Careful Documentation: Your "NOL Compliance File" is your shield. This habit of rigorous record-keeping is what separates professionals who control their finances from amateurs who are controlled by them.

- Leverage Professional Expertise: Being in control also means knowing the limits of your own expertise. Engaging a qualified CPA is not just a cost; it can be an investment in executing your NOL strategy correctly and defending it with confidence.

You have the knowledge. You have the playbook. A down year is no longer just a failure; it's a data point that can produce future tax savings. The numbers on your return are not just a summary of the past - they are tools you can use to build a more resilient and profitable future. If state nexus questions are part of your planning, review Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?. You are in control.

Frequently Asked Questions

Does a freelancer loss carryforward reduce self-employment tax?

No. An NOL carryforward can reduce income tax, but it does not reduce self-employment tax. Self-employment tax is calculated on the current year's net earnings, so a prior-year loss does not change it.

How do I calculate my NOL as a freelancer?

You do not simply use the negative number from Schedule C. The IRS requires a specific calculation in Publication 536 that starts with your AGI and adds back certain non-business deductions, such as the standard deduction, so the final NOL reflects only business operations.

For how many years can a freelancer carry forward a business loss?

For business losses in tax years 2021 or later, the NOL can generally be carried forward indefinitely until fully used. In any single future year, the deduction is limited to 80% of that year's taxable income.

Can intentionally creating a business loss be a smart tax strategy?

Yes, if it comes from legitimate business spending and is timed strategically. The article frames this as using major investments, such as equipment or marketing, to create an NOL that can offset income in a future higher-income year.

What's the difference between a Net Operating Loss and a capital loss?

An NOL comes from active business operations, while a capital loss comes from selling capital assets like stocks or bonds. An NOL can offset ordinary income, but a capital loss primarily offsets capital gains, with only a small amount, typically $3,000, offsetting ordinary income each year.

Do I need a special form to claim a loss carryforward?

No single dedicated carryforward form is used. In a profitable future year, you report the NOL deduction as a negative number on the "Other income" line of Schedule 1 (Form 1040), and it is wise to attach a brief statement showing how you calculated the amount used.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?

Living abroad does not end `state income tax` exposure by itself. The first decision is practical: choose a filing position your facts can support, then build records that support the same story all year.

A Guide to the Qualified Business Income (QBI) Deduction for Freelancers

**You can classify your Section 199A path in one focused session, then move with confidence instead of guessing.** Treat this as an operating manual for the QBI deduction if you freelance. Classify first, optimize second. That order matters even more when you work across borders, where documentation and residency rules can vary by jurisdiction.